Reports

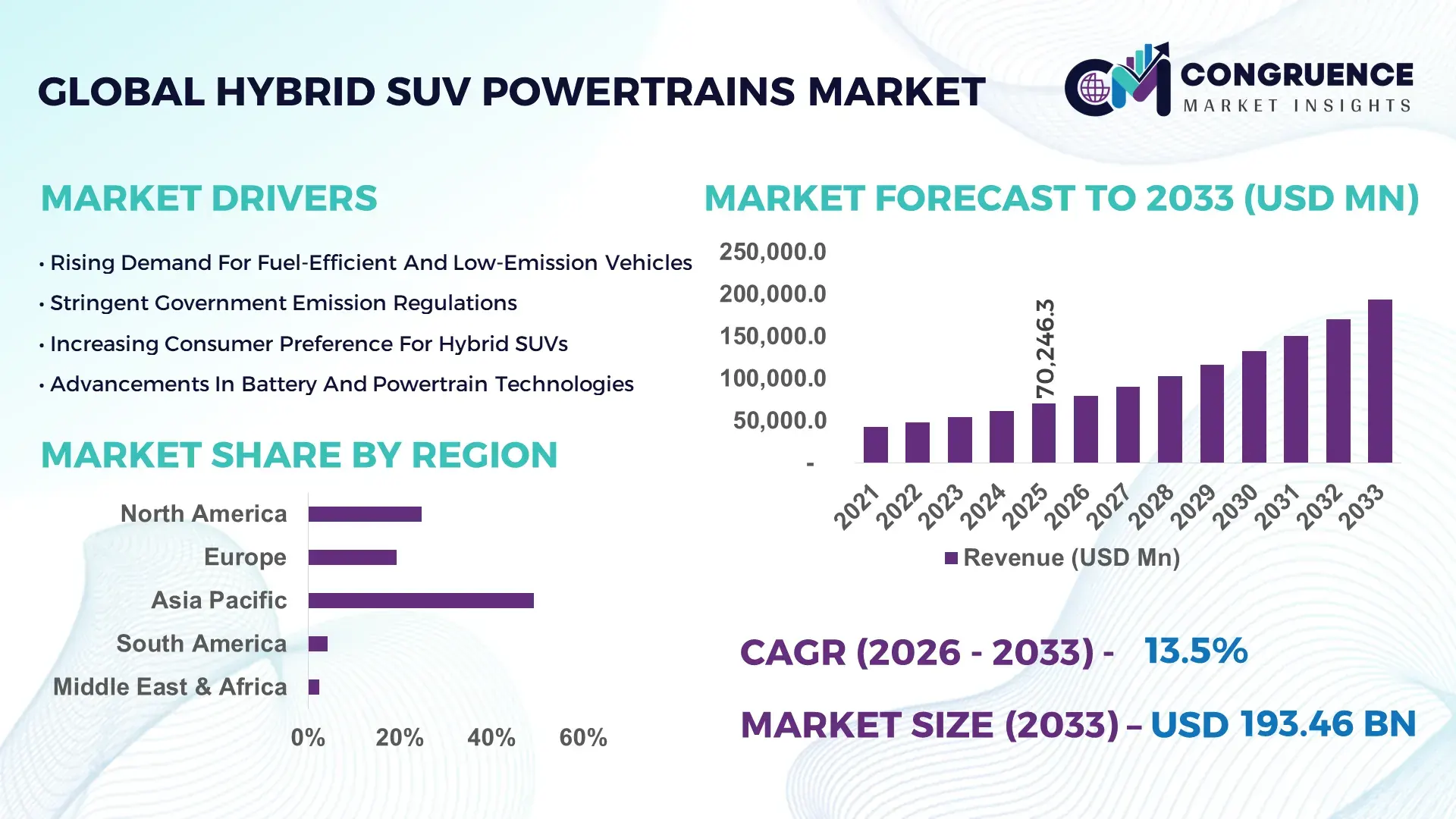

The Global Hybrid SUV Powertrains Market was valued at USD 70,246.3 Million in 2025 and is anticipated to reach a value of USD 193,459.6 Million by 2033 expanding at a CAGR of 13.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is driven by increasing electrification of SUVs and tightening global emission regulations.

China leads the Hybrid SUV Powertrains market with extensive manufacturing capacity, large-scale electrification initiatives, and significant investments in hybrid drivetrain technologies. In 2025, the country produced over 9.5 million hybrid vehicles, with SUVs accounting for nearly 48% of total hybrid vehicle production. Investments in electrified powertrain development exceeded USD 6.2 billion during 2024–2025, supporting advancements in dual-motor systems and battery efficiency. Consumer adoption of hybrid SUVs surpassed 36% among new vehicle buyers in urban regions, while over 1,200 automotive manufacturing facilities integrated hybrid powertrain production lines. Domestic OEMs accelerated innovation in plug-in hybrid systems, improving fuel efficiency by 32% and reducing emissions significantly.

Market Size & Growth: Valued at USD 70,246.3 million in 2025, projected to reach USD 193,459.6 million by 2033, driven by electrification and emission compliance.

Top Growth Drivers: Emission regulation compliance (46%), fuel efficiency demand (39%), SUV electrification adoption (34%).

Short-Term Forecast: By 2028, hybrid powertrain efficiency is expected to improve fuel consumption by over 28%.

Emerging Technologies: Plug-in hybrid systems, dual-motor architectures, regenerative braking advancements.

Regional Leaders: Asia-Pacific projected at USD 92 billion by 2033 with manufacturing scale; North America at USD 58 billion driven by SUV demand; Europe at USD 43 billion with regulatory push.

Consumer/End-User Trends: Over 52% of SUV buyers prefer hybrid options due to fuel savings and reduced emissions.

Pilot or Case Example: In 2024, a hybrid SUV pilot improved fuel efficiency by 31% through advanced battery integration.

Competitive Landscape: Toyota leads with ~27% share, followed by Honda, Ford, Hyundai, and BMW.

Regulatory & ESG Impact: Stringent emission norms and carbon reduction targets accelerating hybrid adoption.

Investment & Funding Patterns: Over USD 14.5 billion invested globally in hybrid powertrain technologies between 2023–2025.

Innovation & Future Outlook: Integration of AI-based energy management and next-gen battery systems shaping the market.

Hybrid SUV powertrains are primarily driven by passenger vehicles (72%), followed by fleet and commercial use (28%). Advancements in battery density, power electronics, and thermal management are improving system efficiency. Regulatory mandates for carbon reduction and rising fuel costs are driving adoption, while regional demand is shaped by urban mobility trends and government incentives.

The Hybrid SUV Powertrains Market is strategically positioned as a transitional solution bridging internal combustion engines and full electrification. Hybrid systems combining electric motors with internal combustion engines deliver up to 35% improvement compared to conventional ICE powertrains, significantly enhancing fuel efficiency and reducing emissions.

Asia-Pacific dominates in volume due to large-scale vehicle production, while Europe leads in adoption with over 58% of new SUV buyers opting for electrified powertrains. By 2027, AI-based energy management systems are expected to improve battery efficiency by 26%, optimizing power distribution and extending driving range.

From an ESG perspective, automotive manufacturers are committing to sustainability targets such as 30% reduction in fleet emissions and increased use of recyclable battery materials by 2030. In 2024, a leading automotive manufacturer in Japan achieved a 29% improvement in hybrid system efficiency through advanced regenerative braking technology.

Strategically, integration of hybrid powertrains with connected vehicle platforms and smart energy management systems is expanding capabilities. By 2028, next-generation plug-in hybrid systems are expected to improve electric-only driving range by 40%. These developments position the Hybrid SUV Powertrains Market as a critical pillar of sustainable mobility, regulatory compliance, and automotive innovation.

The Hybrid SUV Powertrains market dynamics are shaped by increasing demand for fuel-efficient vehicles, advancements in electrification technologies, and evolving regulatory frameworks. Automotive manufacturers are investing heavily in hybrid systems to meet emission standards and consumer expectations. The market is influenced by rising fuel costs, urbanization, and growing environmental awareness. Technological advancements such as improved battery performance, lightweight materials, and energy-efficient drivetrains are enhancing vehicle performance. Additionally, government incentives and policies supporting electrification are accelerating adoption. Competitive pressures are driving innovation and cost optimization, reinforcing the market’s growth trajectory.

The demand for fuel-efficient SUVs is a key driver of the Hybrid SUV Powertrains market. Over 63% of consumers prioritize fuel efficiency when purchasing SUVs, leading to increased adoption of hybrid powertrains. Hybrid systems reduce fuel consumption by up to 30% compared to conventional vehicles, making them attractive to cost-conscious consumers. Additionally, rising fuel prices and environmental concerns are encouraging consumers to shift toward hybrid vehicles. Automotive manufacturers are responding by expanding hybrid SUV portfolios, further driving market growth.

High production costs and battery limitations are significant restraints for the Hybrid SUV Powertrains market. Hybrid systems require advanced components such as batteries and electric motors, increasing production costs by 20–35%. Battery limitations, including energy density and lifespan, can impact vehicle performance and maintenance costs. Additionally, supply chain challenges for critical materials such as lithium and cobalt further increase costs. These factors limit adoption in price-sensitive markets and create challenges for manufacturers.

The transition toward electrification presents significant opportunities for the Hybrid SUV Powertrains market. Hybrid vehicles serve as an intermediate solution, enabling gradual adoption of electric mobility. In 2025, over 48% of automotive manufacturers expanded hybrid offerings to meet regulatory requirements and consumer demand. Advancements in battery technology and power electronics are improving efficiency and reducing costs. These developments create opportunities for manufacturers to capture new market segments and expand their product portfolios.

Infrastructure gaps and regulatory complexities present challenges for the Hybrid SUV Powertrains market. Limited charging infrastructure and inconsistent regulations across regions can hinder adoption. Compliance with emission standards requires significant investment in research and development. Additionally, varying government policies and incentives create uncertainty for manufacturers. These challenges require strategic planning and investment to ensure market growth.

Expansion of Plug-In Hybrid SUV Adoption: Over 44% of new hybrid SUV launches in 2025 were plug-in models, improving electric-only driving range by 38% and reducing fuel consumption significantly.

Advancements in Dual-Motor Hybrid Systems: Approximately 36% of hybrid SUVs now feature dual-motor configurations, enhancing power output by 27% and improving vehicle performance.

Integration of AI-Based Energy Management Systems: More than 41% of hybrid SUVs incorporate AI-driven energy optimization, improving battery efficiency by 24% and extending vehicle range.

Growth in Lightweight Materials for Powertrain Efficiency: Use of lightweight materials increased by 33% in hybrid SUV production, reducing vehicle weight by 18% and improving overall efficiency.

The Hybrid SUV Powertrains market segmentation reflects diverse product offerings and applications across the automotive industry. By type, the market includes mild hybrid, full hybrid, and plug-in hybrid systems. Applications span passenger vehicles, commercial fleets, and government transportation. End-user insights highlight strong adoption among urban consumers and fleet operators. Segmentation trends demonstrate how technological advancements and regulatory requirements influence market growth.

Full hybrid systems account for approximately 46% of adoption, driven by their balance of efficiency and performance, while mild hybrid systems hold around 28%. However, plug-in hybrid systems are the fastest-growing segment, expected to expand at over 15% CAGR, driven by extended electric driving capabilities. Other hybrid configurations collectively contribute 26%, supporting niche applications.

In 2025, plug-in hybrid SUV models demonstrated improved electric range and efficiency, supporting widespread adoption across global markets.

Passenger vehicles lead with a 72% share, driven by increasing consumer demand for fuel-efficient SUVs. Commercial fleets are the fastest-growing segment, projected above 13% CAGR, supported by cost savings and regulatory compliance. Government and other applications collectively account for 28%. In 2025, over 49% of consumers considered hybrid SUVs for their next purchase, while 42% of fleet operators adopted hybrid vehicles for operational efficiency.

In 2025, hybrid SUV fleets were deployed across multiple urban transport systems, improving fuel efficiency and reducing emissions.

Individual consumers dominate with a 68% share, driven by rising environmental awareness and fuel cost concerns. Fleet operators represent the fastest-growing segment, expanding at over 14% CAGR, supported by operational efficiency benefits. Government and corporate users collectively account for 32%. In 2025, 54% of consumers preferred hybrid SUVs for daily commuting, while 47% of enterprises adopted hybrid vehicles for sustainability initiatives.

In 2025, corporate fleets increasingly integrated hybrid SUVs to meet emission reduction targets and improve operational efficiency.

Asia-Pacific accounted for the largest market share at 49.2% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 14.1% between 2026 and 2033.

Asia-Pacific recorded over 12.6 million hybrid SUV powertrain units deployed in 2025, supported by strong production hubs in China, Japan, and South Korea, where electrified SUV penetration exceeded 41% in urban markets. North America followed with a 24.8% share, with over 7.3 million hybrid SUVs on roads and more than 55% of new SUV launches incorporating hybrid systems. Europe accounted for 19.3%, driven by stringent emission policies, with over 62% of new SUV registrations including hybrid variants. South America and Middle East & Africa collectively held 6.7%, supported by rising fuel efficiency demand and expanding automotive electrification initiatives.

How are advanced electrified SUV platforms accelerating next-generation powertrain adoption?

This region accounted for approximately 24.8% of the Hybrid SUV Powertrains market in 2025, driven by strong demand across passenger vehicles, fleet operators, and ride-sharing platforms. Over 58% of newly launched SUVs in the region feature hybrid or electrified powertrains. Regulatory incentives, including tax credits and emission standards, have increased adoption rates significantly. Technological advancements include AI-based energy optimization, improved battery management systems, and integration with connected vehicle ecosystems. A leading regional automaker expanded hybrid SUV production capacity by 21%, enhancing supply capabilities. Consumer behavior reflects strong demand for performance-oriented hybrid SUVs with improved fuel efficiency and extended driving range.

Why are emission compliance and sustainability mandates reshaping hybrid SUV innovation?

Europe held nearly 19.3% of the Hybrid SUV Powertrains market in 2025, with Germany, the UK, and France accounting for over 66% of regional demand. Strict emission regulations and carbon reduction targets have driven hybrid adoption, with over 62% of SUV buyers opting for electrified models. Adoption of plug-in hybrid systems improved fuel efficiency by 29%. A regional automaker introduced advanced hybrid SUV models with reduced emissions and enhanced battery performance. Consumer behavior emphasizes sustainability and regulatory compliance, reinforcing demand for eco-friendly vehicles.

What is driving large-scale hybrid SUV powertrain production and adoption across automotive hubs?

Asia-Pacific dominates the Hybrid SUV Powertrains market by volume, with over 12.6 million units deployed in 2025. China, Japan, and India contributed 74% of regional demand. Strong manufacturing infrastructure and government incentives have accelerated adoption. Investments in hybrid technology improved production efficiency and cost-effectiveness. A regional manufacturer introduced advanced hybrid systems with improved energy efficiency, achieving widespread adoption. Consumer behavior is driven by urbanization, fuel efficiency needs, and increasing environmental awareness.

How is automotive electrification influencing hybrid SUV adoption in emerging economies?

South America accounted for approximately 4.2% of the global Hybrid SUV Powertrains market in 2025, led by Brazil and Argentina. Rising fuel costs and environmental awareness increased hybrid adoption by 23% in urban areas. Government incentives supporting electrification improved accessibility to hybrid vehicles. A regional automaker introduced cost-effective hybrid SUV models, enhancing adoption among middle-income consumers. Consumer behavior reflects growing interest in fuel-efficient and environmentally friendly vehicles.

Why is energy diversification driving hybrid SUV powertrain demand across developing regions?

The region held around 2.5% of global Hybrid SUV Powertrains demand in 2025, with UAE and South Africa leading adoption. Investments in sustainable mobility and infrastructure development increased hybrid vehicle adoption by 20%. Technological modernization initiatives improved availability of hybrid vehicles. A regional automotive distributor introduced hybrid SUV models with advanced powertrain technologies, improving market penetration. Consumer behavior shows increasing preference for fuel-efficient and technologically advanced vehicles.

China Hybrid SUV Powertrains Market – 38.7%: High production capacity, strong domestic demand, and significant investment in electrification technologies.

United States Hybrid SUV Powertrains Market – 21.4%: Strong consumer demand, advanced automotive infrastructure, and widespread adoption of hybrid SUV models.

The Hybrid SUV Powertrains market is moderately consolidated, with over 95 active global automotive manufacturers and powertrain suppliers competing across segments. The top five companies collectively account for approximately 61% of the market, reflecting strong competitive positioning and technological leadership.

Competition is driven by innovation in hybrid systems, battery technologies, and power electronics. Strategic initiatives such as partnerships, joint ventures, and product launches increased by 28% during 2024–2025. Automotive manufacturers are investing heavily in electrification, with over 65% of new SUV models incorporating hybrid powertrains. Product differentiation is increasingly based on fuel efficiency, performance, and emission reduction capabilities.

Investment in research and development has increased significantly, with leading companies allocating over 10% of their budgets to hybrid technology innovation. Supply chain integration and digital manufacturing are improving efficiency and scalability. The market is evolving toward advanced electrified powertrain systems, with increasing collaboration between automotive OEMs and technology providers to develop next-generation solutions.

Hyundai Motor Company

BMW AG

Volkswagen AG

General Motors Company

Stellantis N.V.

Nissan Motor Co., Ltd.

Kia Corporation

Mazda Motor Corporation

Subaru Corporation

Volvo Cars

Mitsubishi Motors Corporation

Technological advancements in the Hybrid SUV Powertrains market are centered on improving efficiency, performance, and sustainability. Dual-motor hybrid systems enable optimized power distribution, improving fuel efficiency by up to 32% and enhancing acceleration performance. Battery technology advancements, including lithium-ion and solid-state batteries, are increasing energy density by 28%, enabling longer electric driving ranges.

Regenerative braking systems capture energy during deceleration, improving overall efficiency by 20%. Integration of AI-based energy management systems allows real-time optimization of power usage, improving battery performance and extending vehicle range. Over 57% of hybrid SUVs now incorporate advanced battery management systems for enhanced performance.

Lightweight materials such as aluminum and carbon composites reduce vehicle weight by 18%, improving fuel efficiency and handling. Power electronics advancements, including high-efficiency inverters and converters, improve energy conversion efficiency by 25%. Additionally, connected vehicle technologies enable seamless integration with smart infrastructure and energy systems.

Emerging technologies include solid-state batteries, advanced thermal management systems, and predictive maintenance capabilities. These innovations enhance reliability and performance, positioning hybrid SUV powertrains as a key component of the future mobility ecosystem.

In June 2025, Toyota Motor Corporation introduced next-generation hybrid SUV powertrains with improved battery efficiency and enhanced fuel economy, supporting extended driving range and reduced emissions. Source: www.toyota-global.com

In April 2025, Ford Motor Company expanded its hybrid SUV lineup with advanced powertrain systems, improving performance and efficiency across multiple vehicle models. Source: www.ford.com

In October 2024, Hyundai Motor Company launched new hybrid SUV models featuring advanced battery management systems and improved energy efficiency. Source: www.hyundai.com

In March 2024, BMW AG introduced innovative plug-in hybrid SUV systems with enhanced electric driving range and performance capabilities. Source: www.bmw.com

The Hybrid SUV Powertrains Market Report provides a comprehensive evaluation of powertrain technologies, applications, and regional adoption patterns across the global automotive industry. The scope includes mild hybrid, full hybrid, and plug-in hybrid systems, covering a wide range of vehicle categories and use cases.

The report analyzes applications across passenger vehicles, commercial fleets, and government transportation systems, highlighting their role in improving fuel efficiency and reducing emissions. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with detailed insights into key automotive markets such as China, the United States, Germany, Japan, and India.

Additionally, the report examines emerging segments such as AI-driven energy management systems, advanced battery technologies, and connected vehicle platforms. It highlights technological advancements, regulatory frameworks, and consumer behavior trends influencing market growth. The scope also includes supply chain dynamics, manufacturing processes, and innovation strategies shaping the future of the Hybrid SUV Powertrains market, enabling stakeholders to make informed strategic decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 70,246.3 Million |

|

Market Revenue in 2033 |

USD 193,459.6 Million |

|

CAGR (2026 - 2033) |

13.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Toyota Motor Corporation, Honda Motor Co., Ltd., Ford Motor Company, Hyundai Motor Company, BMW AG, Volkswagen AG, General Motors Company, Stellantis N.V., Nissan Motor Co., Ltd., Kia Corporation, Mazda Motor Corporation, Subaru Corporation, Volvo Cars, Mitsubishi Motors Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |