Reports

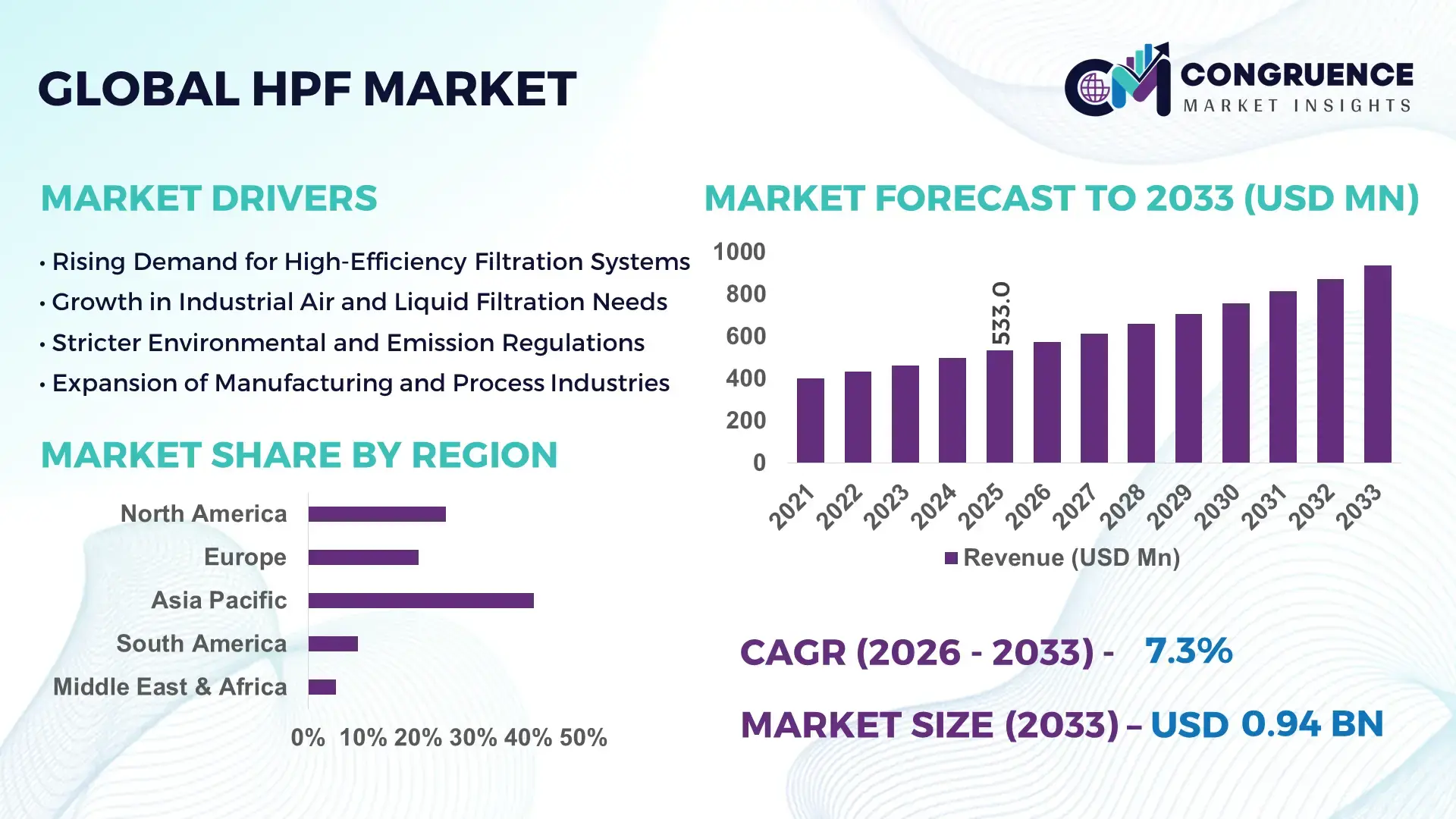

The Global HPF Market was valued at USD 533 Million in 2025 and is anticipated to reach a value of USD 936.53 Million by 2033 expanding at a CAGR of 7.3% between 2026 and 2033. Increasing deployment of high-performance filtration solutions across industrial processing, water treatment, and energy sectors is strengthening long-term market demand.

China operates large-scale HPF production facilities with annual output exceeding 120,000 metric tons and has invested more than USD 1.2 billion in advanced filtration manufacturing upgrades. Nearly 48% of major industrial wastewater treatment plants in the country utilize HPF-based systems integrated with automated monitoring and high-efficiency processing technologies.

Market Size & Growth: Valued at USD 533 Million in 2025 and projected to reach USD 936.53 Million by 2033 at a CAGR of 7.3%, supported by rising demand for industrial-grade filtration efficiency and environmental compliance solutions.

Top Growth Drivers: Industrial filtration adoption 38%, wastewater treatment modernization 31%, efficiency improvements in advanced filtration materials 26%.

Short-Term Forecast: By 2028, HPF-enabled filtration systems are expected to improve operational performance by 22% and reduce maintenance costs by around 17% across large-scale industrial facilities.

Emerging Technologies: Nano-fiber membrane engineering, AI-driven filtration monitoring systems, and hybrid polymer composite filters enhancing durability and lifecycle performance.

Regional Leaders: Asia Pacific projected to reach USD 365 Million by 2033 with rapid industrial adoption; North America USD 241 Million supported by advanced manufacturing investments; Europe USD 198 Million driven by environmental infrastructure upgrades.

Consumer/End-User Trends: Chemical processing companies, energy utilities, and industrial water treatment operators are increasingly adopting high-efficiency HPF solutions to improve process reliability and reduce filtration replacement cycles.

Pilot or Case Example: In 2024, an industrial filtration upgrade pilot recorded a 19% reduction in operational downtime and a 24% increase in filtration throughput using advanced HPF modules.

Competitive Landscape: Leading manufacturer holds approximately 18% market presence, while several global filtration technology companies and specialty material producers continue expanding production capacity and innovation pipelines.

Regulatory & ESG Impact: Strengthening wastewater treatment policies, emission reduction targets, and sustainability compliance requirements are accelerating the integration of advanced filtration materials across industries.

Investment & Funding Patterns: More than USD 820 Million has been invested in filtration technology upgrades, new production facilities, and research initiatives focused on next-generation high-performance filtration materials.

Innovation & Future Outlook: Smart filtration infrastructure, advanced polymer fiber development, and digital performance monitoring are shaping the next phase of scalable HPF deployment across industrial ecosystems.

The HPF market is strongly influenced by industrial water treatment, chemical manufacturing, and power generation sectors, which together contribute a substantial share of total demand. Ongoing innovation in nano-structured filtration media, high-durability polymer filters, and automated monitoring systems is improving efficiency and lifecycle performance. Regulatory pressure on emissions and wastewater discharge, particularly across Asia Pacific and Europe, is accelerating adoption. Increasing industrialization, sustainability initiatives, and infrastructure upgrades are expected to support steady long-term expansion of high-performance filtration technologies.

The HPF market holds strategic importance across industrial manufacturing, water treatment, chemicals, and power generation where advanced filtration reliability directly impacts operational continuity and compliance targets. Companies are prioritizing high-efficiency filtration deployment to reduce system downtime and optimize resource utilization. Nano-fiber filtration technology delivers 28% improvement compared to conventional microfiber filtration systems in contaminant capture efficiency and operational lifespan. Asia Pacific dominates in volume, while North America leads in adoption with nearly 42% of large enterprises integrating advanced HPF monitoring solutions into industrial filtration infrastructure. By 2028, AI-enabled filtration diagnostics are expected to cut maintenance downtime by 25% through predictive monitoring and automated system optimization. Firms are committing to sustainability improvements such as 30% wastewater recycling targets by 2030 through advanced filtration upgrades. In 2024, Germany achieved a 21% reduction in industrial filtration energy consumption through digital filtration optimization initiatives implemented across large processing plants. As industries move toward resilient infrastructure and environmentally responsible production, the HPF market is positioned as a critical pillar supporting operational stability, regulatory alignment, and long-term sustainable industrial growth.

Rapid expansion of industrial wastewater treatment infrastructure is significantly increasing demand for high-performance filtration solutions. More than 52% of new large-scale manufacturing facilities globally now incorporate advanced filtration modules to meet strict discharge standards and water reuse goals. Industries such as chemicals, textiles, and energy production are installing multi-stage filtration systems capable of removing micro-particles and hazardous contaminants. Governments across major industrial economies have introduced stricter discharge thresholds, prompting companies to modernize treatment plants and integrate durable filtration media. High-performance filtration systems are capable of improving contaminant removal efficiency by up to 30% compared with older filtration designs, making them a preferred solution in industrial modernization projects. Additionally, rapid urbanization and increasing industrial water consumption are encouraging investments in sustainable water treatment technologies, which directly supports expansion of advanced filtration deployments in both public and private sector infrastructure.

The deployment of high-performance filtration systems often involves complex installation requirements and integration challenges within existing industrial infrastructure. Many legacy facilities operate with outdated piping systems and filtration frameworks that require extensive modifications before HPF solutions can be installed effectively. Upgrading industrial plants to accommodate advanced filtration modules may require equipment replacement cycles lasting 12 to 24 months, leading to temporary operational disruptions. Additionally, high-precision filtration materials require specialized handling and calibration, increasing training requirements for technical staff. In some regions, limited availability of skilled technicians capable of managing automated filtration systems further slows implementation. Maintenance complexity is another concern, as advanced filtration units often operate under high pressure and require periodic inspection to maintain optimal performance. These integration barriers and operational adjustments can delay adoption among small and mid-sized industrial facilities.

The integration of digital monitoring technologies with high-performance filtration systems presents significant opportunities for industrial efficiency improvements. Smart filtration platforms equipped with sensors and predictive analytics can monitor pressure levels, contamination patterns, and filter lifespan in real time. Industrial facilities implementing digital filtration monitoring have reported operational efficiency improvements of up to 24% through predictive maintenance scheduling. Increasing adoption of Industry 4.0 frameworks is also encouraging manufacturers to integrate connected filtration systems that align with automated production environments. Emerging opportunities are particularly visible in sectors such as semiconductor manufacturing, pharmaceutical production, and advanced materials processing where ultra-clean operational environments are essential. In addition, growing investments in sustainable industrial infrastructure are supporting the development of recyclable filtration materials and energy-efficient filtration modules, which are expected to expand adoption among environmentally focused industrial operators.

One of the major challenges affecting the HPF market is the increasing cost of advanced filtration materials and compliance requirements tied to environmental regulations. High-performance filtration systems rely on specialized polymer fibers, composite membranes, and precision-engineered components that require advanced manufacturing processes. Fluctuations in raw material supply chains can influence production timelines and cost stability. Additionally, regulatory compliance for filtration systems used in industrial wastewater treatment and emissions control often requires extensive testing and certification before deployment. Certification procedures in certain industrial sectors can extend beyond 18 months, delaying technology adoption. Companies must also invest in monitoring systems and performance validation to meet strict environmental performance standards. These regulatory and material-related challenges require manufacturers to balance innovation with cost control while maintaining consistent product reliability across demanding industrial environments.

Rapid Deployment of Smart Filtration Systems Increasing Operational Efficiency: Industrial facilities are accelerating the adoption of sensor-enabled HPF systems capable of real-time monitoring and predictive maintenance. Approximately 46% of large manufacturing plants have integrated digital filtration controls, leading to a 23% improvement in equipment uptime and a 19% reduction in unplanned shutdowns. These intelligent filtration networks allow plant operators to track particulate levels and pressure variations across multiple processing units simultaneously. Adoption is particularly strong in high-throughput chemical processing hubs where production continuity and compliance monitoring are critical to operational performance.

Growing Demand from Industrial Water Reuse Initiatives: Increasing regulatory focus on water reuse and treatment is significantly boosting the installation of advanced HPF filtration infrastructure. Nearly 58% of new industrial wastewater facilities now include multi-layer high-performance filtration modules capable of removing micro-contaminants and heavy particulates. Facilities implementing advanced HPF filtration technologies have reported up to 27% improvement in water recovery efficiency. Industrial clusters in Asia and the Middle East are prioritizing water recycling strategies to manage rising consumption levels while maintaining consistent environmental compliance across large-scale production operations.

Adoption of High-Durability Polymer and Composite Filter Media: Manufacturers are increasingly shifting toward advanced polymer fiber and composite filtration materials designed to withstand extreme industrial conditions. Around 41% of newly installed filtration systems utilize reinforced HPF media capable of operating at pressure levels exceeding 25% higher than traditional filter units. These materials extend filtration lifecycle by nearly 30%, reducing replacement frequency and maintenance costs. The trend is particularly visible in energy production, metal processing, and heavy manufacturing industries where filtration systems operate under continuous high-load environments.

Rise in Modular and Prefabricated Industrial Filtration Infrastructure: Modular and prefabricated system deployment is reshaping installation strategies in the HPF market. Approximately 55% of newly constructed industrial treatment projects report cost efficiencies when using modular filtration units manufactured off-site. Automated fabrication processes enable precise assembly of filtration components, reducing installation timelines by nearly 35% and lowering labor requirements by about 22%. Demand for pre-engineered HPF systems is growing rapidly across Europe and North America where industries prioritize operational efficiency, infrastructure modernization, and faster commissioning of processing facilities.

The HPF market demonstrates diverse segmentation across filtration material types, industrial applications, and end-user industries, reflecting varied operational requirements. Product categories include polymer-based filtration media, ceramic filtration components, composite filter materials, and nano-fiber filtration systems designed for high-efficiency contaminant removal. Application demand is strongly influenced by wastewater treatment, chemical processing, power generation, and advanced manufacturing environments where contamination control and system reliability are critical. End-user adoption patterns indicate strong engagement from heavy industries and industrial utilities operating continuous production lines. Approximately 49% of large-scale industrial filtration installations are concentrated within manufacturing and processing sectors, while environmental infrastructure projects continue expanding filtration deployment in urban industrial zones. Increasing regulatory oversight, sustainability initiatives, and automation upgrades are further shaping how organizations select HPF technologies tailored to operational performance and long-term infrastructure resilience.

Product segmentation in the HPF market includes polymer-based filtration media, ceramic filtration systems, composite filter technologies, and nano-fiber filtration materials. Polymer-based HPF filtration currently accounts for approximately 44% of overall adoption due to its durability, flexibility in industrial environments, and compatibility with automated filtration systems. Ceramic filtration solutions represent around 27% of usage, particularly in high-temperature industrial processes and heavy manufacturing operations requiring heat-resistant filtration components. Composite filtration materials are gaining traction as they combine mechanical strength with improved filtration precision. Nano-fiber filtration technology is the fastest-growing segment, expanding at an estimated CAGR of 8.9% as industries seek ultra-fine particulate removal and improved filtration efficiency in advanced production facilities. Other specialized filtration types collectively contribute nearly 29% of market installations, serving niche industrial applications such as semiconductor manufacturing and pharmaceutical-grade filtration systems.

Applications of HPF systems are widely distributed across industrial wastewater treatment, chemical processing, power generation, oil and gas operations, and advanced manufacturing environments. Wastewater treatment leads application deployment with approximately 39% of total system installations, supported by increasing environmental compliance requirements and industrial water recycling initiatives. Chemical processing applications represent around 24% of the market due to the need for high-precision filtration to maintain process purity and equipment reliability. However, adoption in advanced manufacturing sectors such as electronics and semiconductor production is growing fastest, expanding at an estimated CAGR of 9.4% as facilities require ultra-clean production environments. Oil and gas operations, energy generation plants, and metal processing industries collectively account for nearly 37% of the remaining application demand, where HPF systems are essential for removing particulates and improving operational stability.

End-user adoption of HPF technologies is primarily driven by industrial manufacturing companies, environmental infrastructure operators, energy producers, and chemical processing enterprises. Industrial manufacturing leads the market with approximately 36% of system deployment due to continuous production processes that require reliable filtration performance and contamination control. Environmental utilities and water management organizations account for nearly 28% of adoption as governments expand industrial wastewater treatment infrastructure. However, the fastest-growing end-user segment is semiconductor and advanced electronics manufacturing, expanding at an estimated CAGR of 9.8% as cleanroom environments require ultra-high filtration accuracy and advanced particulate control. Other industries including pharmaceuticals, mining operations, and metal fabrication collectively represent about 36% of installations, reflecting diverse industrial filtration requirements across global production networks.

Asia Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

Asia Pacific’s dominance is supported by large-scale industrial manufacturing zones and expanding wastewater treatment capacity, with more than 62% of new industrial filtration installations occurring in China, India, and Southeast Asia. North America recorded approximately 28% of global HPF system deployments in 2025, driven by modernization of industrial plants and digital filtration monitoring upgrades across over 1,200 facilities. Europe followed with nearly 21% share, supported by strict environmental compliance policies and increased investment in advanced filtration infrastructure. South America accounted for about 6% of the market, while the Middle East & Africa collectively represented close to 4%, with increasing filtration demand linked to energy production, industrial expansion, and water treatment initiatives across emerging economies.

How are advanced industrial filtration upgrades transforming high-efficiency processing systems?

North America holds approximately 28% of the HPF market, supported by widespread industrial modernization and adoption of advanced filtration systems across manufacturing, chemical processing, and energy generation sectors. Over 54% of large industrial plants in the United States and Canada have implemented automated filtration monitoring technologies to enhance operational efficiency. Environmental regulations targeting industrial wastewater discharge limits have led to the installation of more than 850 upgraded filtration units in recent years. Digital transformation initiatives are encouraging integration of AI-driven predictive maintenance tools within filtration infrastructure, improving system uptime by nearly 20%. A notable regional player has expanded its high-performance filtration manufacturing capacity by 30% to meet increasing demand from energy and chemical industries. Regional consumer behavior shows higher enterprise adoption in sectors such as healthcare manufacturing and financial data center cooling infrastructure requiring contamination control systems.

What role do environmental compliance and advanced filtration technologies play in industrial modernization?

Europe accounts for nearly 21% of the HPF market, with major contributions from Germany, the United Kingdom, and France where industrial sustainability targets are accelerating filtration system upgrades. More than 47% of new industrial processing plants in Western Europe have integrated high-performance filtration solutions aligned with strict environmental discharge standards. Regional sustainability initiatives encourage recycling of industrial water, and over 38% of manufacturing facilities now operate filtration systems designed for resource recovery and emission control. Emerging technologies such as nano-fiber filtration and digital filtration monitoring platforms are increasingly deployed across chemical and pharmaceutical manufacturing hubs. A leading European filtration manufacturer recently introduced a new high-capacity filtration module designed to improve industrial contaminant removal efficiency by 25%. Consumer behavior across the region reflects strong regulatory-driven adoption, with industries prioritizing advanced filtration solutions to meet strict environmental compliance frameworks.

How are large-scale manufacturing ecosystems driving advanced filtration adoption?

Asia-Pacific represents the highest market volume globally, accounting for about 41% of total HPF installations, supported by rapid industrialization and infrastructure development. China, India, and Japan are the top consuming countries, collectively contributing more than 68% of regional filtration system demand. Manufacturing output expansion across electronics, chemical processing, and heavy industry has led to the installation of over 1,500 new industrial filtration units in recent years. Industrial parks across China alone operate more than 700 large-scale wastewater treatment facilities incorporating advanced filtration modules. Regional technology innovation hubs are focusing on automated filtration manufacturing, high-durability polymer filtration materials, and smart monitoring solutions. A prominent Asian filtration equipment manufacturer recently expanded its automated production lines by 35%, increasing supply capacity for industrial clients. Regional consumer behavior indicates strong demand from rapidly growing industrial clusters and infrastructure modernization programs.

How are industrial expansion and energy projects influencing filtration technology adoption?

South America accounts for roughly 6% of the HPF market, with Brazil and Argentina leading regional demand due to expanding industrial and energy infrastructure projects. More than 40% of newly developed processing plants in Brazil now integrate high-performance filtration systems to improve operational efficiency and environmental compliance. The region’s mining, oil refining, and power generation sectors are key drivers, collectively representing over 52% of filtration system installations. Government-backed industrial development programs have supported modernization of wastewater treatment facilities across several urban industrial zones. Trade policies encouraging equipment imports and technology upgrades have accelerated adoption of advanced filtration systems. A regional industrial filtration provider has recently increased production capacity by 20% to support infrastructure projects and energy sector expansion. Consumer behavior trends indicate growing demand from industrial operators seeking improved reliability and lower maintenance requirements in filtration systems.

How are industrial diversification and water management initiatives reshaping filtration demand?

The Middle East & Africa region holds approximately 4% of the HPF market, with increasing adoption driven by oil and gas processing, construction expansion, and water treatment investments. Countries such as the United Arab Emirates and South Africa are leading adoption of advanced filtration technologies to support industrial sustainability initiatives. Nearly 36% of large industrial facilities in the region have upgraded filtration systems to improve water reuse efficiency and reduce operational risks. Technological modernization is evident through the integration of automated filtration monitoring platforms and high-capacity filtration modules designed for harsh industrial environments. Trade partnerships and infrastructure development programs are encouraging investments in filtration equipment across industrial zones. A regional filtration technology supplier recently deployed new high-capacity systems across multiple energy processing plants, improving contaminant removal efficiency by 22%. Consumer behavior trends highlight increasing adoption among energy operators and infrastructure developers seeking long-term operational reliability.

China – Holds approximately 29% share in the HPF market due to large-scale industrial manufacturing capacity and extensive deployment of advanced wastewater treatment and filtration infrastructure.

United States – Accounts for around 24% share in the HPF market supported by strong demand from chemical processing, energy production, and advanced industrial automation sectors.

The HPF market demonstrates a moderately fragmented competitive environment with more than 45 active global and regional manufacturers competing across industrial filtration technologies, advanced materials, and smart monitoring systems. The top 5 companies collectively account for approximately 46% of total market presence, indicating a balanced mix of established leaders and specialized innovators. Major players are focusing on product innovation, capacity expansion, and digital integration strategies to strengthen their market positioning. Over the past two years, more than 18 new product launches related to high-efficiency filtration modules and nano-fiber filtration technologies have been introduced to address increasing industrial filtration requirements. Strategic collaborations between filtration manufacturers and industrial automation firms have increased by nearly 22%, enabling integration of predictive maintenance systems and AI-based monitoring tools within HPF solutions. Additionally, around 30% of leading companies are investing in new manufacturing facilities and automated production lines to improve supply chain resilience and reduce delivery timelines. Mergers and strategic acquisitions have also influenced competition, with at least 7 industry consolidation deals completed recently to expand regional market access and technology portfolios. Continuous R&D investment, which has increased by approximately 15% across major companies, is focused on improving filter durability, increasing contaminant capture efficiency, and developing sustainable filtration materials that align with stricter environmental compliance standards across industrial sectors.

Pall Corporation

Donaldson Company

MANN+HUMMEL

Eaton Corporation

Camfil

Ahlstrom

Freudenberg Filtration Technologies

SUEZ

Pentair

Filtration Group

Advanced filtration engineering and digital monitoring technologies are significantly transforming the HPF market across industrial sectors. Nano-fiber membrane technology has improved particulate capture efficiency by nearly 30% compared with traditional microfiber filtration systems, enabling removal of ultra-fine contaminants below 0.3 microns. Around 46% of newly installed industrial filtration systems now include embedded sensors capable of real-time pressure and contamination monitoring, allowing predictive maintenance cycles to reduce downtime by approximately 20%. High-durability polymer composite filtration materials are also gaining traction, extending operational lifespan by up to 28% in heavy manufacturing environments operating under high pressure and temperature conditions. Automated filtration manufacturing lines have increased production precision by nearly 35%, improving product consistency across large-scale installations. In addition, AI-assisted filtration analytics platforms are being integrated into industrial process control systems to optimize flow performance and reduce maintenance intervals. Emerging technologies such as hybrid ceramic-polymer filtration modules and recyclable filtration materials are also being tested across industrial wastewater facilities, where pilot deployments have demonstrated a 24% improvement in filtration reliability and improved sustainability metrics within high-volume industrial operations.

• In April 2025, Donaldson Company announced expansion of its advanced filtration manufacturing capacity in the United States, adding automated production lines designed to increase output efficiency by 25% and support growing demand from industrial processing and energy sector filtration applications. Source: www.donaldson.com

• In September 2024, MANN+HUMMEL introduced a next-generation industrial filtration solution focused on high-efficiency particulate removal for heavy manufacturing plants. The system demonstrated up to 20% improved contaminant capture performance during early industrial deployments across multiple European production facilities. Source: www.mann-hummel.com

• In February 2025, Pall Corporation launched an upgraded filtration monitoring platform integrating digital diagnostics and predictive maintenance capabilities, enabling industrial operators to reduce filtration system downtime by approximately 18% across large processing plants using smart filtration infrastructure. Source: www.pall.com

• In November 2024, Camfil expanded its high-performance filtration production capacity in Europe by opening a new manufacturing facility designed to increase supply for industrial air filtration systems and advanced environmental control solutions across manufacturing and energy industries. Source: www.camfil.com

The HPF Market Report provides a comprehensive analysis of the global market landscape, covering more than 20 countries across five major regions including North America, Europe, Asia Pacific, South America, and the Middle East & Africa. The report evaluates multiple filtration technologies such as nano-fiber membranes, polymer-based filtration materials, composite filtration systems, and smart monitoring platforms integrated with industrial infrastructure. Key application areas analyzed include industrial wastewater treatment, chemical processing, power generation, oil and gas operations, and advanced manufacturing environments where contamination control is critical.

The study also examines over 40 active manufacturers and technology providers participating in the HPF ecosystem, along with strategic initiatives such as product innovation, manufacturing expansion, and digital filtration integration. More than 15 industrial use cases and technology adoption patterns are assessed to understand operational efficiency improvements, filtration performance benchmarks, and sustainability initiatives including water recycling and emission control programs. The report further evaluates emerging niche segments such as smart filtration infrastructure, automated industrial filtration systems, and advanced materials designed for high-pressure industrial environments, offering decision-makers a structured view of evolving market opportunities and operational trends shaping the HPF industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Pall Corporation , Donaldson Company , MANN+HUMMEL, Eaton Corporation, Camfil, Ahlstrom, Freudenberg Filtration Technologies, SUEZ, Pentair, Filtration Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |