Reports

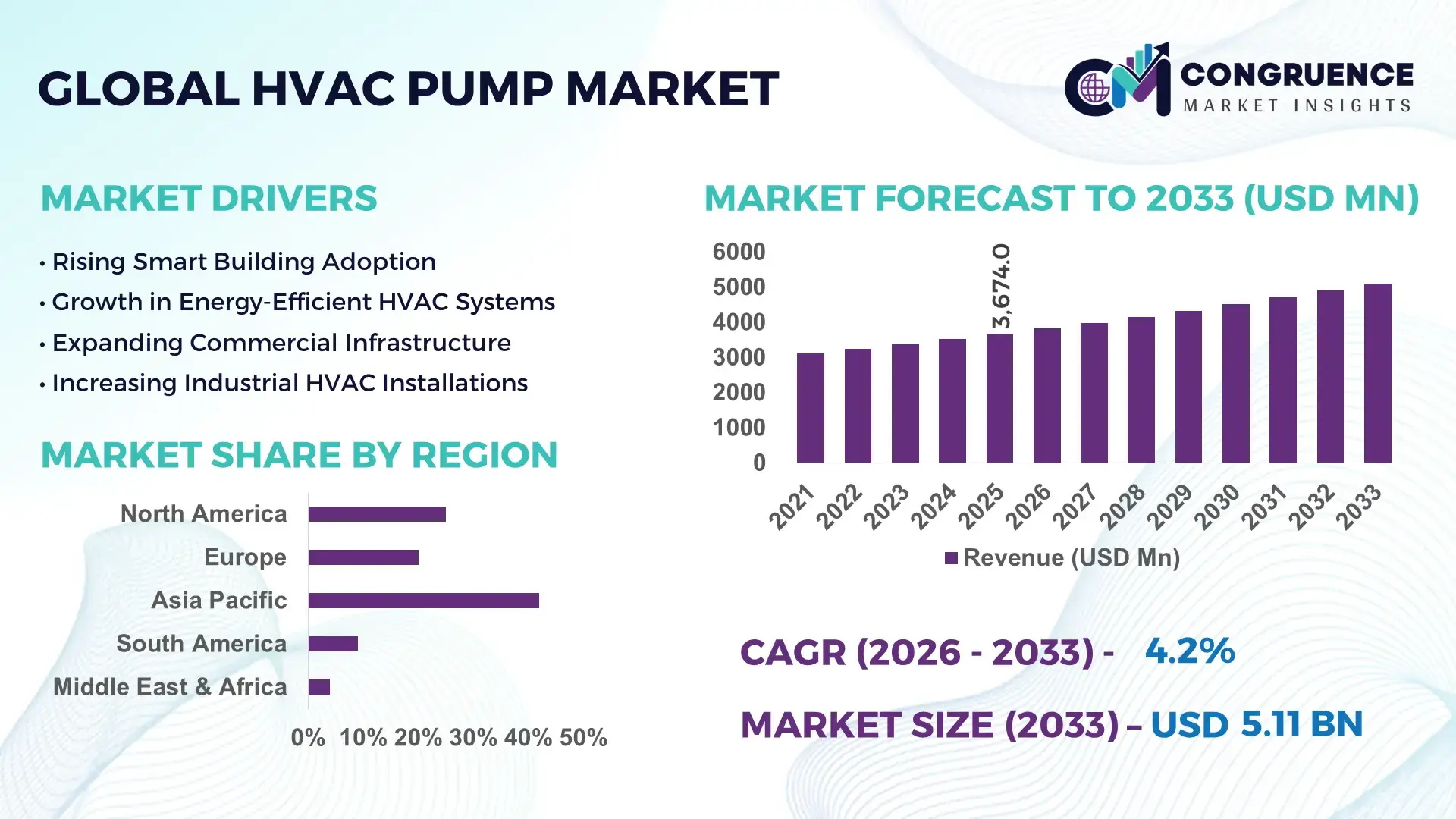

The Global HVAC Pump Market was valued at USD 3674 Million in 2025 and is anticipated to reach a value of USD 5106 Million by 2033 expanding at a CAGR of 4.2% between 2026 and 2033. Rising deployment of variable-speed HVAC circulation pumps, smart building automation, and energy-efficient district cooling systems is reducing commercial energy consumption by 18%–25%, accelerating replacement demand across healthcare, data center, and high-rise infrastructure projects.

China remains the dominant country in the global HVAC pump market, accounting for nearly 31% of total manufacturing capacity in 2026, supported by over USD 9 billion in commercial infrastructure and smart-city HVAC upgrades. More than 62% of newly commissioned large-scale commercial buildings in tier-1 urban regions now integrate digitally monitored variable-flow pumping systems, compared with below 40% adoption in several developing economies. Domestic industrial production advantages and advanced motor integration technologies have improved operating efficiency by nearly 20% versus conventional fixed-speed HVAC pump installations, strengthening export competitiveness across Asia and the Middle East.

Manufacturers prioritizing intelligent pump controls, regionalized supply chains, and low-energy system integration are securing stronger positioning in high-growth commercial retrofitting and sustainable infrastructure contracts.

Market Size & Growth: USD 3674 million in 2025 reaching USD 5106 million by 2033, driven by smart HVAC retrofits, district cooling expansion, and high-efficiency pump adoption at 4.2% CAGR.

Top Growth Drivers: Variable-speed pump penetration rising 24%, commercial retrofit activity up 19%, and smart building integration increasing 28% globally.

Short-Term Forecast: By 2027, advanced HVAC pumps reduce commercial energy consumption by 22% while maintenance downtime declines nearly 17%.

Emerging Technologies: AI-enabled monitoring, IoT-connected circulation systems, and ECM motor integration improve operational efficiency by 20%–26%.

Regional Leaders: Asia-Pacific exceeds USD 2 billion demand with rapid urban infrastructure growth, Europe advances low-carbon HVAC adoption by 31%, and North America expands retrofit installations across data centers.

Consumer/End-User Trends: Nearly 58% of commercial facility operators prioritize intelligent HVAC pumping systems with predictive maintenance capabilities.

Pilot/Case Example: In 2025, a large Middle East district cooling upgrade improved pumping efficiency by 27% and lowered annual operating costs by 18%.

Competitive Landscape: Top manufacturers collectively control nearly 46% market share, with global competition intensifying among energy-efficient HVAC system suppliers.

Regulatory & ESG Impact: Green building mandates and carbon-reduction targets increased high-efficiency HVAC pump installations by over 30% across regulated commercial sectors.

Investment & Funding: More than USD 4.5 billion in industrial expansion and manufacturing investments supported regional production localization between 2024 and 2026.

Innovation & Future Outlook: Magnetic-drive pumps, digital twin diagnostics, and low-noise compact systems are reshaping next-generation HVAC infrastructure strategies.

Commercial real estate, industrial manufacturing, and institutional infrastructure collectively contribute over 72% of global HVAC pump demand, with data centers and healthcare facilities emerging as high-value deployment sectors. Advanced electronically commutated motor systems and AI-based flow optimization technologies improve operational efficiency by nearly 25% while reducing maintenance interventions by 15%. Asia-Pacific maintains above 43% demand concentration due to rapid urban construction activity, while Europe accelerates retrofit adoption under stricter energy-efficiency regulations. Growing regional manufacturing localization and supply-chain diversification are strengthening long-term procurement strategies and supporting broader adoption of intelligent HVAC fluid management systems.

The HVAC pump market is becoming a strategic battleground as commercial infrastructure operators prioritize energy optimization, operational resilience, and lifecycle cost control across high-density urban developments, healthcare campuses, semiconductor plants, and hyperscale data centers. Accelerating electrification policies and stricter building-efficiency mandates are transforming HVAC pumping systems from passive mechanical components into digitally controlled energy-management assets. Between 2024 and 2026, supply-chain regionalization and tightening carbon compliance standards forced manufacturers to accelerate local production strategies and advanced component sourcing. Variable-speed intelligent pumping systems now outperform legacy fixed-speed systems by improving energy efficiency by 28% while reducing operating costs by 19% compared to conventional configurations.

Asia-Pacific leads in installation volume due to large-scale urban infrastructure expansion, while Europe leads in smart HVAC adoption and low-emission system integration with nearly 36% higher penetration of digitally monitored pumping platforms. Over the next three years, predictive maintenance integration and AI-driven flow balancing are projected to reduce unplanned commercial HVAC downtime by 21% and improve system performance consistency by 24%. ESG-focused retrofitting strategies are also creating measurable competitive advantages, with green-certified commercial buildings lowering annual energy expenses by approximately 17%.

In 2025, a large hospital modernization project in the Middle East upgraded to intelligent HVAC circulation systems and achieved a 26% reduction in energy consumption within one operational cycle. Major manufacturers are shifting capital allocation toward connected pump ecosystems, regional assembly expansion, and low-noise high-efficiency motor technologies to secure long-term infrastructure contracts. Companies optimizing digital monitoring capabilities, energy-performance compliance, and localized manufacturing footprints are transforming competitive positioning across the global HVAC pump value chain.

Commercial infrastructure modernization is accelerating demand for intelligent HVAC pumping systems as facility operators target 20%–30% energy optimization across hospitals, data centers, airports, and mixed-use buildings. Rapid expansion of district cooling networks and stricter building-efficiency mandates are forcing replacement of fixed-speed circulation systems with digitally controlled variable-flow technologies. Between 2024 and 2026, supply-chain restructuring and rising electricity costs increased demand for regionally manufactured high-efficiency pumps, particularly across Asia-Pacific and the Middle East. Smart HVAC pump adoption within large commercial facilities increased nearly 27%, while predictive maintenance integration reduced equipment downtime by 18%. Manufacturers are responding through localized production expansion, strategic automation partnerships, and accelerated investment in AI-enabled pump monitoring platforms and advanced motor technologies.

Volatility in copper, stainless steel, and electronic component pricing is constraining HVAC pump manufacturing margins and delaying large-scale procurement cycles. Between 2024 and 2026, industrial motor and semiconductor component costs increased by nearly 14%, while logistics disruptions across Red Sea shipping routes extended delivery timelines by over 20% for several global suppliers. Aging commercial infrastructure in emerging economies is further restricting deployment scalability, particularly where energy distribution systems cannot support advanced digitally controlled HVAC installations. These constraints are increasing retrofit complexity and limiting cost competitiveness for smaller manufacturers. Companies are mitigating exposure through supplier diversification, long-term material agreements, regional assembly investments, and development of compact energy-efficient systems requiring lower installation complexity and reduced infrastructure modifications across aging facilities globally.

AI-enabled predictive control systems, magnetic-drive pump technologies, and digitally integrated building management platforms are redefining HVAC pump market competitiveness. Smart pumping solutions improve operational efficiency by nearly 25% while lowering maintenance intervention frequency by 16%, creating measurable lifecycle cost advantages for commercial operators. Southeast Asia, the Gulf region, and secondary urban markets across Africa are emerging as high-growth deployment zones due to rapid smart-city construction and district cooling expansion. More than 34% of newly planned commercial megaprojects now specify intelligent HVAC flow optimization systems as standard infrastructure requirements. Manufacturers are accelerating R&D investment, expanding regional manufacturing ecosystems, and building software-driven service partnerships to capture recurring performance-management revenue while strengthening long-term positioning within advanced energy-efficient infrastructure markets globally.

Grid instability, fragmented building infrastructure standards, and integration complexity are constraining consistent deployment of advanced HVAC pumping systems across large commercial facilities. Nearly 29% of retrofit projects encounter operational delays due to incompatible legacy infrastructure, while advanced control-system installation costs remain approximately 18% higher than conventional HVAC configurations. Rapid digitalization is also increasing cybersecurity exposure within connected building-management environments, forcing stricter compliance requirements and higher implementation costs. In several emerging markets, inconsistent energy infrastructure continues limiting scalable adoption of high-efficiency intelligent pumping technologies. To remain competitive, manufacturers must strengthen digital security frameworks, accelerate interoperability innovation, and expand technical service partnerships capable of supporting long-cycle infrastructure modernization projects while maintaining performance reliability, energy optimization, and cost discipline across global commercial installations.

32% increase in variable-speed pump deployment is reshaping commercial HVAC operations. Large commercial facilities are replacing fixed-speed systems with intelligent variable-flow configurations to reduce electricity consumption by 20% and improve load balancing accuracy by 18%. Real-time sensor integration and AI-based diagnostics are accelerating across hospitals and data centers, forcing manufacturers to expand software-enabled pump portfolios. Companies are restructuring supply agreements to secure advanced motor components amid continuing electronic component shortages.

27% faster maintenance execution through predictive monitoring is redefining service models. HVAC operators are integrating cloud-connected diagnostics platforms that reduce emergency repair incidents by 21% and extend pump operating life by nearly 15%. Instead of relying on traditional reactive servicing, manufacturers are shifting toward subscription-based monitoring contracts and remote performance management. This operational shift is optimizing labor utilization while creating recurring aftermarket revenue streams for advanced HVAC pump suppliers.

41% rise in district cooling installations across Gulf and Asia-Pacific markets is shifting regional demand patterns. Urban infrastructure developers are deploying centralized chilled water circulation systems to lower building-level cooling energy use by 24%. Asia-Pacific dominates equipment volume, while Middle Eastern operators lead in large-capacity system integration. Companies are responding through localized assembly expansion and strategic engineering partnerships to shorten project delivery timelines amid persistent shipping route disruptions.

19% reduction in installation footprint is accelerating compact HVAC pump adoption. Commercial retrofitting projects increasingly prioritize modular and low-noise pumping systems capable of fitting constrained urban infrastructure layouts. Compact integrated pumps improve installation speed by 16% and reduce maintenance access requirements by 14%, particularly in healthcare and hospitality facilities. Manufacturers are optimizing product designs with lightweight materials and digitally integrated controls to capture high-margin retrofit contracts and space-constrained modernization projects.

The HVAC pump market is segmented by type, application, and end-user, with demand increasingly shifting toward energy-efficient and digitally controlled systems. Centrifugal and variable speed pumps collectively account for over 58% of installations due to scalability and lower operational energy use. Cooling systems and chilled water circulation dominate application demand as commercial infrastructure modernization accelerates globally. Commercial buildings represent nearly 38% of end-user deployment, while healthcare and industrial facilities are rapidly increasing intelligent HVAC integration. Market positioning is shifting toward high-efficiency retrofits, predictive maintenance compatibility, and compact system deployment, forcing manufacturers to prioritize smart pump technologies, localized production, and application-specific customization strategies.

Centrifugal pumps dominate the HVAC pump market with approximately 34% share due to their scalability, stable flow control, lower maintenance complexity, and compatibility with large commercial cooling networks. Their structural dominance remains strongest across district cooling systems, industrial HVAC infrastructure, and high-capacity circulation applications where continuous operational reliability is critical. However, variable speed pumps are emerging as the fastest-growing segment, recording nearly 18% adoption growth as energy optimization mandates accelerate intelligent HVAC retrofits globally. Compared with conventional centrifugal systems, advanced variable speed pumps reduce electricity consumption by nearly 25% while improving flow precision across dynamic load environments. Circulator pumps maintain strong penetration in residential and light commercial infrastructure because of compact installation advantages and simplified operational control. Booster pumps and condensate pumps collectively account for nearly 26% of market demand, serving niche but strategically important applications involving pressure stabilization, condensate management, and multi-floor building infrastructure. Manufacturers are shifting product development toward digitally integrated variable-speed technologies, localized assembly expansion, and compact low-noise systems to capture growing retrofit opportunities and compliance-driven infrastructure modernization projects.

“According to a 2025 report by the International Energy Agency, variable speed pump technology was adopted by over 48% of newly upgraded commercial HVAC facilities, resulting in nearly 23% energy efficiency improvement and significant operating cost optimization, reinforcing its growing strategic importance.”

Cooling systems lead the HVAC pump market with nearly 36% demand concentration due to expanding commercial infrastructure, district cooling deployment, and rising cooling loads across data centers, healthcare campuses, and mixed-use developments. Usage concentration remains strongest in Asia-Pacific and Middle Eastern urban projects where large-capacity thermal management systems operate continuously under high ambient conditions. Chilled water circulation is the fastest-growing application segment, expanding by approximately 19% as intelligent cooling networks and centralized HVAC infrastructure gain priority within energy-efficiency modernization programs. Compared with traditional boiler water circulation systems, chilled water circulation platforms deliver nearly 21% lower operational energy consumption and improved thermal distribution consistency. Heating systems and commercial HVAC operations continue holding substantial combined market share exceeding 40%, particularly across institutional and industrial facilities requiring stable year-round climate control. Ventilation systems and boiler water circulation maintain niche operational importance within retrofit-intensive infrastructure environments. Companies are accelerating deployment of AI-enabled flow optimization systems, modular pumping configurations, and digitally monitored circulation platforms to capture rising demand for high-efficiency commercial HVAC operations and centralized thermal infrastructure modernization.

“According to a 2025 report by the International District Energy Association, chilled water circulation systems were deployed across over 12,000 large commercial facilities, improving cooling efficiency by nearly 24%, highlighting their rapid operational adoption.”

Commercial buildings dominate the HVAC pump market with nearly 38% share due to continuous HVAC utilization across office towers, retail complexes, airports, and mixed-use infrastructure. High occupancy density, centralized cooling requirements, and growing smart-building integration are driving large-scale deployment of intelligent pumping systems within this segment. Healthcare facilities represent the fastest-growing end-user category, recording approximately 17% adoption growth as hospitals prioritize uninterrupted climate control, infection-sensitive airflow management, and energy-efficient infrastructure modernization. Compared with residential buildings, healthcare facilities deploy significantly more advanced digitally monitored HVAC pumping systems to ensure operational continuity and regulatory compliance. Industrial facilities, hospitality sector deployments, and educational institutions collectively contribute nearly 42% of market demand, supported by expanding retrofit programs and rising operational efficiency requirements. Residential buildings continue emphasizing compact low-noise circulation systems and cost-sensitive installations. Manufacturers are increasingly targeting commercial and healthcare operators through predictive maintenance partnerships, customized energy-efficiency solutions, and long-cycle service agreements to strengthen recurring revenue streams and secure strategic infrastructure modernization contracts.

“According to a 2025 report by the American Society of Heating, Refrigerating and Air-Conditioning Engineers, adoption among healthcare facilities increased by 22%, with over 8,500 institutions implementing intelligent HVAC pumping systems, leading to nearly 19% energy optimization and improved environmental control reliability, indicating a strong shift in demand dynamics.”

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.4% between 2026 and 2033.

Asia-Pacific leads global HVAC pump demand due to large-scale commercial infrastructure expansion, localized manufacturing capacity, and aggressive smart-city deployment across China, India, and Southeast Asia. North America contributes nearly 26% of market demand, driven by data center cooling upgrades and intelligent retrofit adoption, while Europe holds approximately 22% share through energy-efficiency compliance and low-emission building modernization programs. The Middle East & Africa region is accelerating rapidly as district cooling investments and large infrastructure projects expand across Gulf economies. Between 2024 and 2026, regional supply-chain localization and stricter building efficiency regulations reshaped procurement priorities globally. Companies are increasingly focusing investment on Asia-Pacific production expansion, European smart HVAC integration, and Middle Eastern infrastructure partnerships to strengthen long-term market positioning.

North America accounts for nearly 26% of global HVAC pump demand, supported by accelerating retrofit activity across commercial buildings, healthcare infrastructure, and hyperscale data centers. Facility operators are prioritizing intelligent variable-speed pumping systems capable of reducing energy consumption by 22% while improving operational monitoring efficiency. Tightening building-efficiency standards and rising electricity costs are forcing rapid replacement of legacy fixed-speed HVAC infrastructure across the United States and Canada. More than 48% of newly upgraded commercial facilities now integrate predictive maintenance-enabled HVAC pumping platforms. Manufacturers are expanding regional assembly operations and strengthening software integration partnerships to support digitally connected building management systems. Enterprise buyers increasingly prioritize lifecycle cost optimization, low-maintenance performance, and compliance-ready infrastructure, reinforcing North America as a high-value region for advanced HVAC pump deployment and strategic expansion.

Europe represents approximately 22% of the global HVAC pump market, with Germany, France, and the Nordic countries leading adoption of high-efficiency commercial climate-control systems. Aggressive carbon-reduction policies and tightening building energy directives are reshaping procurement priorities, forcing rapid deployment of digitally monitored low-energy HVAC pumping solutions. More than 39% of commercial retrofit projects across Western Europe now specify variable-speed circulation systems to improve energy optimization and emissions compliance. Smart HVAC integration and low-noise compact pumping technologies are accelerating within healthcare, hospitality, and institutional infrastructure environments. Manufacturers are investing in advanced motor technologies, localized component sourcing, and ESG-aligned product engineering to strengthen regulatory compatibility. European enterprises consistently favor efficiency-focused, compliance-driven infrastructure investments, making the region a critical benchmark for innovation, operational sustainability, and next-generation HVAC system standardization.

Asia-Pacific leads the global HVAC pump market with nearly 43% demand concentration, supported by rapid commercial construction, industrial expansion, and high-volume manufacturing capacity across China, India, Japan, and Southeast Asia. China alone contributes over 31% of regional production capacity through vertically integrated HVAC equipment manufacturing ecosystems and export-oriented supply networks. Large-scale adoption of district cooling systems, intelligent commercial infrastructure, and smart-building technologies is accelerating deployment of digitally controlled HVAC pumps. More than 52% of newly developed urban commercial projects in major metropolitan zones now integrate energy-efficient circulation systems. Manufacturers are rapidly expanding localized production, automation capabilities, and regional supplier partnerships to shorten delivery cycles and reduce import dependency. Enterprise buyers prioritize scalable deployment, competitive pricing, and operational speed, positioning Asia-Pacific as the primary global expansion and manufacturing hub for HVAC pump suppliers.

South America accounts for nearly 7% of global HVAC pump demand, with Brazil and Argentina leading deployment across commercial infrastructure, industrial facilities, and institutional buildings. Rising urbanization and expansion of healthcare and retail infrastructure are increasing demand for energy-efficient HVAC circulation systems. However, currency volatility, import dependency, and inconsistent infrastructure investment continue constraining large-scale modernization projects across several economies. Nearly 34% of commercial buyers prioritize lower-maintenance HVAC pumping systems to reduce long-term operational costs amid tightening capital budgets. Localized demand for compact and retrofit-compatible systems is accelerating, particularly within urban commercial developments. Manufacturers are strengthening distributor partnerships and regional inventory networks to improve delivery stability and pricing flexibility. The region presents strong infrastructure-driven opportunity, but long-term success depends on balancing affordability, supply-chain resilience, and localized service capabilities.

Middle East & Africa contributes approximately 11% of global HVAC pump demand, driven by large-scale commercial construction, district cooling expansion, and infrastructure modernization across the United Arab Emirates, Saudi Arabia, and South Africa. High ambient temperatures and continuous cooling requirements are accelerating deployment of high-capacity chilled water circulation systems across airports, hospitality complexes, and mixed-use urban developments. More than 46% of major commercial infrastructure projects across Gulf economies now integrate intelligent HVAC flow-management technologies to improve energy efficiency and operational stability. Regional governments and private developers are increasing investment in smart-city infrastructure and localized engineering partnerships to strengthen long-term cooling resilience. Commercial buyers prioritize durability, energy optimization, and rapid deployment capabilities, positioning the region as a strategically important growth corridor for advanced HVAC pump manufacturers and infrastructure technology providers.

China – Holds approximately 31% share of the global HVAC Pump market due to large-scale manufacturing capacity, rapid smart-city expansion, and strong commercial infrastructure deployment.

United States – Accounts for nearly 24% share of the HVAC Pump market driven by advanced retrofit demand, data center cooling investments, and widespread adoption of intelligent HVAC technologies.

The HVAC pump market is defined by intense competition between global engineering leaders, regional manufacturing specialists, and digitally focused HVAC technology providers. Major players including Grundfos, Xylem, Wilo, KSB, and Armstrong Fluid Technology collectively control nearly 46% of global market activity, competing aggressively across commercial infrastructure, district cooling, and industrial HVAC modernization projects. Competition is increasingly shifting from price-based procurement toward energy optimization, predictive maintenance integration, and localized supply-chain execution. Advanced variable-speed systems improve operational efficiency by nearly 25%, while digitally connected monitoring platforms reduce maintenance downtime by approximately 18%, forcing rapid technology adoption across the competitive landscape. Global manufacturers are expanding localized assembly operations, strengthening software partnerships, and vertically integrating motor and control-system production to secure delivery reliability and compliance advantages. Rising component costs and advanced software integration requirements are increasing entry barriers. Winning increasingly depends on intelligent system integration, regional execution capability, lifecycle efficiency performance, and infrastructure-scale service support.

Grundfos

Xylem Inc.

Wilo Group

KSB SE & Co. KGaA

Armstrong Fluid Technology

Taco Comfort Solutions

Pentair plc

Danfoss

Sulzer Ltd.

Ebara Corporation

ITT Inc.

Kirloskar Brothers Limited

Flowserve Corporation

SPX FLOW Inc.

Advanced variable-speed pumping systems and electronically commutated motor technologies are currently reshaping HVAC infrastructure efficiency across commercial buildings, hospitals, and data centers. Intelligent circulation systems reduce electricity consumption by nearly 25% while improving flow precision by 18% compared to conventional fixed-speed pumps. More than 52% of newly installed commercial HVAC systems now integrate smart control platforms with predictive monitoring capabilities. This shift is optimizing energy performance, lowering maintenance intervention frequency, and strengthening lifecycle cost competitiveness for infrastructure operators managing large-scale cooling and heating environments.

Emerging technologies including AI-driven flow optimization, IoT-enabled remote diagnostics, and digital twin simulation platforms are accelerating operational transformation between 2026 and 2028. Connected HVAC pumping networks reduce unplanned downtime by approximately 21% and improve maintenance response efficiency by 16%. Manufacturers are integrating cloud-based monitoring ecosystems into commercial HVAC portfolios to secure recurring service contracts and improve operational visibility. Companies with advanced software integration capabilities are gaining stronger positioning across retrofit-intensive smart-building modernization projects and district cooling infrastructure deployments.

Disruptive compact modular pumping systems and magnetic-drive technologies are redefining installation flexibility and operational reliability within constrained infrastructure environments. Compared with legacy large-footprint systems, modular integrated pumps reduce installation space requirements by nearly 19% and shorten deployment timelines by 14%. More than 34% of high-density urban retrofit projects now prioritize compact digitally integrated HVAC pump configurations. Manufacturers accelerating investment in low-noise intelligent systems, regional automation capabilities, and cybersecurity-enabled controls are capturing higher-margin commercial modernization contracts and long-cycle infrastructure partnerships.

February 2025 – Grundfos launched advanced MIXIT and IE5 HVAC pump solutions targeting district cooling and data center infrastructure, improving energy efficiency by nearly 20% across commercial cooling applications. The expansion strengthened the company’s intelligent cooling portfolio amid rising urban infrastructure demand in Asia. [Smart Cooling Shift] Source: Everything About Water

June 2025 – Grundfos expanded its Commercial Building Services portfolio in India with energy-efficient HVAC pumping systems optimized for healthcare, hospitality, and data centers. The rollout targeted commercial cooling demand rising by 15%–20% annually, accelerating localized deployment and strengthening regional infrastructure positioning. [Localized Expansion Push] Source: Commercial Design India

January 2026 – Wilo accelerated deployment of IoT-enabled remote monitoring platforms for HVAC and industrial pump systems, enabling real-time diagnostics and predictive maintenance optimization. The digital service platform improved maintenance efficiency while supporting scalable remote infrastructure management across connected commercial facilities globally. [Digital Service Integration] Source: IoT Use Case

July 2024 – Wilo introduced the Wilo-TP Control intelligent monitoring system for water and HVAC infrastructure applications in the Middle East, improving operational reliability and process optimization through digitally integrated control functions. The solution aligned with regional sustainability modernization initiatives and strengthened smart infrastructure deployment capabilities. [Intelligent Control Upgrade] Source: Zawya

This HVAC pump market report delivers comprehensive coverage across core product categories including centrifugal pumps, circulator pumps, booster pumps, condensate pumps, and variable speed pumps, alongside key applications such as heating systems, cooling systems, chilled water circulation, and commercial HVAC operations. The report evaluates demand across residential buildings, commercial infrastructure, industrial facilities, healthcare institutions, hospitality environments, and educational campuses. Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with strategic assessment of regional manufacturing shifts, smart infrastructure deployment, and energy-efficiency modernization trends.

The study analyzes more than 20 operational market indicators including adoption penetration, deployment intensity, infrastructure modernization activity, and intelligent HVAC integration trends. Variable-speed and digitally monitored HVAC systems now represent over 52% of new commercial installations, while retrofit-focused cooling applications account for nearly 36% of infrastructure upgrades globally. The report also profiles major HVAC pump manufacturers, competitive technology positioning, supply-chain restructuring strategies, and emerging software-enabled service models shaping operational differentiation.

From 2026 to 2033, the report provides forward-looking analysis on AI-driven HVAC optimization, IoT-connected pumping platforms, modular compact systems, and district cooling infrastructure expansion. It supports investment planning, regional expansion decisions, supplier benchmarking, and competitive positioning through measurable operational and adoption-focused insights.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3674 Million |

|

Market Revenue in 2033 |

USD 5106 Million |

|

CAGR (2026 - 2033) |

4.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Grundfos, Xylem Inc., Wilo Group, KSB SE & Co. KGaA, Armstrong Fluid Technology, Taco Comfort Solutions, Pentair plc, Danfoss, Sulzer Ltd., Ebara Corporation, ITT Inc., Kirloskar Brothers Limited, Flowserve Corporation, SPX FLOW Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |