Reports

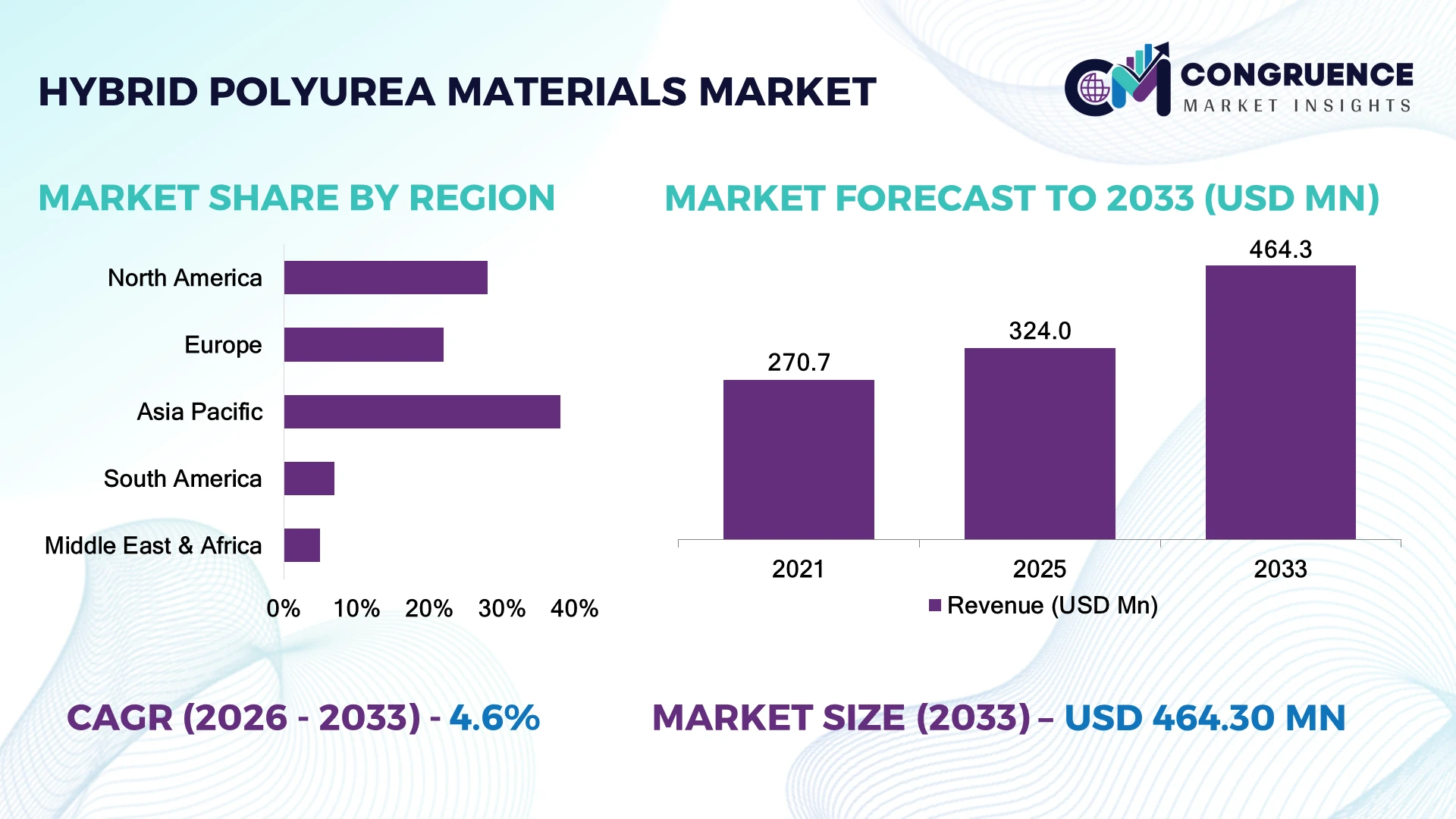

The Global Hybrid Polyurea Materials Market was valued at USD 324.0 Million in 2025 and is anticipated to reach a value of USD 464.3 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. Growth is driven by rising adoption of hybrid polyurea coatings in protective infrastructure, automotive components, industrial flooring, and corrosion-resistant applications due to faster curing, superior durability, and reduced maintenance cycles.

China dominates the market landscape with nearly 35% share, supported by large-scale construction activity, chemical manufacturing capacity, and infrastructure modernization programs under national industrial expansion initiatives. The country has invested billions in urban infrastructure upgrades, while the U.S. maintains strong adoption through defense, transportation, and industrial applications with over 25% of global demand concentration. China’s production capacity exceeds regional competitors, while North American users prioritize advanced protective coating technologies with approximately 30% higher adoption in high-performance applications.

Strategic decisions are increasingly focused on regional manufacturing expansion and technology-driven material optimization.

Market Size & Growth: Valued at USD 324.0 Million in 2025 and reaching USD 464.3 Million by 2033 at a 4.6% CAGR, driven by advanced protective coating adoption across infrastructure and industrial sectors.

Top Growth Drivers: Infrastructure refurbishment (35%), corrosion protection applications (30%), and automotive/transportation coatings (20%) represent major growth contributors.

Short-Term Forecast: By 2028, hybrid polyurea applications achieve 15–20% higher coating efficiency through improved spray systems and optimized formulations.

Emerging Technologies: AI-assisted material formulation, automated spraying systems, and advanced polymer blends are reshaping high-performance coating development.

Regional Leaders: Asia Pacific reaches approximately USD 190 Million by 2033 with construction expansion; North America approaches USD 120 Million through industrial upgrades; Europe exceeds USD 90 Million with sustainability-focused coatings.

Consumer/End-User Trends: Over 60% of industrial users prioritize longer-lasting protective materials to reduce maintenance downtime and lifecycle costs.

Pilot/Case Example: In 2024, infrastructure coating projects using hybrid polyurea systems reported nearly 30% faster application completion compared with conventional protective coatings.

Competitive Landscape: Huntsman, BASF, Covestro, Dow, and PPG lead competition, with top manufacturers collectively controlling around 40% of global supply through formulation expertise and distribution networks.

Regulatory & ESG Impact: Environmental compliance initiatives are increasing demand for low-VOC coating solutions, with sustainable formulations gaining adoption across 25%+ of new industrial coating projects.

Investment & Funding: More than USD 500 Million is directed toward polymer innovation, production expansion, and strategic partnerships as companies strengthen regional supply chains.

Innovation & Future Outlook: Next-generation hybrid polyurea materials emphasize lightweight protection, smart coatings, and automated application technologies to improve industrial performance.

Hybrid polyurea materials are gaining importance across infrastructure, transportation, and industrial protection sectors due to their rapid application capability and enhanced resistance against abrasion, chemicals, and extreme environments. Approximately 40% of new coating developments emphasize improved durability and lower lifecycle maintenance requirements. Global supply-chain restructuring and regional manufacturing investments are accelerating product availability, especially across Asia Pacific and North America. Recent innovations focus on low-emission formulations, automated spraying technologies, and customized protective solutions for demanding operational environments, creating a stronger foundation for strategic expansion.

Hybrid polyurea materials are becoming strategically important as industries seek faster, more durable, and cost-efficient protection solutions for infrastructure, manufacturing facilities, transportation assets, and energy projects. The shift toward infrastructure modernization and stricter environmental standards is encouraging companies to replace traditional coatings with advanced polymer-based systems that deliver improved lifecycle performance.

Compared with conventional epoxy coatings, hybrid polyurea systems provide significantly faster curing times, often reducing application downtime by more than 50%, while offering enhanced resistance against moisture, chemicals, and mechanical stress. North America leads in premium industrial applications driven by aerospace, defense, and energy sectors, whereas Asia Pacific demonstrates larger-scale deployment through construction growth and manufacturing expansion. Europe focuses strongly on sustainable formulations aligned with environmental compliance requirements.

Over the next 2–3 years, companies are prioritizing automated application equipment, regional production facilities, and strategic partnerships to strengthen supply reliability. For example, industrial flooring and pipeline protection projects increasingly use hybrid polyurea coatings to shorten maintenance windows and improve operational continuity. Competitive advantage will depend on formulation innovation, localized supply networks, and the ability to deliver high-performance materials aligned with evolving industrial requirements.

Rising infrastructure rehabilitation and industrial asset protection are accelerating hybrid polyurea adoption, particularly in China, the U.S., and Germany. Demand is strengthened by applications requiring rapid curing, abrasion resistance, and chemical protection, with industrial coating upgrades accounting for nearly 30% of new protective material installations and infrastructure projects representing over 35% of consumption. Global manufacturers are responding by expanding formulation capabilities, improving spray technology partnerships, and developing low-emission solutions. The U.S. infrastructure modernization push and stricter asset durability requirements are increasing preference for hybrid polyurea systems, enabling companies to reduce maintenance cycles and improve long-term operational efficiency.

Hybrid polyurea production remains constrained by fluctuations in isocyanate and resin raw material availability, affecting manufacturing costs and supply consistency. Price volatility in key chemical inputs has influenced approximately 15–20% variation in production expenses, while dependence on specialized suppliers limits flexibility for smaller manufacturers. China’s dominance in chemical production creates both supply advantages and concentration risks during periods of trade disruption or logistics constraints. Companies are mitigating exposure through supplier diversification, regional sourcing agreements, and expanded inventory planning. The strategic challenge is maintaining competitive pricing while preserving advanced formulation quality and consistent product performance across industrial applications.

New opportunities are emerging through smart protective coatings, automated application systems, and expansion into energy, transportation, and marine infrastructure sectors. Automated spraying technologies can improve application productivity by approximately 25–40%, while advanced formulations are increasing demand for lightweight and durable protection solutions. India’s infrastructure development programs and expanding manufacturing base are creating additional opportunities for hybrid polyurea deployment in industrial facilities and transportation projects. Companies are investing in R&D partnerships, customized formulations, and digital application monitoring platforms. A key strategic opportunity lies in combining hybrid polyurea with sensor-enabled coating technologies to enable predictive maintenance and reduce lifecycle costs.

Scaling hybrid polyurea deployment requires skilled application teams, specialized equipment, and consistent quality control across diverse industrial environments. Approximately 20–30% of project delays are linked to installation complexity, surface preparation requirements, and limited technical expertise. Emerging markets often face shortages of trained applicators and inadequate coating infrastructure, affecting adoption consistency. Companies are addressing these barriers through certification programs, contractor partnerships, and automated equipment investments. Long-term competitiveness depends on improving application reliability, developing easier-to-deploy formulations, and ensuring technical support networks can meet rising demand from infrastructure, energy, and industrial sectors.

Automated Coating Deployment Growth Industrial users are accelerating automated spray application systems, with adoption rising by nearly 25% in large-scale coating projects to improve consistency and reduce labor dependency. U.S. infrastructure contractors and Chinese manufacturing facilities are integrating robotic application tools to achieve 30% faster project completion. Companies are responding through equipment partnerships and digital workflow integration, creating more predictable coating performance and reducing operational downtime.

Low-Emission Formulation Shift Environmental compliance requirements are reshaping product development, with approximately 35% of new hybrid polyurea formulations emphasizing reduced VOC characteristics and improved sustainability profiles. European manufacturers are prioritizing compliant materials as regulatory frameworks tighten, while suppliers restructure chemical processes to support greener production. A non-obvious shift is the growing preference for durable coatings that reduce replacement frequency rather than focusing only on initial material costs.

Localized Supply Chain Expansion Chemical manufacturers are increasing regional production capacity as supply-chain disruptions highlight dependency risks. Nearly 20% of producers have expanded local sourcing strategies for critical resins and additives, particularly across China, India, and North America. Companies are establishing supplier networks and inventory buffers to improve delivery reliability, protect margins, and support faster project execution for industrial customers.

Smart Material Integration Advances Hybrid polyurea development is moving toward intelligent coating systems incorporating monitoring capabilities and advanced polymer engineering. Around 15% of premium industrial coating projects now evaluate sensor-enabled or performance-tracking solutions. Energy and transportation operators are adopting these technologies to improve asset visibility, while companies are investing in R&D collaborations to create predictive maintenance-oriented coating platforms.

Hybrid polyurea coatings represent the leading type segment, accounting for approximately 55% of market adoption due to their balanced performance, rapid curing capability, and compatibility with industrial protection requirements. Their dominance is supported by widespread use in infrastructure, transportation, and manufacturing applications where durability and reduced maintenance cycles are critical. Pure polyurea alternatives maintain relevance in high-performance applications, while other blended formulations capture niche requirements. Hybrid formulations have gained nearly 20% higher preference among industrial users seeking easier application and improved surface compatibility. The fastest-growing type category is advanced modified hybrid polyurea, driven by demand for enhanced chemical resistance, sustainability improvements, and customized industrial performance. Manufacturers are increasing investment in polymer research, application partnerships, and regional production capabilities to address evolving customer specifications. Companies are shifting product portfolios toward specialized formulations that improve lifecycle value rather than competing only on material pricing.

Infrastructure protection is the leading application segment, representing nearly 40% of hybrid polyurea consumption due to demand from bridges, pipelines, commercial structures, and industrial facilities. Its dominance comes from the material’s ability to provide waterproofing, corrosion resistance, and rapid application advantages in complex environments. Industrial flooring and transportation applications collectively contribute around 35% of demand, supported by manufacturing expansion and asset protection requirements. The fastest-growing application area is energy infrastructure, where hybrid polyurea adoption is increasing due to renewable energy facilities, storage systems, and pipeline protection requirements. Deployment in these applications is expanding by approximately 25% as operators prioritize longer asset lifecycles and reduced maintenance interruptions. Companies are responding through specialized coating solutions, contractor networks, and application technology improvements. Marine and automotive applications continue developing through lightweight protection needs and advanced material integration strategies.

Industrial manufacturers and infrastructure operators represent the leading end-user segment with approximately 45% market share, driven by extensive requirements for corrosion protection, equipment preservation, and facility maintenance. Large industrial facilities in China, the U.S., and Germany increasingly adopt hybrid polyurea systems to minimize downtime and extend asset service periods. Commercial construction users account for nearly 25% of demand as developers prioritize waterproofing and long-term structural protection. The fastest-growing end-user group is the energy sector, expanding through investments in renewable installations, storage infrastructure, and pipeline networks. Adoption among energy companies is increasing by more than 20% as operators seek materials capable of handling harsh environments. Companies are targeting this segment through customized solutions, technical partnerships, and application support programs. Government infrastructure projects and transportation operators remain strategically important, creating opportunities for suppliers that combine material innovation with reliable deployment capabilities.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America represents approximately 28% of the global hybrid polyurea materials market, supported by strong demand from infrastructure rehabilitation, defense, transportation, energy, and industrial flooring applications. The United States contributes the majority of regional consumption due to extensive infrastructure maintenance requirements and advanced coating technology adoption. More than 35% of industrial coating projects in the region prioritize high-durability materials that reduce maintenance frequency. Manufacturers are strengthening regional supply networks, expanding formulation capabilities, and partnering with application specialists to improve deployment efficiency across commercial and industrial projects.

United States Market Outlook: The United States remains the leading North American market due to its large industrial base, infrastructure modernization programs, and advanced manufacturing ecosystem. Demand is concentrated in pipeline protection, aerospace facilities, warehouses, and transportation infrastructure. Over 40% of premium protective coating applications in critical industrial sectors emphasize rapid-curing and long-life solutions, encouraging companies to invest in localized production capacity and specialized coating technologies.

Europe accounts for nearly 22% of the global hybrid polyurea materials market, driven by infrastructure renovation, industrial modernization, and increasing preference for sustainable protective materials. Germany, France, and the United Kingdom represent key adoption centers due to strong manufacturing capabilities and environmental compliance requirements. Nearly 30% of new industrial coating developments in Europe focus on reduced environmental impact and improved lifecycle performance. Companies are adapting through low-emission formulation development, technology partnerships, and investments in advanced polymer systems to meet evolving industrial standards.

Germany Market Outlook: Germany leads European adoption through its advanced automotive, chemical, manufacturing, and industrial infrastructure sectors. The country’s strong engineering ecosystem supports the use of high-performance protective coatings in factories and heavy industries. More than 25% of industrial facilities implementing modernization programs are incorporating advanced coating technologies to improve equipment durability, operational efficiency, and maintenance planning.

Asia-Pacific holds the largest market position with approximately 38% share, supported by extensive construction activity, manufacturing expansion, and growing industrial asset protection requirements. China, Japan, South Korea, and India are major contributors, with China accounting for the highest production and consumption capacity. More than 45% of regional demand comes from construction, transportation, and industrial applications. Manufacturers are expanding production facilities, improving supply-chain localization, and developing customized formulations to support large-scale infrastructure projects and export opportunities.

China Market Outlook: China dominates the Asia-Pacific market due to its extensive chemical manufacturing capacity, infrastructure development programs, and large industrial base. The country contributes more than one-third of global hybrid polyurea consumption through construction, transportation, and manufacturing applications. Increasing investments in urban infrastructure and industrial modernization are encouraging producers to expand advanced polymer coating capabilities and strengthen domestic supply networks.

South America represents around 7% of the global hybrid polyurea materials market, with demand concentrated in Brazil, Argentina, and Chile. Growth is supported by mining, oil and gas infrastructure, commercial construction, and water management projects requiring corrosion-resistant protective materials. Approximately 20% of industrial facilities in key markets are shifting toward longer-lasting coating solutions to reduce maintenance interruptions. Companies are strengthening distributor networks, forming regional partnerships, and improving technical support capabilities to overcome application expertise limitations and expand industrial adoption.

Brazil Market Outlook: Brazil is the largest South American market due to its mining, energy, agriculture infrastructure, and industrial processing sectors. The country’s extensive pipeline and industrial asset network creates strong demand for protective coating technologies. More than 15% of large industrial maintenance projects are adopting advanced coating solutions to improve asset durability and reduce operational disruptions.

Middle East & Africa accounts for approximately 5% of the global hybrid polyurea materials market, supported by oil and gas infrastructure, water management projects, commercial construction, and large-scale urban development initiatives. Countries including Saudi Arabia, the UAE, and South Africa are increasing adoption of advanced protective coatings for extreme climate conditions and industrial assets. Infrastructure projects in the Gulf region are driving demand for fast-installation and high-durability materials, with more than 20% of new industrial protection projects evaluating advanced polymer coatings. Companies are expanding partnerships and establishing regional service networks to support project execution.

Saudi Arabia Market Outlook: Saudi Arabia represents the most strategically significant market in the region due to major infrastructure investments, energy-sector modernization, and industrial diversification initiatives. The country’s large-scale construction and energy projects are increasing demand for durable protective materials. More than 30% of major infrastructure developments incorporate advanced corrosion and waterproofing solutions, creating opportunities for suppliers focused on high-performance hybrid polyurea systems.

The Hybrid Polyurea Materials Market features competition between global chemical manufacturers, specialty coating suppliers, and regional formulation companies. Leading players such as Huntsman, BASF, Covestro, Dow, and PPG compete against specialized coating providers including Nukote and Specialty Products Inc. Global suppliers compete through technology leadership, while regional players focus on customization, pricing, and application support. The top five companies collectively account for approximately 40–45% of market supply. Competition is driven by formulation performance, raw material control, application speed, and customer-specific solutions, with advanced products improving durability by 20–30% over conventional coatings. Companies are expanding through partnerships, localized production, and sustainable material development. The competitive landscape is shifting toward low-emission formulations, circular materials, and supply-chain localization. High technical expertise and formulation know-how remain major entry barriers. Winning requires combining innovation, reliable supply networks, and application-focused customer solutions.

BASF SE

Covestro AG

Dow Inc.

PPG Industries Inc.

The Sherwin-Williams Company

Specialty Products Inc.

Nukote Coating Systems International

Rhino Linings Corporation

Wasser Corporation

Kukdo Chemical Co., Ltd.

Carboline Company

Versaflex Inc.

Armorthane Inc.

Hybrid polyurea technology is advancing through improved polymer chemistry, automated application systems, and sustainable formulation development. New-generation hybrid formulations deliver enhanced abrasion resistance, faster curing, and improved substrate adhesion, providing approximately 20–30% longer service performance compared with traditional epoxy-based protective coatings. Manufacturers are integrating advanced additives and modified resin systems to improve chemical resistance and temperature stability.

Automation is becoming a competitive differentiator, with robotic spray systems and digital monitoring platforms improving coating consistency by nearly 25% while reducing labor dependency. Large industrial operators in North America and Asia are increasing deployment of automated coating workflows to improve project speed and quality control. Companies benefiting most are those combining material innovation with application technology partnerships.

Between 2026 and 2028, smart coating integration, low-emission chemistry, and circular material development will shape competitive positioning. Sustainable hybrid polyurea systems incorporating recycled or bio-based components are gaining attention, with adoption increasing across environmentally regulated industries. Companies acting early on advanced formulations, automation capabilities, and localized technology support will secure stronger operational advantages.

March 2025 Huntsman Corporation introduced its POLYRESYST® S4010C coating system containing up to 20% circular content for protective coating applications, improving sustainability while maintaining performance. The launch strengthened Huntsman’s position in advanced coating innovation and circular material development. Source: www.huntsman.com

July 2025 Covestro AG partnered with CSIR-National Chemical Laboratory in India to develop polyurethane waste upcycling solutions. The initiative targets improved recycling pathways and supports circular material strategies, strengthening Covestro’s sustainability-focused innovation pipeline. Source: www.covestro.com

2024 PPG Industries Inc. expanded industrial coating capabilities with advanced polyurea flooring solutions designed for abrasion resistance, UV stability, and cold-temperature application performance. The product supports industrial users seeking durable flooring systems with improved operational reliability. Source: www.ppg.com

2025 Covestro AG advanced automotive coating innovation through integrated Direct Coating technology, combining molding and coating processes to reduce production complexity and energy usage. The approach improves manufacturing efficiency and supports next-generation mobility applications.

The Hybrid Polyurea Materials Market Report provides comprehensive coverage across product types, applications, end-users, regional markets, and competitive strategies shaping industry development. The analysis evaluates hybrid formulations, protective coatings, infrastructure applications, industrial usage, transportation requirements, and emerging sectors adopting advanced polymer technologies. Regional assessment covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with country-level insights on manufacturing strength, deployment trends, and investment activity.

The report examines technology advancements including sustainable formulations, automated application systems, advanced additives, and next-generation coating solutions. It evaluates participation from global manufacturers, specialty suppliers, and regional innovators, highlighting strategic opportunities, competitive positioning, supply-chain dynamics, and expansion priorities. The study supports investment planning and business decisions by identifying adoption patterns, emerging demand areas, and market direction through 2026–2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 324.0 Million |

| Market Revenue (2033) | USD 464.3 Million |

| CAGR (2026–2033) | 4.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Huntsman Corporation; BASF SE; Covestro AG; Dow Inc.; PPG Industries Inc.; The Sherwin-Williams Company; Specialty Products Inc.; Nukote Coating Systems International; Rhino Linings Corporation; Wasser Corporation; Kukdo Chemical Co., Ltd.; Carboline Company; Versaflex Inc.; Armorthane Inc. |

| Customization & Pricing | Available on Request (10% Customization Free) |