Reports

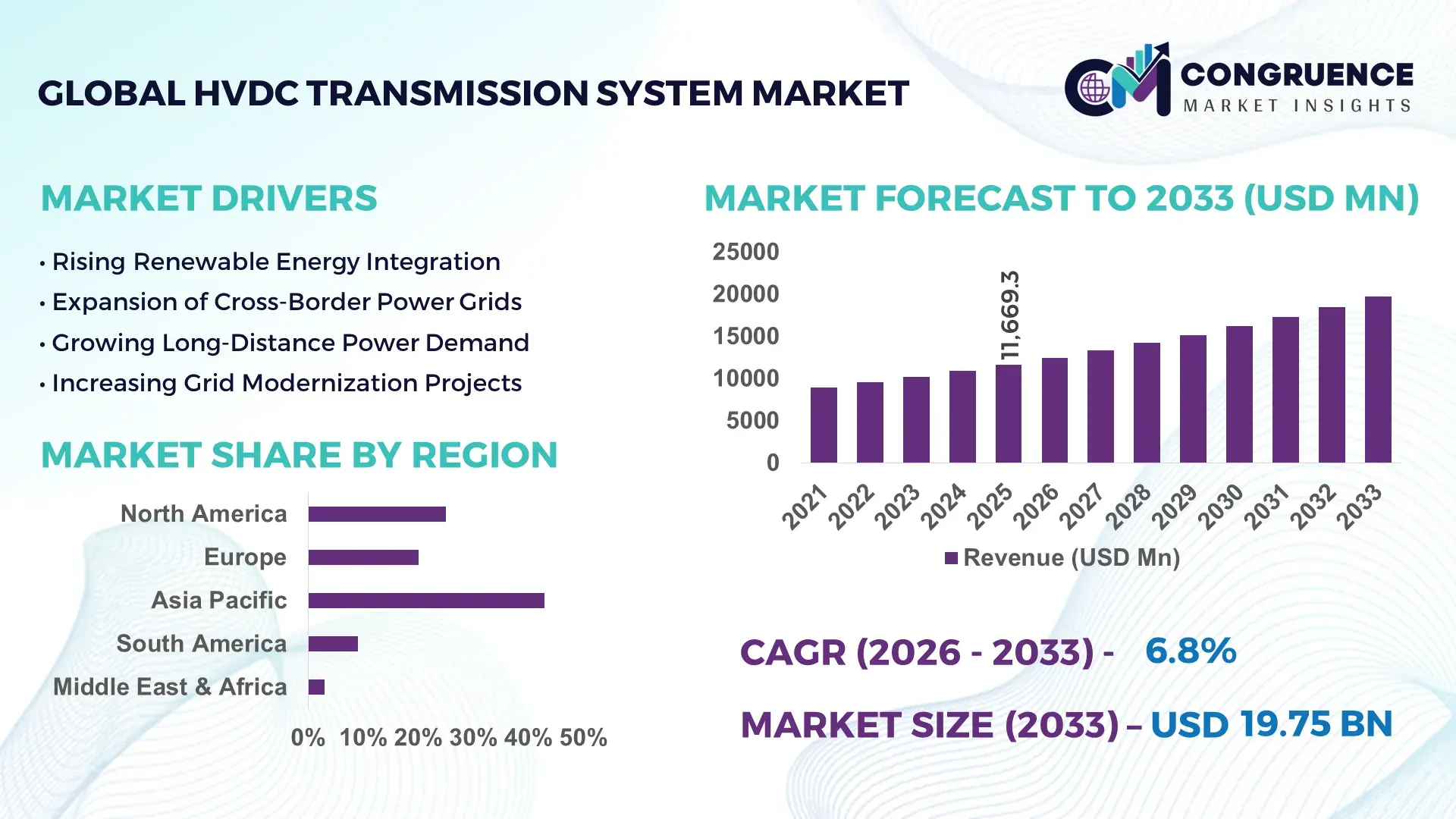

The Global HVDC Transmission System Market was valued at USD 11669.25 Million in 2025 and is anticipated to reach a value of USD 19752.08 Million by 2033 expanding at a CAGR of 6.8% between 2026 and 2033. Accelerated offshore wind integration, cross-border grid interconnection projects, and high-capacity renewable transmission corridors are driving deployment, with converter station efficiency surpassing 98% in advanced voltage source converter systems.

China continues to dominate the global HVDC transmission system market with more than 38% installed ultra-high-voltage DC capacity, supported by multi-billion-dollar investments in long-distance renewable power corridors linking western hydropower and desert solar clusters to eastern industrial hubs. State-backed grid modernization programs added over 12 GW of new HVDC-linked renewable integration capacity in 2025 alone, while Europe intensified subsea interconnection projects following energy security disruptions linked to the Russia-Ukraine conflict. Compared with conventional HVAC networks, modern HVDC systems reduce transmission losses by nearly 30% across distances exceeding 800 km, strengthening adoption among utility-scale power operators, mining clusters, and energy-intensive manufacturing industries.

Strategic investment focus is shifting toward digitally managed multi-terminal HVDC infrastructure capable of improving grid resilience, lowering curtailment rates, and supporting long-duration renewable energy balancing.

Market Size & Growth: USD 11.6 billion valuation in 2025 advances toward USD 19.7 billion by 2033, driven by offshore wind connectivity and ultra-high-voltage grid expansion at 6.8% annual growth.

Top Growth Drivers: Offshore renewable integration contributes 34% demand expansion, cross-border transmission projects add 29%, and industrial electrification supports 22% infrastructure acceleration.

Short-Term Forecast: By 2028, advanced converter technologies are projected to reduce transmission losses by 18% while improving long-distance grid efficiency above 97%.

Emerging Technologies: AI-based grid balancing, modular multilevel converters, and digital substations are improving operational responsiveness by 25% across advanced utility networks.

Regional Leaders: China exceeds USD 6 billion deployment activity, Europe crosses USD 4 billion in subsea interconnectors, and India expands renewable-linked corridors beyond USD 2 billion infrastructure value.

Consumer/End-User Trends: Nearly 46% of utility operators prioritize HVDC integration for renewable-heavy networks to stabilize voltage fluctuation and reduce congestion risk.

Pilot/Case Example: In 2025, a North Sea offshore HVDC project improved renewable transmission stability by 21% while lowering curtailment losses by 14%.

Competitive Landscape: Hitachi Energy holds approximately 17% market influence alongside Siemens Energy, GE Vernova, Mitsubishi Electric, and ABB in high-capacity transmission projects.

Regulatory & ESG Impact: Grid decarbonization mandates reduced fossil-based balancing dependence by 19% across advanced electricity markets after 2025 policy revisions.

Investment & Funding: Global utilities and sovereign-backed infrastructure programs surpassed USD 30 billion in HVDC-focused investments tied to energy security and supply-chain localization.

Innovation & Future Outlook: Multi-terminal HVDC grids, hybrid AC/DC architectures, and cybersecurity-integrated substations are reshaping next-generation transmission competitiveness.

Utility transmission operators account for nearly 52% of total HVDC deployment demand, followed by offshore renewable developers and heavy industrial power corridors supporting steel, chemicals, and mining sectors. Advanced modular multilevel converter systems improved transmission controllability by 20% compared with legacy line-commutated systems, while digital monitoring platforms accelerated predictive maintenance adoption across Europe and Asia. Demand growth remains strongest in China, India, and the North Sea energy corridor as governments prioritize grid resilience, domestic equipment sourcing, and renewable balancing capacity amid ongoing supply-chain restructuring. The market is steadily transitioning toward integrated multi-terminal transmission ecosystems supporting flexible, high-capacity energy exchange strategies.

The HVDC transmission system market is becoming strategically critical as governments and utilities prioritize energy security, renewable integration, and grid modernization. Electrification targets across China, India, and Europe are increasing demand for long-distance high-capacity transmission capable of supporting variable renewable generation without major stability losses. Supply-chain restructuring after the Russia-Ukraine energy disruption accelerated domestic manufacturing investments in converter stations, subsea cables, and advanced semiconductors used in HVDC infrastructure.

Modern voltage source converter systems deliver nearly 30% lower transmission losses over long distances compared with conventional HVAC networks while requiring narrower transmission corridors and improved reactive power management. Europe leads in offshore and subsea interconnector deployment, whereas China dominates ultra-high-voltage inland transmission linking renewable-rich western provinces with industrial demand centers. By 2028, digitally automated converter stations are expected to reduce outage response times by over 20% through AI-enabled monitoring and predictive maintenance systems.

Large-scale offshore wind integration projects in the North Sea and India’s renewable corridor expansion programs are pushing utilities toward strategic partnerships with technology providers and cable manufacturers. Companies are prioritizing localized production, cybersecurity integration, and multi-terminal grid capability to strengthen operational resilience and secure long-term transmission competitiveness.

Rapid renewable energy expansion and national grid modernization initiatives are intensifying HVDC deployment across utility-scale transmission corridors. China added more than 12 GW of HVDC-linked renewable integration capacity during 2025, while India accelerated green energy corridor investments supporting high-voltage interregional transmission. Advanced voltage source converter technology now improves power flow controllability by nearly 25% compared with legacy systems, enabling utilities to stabilize renewable-heavy grids more effectively. Europe’s offshore wind expansion and energy security policies following the Russia-Ukraine conflict further strengthened subsea HVDC interconnection demand. In response, major transmission technology providers are expanding localized manufacturing capacity, forming long-term cable supply agreements, and increasing investment in digital substations and AI-based monitoring platforms to improve operational flexibility and project execution efficiency.

HVDC transmission deployment remains constrained by elevated converter station costs, semiconductor dependency, and specialized cable manufacturing bottlenecks. Converter stations account for nearly 40% of total project expenditure, while high-voltage insulated cable prices increased by approximately 18% between 2024 and 2025 due to copper and rare-earth material volatility. Europe’s dependence on limited high-capacity subsea cable suppliers has extended lead times beyond 24 months for several offshore transmission projects. These structural pressures reduce project scalability and increase financing complexity for utility operators managing large interconnection programs. To reduce operational exposure, companies are localizing component sourcing, diversifying semiconductor partnerships, and adopting modular construction strategies that shorten commissioning timelines and improve procurement flexibility across high-priority transmission corridors.

Multi-terminal HVDC architecture and AI-driven grid intelligence platforms are creating significant long-term operational opportunities for transmission operators and infrastructure developers. Digital monitoring systems improved fault detection accuracy by nearly 28% in advanced pilot deployments, while modular multilevel converters enhanced grid stability under variable renewable loads. India and Saudi Arabia are increasing investment in smart transmission corridors integrating renewable balancing, industrial electrification, and cross-border power exchange capability. Emerging hybrid AC/DC grid models also reduce land-use intensity and optimize long-distance power routing efficiency. Technology providers are responding through R&D partnerships, advanced cybersecurity integration, and software-driven energy management ecosystems designed for predictive grid optimization. A major non-obvious opportunity lies in industrial decarbonization clusters requiring stable ultra-high-capacity transmission for green hydrogen, steel, and battery manufacturing operations.

Large-scale HVDC deployment faces rising execution complexity tied to interoperability, cybersecurity, workforce specialization, and grid synchronization requirements. Multi-vendor transmission environments increase integration engineering workloads by nearly 22%, while cyberattack exposure on digitally connected substations intensified following rapid grid automation adoption. Germany and the United Kingdom are confronting skilled labor shortages in high-voltage engineering and subsea cable installation, delaying several strategic transmission projects. Inconsistent regulatory approval structures and environmental permitting timelines further complicate cross-border infrastructure deployment. These pressures directly affect transmission reliability, commissioning consistency, and long-term infrastructure competitiveness. Companies must strengthen engineering partnerships, expand workforce training programs, and invest in standardized digital control systems capable of supporting secure, scalable, and resilient next-generation HVDC transmission ecosystems.

Bipolar Systems remain the leading segment due to superior reliability, high-capacity power transfer capability, and lower transmission losses during long-distance operation. Nearly 48% of utility-scale HVDC installations commissioned after 2024 adopted bipolar architecture because of improved fault tolerance and operational continuity in ultra-high-voltage corridors. Voltage Source Converter systems represent the fastest-growing type as renewable-heavy grids increasingly require flexible reactive power management and black-start capability. Compared with Line Commutated Converter systems, advanced VSC technology improves grid controllability by approximately 22% while reducing substation footprint requirements. Monopolar Systems continue serving cost-sensitive and lower-capacity applications, particularly in remote industrial transmission routes, whereas Back-to-Back Systems are gaining strategic relevance in asynchronous grid interconnection projects across Europe and the Middle East. Technology providers are prioritizing converter efficiency upgrades, modular designs, and digital control integration while expanding partnerships with utilities developing offshore and cross-border transmission infrastructure.

Power Transmission remains the dominant application due to extensive demand for long-distance high-capacity electricity transfer connecting industrial hubs, renewable corridors, and urban load centers. More than 54% of active HVDC projects globally focus on bulk power transmission efficiency and grid stabilization objectives. Offshore Wind Connectivity is emerging as the fastest-growing application as offshore generation capacity expansion intensifies across the North Sea and East Asia. Dedicated offshore HVDC systems reduce transmission losses by nearly 30% compared with traditional HVAC export solutions over long marine distances. Renewable Energy Integration and Grid Interconnection applications are also expanding rapidly as utilities modernize networks to accommodate distributed renewable generation and cross-border energy exchange. Submarine Transmission continues gaining importance in island-grid connectivity and underwater interconnector projects. Companies are responding through automated converter platforms, subsea cable scaling, and integrated transmission management systems that improve operational reliability and reduce grid balancing complexity across renewable-heavy electricity networks.

Industry deployment assessments presented during recent European transmission operator forums indicated that offshore wind-linked HVDC applications accounted for nearly 40% of newly planned subsea transmission infrastructure projects entering development review during 2025.

Utilities remain the largest end-user segment due to large-scale responsibility for grid modernization, renewable balancing, and interregional electricity transmission infrastructure. Nearly 58% of HVDC deployment activity is concentrated among national and private utility operators managing high-capacity transmission corridors and cross-border interconnections. Renewable Energy companies represent the fastest-growing end-user group as offshore wind developers and utility-scale solar operators increasingly require dedicated long-distance transmission integration. Industrial Sector demand is also strengthening, particularly across mining, steel, and chemical manufacturing facilities requiring stable high-load electricity supply with lower transmission losses. Government Agencies continue driving strategic interconnection programs tied to energy security and decarbonization mandates, while Oil and Gas operators are adopting HVDC systems for offshore platform electrification. Transportation Sector applications remain comparatively niche but are expanding in rail electrification and smart mobility infrastructure. Equipment suppliers are targeting utilities and renewable developers through customized converter systems, long-term maintenance contracts, and localized manufacturing partnerships designed to improve project execution efficiency and lifecycle reliability.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

Grid modernization and renewable balancing reshape transmission priorities

North America maintains strong HVDC deployment momentum through utility-led grid modernization, offshore wind integration, and cross-border electricity exchange programs. The region contributes nearly 24% of global HVDC infrastructure activity, supported by rising investments in long-distance renewable transmission corridors connecting western renewable clusters with industrial demand hubs. The United States and Canada accelerated interregional transmission planning after grid congestion increased renewable curtailment rates by approximately 14% during peak demand periods. Utilities are prioritizing digitally managed converter stations and underground transmission expansion to strengthen resilience against climate-driven outages. Recent transmission partnerships linked to offshore wind and battery-storage integration improved operational flexibility and reduced transmission losses across high-load interstate corridors.

The United States leads regional deployment through large-scale renewable integration programs, offshore wind transmission development, and federal infrastructure modernization initiatives. More than 35 GW of planned renewable projects require advanced HVDC connectivity to reduce interconnection bottlenecks and improve long-distance electricity transfer efficiency. Domestic manufacturers are expanding converter assembly operations and cable supply partnerships to strengthen local sourcing capability and reduce dependency on imported high-voltage components.

Subsea interconnection and decarbonization accelerate deployment scale

Europe remains a major innovation hub for subsea HVDC infrastructure, supported by aggressive decarbonization policies, offshore wind expansion, and cross-border grid synchronization projects. The region represents approximately 29% of global HVDC deployment concentration, with North Sea interconnectors and offshore transmission systems driving operational expansion. Germany, the United Kingdom, and the Netherlands intensified investment in multi-terminal subsea transmission corridors after energy security concerns exposed grid balancing limitations following the Russia-Ukraine conflict. Advanced voltage source converter adoption increased by nearly 27% across newly approved projects due to stronger renewable integration requirements. Utilities and transmission operators are restructuring procurement strategies and expanding domestic cable manufacturing to reduce supply-chain dependency and improve project delivery timelines.

Germany maintains strategic leadership through energy transition programs focused on renewable-heavy transmission modernization and industrial electrification. Large north-to-south HVDC corridors are being expanded to support offshore wind balancing and manufacturing-sector energy stability. The country accelerated permitting reforms in 2025 to reduce infrastructure approval delays, while utilities increased investment in underground HVDC cable deployment and AI-enabled grid management systems supporting transmission efficiency optimization.

Ultra-high-voltage deployment drives regional dominance

Asia-Pacific dominates the global HVDC transmission system market through extensive ultra-high-voltage deployment, renewable corridor expansion, and industrial electrification initiatives. The region controls nearly 43% of global HVDC infrastructure activity, led by China and India’s large-scale transmission modernization programs. China added more than 12 GW of HVDC-linked renewable integration capacity during 2025, while India accelerated green corridor projects supporting high-capacity interstate transmission. Manufacturing scale advantages and localized converter production reduced procurement costs by approximately 16% compared with imported infrastructure models. Utilities and equipment providers are strengthening long-term technology alliances, modular converter deployment, and smart grid synchronization to support rising industrial electricity demand and renewable balancing complexity across dense urban and manufacturing clusters.

China remains the world’s largest HVDC deployment hub through state-backed ultra-high-voltage expansion and renewable transmission integration. The country operates multiple long-distance HVDC corridors connecting western hydropower and desert solar regions with eastern industrial centers. More than 38% of global installed ultra-high-voltage DC capacity is concentrated in China, while domestic manufacturers continue scaling converter technology innovation, high-voltage semiconductor production, and digitally automated transmission infrastructure development.

Hydropower connectivity strengthens transmission investment

South America is expanding HVDC deployment through hydropower transmission modernization, mining-sector electrification, and intercountry electricity exchange initiatives. Brazil and Chile account for the majority of regional deployment activity, with the region contributing nearly 6% of global HVDC infrastructure concentration. Long-distance renewable and hydropower transmission requirements are increasing demand for efficient high-capacity electricity corridors across geographically remote industrial zones. However, infrastructure financing constraints and uneven transmission modernization continue limiting project execution speed in several markets. Utilities are responding through public-private transmission partnerships and phased infrastructure expansion models. Recent renewable-linked transmission upgrades improved long-distance electricity transfer efficiency by approximately 15% across selected mining and industrial power corridors.

Brazil leads South American HVDC adoption through hydropower integration, renewable expansion, and transmission connectivity across large geographic distances. National transmission operators are strengthening north-to-south electricity transfer capability to improve industrial supply reliability and renewable balancing efficiency. HVDC deployment linked to hydropower assets reduced transmission losses in selected long-distance corridors, while domestic infrastructure programs continue supporting grid resilience upgrades and high-capacity transmission modernization.

Energy diversification and megaproject investment expand infrastructure

Middle East & Africa is emerging as a high-priority HVDC investment zone driven by energy diversification programs, industrial megaprojects, and renewable integration strategies. The region currently contributes approximately 8% of global HVDC activity, but deployment intensity is rising rapidly through utility-scale solar transmission and cross-border electricity connectivity projects. Saudi Arabia and the United Arab Emirates accelerated grid modernization programs tied to industrial diversification and green hydrogen infrastructure development. Large transmission projects integrating renewable energy reduced grid congestion pressure by nearly 18% in recently upgraded corridors. Utilities and sovereign-backed developers are expanding partnerships with international converter manufacturers and cable suppliers to strengthen localized infrastructure capability and improve long-term energy security resilience.

Saudi Arabia is advancing HVDC deployment through renewable corridor expansion, industrial electrification, and smart grid modernization under national diversification initiatives. Utility operators are integrating high-capacity transmission systems supporting large-scale solar and green hydrogen projects across remote industrial zones. Infrastructure modernization programs accelerated investment in digitally monitored converter stations and cross-border interconnection capability, while transmission developers expanded partnerships focused on localized engineering expertise and advanced grid stability management.

Hitachi Energy, Siemens Energy, GE Vernova, Mitsubishi Electric, and Nexans collectively control nearly 58% of global HVDC infrastructure influence, competing against regional cable manufacturers and converter-system specialists on technology efficiency, execution speed, and supply security. European OEMs dominate offshore and subsea transmission, while Chinese suppliers compete aggressively through localized manufacturing and lower procurement costs. Converter efficiency improvements exceeding 22% and project delivery acceleration near 18% increasingly determine contract wins. Companies are pursuing vertical integration, semiconductor partnerships, and long-term cable agreements to reduce supply bottlenecks. High capital intensity, engineering complexity, and grid certification requirements remain major entry barriers. Winning requires scalable technology, resilient supply chains, and rapid infrastructure execution capability.

Hitachi Energy

Siemens Energy

GE Vernova

Mitsubishi Electric Corporation

Toshiba Energy Systems & Solutions Corporation

Nexans

Prysmian Group

NKT A/S

LS Cable & System

NR Electric Co., Ltd.

Hyosung Heavy Industries

Bharat Heavy Electricals Limited

Schneider Electric

Fuji Electric Co., Ltd.

Voltage Source Converter technology remains the dominant operational upgrade in HVDC infrastructure, particularly across renewable-heavy transmission corridors and offshore wind integration projects. Advanced VSC systems improve power-flow controllability by nearly 22% compared with legacy Line Commutated Converter platforms while reducing converter station footprint requirements by approximately 18%. More than 45% of newly approved HVDC projects entering execution during 2026 incorporate digitally managed VSC architecture for faster grid balancing and reactive power support. Utilities benefit through lower transmission instability, reduced curtailment losses, and stronger integration of variable renewable generation into national grids.

AI-enabled grid automation and predictive maintenance platforms are emerging as high-impact technologies reshaping operational reliability. Machine-learning diagnostics reduced outage response time by nearly 24% in pilot deployments across Europe and Asia, while digital twin modeling improved maintenance planning efficiency by 17%. Multi-terminal HVDC networks are also gaining traction, enabling synchronized renewable balancing across interconnected transmission corridors. Companies investing early in AI-integrated converter stations and software-defined transmission control systems are securing operational advantages in utility modernization contracts and large offshore infrastructure deployments.

Wide-bandgap semiconductors, hybrid AC/DC grid architecture, and compact underground converter systems represent the next disruptive technology layer between 2026 and 2028. Silicon carbide-based power electronics improve thermal efficiency by nearly 15% over conventional insulated-gate bipolar transistor systems while supporting faster switching performance and lower operational losses. China, Germany, and India are accelerating deployment of integrated smart transmission ecosystems combining HVDC infrastructure with energy storage and real-time digital grid synchronization. Technology leaders capable of scaling localized manufacturing, cybersecurity-integrated controls, and modular converter deployment will gain stronger positioning in future interconnection and renewable transmission programs.

April 2025 – Hitachi Energy secured a 950-km, 6 GW HVDC transmission contract in India connecting Rajasthan and Uttar Pradesh renewable corridors, strengthening interstate clean-energy transfer efficiency and supporting grid modernization expansion. Source: Hitachi Energy

April 2026 – Hitachi Energy and Adani Energy Solutions commissioned a 1,000 MW HVDC city infeed project in Mumbai, increasing external electricity supply capacity by 50% while improving urban grid resilience and renewable integration capability. Source: Hitachi Global

September 2025 – Siemens Energy announced a €220 million expansion of its Nuremberg transformer manufacturing facility, increasing production capacity by 50% to address accelerating grid infrastructure and HVDC equipment demand globally. Source: Reuters

December 2025 – Multiple grid equipment manufacturers including Hitachi Energy and Siemens expanded U.S. transformer and transmission infrastructure investments exceeding USD 1 billion combined, responding to a 274% rise in transformer demand since 2019.

This report provides comprehensive analysis of the HVDC Transmission System market across key technology types, applications, end-users, and major regional deployment hubs between 2026 and 2033. The study evaluates Monopolar Systems, Bipolar Systems, Back-to-Back Systems, Voltage Source Converter, and Line Commutated Converter technologies while assessing operational demand across power transmission, offshore wind connectivity, submarine transmission, and renewable integration networks. More than 55% of current deployment activity remains concentrated in utility-led grid modernization and renewable balancing infrastructure.

The report further examines competitive positioning, infrastructure investment patterns, supply-chain transformation, and digital transmission technologies influencing strategic decision-making. Regional analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa with detailed country-level operational insights. It also evaluates adoption trends in utilities, industrial electrification, renewable energy developers, transportation infrastructure, and government-backed interconnection programs. Strategic intelligence on AI-enabled substations, multi-terminal HVDC networks, semiconductor innovation, and localized manufacturing expansion supports investment planning, partnership strategy, and future infrastructure prioritization.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 11669.25 Million |

|

Market Revenue in 2033 |

USD 19752.08 Million |

|

CAGR (2026 - 2033) |

6.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Hitachi Energy, Siemens Energy, GE Vernova, Mitsubishi Electric Corporation, Toshiba Energy Systems & Solutions Corporation, Nexans, Prysmian Group, NKT A/S, LS Cable & System, NR Electric Co., Ltd., Hyosung Heavy Industries, Bharat Heavy Electricals Limited, Schneider Electric, Fuji Electric Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |