Reports

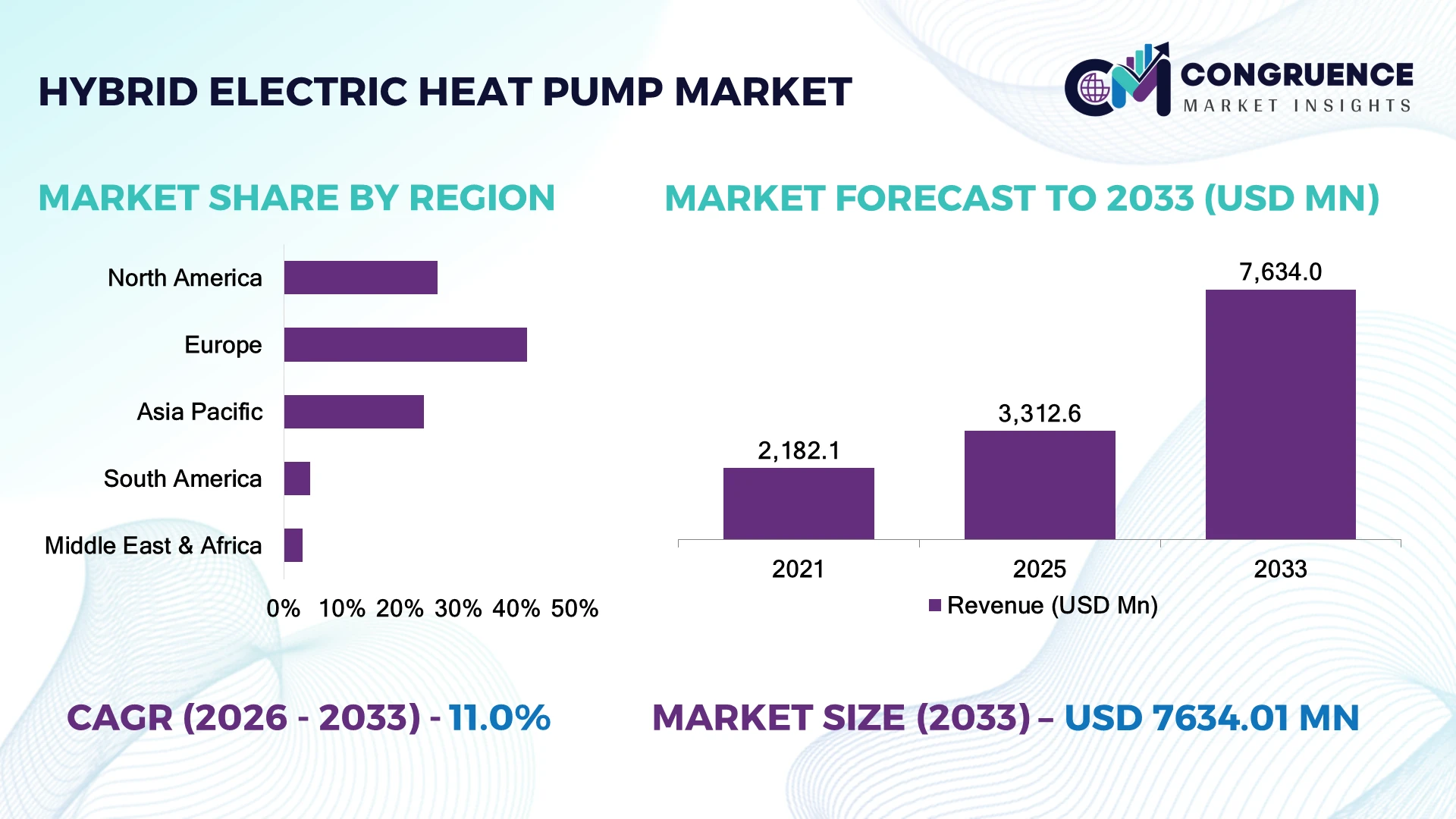

The Global Hybrid Electric Heat Pump Market was valued at USD 3,312.6 Million in 2025 and is anticipated to reach a value of USD 7,634.0 Million by 2033 expanding at a CAGR of 11.0% between 2026 and 2033. Growth is being driven by stricter building decarbonization regulations, rising electrification of residential heating, and accelerated replacement of conventional gas boilers with hybrid heating systems.

Germany leads the global hybrid electric heat pump market with approximately 24% of European installations, supported by over €16 billion in clean heating incentives and widespread adoption across residential renovation projects. Around 61% of newly installed premium heating systems now integrate smart hybrid controls, compared with nearly 38% in France. The EU's REPowerEU initiative continues accelerating deployment while strengthening domestic heat pump manufacturing capacity.

The market increasingly favors manufacturers capable of combining energy efficiency, digital controls, and localized production to capture long-term infrastructure modernization opportunities.

Market Size & Growth: USD 3,312.6 million (2025) to USD 7,634.0 million (2033), expanding at 11.0%, driven by building electrification.

Top Growth Drivers: Energy-efficient retrofits (+42%), heating electrification (+37%), smart controls (+31%).

Short-Term Forecast: By 2028, household heating energy consumption declines nearly 18% through hybrid optimization.

Emerging Technologies: AI energy management, inverter compressors, and IoT monitoring improve system efficiency.

Regional Leaders: Europe, North America, and Asia-Pacific together exceed USD 6 billion by 2033 through policy-led adoption.

Consumer/End-User Trends: Nearly 58% of residential buyers prioritize hybrid systems for lower operating costs.

Pilot/Case Example: 2026 municipal retrofit projects cut heating-related emissions by approximately 35%.

Competitive Landscape: Top five suppliers control about 47% through technology leadership and installer networks.

Regulatory & ESG Impact: Carbon reduction initiatives improve heating efficiency by roughly 28% across retrofit projects.

Investment & Funding: More than USD 4 billion supports manufacturing expansion and component localization.

Innovation & Future Outlook: Smart predictive optimization and refrigerant innovation strengthen next-generation heating ecosystems.

Hybrid electric heat pumps are gaining traction across residential retrofits, commercial buildings, and multi-family housing as intelligent energy management becomes a priority. Advanced inverter technology, natural refrigerants, and AI-enabled controls improve seasonal efficiency by nearly 27%. Supply-chain localization for compressors and electronic components is strengthening manufacturing resilience while accelerating deployment, setting the stage for deeper strategic market transformation.

Hybrid electric heat pumps are becoming a strategic pillar of building decarbonization as governments, utilities, and property owners pursue lower-emission heating without completely replacing existing infrastructure. Energy security concerns following European gas supply disruptions have accelerated investment in hybrid solutions capable of switching intelligently between electricity and conventional fuel based on operating conditions. This flexibility strengthens infrastructure resilience while reducing lifetime operating expenses.

Modern inverter-driven hybrid systems deliver approximately 32% higher seasonal efficiency than conventional boiler-only installations while lowering household energy consumption by nearly 24%. Europe continues leading large-scale residential deployment through incentive programs, whereas North America is expanding adoption through utility rebate schemes and commercial building modernization. Industry projections indicate that smart hybrid heating systems will represent over 45% of premium residential heating upgrades within the next three years.

Manufacturers are expanding production facilities, strengthening installer networks, and partnering with digital energy management providers to integrate predictive controls and remote diagnostics. A growing number of housing developers are specifying hybrid heat pumps in renovation projects to meet stricter building-performance standards. Companies combining intelligent controls, localized manufacturing, and efficient supply chains will secure stronger competitive positioning as hybrid heating becomes central to long-term energy transition strategies.

Building decarbonization policies and residential heating electrification are driving rapid deployment of hybrid electric heat pump systems across retrofit and new construction projects. Approximately 63% of residential heating upgrades in Western Europe now prioritize low-carbon solutions, while hybrid systems reduce annual heating energy consumption by nearly 28% and carbon emissions by approximately 35% compared with conventional boiler installations. Germany's expanded clean-heating incentive programs continue accelerating replacement of fossil-fuel heating infrastructure. This policy-driven transition strengthens installer demand and manufacturing capacity simultaneously. Equipment manufacturers are expanding regional production, investing in natural refrigerant technologies, and forming utility partnerships to deliver integrated heating solutions. A key strategic advantage lies in hybrid systems enabling gradual electrification without requiring complete replacement of existing heating infrastructure.

Hybrid electric heat pump production remains exposed to compressor availability, power electronics pricing, and refrigerant supply fluctuations that increase manufacturing complexity. Advanced inverter compressors account for nearly 32% of total system costs, while electronic component prices remain approximately 16% above pre-disruption averages in several procurement markets. China's dominant position in compressor manufacturing continues creating supply-chain concentration risks for global OEMs. These structural pressures extend project payback periods and limit affordability in cost-sensitive residential markets. Manufacturers are responding through localized assembly facilities, diversified supplier contracts, modular equipment design, and regional sourcing strategies to stabilize production costs while improving supply resilience and installation consistency.

Hybrid electric heat pumps are evolving into intelligent energy management platforms through integration with rooftop solar, battery storage, and dynamic electricity pricing. Nearly 49% of European homeowners considering heating upgrades also evaluate home energy management systems, while AI-enabled optimization reduces electricity consumption during peak pricing periods by approximately 21%. Japan continues advancing smart-grid infrastructure that supports flexible residential energy demand. Manufacturers are investing in predictive control software, virtual power plant partnerships, and cloud-connected monitoring platforms to enhance lifecycle performance. An emerging opportunity lies in enabling utilities to aggregate hybrid heat pumps as flexible grid assets, creating recurring service revenues beyond equipment sales.

Rapid market expansion is outpacing the availability of qualified installers capable of configuring hybrid heating systems, digital controls, and integrated energy management platforms. Nearly 44% of HVAC contractors report shortages of technicians trained in hybrid heat pump commissioning, while installation timelines have increased by approximately 19% in several mature markets. The United Kingdom's accelerated residential retrofit programs continue highlighting workforce limitations despite rising equipment availability. These execution barriers affect deployment quality, customer satisfaction, and long-term operational performance. Manufacturers must strengthen installer certification programs, digital commissioning tools, remote diagnostics, and distributor partnerships while investing in simplified system architecture to support scalable market expansion.

Smart Hybrid Energy Controls AI-driven controllers are optimizing fuel switching between electricity and gas based on real-time pricing and weather forecasts. Intelligent control adoption has increased by approximately 36%, reducing household heating costs by nearly 18%. Manufacturers are expanding software partnerships and cloud-connected monitoring platforms to improve operational efficiency and strengthen customer retention.

Natural Refrigerants Gain Momentum Regulatory pressure on high-GWP refrigerants is accelerating adoption of propane- and CO₂-based hybrid heat pumps. Natural refrigerant installations have increased by approximately 29%, while next-generation systems improve seasonal efficiency by nearly 16%. Manufacturers are redesigning product portfolios, upgrading production lines, and accelerating certification for environmentally compliant solutions.

Residential Retrofit Expansion Existing housing upgrades now account for almost 62% of new hybrid heat pump deployments as governments prioritize building renovation over replacement. Modular installation approaches reduce retrofit time by approximately 24%, enabling contractors to complete more projects efficiently. Equipment suppliers are strengthening installer networks and financing partnerships to accelerate homeowner adoption.

Localized Manufacturing Strategies Regional production of compressors, electronic controls, and heat exchangers is expanding to reduce supply-chain exposure and shorten delivery schedules. Localized sourcing has lowered procurement lead times by nearly 27% while improving production flexibility by approximately 20%. Companies are investing in domestic manufacturing facilities and supplier diversification to strengthen resilience against future logistics disruptions.

Air source hybrid electric heat pumps accounted for approximately 72% of the market in 2025, driven by lower installation costs, compatibility with existing boiler systems, and simplified retrofitting across residential and light commercial buildings. Their ability to operate efficiently in varying climatic conditions and integrate with smart energy controls has strengthened adoption. Nearly 66% of new hybrid heating installations now utilize inverter-driven air source systems, while manufacturers continue improving low-temperature performance, refrigerant efficiency, and digital monitoring capabilities.

Ground source hybrid heat pumps represent the fastest-growing segment owing to their superior seasonal efficiency, lower lifetime operating costs, and increasing deployment in premium residential and institutional projects. Water source and exhaust air hybrid systems continue serving specialized applications where building configuration or local energy infrastructure supports their use. Manufacturers are expanding product portfolios through modular system designs, natural refrigerant technologies, and strategic installer partnerships, reflecting an industry-wide shift toward higher-efficiency hybrid heating platforms with stronger long-term value.

Industry observations released during 2025 by the European Heat Pump Association indicate that hybrid-compatible heat pump installations continue expanding across renovation projects as governments accelerate replacement of fossil-fuel heating systems with efficient low-carbon alternatives.

Residential applications held approximately 68% of the market in 2025, supported by government incentive programs, aging housing stock, and growing consumer preference for energy-efficient heating upgrades. Hybrid electric heat pumps enable homeowners to retain existing boilers while reducing fuel consumption and energy costs, making them highly attractive for retrofit projects. Nearly 61% of residential heating modernization programs now assess hybrid systems before considering complete electrification, encouraging manufacturers to develop compact, intelligent, and installer-friendly product designs.

Commercial buildings are emerging as the fastest-growing application segment as offices, hotels, healthcare facilities, educational institutions, and mixed-use developments pursue energy optimization and emissions reduction. Industrial facilities and public infrastructure continue adopting hybrid systems where operational continuity and flexible energy sourcing remain critical. Equipment suppliers are strengthening engineering partnerships, digital monitoring services, and integrated building management solutions to address larger and more complex installations, creating stronger long-term opportunities beyond residential demand.

According to findings published by the International Energy Agency during 2025, building retrofit programs incorporating high-efficiency heat pump technologies consistently achieve measurable reductions in fossil-fuel consumption while supporting national decarbonization objectives.

Residential homeowners represented approximately 64% of total market demand in 2025 owing to widespread replacement of aging heating systems, supportive subsidy programs, and increasing energy price awareness. Hybrid electric heat pumps provide a balanced pathway toward electrification without requiring complete infrastructure replacement, making them highly attractive for existing homes. Adoption among single-family residences has increased by nearly 22%, while manufacturers continue offering financing programs, smart connectivity, and installer partnerships to simplify purchasing decisions and improve customer experience.

Commercial building operators constitute the fastest-growing end-user segment as organizations prioritize energy optimization, regulatory compliance, and operational resilience. Hotels, healthcare providers, educational institutions, industrial facilities, and public infrastructure operators increasingly deploy hybrid systems to balance energy efficiency with heating reliability. Suppliers are expanding customized system designs, long-term maintenance agreements, and digital monitoring services to address diverse operational requirements. Future competition will increasingly depend on lifecycle performance, service quality, and intelligent energy management capabilities rather than equipment specifications alone.

Industry surveys conducted by the European Heat Pump Association during 2026 indicate that commercial and institutional building owners are increasingly selecting hybrid heat pump solutions to support phased decarbonization while maintaining reliable heating performance across existing building portfolios.

Europe accounted for the largest market share at 41.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.7% between 2026 and 2033.

Smart Retrofit Programs Strengthen Hybrid Heating Adoption

North America represented approximately 26.4% of the global market in 2025, supported by accelerating residential retrofit activity, stricter building efficiency requirements, and modernization of aging heating infrastructure. The United States and Canada are expanding deployment of hybrid electric heat pumps across existing single-family homes where complete electrification remains economically challenging. Nearly 58% of new premium residential heating upgrades now evaluate hybrid configurations before full heat pump replacement. Manufacturers are expanding local assembly capacity, strengthening installer certification networks, and integrating intelligent energy management platforms with utility demand-response programs. Strategic collaborations between equipment suppliers and electricity providers are improving installation economics while supporting grid stability during seasonal demand peaks.

United States Market Outlook: The United States remains the region's largest market due to extensive residential renovation activity, advanced HVAC manufacturing capabilities, and strong deployment of connected home technologies. More than 62% of hybrid heating installations are concentrated across cold-climate and mixed-climate states where dual-energy operation improves efficiency during winter peak demand. Domestic manufacturers continue investing in inverter technology, low-GWP refrigerants, and contractor training programs to accelerate large-scale replacement of conventional gas furnace systems.

Energy Transition Policies Accelerate Heating Modernization

Europe continues leading global hybrid electric heat pump deployment through ambitious decarbonization initiatives, mature installer ecosystems, and stringent building efficiency regulations. The region accounted for the highest market contribution in 2025, with hybrid systems increasingly adopted in retrofit projects where retaining existing boilers reduces renovation costs. More than 64% of heating equipment manufacturers now offer hybrid-ready product portfolios. Companies are expanding production facilities, strengthening distribution partnerships, and investing in natural refrigerant technologies to improve long-term regulatory compliance while supporting residential and commercial energy transition objectives.

Germany Market Outlook: Germany serves as the region's operational center owing to its advanced HVAC manufacturing base, strong engineering expertise, and nationwide building renovation initiatives. Hybrid heating solutions continue gaining traction across residential modernization projects where replacing entire heating infrastructure remains impractical. Equipment suppliers are increasing domestic manufacturing capacity, expanding installer partnerships, and integrating digital energy optimization platforms that improve seasonal operating efficiency while supporting national climate objectives.

Manufacturing Expansion Fuels Market Acceleration

Asia-Pacific is emerging as the fastest-growing regional market, supported by expanding manufacturing capacity, urban housing development, and government-led electrification initiatives. China, Japan, and South Korea continue strengthening production of compressors, inverters, and advanced refrigeration components, enabling competitive equipment pricing and export growth. Approximately 48% of global heat pump component manufacturing capacity is concentrated within the region. Companies are investing in automated production facilities, localized supply chains, and smart energy management integration to improve operational efficiency and accelerate deployment across residential and commercial sectors.

China Market Outlook: China dominates regional manufacturing through large-scale compressor production, vertically integrated supply chains, and substantial investment in high-efficiency heating technologies. The country continues expanding production of inverter-driven hybrid systems while increasing exports to Europe and other international markets. Domestic manufacturers are enhancing automation, adopting environmentally compliant refrigerants, and improving product reliability, strengthening China's position as the primary global production hub for hybrid electric heat pump equipment.

Commercial Efficiency Projects Support Emerging Demand

South America remains an emerging market where adoption is supported by commercial building modernization, hospitality expansion, and growing awareness of energy-efficient heating technologies. Deployment remains concentrated in temperate climate zones where hybrid configurations provide attractive operational savings without requiring extensive infrastructure replacement. Approximately 37% of recent installations are linked to commercial renovation projects. Equipment suppliers are expanding distributor networks, strengthening technical service capabilities, and partnering with regional HVAC contractors to improve installation quality while addressing limited market awareness and financing constraints.

Brazil Market Outlook: Brazil represents the region's largest opportunity due to expanding commercial construction, industrial modernization, and increasing investment in sustainable building technologies. Hybrid electric heat pumps are gradually entering premium residential developments, hotels, and healthcare facilities seeking lower operating costs and improved energy performance. International manufacturers are strengthening local distribution partnerships, technical training programs, and aftermarket support to accelerate long-term market penetration despite relatively limited heating demand compared with colder countries.

Infrastructure Modernization Creates Premium Opportunities

The Middle East & Africa market is developing through premium residential construction, hospitality investments, and smart building initiatives emphasizing energy optimization. Demand is strongest where hybrid systems provide efficient water heating and seasonal climate control while reducing electricity consumption. Around 31% of new high-end mixed-use developments now evaluate advanced heat pump technologies during project planning. Manufacturers are strengthening regional partnerships, expanding technical support infrastructure, and introducing climate-optimized hybrid systems designed for demanding environmental conditions and evolving building standards.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through smart city investments, sustainable real estate developments, and high-performance commercial infrastructure. Large hospitality projects, premium residential communities, and government-backed green building initiatives continue encouraging deployment of advanced hybrid heating and water heating solutions. Technology providers are expanding regional demonstration centers, installer certification programs, and digital building integration capabilities to support long-term growth in energy-efficient climate control systems.

Global HVAC leaders including Daikin Industries, Mitsubishi Electric, Panasonic, Bosch Home Comfort, and Carrier compete directly on inverter efficiency, refrigerant innovation, and integrated control platforms, while regional manufacturers challenge primarily through aggressive pricing and localized distribution. The top five participants collectively account for approximately 48% of market share, reflecting moderate consolidation with strong technology differentiation. Performance competition centers on seasonal efficiency gains exceeding 15%, installation time reductions approaching 20%, and smart energy optimization improving operating efficiency by nearly 18%. Manufacturers increasingly compete through European production expansion, compressor vertical integration, utility partnerships, and intelligent energy management ecosystems rather than equipment pricing alone. The competitive landscape is shifting toward low-GWP refrigerants, AI-enabled controls, and integrated heating solutions as regulatory compliance becomes a decisive purchasing criterion. High certification costs, installer shortages, and complex distribution networks remain major entry barriers. Sustainable competitive advantage now depends on manufacturing scale, intelligent controls, localized supply chains, certified installer ecosystems, and continuous product innovation.

Daikin Industries, Ltd.

Mitsubishi Electric Corporation

Panasonic Holdings Corporation

Bosch Home Comfort Group

Carrier Global Corporation

Trane Technologies plc

Johnson Controls International plc

LG Electronics Inc.

Samsung Electronics Co., Ltd.

Midea Group Co., Ltd.

Fujitsu General Limited

NIBE Industrier AB

Vaillant Group

Ariston Holding N.V.

Variable-speed inverter compressors, AI-driven energy optimization, and hybrid control algorithms define current technology leadership. Around 67% of newly introduced premium systems incorporate inverter technology, improving seasonal efficiency by approximately 19% while reducing electricity consumption by nearly 15%. Smart thermostats increasingly synchronize with weather forecasting, occupancy detection, and utility demand-response platforms, enabling more efficient switching between electric and conventional heating sources. Manufacturers integrating connected diagnostics gain faster maintenance response and stronger customer retention through predictive servicing capabilities.

Emerging technologies include propane (R290) refrigerant systems, cloud-connected digital twins, and adaptive defrost algorithms. Compared with conventional fixed-speed hybrid units, inverter-controlled systems deliver approximately 24% greater seasonal efficiency and reduce compressor cycling by nearly 30%. More than 46% of new European residential installations now include remote monitoring functionality. Companies with proprietary compressors, intelligent software, and vertically integrated manufacturing benefit most because they can optimize hardware and software simultaneously while accelerating compliance with evolving environmental regulations.

Between 2026 and 2028, AI-assisted energy management, predictive maintenance, and grid-interactive hybrid heat pumps will reshape product differentiation. Intelligent load balancing is expected to improve operational efficiency by approximately 16%, while predictive diagnostics can reduce unplanned maintenance by nearly 20%. Businesses investing early in software-enabled heating ecosystems, advanced refrigerants, and integrated energy platforms will strengthen competitive positioning as utilities increasingly prioritize flexible electrification technologies.

December 2024 Mitsubishi Electric announced a US$143.5 million investment to establish a heat pump compressor manufacturing facility in Kentucky, supporting North American localization and expanding production for high-efficiency HVAC systems. Source: mitsubishielectric.com

July 2025 Daikin signed a five-year collaboration with Greater Manchester to accelerate low-carbon heating deployment, strengthening workforce development and regional decarbonization through coordinated heat pump expansion. Source: daikin.com

May 2026 Daikin inaugurated its Poland manufacturing facility following an investment of approximately €300 million, creating a strategic European production hub for residential heat pumps and strengthening supply resilience. Source: daikin.com

2025 Bosch continued expanding its European heat pump manufacturing network with around €100 million investment in Portugal, increasing production capability and engineering capacity while reinforcing regional supply security. Source: bosch.com

This report provides comprehensive analysis of the hybrid electric heat pump market across system types, residential and commercial applications, and major end-user categories. It evaluates competitive positioning, technology adoption, deployment patterns, regulatory developments, and manufacturing strategies across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Approximately 60% of the assessment focuses on residential deployment trends, while commercial modernization and institutional adoption receive dedicated strategic coverage alongside emerging retrofit opportunities.

The study examines inverter technologies, low-GWP refrigerants, AI-enabled energy management, smart controls, and hybrid heating integration while assessing adoption patterns, installer ecosystem development, and production localization. It supports investment prioritization, market entry planning, partnership evaluation, supply-chain optimization, and competitive benchmarking between 2026 and 2033. Strategic insights also cover regional policy impacts, product differentiation, demand evolution, and innovation priorities shaping future market direction.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3,312.6 Million |

|

Market Revenue in 2033 |

USD 7,634.0 Million |

|

CAGR (2026 - 2033) |

11% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Daikin Industries, Ltd., Mitsubishi Electric Corporation, Panasonic Holdings Corporation, Bosch Home Comfort Group, Carrier Global Corporation, Trane Technologies plc, Johnson Controls International plc, LG Electronics Inc., Samsung Electronics Co., Ltd., Midea Group Co., Ltd., Fujitsu General Limited, NIBE Industrier AB, Vaillant Group, Ariston Holding N.V. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |