Reports

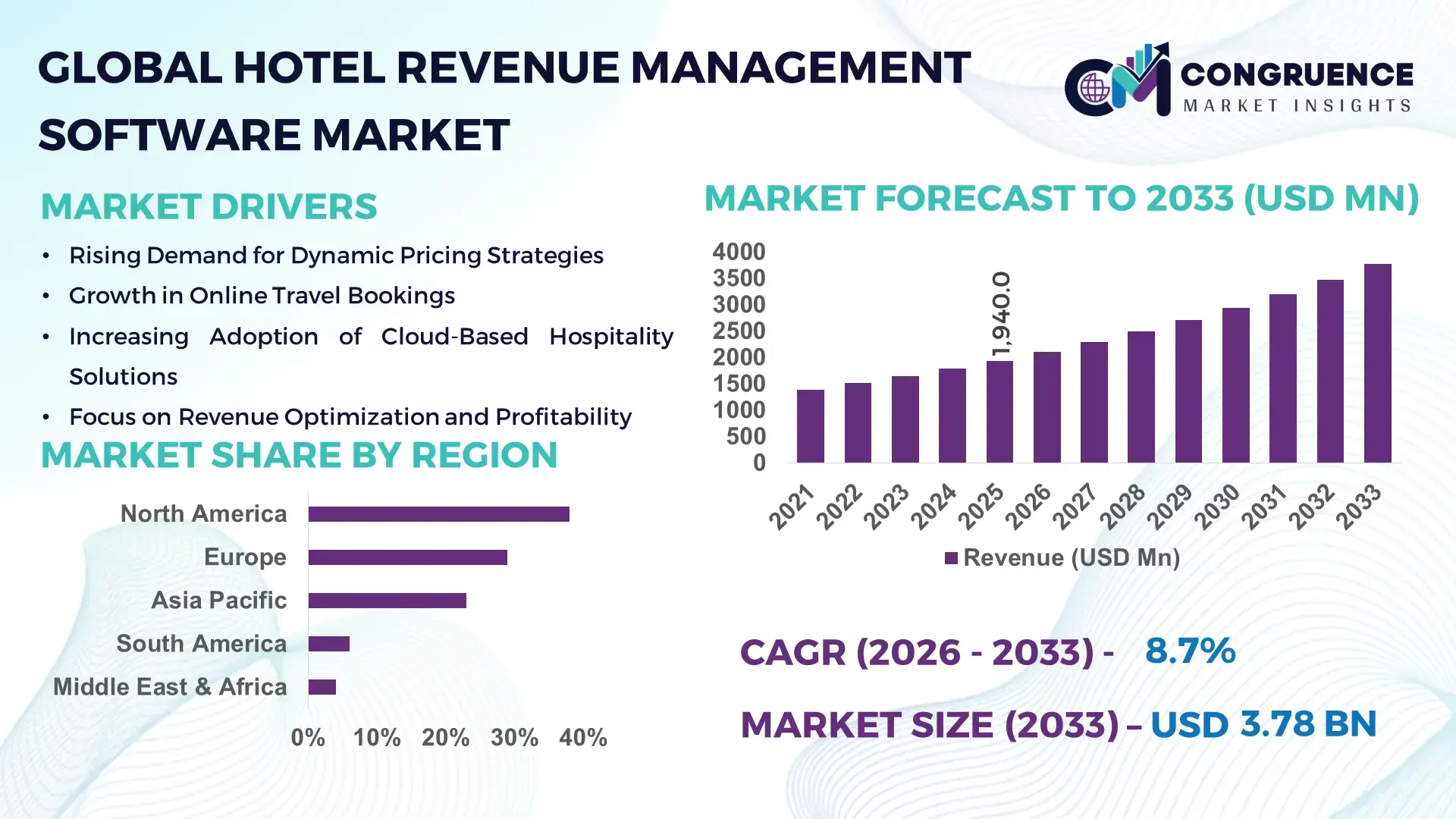

The Global Hotel Revenue Management Software Market was valued at USD 1,940.0 Million in 2025 and is anticipated to reach a value of USD 3,781.3 Million by 2033 expanding at a CAGR of 8.7% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing adoption of AI-powered pricing engines, real-time demand forecasting tools, and integrated property management platforms across global hospitality chains.

The United States represents the dominant country in the marketplace, supported by an advanced hospitality infrastructure of over 5.3 million hotel rooms and more than 61,000 properties. Approximately 72% of upscale and luxury hotel chains in the U.S. deploy automated revenue management systems integrated with cloud-based property management systems. Annual hospitality technology investments in the country exceed USD 1.2 billion, with major applications concentrated in dynamic pricing, channel optimization, and centralized portfolio management. AI-driven forecasting tools have demonstrated up to 15% improvement in RevPAR performance across multi-property operators. Cloud deployment accounts for nearly 68% of newly implemented systems, reflecting accelerated digital transformation and SaaS adoption across enterprise-level hotel groups.

Market Size & Growth: USD 1,940.0 Million in 2025, projected to reach USD 3,781.3 Million by 2033, expanding at 8.7% CAGR; growth supported by AI-enabled pricing automation and cloud adoption.

Top Growth Drivers: 72% AI-based pricing adoption in premium hotels; 18% RevPAR optimization improvement; 65% shift toward cloud-native deployments.

Short-Term Forecast: By 2028, predictive analytics integration is expected to improve occupancy forecasting accuracy by 22%.

Emerging Technologies: Machine learning-based demand forecasting, API-driven channel integration, and real-time competitor rate intelligence platforms.

Regional Leaders: North America projected at USD 1,420.0 Million by 2033 with high SaaS penetration; Europe at USD 980.0 Million driven by independent hotel digitization; Asia-Pacific at USD 860.0 Million supported by smart hotel expansion.

Consumer/End-User Trends: Luxury and upper-midscale hotels account for over 60% of deployments; independent boutique hotels show 25% annual rise in SaaS adoption.

Pilot or Case Example: In 2024, a multi-property U.S. hotel chain achieved 14% revenue uplift through AI-driven dynamic pricing optimization.

Competitive Landscape: Market leader holds approximately 21% share, followed by four major global hospitality tech providers with enterprise cloud portfolios.

Regulatory & ESG Impact: Data privacy compliance (GDPR, CCPA) influencing 40% of procurement decisions; energy-efficient pricing models aligned with ESG reporting goals.

Investment & Funding Patterns: Over USD 900 Million invested globally in hospitality SaaS platforms during 2023–2025, with strong venture participation.

Innovation & Future Outlook: Integration with CRM, business intelligence dashboards, and automated upselling engines is reshaping revenue strategy frameworks.

Hotel revenue management software is primarily deployed across luxury (38%), upscale (24%), and midscale (21%) hotel segments. Recent innovations include AI-driven demand sensing, automated rate parity monitoring, and mobile dashboard analytics. Data governance regulations and cybersecurity mandates influence procurement strategies. North America and Europe collectively account for over 60% of enterprise deployments, while Asia-Pacific demonstrates accelerated adoption among smart hotels. Future outlook centers on predictive analytics, API-led integration ecosystems, and sustainable revenue optimization frameworks.

The Hotel Revenue Management Software Market holds strategic relevance as hospitality operators prioritize data-driven pricing precision, operational efficiency, and portfolio-wide revenue visibility. Modern AI-powered revenue engines deliver up to 18% improvement in RevPAR compared to traditional spreadsheet-based pricing models. Cloud-native systems offer 30% faster deployment cycles compared to legacy on-premise installations, enhancing scalability for multi-property operators.

North America dominates in volume of deployments due to enterprise hotel concentration, while Europe leads in adoption intensity, with nearly 64% of independent hotel groups integrating automated pricing platforms. By 2028, generative AI-based demand forecasting is expected to improve booking conversion rates by 20% and reduce manual rate adjustment time by 35%. ESG alignment is becoming central to procurement decisions, with hospitality firms committing to 25% energy efficiency improvements by 2030 through optimized occupancy and dynamic load balancing strategies.

In 2024, a leading U.S.-based hospitality operator achieved a 14% occupancy uplift and 12% cost reduction by implementing machine learning-driven rate optimization across 120 properties. Comparative benchmarking indicates that automated revenue intelligence platforms deliver 22% greater forecasting accuracy compared to rule-based systems.

Looking ahead, integration with CRM, digital marketing automation, and IoT-based occupancy tracking will position the Hotel Revenue Management Software Market as a pillar of resilience, regulatory compliance, and sustainable growth within the global hospitality technology ecosystem.

The Hotel Revenue Management Software Market is shaped by rapid digitization across hospitality enterprises, increasing reliance on predictive analytics, and expansion of multi-property hotel chains. Demand is closely linked to occupancy rate volatility, online travel agency integration, and growth in direct booking platforms. Over 70% of global hotel bookings now occur through digital channels, increasing the need for automated rate optimization tools. Cloud-based deployment models account for more than two-thirds of new implementations, reflecting industry preference for scalable SaaS solutions. Interoperability with property management systems, customer relationship management platforms, and distribution channels is influencing vendor selection criteria. Additionally, cybersecurity compliance and data governance regulations are redefining system architecture standards. Competitive intensity is increasing as vendors embed artificial intelligence, real-time competitor benchmarking, and mobile-based revenue dashboards to enhance decision-making efficiency for revenue managers and hotel executives.

Digital channels account for over 70% of global hotel reservations, increasing pricing volatility and competitive benchmarking complexity. Hotels using automated pricing engines report up to 18% improvement in RevPAR and 20% reduction in manual rate adjustments. Integration with online travel agencies and direct booking engines enables real-time demand response, supporting data-driven revenue strategies. Growing multi-property portfolios further intensify demand for centralized dashboards capable of managing 50–200 properties simultaneously, strengthening software deployment across enterprise chains.

Nearly 40% of midscale and independent hotels still operate legacy property management systems lacking API compatibility. Integration costs can increase implementation timelines by 25–30%. Data migration challenges and cybersecurity upgrades add operational burdens. Smaller hotels often face skill gaps in data analytics, limiting effective utilization of advanced forecasting tools. Additionally, compliance with GDPR and CCPA requires structured data governance frameworks, increasing implementation complexity for regional operators.

AI-enabled personalization engines can increase booking conversion rates by 20% through targeted pricing and upselling. Integration with CRM platforms enables segmentation-based rate strategies for loyalty members and repeat guests. Emerging markets in Asia-Pacific show over 30% annual growth in smart hotel adoption, creating demand for automated pricing modules. Mobile-based dashboards and predictive analytics tools are expanding adoption among boutique hotels, opening untapped SaaS subscription opportunities.

Hospitality remains a high-risk sector for data breaches, with cyber incidents rising by over 15% annually. Revenue management systems process payment and booking data, requiring encrypted storage and multi-layer authentication. Compliance audits increase operational overhead for vendors. Smaller operators face budget constraints for cybersecurity infrastructure, potentially delaying software deployment. Balancing open API integration with secure data frameworks remains a technical and regulatory challenge.

AI-Driven Dynamic Pricing Adoption Surpasses 70% in Premium Hotels: Over 72% of luxury and upper-upscale hotels now deploy AI-based pricing engines capable of adjusting rates in under 5 minutes. Hotels leveraging machine learning forecasting report 18% higher RevPAR and 22% improved demand prediction accuracy compared to rule-based models. Automated competitor rate tracking systems process more than 10,000 daily data points per property, enhancing real-time pricing precision.

Cloud-Native Deployment Expands Beyond 65% of New Installations: Approximately 68% of newly deployed systems are SaaS-based, reducing IT infrastructure costs by 28%. Multi-property operators managing over 100 hotels report 30% faster deployment cycles through centralized cloud dashboards. Subscription-based pricing models have increased adoption among boutique hotels by 25% annually.

Integration with CRM and Direct Booking Engines Improves Conversion by 20%: Hotels integrating revenue management with CRM platforms achieve 20% higher direct booking conversions and 15% reduction in OTA commission dependency. API-driven connectivity supports over 50 distribution channels per property, enhancing revenue diversification strategies.

ESG-Aligned Revenue Optimization Enhances Energy Efficiency by 25%: Advanced occupancy forecasting tools support energy load balancing, enabling hotels to reduce energy consumption by up to 25%. Approximately 40% of enterprise hospitality groups now link pricing strategies with sustainability KPIs, integrating occupancy analytics with smart building management systems to support carbon reduction targets.

The Hotel Revenue Management Software Market is strategically segmented by type, application, and end-user, reflecting evolving operational priorities across hospitality enterprises. Deployment architecture remains a primary classification, with cloud-based systems accounting for over 65% of new installations due to scalability and centralized portfolio control. Application-wise, pricing and demand forecasting modules represent the most critical functional components, given that over 70% of bookings now occur through digital channels requiring dynamic rate adjustments. From an end-user perspective, luxury and upper-upscale hotel chains demonstrate the highest penetration levels, supported by multi-property management requirements and advanced analytics capabilities. Independent and boutique hotels are increasingly adopting subscription-based platforms, driven by ease of deployment and integration with online travel agencies. Decision-makers are prioritizing interoperability, cybersecurity compliance, and AI-driven automation as essential evaluation criteria, influencing procurement strategies across global hospitality portfolios.

The market by type is categorized into Cloud-Based Revenue Management Software, On-Premise Revenue Management Software, and Hybrid Deployment Models. Cloud-based systems lead the segment, accounting for approximately 68% of total deployments due to centralized dashboards, remote accessibility, and lower upfront IT infrastructure requirements. On-premise systems hold nearly 22% share, primarily among legacy hotel groups with established data centers and strict internal IT governance frameworks. Hybrid models contribute the remaining 10%, offering transitional flexibility for operators migrating from legacy infrastructure. Cloud-based deployment remains the fastest-growing type, expanding at an estimated CAGR of 11.2%, supported by SaaS subscription models, API-led integrations, and faster deployment cycles that reduce implementation timelines by nearly 30%. Hotels managing portfolios exceeding 50 properties prefer cloud-native systems for real-time rate synchronization across multiple distribution channels. On-premise systems retain niche relevance in regions with stringent data localization policies, while hybrid models appeal to enterprise chains balancing control and scalability. Combined, on-premise and hybrid segments represent 32% of installations, largely concentrated in Europe and select Asia-Pacific markets.

In 2025, the American Hotel & Lodging Association reported that more than 70% of newly renovated U.S. hotels integrated cloud-based revenue management platforms as part of their digital modernization initiatives, improving portfolio-wide rate alignment across thousands of rooms.

By application, the market includes Pricing & Rate Optimization, Demand Forecasting & Analytics, Channel Management Integration, Inventory Control & Distribution, and Reporting & Business Intelligence. Pricing and rate optimization leads with approximately 39% adoption share, as real-time competitor benchmarking and dynamic rate adjustments directly influence occupancy and profitability metrics. Demand forecasting systems account for around 27%, supporting predictive occupancy planning and event-based pricing strategies. While pricing optimization dominates current usage, demand forecasting tools are the fastest-growing application segment, expanding at an estimated CAGR of 10.6%, driven by machine learning algorithms capable of analyzing over 10,000 daily data variables per property. Channel management integration represents nearly 18% share, reflecting the need to coordinate rates across more than 50 online distribution platforms. Inventory control and BI tools collectively account for 16%, primarily serving multi-property chains. In 2025, more than 41% of global hospitality enterprises reported piloting AI-powered forecasting modules for direct booking platforms. Additionally, nearly 58% of upscale hotels indicated improved conversion rates after integrating automated pricing with CRM systems.

In 2024, the European Travel Commission highlighted that AI-based pricing systems were deployed across over 3,000 hotel properties in the EU to optimize seasonal demand fluctuations and event-driven occupancy management.

End-user segmentation comprises Luxury & Upper-Upscale Hotels, Midscale & Economy Hotels, Boutique & Independent Hotels, and Resort & Extended-Stay Properties. Luxury and upper-upscale hotels dominate with approximately 44% adoption share, supported by higher digital transformation budgets and centralized revenue strategy teams managing portfolios exceeding 100 properties. Midscale and economy hotels represent 28%, leveraging SaaS platforms to automate rate adjustments across high-volume occupancy cycles. Boutique and independent hotels are the fastest-growing end-user group, expanding at an estimated CAGR of 12.4%, fueled by subscription-based pricing models and simplified API integration with online travel agencies. Resort and extended-stay properties account for roughly 14%, utilizing demand forecasting tools to manage seasonal fluctuations and group bookings. In 2025, over 46% of independent hotels globally reported transitioning from manual spreadsheets to automated pricing dashboards. Furthermore, 63% of multi-property operators indicated that centralized revenue platforms improved cross-property rate consistency and reporting transparency.

In 2025, a Gartner hospitality technology survey noted that digital revenue management adoption among independent hotel chains increased by 24%, enabling more than 600 properties to automate rate optimization and improve occupancy planning accuracy.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.9% between 2026 and 2033.

Europe holds approximately 29% of global adoption, followed by Asia-Pacific at 23%, while South America and Middle East & Africa collectively contribute nearly 10%. Over 72% of enterprise hotel chains in North America utilize automated pricing platforms, compared to 64% in Europe and 48% in Asia-Pacific. More than 65% of new system deployments globally are cloud-based, with Asia-Pacific witnessing over 30% annual increase in SaaS-based hotel technology subscriptions. Europe reports that nearly 40% of independent hotels have integrated revenue optimization modules to reduce OTA dependency. In the Middle East, luxury hotel concentration exceeds 60% of total room inventory in key tourism hubs, driving high-value software deployment. South America shows digital booking penetration of nearly 55%, influencing rate automation adoption. Regional investment in hospitality digital infrastructure surpassed USD 2.5 billion collectively in 2025, underscoring sustained modernization initiatives worldwide.

North America holds approximately 38% of the global Hotel Revenue Management Software Market share, supported by a mature hospitality ecosystem comprising over 61,000 hotel properties and more than 5 million rooms. Key demand originates from luxury chains, business travel hotels, and large resort groups managing multi-property portfolios exceeding 100 locations. Regulatory frameworks such as CCPA and enhanced cybersecurity mandates influence procurement strategies, prompting 68% of enterprise hotels to prioritize encrypted cloud solutions. AI-based pricing engines are deployed in nearly 72% of upscale properties, improving demand forecasting accuracy by up to 20%. Digital transformation initiatives are accelerating integration with CRM and direct booking platforms, reducing OTA commission reliance by 15–18%. A leading regional player, Duetto, has expanded its AI-driven Open Pricing platform across hundreds of properties, enabling real-time rate adjustments within minutes. Consumer behavior reflects strong preference for direct digital booking, with over 70% of travelers reserving rooms via online channels, reinforcing automated rate optimization demand.

Europe accounts for approximately 29% of the global Hotel Revenue Management Software Market share, led by Germany, the United Kingdom, and France, which collectively represent over 55% of regional deployments. GDPR compliance significantly shapes data architecture design, with nearly 62% of hotel groups implementing structured data governance policies. Sustainability mandates under EU climate frameworks encourage occupancy-driven energy optimization, prompting integration of forecasting tools with smart building systems. Approximately 64% of independent and boutique hotels in Western Europe utilize automated rate optimization systems to manage high cross-border tourism flows. Cloud adoption exceeds 60% in urban hospitality clusters. A regional technology provider, IDeaS (with strong European operations), continues expanding analytics-driven pricing solutions across multinational hotel chains. European consumer behavior emphasizes transparency and fair pricing, resulting in higher demand for explainable AI pricing modules and audit-ready reporting dashboards.

Asia-Pacific represents roughly 23% of global market volume and ranks as the fastest-growing regional cluster. China, India, and Japan collectively account for over 65% of regional hotel inventory. The region has added more than 400,000 new hotel rooms in recent years, intensifying the need for automated pricing coordination. Cloud-based deployments exceed 55% of new installations, reflecting strong SaaS acceptance among midscale and smart hotel brands. Major tourism infrastructure initiatives and smart city developments are accelerating software integration. In India, digital booking penetration has crossed 60%, while China’s mobile-based reservations exceed 75%, driving AI-based pricing demand. A regional hospitality tech firm, RateGain, has expanded its AI-powered rate intelligence solutions across thousands of properties, enhancing competitor benchmarking accuracy. Consumer behavior is heavily mobile-centric, with app-based bookings contributing more than 65% of online reservations in leading markets.

South America contributes approximately 6% of the global Hotel Revenue Management Software Market share, with Brazil and Argentina leading regional adoption. Brazil accounts for nearly 45% of the region’s hotel inventory, supported by growing urban tourism and business travel. Digital booking penetration stands at approximately 55%, increasing reliance on automated rate optimization. Government-backed tourism promotion programs and trade partnerships have stimulated technology modernization across metropolitan hotel clusters. Cloud-based platforms represent over 50% of new deployments due to lower upfront costs. Regional hospitality operators increasingly adopt centralized dashboards to manage fluctuating demand during seasonal travel peaks. Consumer behavior reflects strong dependence on online travel agencies and localized pricing adjustments, particularly in Portuguese- and Spanish-speaking markets, encouraging multilingual analytics integration.

The Middle East & Africa accounts for nearly 4% of global market share, led by the United Arab Emirates and South Africa. The UAE alone hosts over 200,000 hotel rooms, with luxury properties representing more than 60% of premium inventory in Dubai and Abu Dhabi. Major tourism expansion programs and mega-events have increased demand for real-time rate optimization tools. Smart city initiatives and hospitality modernization strategies have pushed cloud adoption above 58% in key Gulf markets. Trade partnerships and regulatory frameworks encourage digital transformation aligned with data protection standards. Regional consumer behavior shows high preference for luxury and premium accommodations, resulting in strong uptake of AI-driven dynamic pricing platforms capable of processing thousands of booking variables daily.

United States – 34% Market Share: It is driven by large-scale multi-property hotel chains, high digital booking penetration exceeding 70%, and strong enterprise investment in AI-based pricing platforms.

Germany – 11% Market Share: It benefits from advanced hospitality infrastructure, strong regulatory compliance frameworks, and high adoption of automated pricing systems among independent and business hotels.

The Hotel Revenue Management Software Market exhibits a moderately fragmented competitive structure, with more than 45 active global and regional vendors offering pricing optimization, forecasting, and channel integration platforms. The top five companies collectively account for approximately 52% of global deployments, reflecting a competitive but innovation-driven environment. Leading players differentiate through AI-enabled forecasting accuracy exceeding 20% performance gains compared to rule-based systems, as well as integration capabilities spanning over 100 distribution channels per property.

Strategic initiatives between 2023 and 2025 have included over 18 partnership agreements between revenue management vendors and property management system (PMS) providers to strengthen API interoperability. Product innovation remains central, with nearly 70% of major vendors launching machine learning–enhanced modules featuring automated competitor rate scraping and predictive occupancy dashboards.

Mergers and acquisitions activity has intensified, particularly among SaaS providers seeking portfolio expansion across Europe and Asia-Pacific. More than 60% of enterprise-level hotel chains now require unified dashboards capable of managing portfolios exceeding 50 properties, intensifying vendor competition for large contracts. Competitive positioning is increasingly defined by cloud scalability, cybersecurity certifications, ESG-aligned analytics modules, and integration with CRM and digital marketing platforms. Vendors investing in generative AI, real-time rate adjustment engines, and mobile-first dashboards are gaining measurable enterprise traction across luxury and multi-brand hotel operators.

Atomize

Beonprice

Cloudbeds

Infor (Hospitality Revenue Management Solutions)

Sabre Hospitality Solutions

Oracle Hospitality

RoomPriceGenie

Pace Revenue

LodgIQ

eRevMax

HotelPartner Revenue Management

RevPar Guru

Technological innovation within the Hotel Revenue Management Software Market is centered on artificial intelligence, machine learning, and cloud-native architecture. Over 72% of upscale hotels currently deploy AI-based pricing engines capable of recalculating rates in under 5 minutes based on demand shifts, competitor pricing, and booking pace analytics. Machine learning forecasting models process more than 10,000 daily data variables per property, improving occupancy prediction accuracy by up to 22% compared to static pricing frameworks.

Cloud computing dominates deployment strategies, accounting for nearly 68% of new implementations, enabling multi-property operators to centralize dashboards and synchronize pricing across more than 50 distribution channels. API-first architectures now allow seamless integration with property management systems (PMS), CRM platforms, and channel managers, reducing integration time by approximately 30%.

Emerging technologies include generative AI for automated demand scenario simulation, enabling revenue managers to evaluate multiple pricing outcomes simultaneously. Advanced data visualization dashboards offer real-time KPI tracking across portfolios exceeding 100 hotels, supporting enterprise-level analytics. Additionally, predictive analytics integrated with smart building systems contribute to 25% energy optimization improvements by aligning occupancy forecasts with energy consumption planning.

Cybersecurity enhancements such as end-to-end encryption and multi-factor authentication are implemented in over 80% of enterprise deployments, reflecting stricter compliance mandates. Mobile-first dashboards and AI-driven upselling modules further enhance direct booking conversions by approximately 15–20%, reinforcing technology as a strategic differentiator in revenue optimization frameworks.

• In March 2025, RateGain Travel Technologies Limited announced a strategic partnership with Mews to integrate its AI-powered Channel Manager with Mews’ cloud-native PMS, enabling hoteliers to manage rates, inventory, and reservations across 400+ distribution channels, streamline operations, and foster efficiency. Source: www.rategain.com

• In July 2025, RateGain further expanded collaboration with Cloudbeds, integrating its UNO Channel Manager with Cloudbeds’ property management system to reduce manual processes, eliminate overbookings, and offer real-time distribution management across 400+ channels, enhancing hotel distribution through AI-driven automation. Source: www.rategain.com

• In March 2025, Duetto and Cloudbeds announced a strategic partnership to integrate Duetto’s revenue strategy platform with Cloudbeds’ hospitality management software, enabling enhanced efficiency, scalability, and advanced revenue optimization tools for hotels of all sizes. Source: www.duettocloud.com

• In June 2025, Duetto launched the Revenue & Profit Operating System (RP-OS) — a new platform designed to unify revenue and profit tools with advanced AI and automation, marking a significant evolution beyond traditional RMS into a comprehensive revenue + profit optimization ecosystem for hotel operations. Source: www.hospitalitynet.org

The Hotel Revenue Management Software Market Report provides comprehensive coverage of deployment types, application modules, end-user segments, and geographic landscapes across five major regions and more than 20 key countries. The report evaluates cloud-based, on-premise, and hybrid deployment architectures, with cloud installations accounting for over 65% of new implementations globally. Application analysis covers pricing optimization, demand forecasting, channel management integration, business intelligence dashboards, and inventory control systems, reflecting functional adoption patterns across luxury, midscale, boutique, and resort properties.

Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, incorporating region-specific adoption metrics such as digital booking penetration exceeding 70% in mature markets and mobile-based reservations surpassing 65% in high-growth economies. The report assesses more than 45 active vendors, including enterprise SaaS providers and specialized analytics firms, examining competitive positioning, partnership strategies, and integration ecosystems.

Technology evaluation includes AI-driven forecasting, generative analytics, API interoperability, cybersecurity compliance frameworks, and ESG-linked occupancy optimization tools. The report further analyzes procurement criteria such as system scalability for portfolios exceeding 100 properties, data governance requirements, and integration with over 50 distribution channels. Emerging segments including AI-powered personalization engines, mobile-first dashboards, and predictive energy optimization modules are also explored, offering decision-makers strategic insight into innovation pathways and digital transformation priorities shaping the Hotel Revenue Management Software Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,940.0 Million |

| Market Revenue (2033) | USD 3,781.3 Million |

| CAGR (2026–2033) | 8.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Duetto; IDeaS Revenue Solutions; RateGain Travel Technologies; Atomize; Beonprice; Cloudbeds; Infor; Sabre Hospitality Solutions; Oracle Hospitality; RoomPriceGenie; Pace Revenue; LodgIQ; eRevMax; HotelPartner Revenue Management; RevPar Guru |

| Customization & Pricing | Available on Request (10% Customization Free) |