Reports

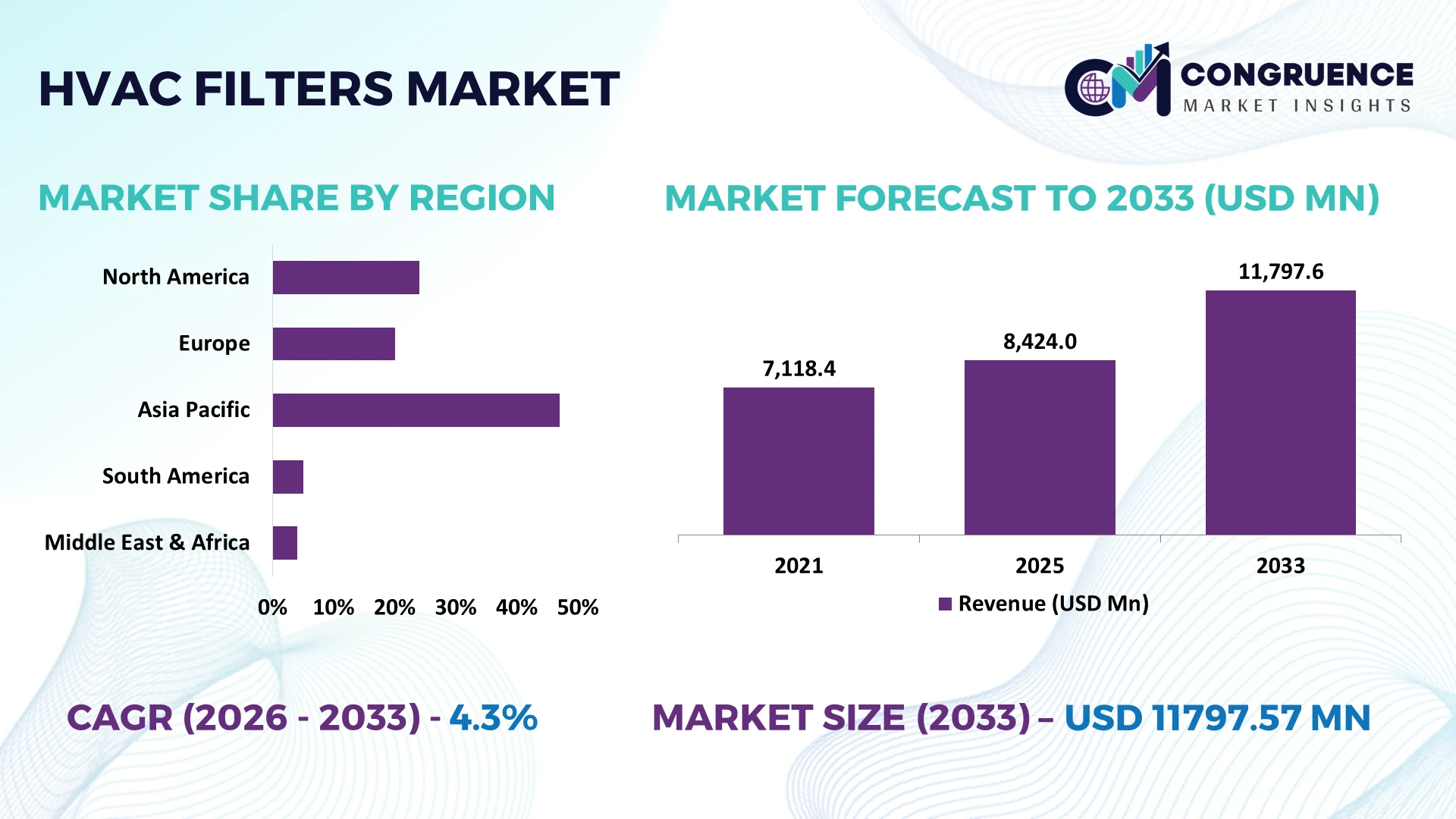

The Global HVAC Filters Market was valued at USD 8424 Million in 2025 and is anticipated to reach a value of USD 11797.57 Million by 2033 expanding at a CAGR of 4.3% between 2026 and 2033. Growth is driven by stricter indoor air quality standards, commercial building retrofits, smart HVAC integration, and rising deployment of high-efficiency filtration systems across healthcare, manufacturing, and data center infrastructure.

The United States remains the dominant country, accounting for approximately 31% of global HVAC filter demand, supported by extensive commercial infrastructure, healthcare facilities, and advanced manufacturing investments exceeding USD 50 billion annually in industrial modernization. Compared with Germany, where industrial filtration adoption exceeds 70% across large manufacturing sites, the U.S. benefits from broader smart-building integration and accelerated replacement cycles. Ongoing supply-chain diversification following global trade realignments in 2026 has strengthened domestic production capacity and improved premium filter availability.

Businesses prioritizing regional manufacturing partnerships and high-performance filtration portfolios are positioned to secure long-term procurement opportunities in high-value commercial and industrial applications.

Market Size & Growth: USD 8424 Million in 2025, reaching USD 11797.57 Million by 2033 at 4.3% CAGR, supported by smart building upgrades and high-efficiency filtration deployment.

Top Growth Drivers: Indoor air quality initiatives (+28%), commercial retrofit activity (+22%), and industrial clean-air investments (+19%) continue accelerating global demand.

Short-Term Forecast: By 2027, predictive maintenance and optimized filtration systems reduce maintenance costs by nearly 15% while improving HVAC energy efficiency by approximately 12%.

Emerging Technologies: AI-enabled monitoring, antimicrobial filter media, and nanofiber filtration improve operational performance and extend replacement intervals by up to 25%.

Regional Leaders: North America exceeds USD 3.8 billion, Asia-Pacific approaches USD 3.3 billion, and Europe surpasses USD 2.5 billion, driven by commercial retrofits, manufacturing expansion, and energy-efficiency adoption.

Consumer/End-User Trends: More than 60% of large commercial facilities prioritize premium filtration solutions to improve indoor air quality and optimize building performance.

Pilot/Case Example: A 2026 smart-building upgrade achieved approximately 18% lower energy consumption through intelligent HVAC filter monitoring and optimized maintenance scheduling.

Competitive Landscape: Leading manufacturers collectively control nearly 45% of the market, with companies including Camfil, Donaldson, Parker Hannifin, Freudenberg, and AAF International strengthening advanced filtration portfolios.

Regulatory & ESG Impact: High-efficiency filtration programs improve particulate capture by over 30%, supporting energy optimization and stricter sustainability compliance across commercial facilities.

Investment & Funding: More than USD 2 billion in manufacturing expansion and strategic partnerships supports regional production diversification amid evolving global supply-chain strategies.

Innovation & Future Outlook: Next-generation recyclable filter materials, IoT-enabled diagnostics, and digital lifecycle management accelerate the shift toward intelligent, high-performance HVAC filtration ecosystems.

Growing demand across healthcare, semiconductor manufacturing, pharmaceutical production, commercial buildings, and hyperscale data centers continues to reshape the HVAC Filters Market. Advanced nanofiber media and IoT-enabled condition monitoring improve filtration efficiency by over 20% while extending maintenance intervals. Regulatory emphasis on indoor air quality and continued regional supply-chain localization in 2026 are accelerating premium product adoption, setting the stage for broader strategic market evaluation.

The HVAC Filters Market has become strategically important as indoor air quality, energy optimization, and infrastructure modernization move to the center of corporate investment decisions. Commercial property owners, healthcare providers, semiconductor manufacturers, and data center operators increasingly prioritize advanced filtration to improve operational continuity while complying with stricter air quality requirements. In 2026, continued supply-chain restructuring has encouraged manufacturers to localize production and diversify component sourcing, reducing procurement delays and strengthening resilience across industrial filtration networks.

Advanced nanofiber and electrostatic filtration systems capture finer particulate matter while lowering airflow resistance by nearly 18% compared with conventional fiberglass filters, reducing fan energy consumption by approximately 12%. The United States leads large-scale deployment through smart commercial buildings and healthcare modernization, whereas Japan emphasizes precision filtration for electronics and pharmaceutical manufacturing. Over the next two to three years, digital filter monitoring adoption is expected to exceed 40% among large commercial facilities, enabling predictive maintenance and more efficient replacement planning.

A practical example is the deployment of IoT-enabled filtration management in hyperscale data centers, where continuous monitoring minimizes downtime and optimizes maintenance scheduling. Manufacturers are expanding partnerships with HVAC system integrators, investing in recyclable filter materials, and strengthening domestic production capabilities. Organizations that combine intelligent filtration technologies with resilient manufacturing strategies will secure stronger competitive positioning, lower operating costs, and long-term differentiation in premium air quality solutions.

Healthcare campuses, semiconductor fabrication plants, pharmaceutical facilities, and commercial buildings are accelerating investments in advanced HVAC filtration as indoor air quality becomes a measurable operational priority. More than 65% of new commercial projects specify higher-efficiency filtration, while smart building platforms improve maintenance productivity by approximately 20%. In the United States, updated building modernization initiatives continue driving premium filter replacement cycles, encouraging manufacturers to expand local production capacity. This structural shift improves procurement stability, strengthens aftermarket demand, and supports long-term service contracts. Companies are responding through automated manufacturing, product innovation, and strategic partnerships with HVAC equipment providers to deliver integrated filtration solutions with lower lifecycle costs.

Volatility in synthetic fiber, specialty media, and resin supplies continues to pressure production economics, with raw material costs fluctuating by approximately 12–18% across procurement cycles. Premium filtration products remain 20% to 30% more expensive than conventional alternatives, slowing adoption among cost-sensitive facilities. China-dependent component sourcing has also exposed manufacturers to logistics disruptions and longer procurement lead times during supply-chain adjustments. These constraints reduce pricing flexibility and compress operating margins. Companies are mitigating risk by localizing production, securing long-term supplier agreements, and introducing modular filter designs that reduce material consumption while maintaining filtration performance and product consistency.

Digital monitoring, recyclable filtration media, and AI-enabled maintenance platforms are creating high-value opportunities beyond traditional replacement sales. Intelligent filter management reduces unplanned maintenance by nearly 25%, while recyclable filter designs decrease disposal waste by approximately 30%. Germany is expanding industrial deployment of connected HVAC infrastructure across manufacturing facilities, encouraging suppliers to integrate sensors and predictive analytics into premium product portfolios. Manufacturers are increasing R&D investment, collaborating with automation companies, and developing subscription-based maintenance services. This transition shifts competition from component supply toward long-term performance management, creating stronger customer retention and differentiated lifecycle value.

Deploying connected filtration systems across aging commercial infrastructure remains operationally complex because legacy HVAC equipment often lacks compatibility with digital monitoring platforms. Nearly 40% of existing commercial buildings require significant control-system upgrades before intelligent filtration can be fully implemented, while skilled HVAC automation specialists remain in limited supply. In the United Kingdom, retrofit projects frequently experience extended commissioning periods due to integration complexity between legacy mechanical systems and modern building management software. Companies must invest in interoperable platforms, workforce training, standardized communication protocols, and scalable retrofit solutions to achieve consistent deployment quality while maintaining operational efficiency and long-term competitiveness.

Smart Filter Performance Monitoring Intelligent filter monitoring is becoming standard across large commercial facilities, with connected HVAC deployments increasing by approximately 34% and predictive maintenance reducing unexpected service events by nearly 22%. Labor shortages and digital building management adoption are accelerating automated monitoring, prompting manufacturers to integrate IoT sensors and cloud-based diagnostics into premium filtration portfolios while expanding software partnerships.

Localized Manufacturing Expansion Manufacturers are restructuring production networks as supply-chain diversification continues across the United States and India. Domestic sourcing has increased by roughly 18%, while procurement lead times have declined by nearly 15% through regional manufacturing expansion. Companies are strengthening supplier ecosystems, increasing inventory resilience, and establishing localized assembly operations to improve delivery reliability and customer responsiveness.

Advanced Sustainable Filter Materials Recyclable media, synthetic nanofibers, and low-pressure-drop designs are gaining commercial acceptance, improving filtration efficiency by around 20% while lowering energy consumption by approximately 12%. Tighter environmental compliance and corporate sustainability targets are driving this transition. Companies are scaling recyclable product lines, redesigning manufacturing processes, and collaborating with material specialists to improve lifecycle performance without compromising operational reliability.

Precision Filtration for Critical Facilities Semiconductor fabrication plants, healthcare campuses, and hyperscale data centers are increasing deployment of premium filtration systems, with high-efficiency filter installations expanding by nearly 26% and contamination-related maintenance events declining by approximately 17%. A notable operational shift is the integration of filtration performance into facility management software, encouraging suppliers to develop intelligent service contracts and performance-based maintenance models.

HEPA filters lead the HVAC Filters Market with an estimated 36% market share, supported by superior particulate removal performance, regulatory compliance, and widespread deployment across healthcare, pharmaceuticals, and high-tech manufacturing. Their ability to integrate into advanced HVAC systems while maintaining strict air quality requirements makes them the preferred premium solution. Electrostatic filters represent the fastest-growing category as reusable designs, lower operating costs, and smart-building compatibility encourage broader commercial adoption. Manufacturers continue expanding high-efficiency product portfolios while investing in advanced filter media innovation.

Pleated filters remain the largest mainstream replacement option because they balance filtration efficiency with competitive lifecycle costs, making them widely adopted in commercial and residential buildings. Activated carbon filters continue gaining importance where odor and gaseous contaminant control are operational priorities, while fiberglass filters retain relevance in budget-sensitive applications despite gradual market share erosion. Approximately 48% of commercial replacement demand now favors higher-efficiency filtration products, encouraging companies to strengthen manufacturing capacity, expand premium product offerings, and establish strategic distribution partnerships targeting performance-driven customers.

Commercial applications account for approximately 39% of total HVAC filter demand due to extensive deployment across office buildings, retail complexes, educational institutions, and hospitality facilities requiring continuous indoor air quality management. Data centers represent the fastest-growing application as hyperscale computing infrastructure expands and contamination control becomes operationally critical. Intelligent facility management platforms have improved maintenance scheduling by nearly 20%, encouraging operators to standardize premium filtration across mission-critical assets. Suppliers are scaling production, integrating digital monitoring, and strengthening partnerships with commercial HVAC system providers.

Healthcare facilities continue increasing demand for high-efficiency filtration to support infection prevention and regulatory compliance, while industrial facilities prioritize dust control and equipment protection. Residential applications maintain stable replacement demand through growing consumer awareness of indoor air quality. Data centers now specify premium filtration in over 70% of newly commissioned hyperscale facilities, prompting manufacturers to customize filtration products for precision cooling environments and long-term operational reliability.

Commercial buildings represent the largest end-user group with approximately 41% market share, supported by large installed HVAC infrastructure, mandatory maintenance schedules, and increasing indoor air quality requirements. Data centers are the fastest-growing end-user segment as digital infrastructure expansion requires continuous environmental control and contamination prevention. Around 32% of enterprise facility managers are accelerating investments in connected filtration management platforms to improve operational efficiency and reduce maintenance interruptions. Manufacturers are responding through customized filtration packages, digital service offerings, and long-term maintenance agreements.

Residential buildings continue generating stable replacement demand through routine HVAC servicing, while manufacturing facilities prioritize filtration to protect sensitive production equipment and maintain workplace safety. Healthcare facilities increasingly specify premium air filtration for critical care environments, encouraging suppliers to develop application-specific product ranges. Companies are differentiating through tailored pricing strategies, integrated building management compatibility, and strategic partnerships that strengthen recurring aftermarket relationships across high-value customer segments.

North America accounted for the largest market share at 35.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 5.4% CAGR between 2026 and 2033.

Strategic Building Modernization Strengthens Premium Filtration Demand

North America remains the largest regional market, supported by extensive commercial infrastructure, advanced healthcare networks, hyperscale data centers, and strict indoor air quality standards. Large-scale retrofit programs continue replacing conventional filtration with high-efficiency solutions integrated into smart building management platforms. Nearly 68% of premium commercial HVAC projects now specify higher-performance filtration systems, while predictive maintenance deployment has reduced unscheduled service requirements by approximately 20%. Manufacturers are expanding automated production capacity and strengthening partnerships with HVAC equipment providers to improve supply reliability. Continuous investment in pharmaceutical manufacturing, semiconductor facilities, and mission-critical infrastructure further reinforces demand for advanced filtration technologies designed to maximize operational efficiency and equipment protection.

United States Market Outlook: The United States leads regional demand through its extensive installed HVAC base, strong commercial construction activity, and rapid modernization of healthcare and data center infrastructure. More than 70% of newly commissioned hyperscale facilities incorporate premium air filtration systems with digital monitoring capabilities. Domestic manufacturers continue expanding localized production, automation, and enterprise partnerships to improve delivery performance while supporting increasingly stringent indoor air quality requirements across institutional and industrial facilities.

Sustainability Standards Accelerate High-Efficiency Filtration Adoption

Europe maintains a strong position through energy-efficient building modernization, industrial sustainability initiatives, and stringent environmental regulations. Approximately 29% of global premium filtration deployment is concentrated across European commercial and industrial facilities, where lifecycle efficiency increasingly influences procurement decisions. Manufacturers are introducing recyclable filter materials, lower-pressure-drop media, and digitally connected maintenance solutions to reduce operating costs. Building renovation programs continue supporting replacement demand, while advanced manufacturing sectors strengthen adoption of precision filtration systems. Strategic collaboration between HVAC equipment suppliers and automation companies is improving integrated building performance while supporting long-term operational sustainability across commercial infrastructure.

Germany Market Outlook: Germany serves as the region's primary industrial hub, supported by advanced manufacturing, pharmaceutical production, and engineering excellence. More than 72% of large industrial facilities utilize high-efficiency HVAC filtration for production quality and workplace compliance. Companies continue investing in automated manufacturing, sustainable filtration materials, and smart factory integration, positioning the country as a technology leader in premium filtration innovation and industrial deployment.

Manufacturing Scale and Infrastructure Expansion Drive Deployment

Asia-Pacific represents the fastest-expanding regional market as industrialization, urban infrastructure development, and commercial construction continue accelerating HVAC installation activity. The region contributes approximately 33% of global manufacturing capacity for HVAC filtration products, supported by expanding production ecosystems and competitive component supply chains. New semiconductor plants, electronics manufacturing facilities, and healthcare infrastructure projects continue increasing demand for high-performance filtration systems. Manufacturers are expanding regional production facilities, investing in automation, and strengthening distribution networks to improve delivery speed while supporting growing domestic and export demand.

China Market Outlook: China remains the region's largest production and consumption center through its extensive manufacturing ecosystem, commercial construction pipeline, and electronics industry expansion. Industrial automation continues increasing demand for advanced filtration across precision manufacturing facilities, while domestic producers are expanding capacity and upgrading production technologies. More than 60% of large electronics manufacturing facilities have implemented higher-efficiency HVAC filtration to improve contamination control and operational consistency.

Commercial Modernization Supports Stable Market Expansion

South America is experiencing gradual demand growth through commercial infrastructure upgrades, healthcare modernization, and expanding food processing industries. Approximately 18% of new commercial HVAC installations now incorporate higher-efficiency filtration systems as facility operators prioritize energy optimization and indoor environmental quality. Although infrastructure investment varies across countries, multinational manufacturers continue strengthening local distribution partnerships and regional inventory networks to improve product availability. Industrial maintenance programs and replacement demand remain the primary market drivers, while localized assembly operations help reduce procurement lead times and improve customer responsiveness.

Brazil Market Outlook: Brazil represents the largest national market due to its broad commercial building stock, expanding healthcare infrastructure, and diversified industrial base. Large metropolitan areas continue increasing investment in modern HVAC systems for office complexes, hospitals, and manufacturing facilities. Approximately 24% of commercial retrofit projects now include upgraded filtration solutions, encouraging suppliers to expand technical support capabilities and localized distribution partnerships.

Infrastructure Investment Fuels Premium Air Quality Solutions

The Middle East & Africa market is strengthening through large-scale infrastructure investment, airport expansion, healthcare construction, and commercial real estate development. High ambient temperatures and demanding operating environments increase reliance on durable, high-performance HVAC filtration systems. More than 35% of newly developed premium commercial facilities specify advanced filtration integrated with intelligent building management platforms. Companies are expanding regional service networks, establishing strategic partnerships, and introducing products optimized for harsh climatic conditions. Continued investment in tourism, logistics, and smart-city developments supports sustained deployment of premium HVAC technologies across major infrastructure projects.

Saudi Arabia Market Outlook: Saudi Arabia leads regional market activity through extensive infrastructure investment, industrial diversification, and large-scale commercial development initiatives. Modern healthcare facilities, hospitality projects, and mixed-use developments continue driving advanced HVAC deployment. Approximately 40% of major new commercial projects incorporate smart building technologies with integrated filtration management, encouraging manufacturers to expand local technical services, regional warehousing, and enterprise collaboration initiatives.

The HVAC Filters Market is led by Camfil, AAF International, Donaldson Company, Freudenberg Filtration Technologies, and Parker Hannifin, competing directly with regional manufacturers on performance, delivery capability, and lifecycle value. The top five players collectively control approximately 44% of global demand, while regional suppliers compete aggressively through localized production and pricing flexibility. Premium manufacturers emphasize advanced filtration media delivering up to 20% lower pressure drop and extending service intervals by nearly 25%, whereas cost-focused suppliers prioritize standardized products and rapid fulfillment. Competition increasingly centers on digital monitoring, customized filtration, resilient supply chains, and application-specific engineering rather than unit pricing alone. Companies are expanding manufacturing capacity, strengthening OEM partnerships, investing in recyclable filter technologies, and integrating predictive maintenance capabilities into filtration portfolios. Industry consolidation and supply-chain localization continue raising entry barriers because premium media expertise, certification requirements, and established distribution networks are difficult to replicate. Success increasingly depends on combining technological differentiation, manufacturing resilience, application expertise, and responsive aftermarket service with scalable production efficiency.

Camfil

AAF International

Donaldson Company

Freudenberg Filtration Technologies

Parker Hannifin

MANN+HUMMEL

Koch Filter

Filtration Group

American Air Filter

Trox GmbH

Nordic Air Filtration

Purafil

MayAir Group

AIRTECH Japan Ltd.

Advanced filtration technology is rapidly shifting from passive air cleaning toward intelligent performance management. Nanofiber filter media, antimicrobial coatings, and low-pressure-drop designs improve particle capture while reducing airflow resistance by approximately 18% and lowering HVAC energy consumption by nearly 12%. More than 40% of newly specified premium commercial filtration systems now incorporate high-efficiency media optimized for extended operational life. Healthcare providers, semiconductor manufacturers, and hyperscale data centers benefit most because contamination control directly affects operational continuity and equipment reliability.

Connected filtration is becoming a competitive differentiator through IoT-enabled sensors, cloud analytics, and predictive maintenance platforms. Compared with conventional time-based replacement schedules, intelligent monitoring reduces unnecessary filter replacements by nearly 22% while improving maintenance planning accuracy by approximately 30%. Building owners increasingly integrate filtration diagnostics into centralized building management systems, enabling continuous performance optimization. Manufacturers with digital service capabilities gain stronger aftermarket retention through performance-based maintenance contracts and lifecycle management solutions.

Between 2026 and 2028, recyclable filtration materials, AI-driven airflow optimization, and digital twin integration will redefine product development priorities. Companies investing early in intelligent filtration ecosystems, automation, and sustainable manufacturing will secure stronger enterprise partnerships, faster product qualification, and higher-value commercial contracts as procurement increasingly prioritizes measurable operational performance over conventional replacement-based purchasing.

March 2025 MANN+HUMMEL opened a new manufacturing facility in Kempton Park, South Africa, adding a 3,200-square-meter production site to strengthen regional filtration supply. The expansion improves local manufacturing capacity, shortens delivery timelines, and enhances customer support across Southern Africa.

February 2026 Donaldson Company introduced ArmorSeal™ air filtration technology for heavy-duty equipment, engineered to improve seal integrity and durability under demanding operating conditions. The innovation targets higher vibration and dust environments, strengthening product reliability and reinforcing Donaldson's premium filtration portfolio. Source: donaldson.com

January 2026 MANN+HUMMEL announced its long-term filtration innovation strategy, supported by more than 250 filtration-media patents and operations across 80+ global locations. The initiative accelerates investment in digital platforms and advanced filtration materials, strengthening competitive leadership in industrial and air filtration.

June 2026 MANN+HUMMEL confirmed the rollout of sustainable filtration innovations for Automechanika Frankfurt, highlighting next-generation filtration technologies across three product brands. The product strategy strengthens sustainable filtration adoption and expands advanced solution availability for global aftermarket customers. Source: mann-filter.com

The report provides a comprehensive assessment of the HVAC Filters Market across major product types, including Fiberglass, Pleated, HEPA, Electrostatic, and Activated Carbon filters, while evaluating demand across Residential, Commercial, Industrial, Healthcare, and Data Center applications. It further examines purchasing trends among Residential Buildings, Commercial Buildings, Manufacturing, Healthcare Facilities, and Data Centers across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of premium commercial installations now emphasize high-efficiency filtration integrated with intelligent building management systems.

The study analyzes competitive positioning, technology evolution, manufacturing strategies, supply-chain developments, regulatory influences, and regional deployment patterns shaping the market between 2026 and 2033. It evaluates advanced filtration media, IoT-enabled monitoring, predictive maintenance, recyclable materials, and automation trends while profiling leading industry participants. The report supports investment planning, product development, geographic expansion, partnership evaluation, portfolio optimization, and long-term competitive decision-making through actionable operational and strategic market intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 8424 Million |

Market Revenue in 2033 | USD 11797.57 Million |

CAGR (2026 - 2033) | 4.3% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Camfil, AAF International, Donaldson Company, Freudenberg Filtration Technologies, Parker Hannifin, MANN+HUMMEL, Koch Filter, Filtration Group, American Air Filter, Trox GmbH, Nordic Air Filtration, Purafil, MayAir Group, AIRTECH Japan Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |