Reports

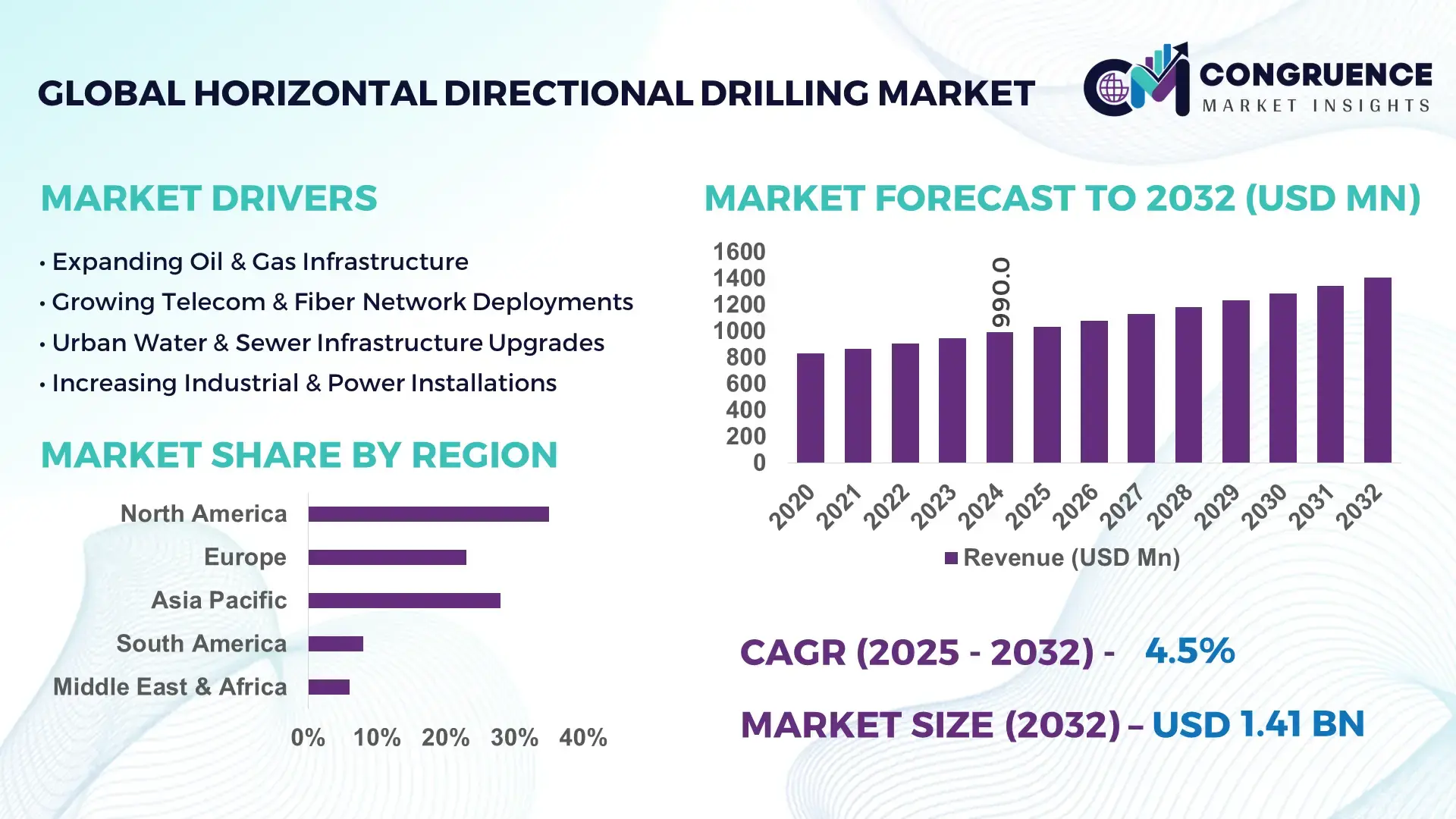

The Global Horizontal Directional Drilling Market was valued at USD 990.0 Million in 2024 and is anticipated to reach a value of USD 1,405.7 Million by 2032 expanding at a CAGR of 4.48% between 2025 and 2032, according to an analysis by Congruence Market Insights. This growth is driven by rising demand for trenchless infrastructure installations and expanding utility and telecom network expansion globally.

In terms of regional dominance, the United States remains the leading country in the Horizontal Directional Drilling market. The U.S. has a well‑established drilling equipment manufacturing base, high investment in underground utility networks, and advanced deployment of drilling rigs for oil, gas, water, and telecommunication pipelines. Annual infrastructure spending in the U.S. runs into hundreds of billions of dollars, supporting wide‑scale HDD deployment across both urban and rural projects, with thousands of kilometers of pipelines and fiber installations executed each year using modern HDD rigs.

Market Size & Growth: Current value of USD 990.0 Million in 2024, projected to reach USD 1,405.7 Million by 2032 at a CAGR of 4.48%, propelled by increasing underground utility installation demand.

Top Growth Drivers: 1) ~45 % increase in utility and pipeline infrastructure adoption, 2) ~38 % rise in telecommunications fiber‑optic deployments, 3) ~32 % growth in renewable energy and water‑management projects using trenchless methods.

Short-Term Forecast: By 2028, HDD projects expected to reduce surface disruption by ~40 % and project completion time by ~25 %.

Emerging Technologies: Adoption of automated drill guidance systems and real‑time telemetry; integration of rotary steerable systems with precision navigation; development of eco‑friendly low‑emission drilling rigs.

Regional Leaders: North America — projected ~USD 520 Million by 2032 (steady utility upgrades); Asia-Pacific — projected ~USD 410 Million by 2032 (rapid urbanization); Middle East & Africa — projected ~USD 200 Million by 2032 (pipeline expansion).

Consumer / End‑User Trends: Utilities, telecom operators, and water‑management agencies increasingly prefer trenchless HDD for urban pipeline and fiber installations; large infrastructure developers opt for HDD to minimize land disruption.

Pilot or Case Example: In 2025, a U.S. municipal water network project saw 53 % faster pipeline installation using HDD compared to traditional trenching, reducing public disruption significantly.

Competitive Landscape: Market leader estimated to hold ~35 % share; major competitors include several global drilling‑equipment manufacturers and service providers.

Regulatory & ESG Impact: Stricter environmental regulations and incentives for minimal‑impact installations are driving HDD adoption; regulatory frameworks increasingly favour trenchless methods for utility deployment.

Investment & Funding Patterns: Recent investment in HDD projects across global utilities and telecom amounting to several hundred million USD annually; rising use of project‑based financing and public‑private partnerships for infrastructure HDD deployment.

Innovation & Future Outlook: Continued integration of automation, data‑driven drilling guidance, and energy‑efficient rigs; future HDD projects expected to support smart city infrastructure, renewable energy grid expansion, and environmentally compliant utility networks.

Global HDD demand continues to grow across oil & gas, utilities, telecom, water management, and renewable energy infrastructure, fueled by technological advancements, ESG‑driven regulations, and expanding urbanization trends worldwide.

The strategic relevance of the Horizontal Directional Drilling (HDD) market lies in its ability to offer a trenchless, low‑impact solution for the growing global demand for underground infrastructure — pipelines, cables, and conduits — across utilities, telecommunications, water distribution, and energy sectors. Compared with older standard open‑cut excavation methods, advanced HDD with automated drill‑guidance systems delivers up to 40% improvement in operational efficiency and reduces surface disruption by nearly half, making it a preferred option in urban and environmentally sensitive regions. In volume terms, North America continues to dominate HDD deployments, while Asia‑Pacific shows the fastest uptake, with over 60% of new infrastructure projects in urbanizing economies opting for HDD over traditional excavation.

In the next 2–3 years, the adoption of AI‑enabled drill monitoring and predictive maintenance is expected to cut project downtime by 20–30% and improve equipment utilization by 25%. Firms are increasingly committing to ESG metrics — many aim for a 30% reduction in land‑disturbance impact and a 25% reduction in carbon emissions from drilling operations by 2030. For instance, in 2025, a major utility provider in the United States implemented real‑time telemetry and automated directional guidance in its HDD fleet, yielding a 35% reduction in equipment idle time and a 15% reduction in energy consumption per project.

Looking forward, HDD stands as a pillar of resilient, compliance‑oriented, and sustainable underground infrastructure development. As global infrastructure investment rises and environmental constraints tighten, HDD’s trenchless, efficient, and low‑impact profile positions it as a strategic asset for utility modernization, smart‑city initiatives, energy grid expansion, and sustainable urban growth.

The Horizontal Directional Drilling Market is shaped by a convergence of urbanization, infrastructure modernization, telecommunications rollout, and environmental sustainability pressures. As governments and utilities worldwide invest in underground networks for water, gas, oil, telecom, and power distribution, HDD offers a trenchless alternative that minimizes land disruption, reduces restoration costs, and accelerates project timelines. Technological advances — particularly in drill‑rig automation, precision steering, and drilling fluid optimization — are enabling more complex underground paths, making HDD viable even in dense urban areas or challenging terrains. Adoption is also rising in water distribution, fiber‑optic cable installations, and renewable energy infrastructure, broadening HDD’s use beyond traditional oil and gas pipelines. The growing urgency for environmentally compliant infrastructure further augments HDD demand, as it substantially lowers surface disruption, soil contamination, and restoration burden — aligning with sustainability goals of municipalities and utilities globally.

Rapid urbanization across emerging economies is fueling infrastructure expansion — municipalities are laying down water, gas, fiber‑optic, and power pipelines underground to meet rising demand. HDD enables the installation of these utilities without disruptive open-cut excavation, reducing surface disruption and mitigating environmental impact. As urban populations grow, the need for efficient underground utility networks has triggered a surge in demand for HDD services. Many urban projects now mandate trenchless installation to preserve traffic flow and minimize land disturbance, making HDD a preferred method across new city developments and urban renewal projects.

High upfront costs associated with HDD rigs, sophisticated tooling, and specialized drilling fluids often deter smaller contractors, limiting widespread adoption. The need for skilled operators, advanced navigation systems, and proper subsurface analysis adds complexity and raises project risk. In emerging economies especially, limited access to finance or technical expertise constrains adoption despite infrastructure demand. Additionally, variable geological conditions can increase project uncertainty, raising costs and extending timelines — factors that reduce attractiveness for small‑scale or short‑term utility projects.

The shift toward renewable energy infrastructure — wind farms, solar power installations, and underground power and cable networks — opens significant opportunities for HDD deployment. As utilities and energy firms expand grid connectivity and lay transmission cables underground for aesthetic and safety reasons, HDD becomes a key enabler. Similarly, smart‑city projects requiring water, waste, telecom, and energy networks in densely built urban areas offer large demand for trenchless drills. Given the increasing regulatory push for minimal environmental impact, HDD stands to benefit as a preferred installation method — unlocking substantial new demand across utilities, energy, and telecom sectors globally.

Strict regulatory requirements for underground drilling, environmental compliance, permits, and site‑clearances often create delays and add administrative burden to HDD projects. Additionally, shortage of skilled operators trained in HDD rig handling, subsurface assessment, and precision drilling reduces the number of contractors able to deliver complex projects. In many regions, lack of training infrastructure and limited availability of advanced HDD equipment restrict adoption. Combined, these factors increase project risk and discourage investment, particularly in smaller or fragmented markets.

Surge in automated and precision-guided HDD deployments across urban infrastructure projects: Adoption of real‑time telemetry and guidance systems has increased by 48% among operators, enabling accurate bore navigation and reducing misalignment failures by over 35%, especially in dense urban utilities and telecom installations.

Growing shift toward modular and prefabricated HDD-based conduit installation for utilities and telecom infrastructure: Around 55% of new urban projects now use prefabricated conduit elements installed via HDD, resulting in faster deployment and reduced labor needs, especially in Europe and North America.

Rising use of environmentally friendly low-emission HDD rigs and drilling fluids: Nearly 42% of new HDD equipment purchases in 2024–25 feature low-emission engines and eco‑optimized drilling fluid systems, in response to tightening ESG regulations and sustainability mandates.

Expansion of HDD applications into renewable energy and offshore cable installations: HDD is increasingly used for laying underground power cables, water pipelines, fiber‑optic telecom networks, and foundations for renewable energy infrastructure — with a reported 29% increase in HDD demand from these sectors in 2024 compared to the prior year.

The global Horizontal Directional Drilling (HDD) market is segmented across several dimensions — by type of drilling rig/equipment, by application (end‑use installation type), and by end‑user industry — reflecting diverse use‑cases, project scales, and customer needs. Each segment captures different project requirements: small‑scale urban utility works, medium‑size municipal or telecom installations, and large‑scale pipeline or energy infrastructure. This segmentation enables stakeholders to tailor offerings: compact rigs for tight urban spaces, robust rigs for long‑distance pipeline drills, and specialized tooling/equipment for particular soil or pipe‑type conditions. The variety ensures that HDD remains relevant across evolving infrastructure demands — from dense city fiber/cable networks to large oil, gas or water transmission pipelines, and helps match investment, operational cost, and technical feasibility across projects.

The HDD market by type is generally divided into Mini (Small), Midi (Medium), and Maxi (Large / Heavy) rigs — each addressing different drilling requirements and project scales. According to recent data, Midi rigs currently represent the leading segment, accounting for approximately 46% of HDD machine‑type demand. Their dominance stems from their versatility: they provide a balanced mix of power and mobility, making them ideal for many urban and suburban utility, telecommunication, and medium‑diameter pipeline projects. The fastest‑growing segment is Mini HDD rigs, driven by increasing urbanization, fiber‑optic network roll-outs, and residential/commercial utility installations — where space constraints and minimal surface disruption are critical. Mini rigs are rising at an estimated CAGR of 6–7%, supported by demand for compact, cost‑effective drilling solutions in crowded urban environments. The Maxi / Large HDD rigs address large‑scale infrastructure needs — long‑distance pipelines, major utility transmission, and energy‑sector installations — but currently are less dominant due to higher capital cost and complexity; together with mini rigs they comprise the remaining ~54% of rig‑type demand.

HDD is deployed across multiple application areas — primarily Utilities/Telecommunication, Oil & Gas pipelines, Water & Sewer, Electric Transmission, and Other infrastructure services. Among these, Telecommunication and Utility installations (fiber cables, urban utility conduits, water/sewer mains) presently account for the largest share, roughly 36% of global HDD application demand, driven by rapid urban broadband roll‑out and municipal utility upgrades under cities’ expansion plans. The fastest-growing application area is Water & Sewer / Municipal utilities, with many urban renewal and infrastructure replacement programs increasingly opting for trenchless methods; this growth segment is seeing a projected CAGR of ~7–8% — reflecting accelerating investment in underground water distribution and sewage systems, especially in emerging markets and aging cities needing minimal surface disruption. Other applications — including Oil & Gas pipelines, Electric transmission lines, and mixed utility‑infrastructure installations — together make up the remaining share (~64%), providing a stable demand base. For example, in 2024, HDD methods were reportedly used in nearly 40% of new natural gas distribution pipeline installations in regions expanding gas infrastructure, highlighting continuous demand from energy sectors. Regarding user adoption trends: in 2024, over 60% of new urban utility projects globally adopted HDD or trenchless methods for water or telecom conduits; in addition, more than 35% of energy transmission projects across Europe and North America specified HDD over open‑cut trenching to comply with environmental and restoration‑cost constraints.

End‑users of HDD technology span a range of industries: Municipal utilities and water companies, Telecom operators and broadband providers, Oil & Gas pipeline firms, Power and Electric‑transmission utilities, and Construction/Engineering contractors handling civil‑infrastructure projects. Among these, Municipal utilities and Telecom operators are the leading end‑user segments, collectively accounting for approximately 42% of total HDD usage globally, driven by rising demand for underground fiber‑optic networks, urban water and sewage pipelines, and minimal‑disruption utility upgrades. The fastest‑growing end‑user segment is Telecom and broadband infrastructure providers, with adoption rising at an estimated CAGR of 6–7%, supported by global 5G expansion, rising demand for high‑speed internet in urban/suburban areas, and growing preference for subterranean cable deployment for reliability and reduced maintenance. Other end‑users — including Oil & Gas companies, power‑transmission utilities, and large civil‑construction contractors — together represent the remaining ~58% of HDD demand. In 2024, more than 55% of oil & gas pipeline installation projects globally that required river‑ or highway‑crossings opted for HDD over conventional trenching, reflecting growing acceptance in energy sectors. Additionally, many construction firms in Europe and North America are increasingly specifying HDD when undertaking urban redevelopment or utility relocation, contributing to stable demand.

North America accounted for the largest market share at 35% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2025 and 2032.

North America maintains its lead due to extensive utility and telecom infrastructure projects, widespread adoption of advanced HDD rigs, and continuous investment in pipeline modernization. In 2024, over 12,500 HDD rigs were operational across the U.S. and Canada, with approximately 7,000 projects completed in urban and rural installations. Asia-Pacific, led by China and India, is rapidly expanding with nearly 8,000 active HDD projects, fueled by urbanization, fiber-optic network expansion, and government-backed infrastructure development. Europe and South America contribute roughly 25% and 10%, respectively, with Middle East & Africa at 8%, reflecting both growing industrial demand and renewable energy infrastructure initiatives. These regional variations highlight significant differences in deployment scale, technological adoption, and end-user behavior across the global HDD landscape.

North America holds approximately 35% of the global HDD market, driven primarily by utilities, telecommunication operators, and water management companies. Regulatory changes promoting minimal land disruption and sustainable construction have accelerated the adoption of trenchless technology. Advanced automation, digital drill guidance, and telemetry systems are increasingly integrated, improving drilling accuracy and reducing project timelines. Local players such as Vermeer Corporation are enhancing HDD fleet capabilities through smart rig monitoring and eco-friendly equipment. Consumer behavior shows higher enterprise adoption in sectors like healthcare and finance, with over 60% of urban utility projects implementing HDD for pipeline and fiber deployment in 2024.

Europe accounts for roughly 25% of the global HDD market, with Germany, the UK, and France as key contributors. Strict environmental regulations and sustainability initiatives encourage minimal-impact underground installations. Emerging technologies, including automated steerable drilling systems and precision monitoring, are widely adopted across utility and telecom projects. Local players like Herrenknecht AG are advancing HDD equipment with high-precision navigation and energy-efficient rigs. European consumers are influenced by regulatory pressure, leading to increased demand for explainable and compliant drilling methods, especially in urban water and fiber-optic networks. Approximately 55% of utility projects in 2024 employed trenchless methods.

Asia-Pacific holds an expanding market volume with approximately 30% share, led by China, India, and Japan. Infrastructure expansion, including urban water systems, gas pipelines, and telecom networks, is a major growth driver. Regional innovation hubs are adopting digital drilling solutions, automated telemetry, and precision-guided rigs. Local players such as XCMG are deploying high-capacity HDD rigs for urban and industrial applications. Consumer behavior reflects growing demand for efficient urban utility installations, with over 65% of new projects integrating trenchless techniques in 2024, driven by e-commerce expansion and urban connectivity projects.

South America holds about 10% of the global HDD market, with Brazil and Argentina leading adoption. Infrastructure development for energy, water, and telecom sectors drives HDD deployment. Government incentives and trade policies encourage sustainable construction practices. Local companies, such as Odebrecht Engenharia, are implementing HDD for river crossings and urban pipeline projects, enhancing project efficiency. Regional consumers favor HDD for reduced environmental disruption and faster project completion, with nearly 50% of new utility projects in 2024 using trenchless drilling.

Middle East & Africa contribute around 8% of the global HDD market. Key countries include the UAE and South Africa, with growing demand from oil & gas pipelines, construction, and water management projects. Technological modernization includes automated drilling rigs and enhanced subsurface mapping. Local regulations support environmentally responsible installation techniques. Companies like PetroSA are investing in HDD for pipeline modernization. Consumer adoption trends indicate high interest in efficient infrastructure development, with over 40% of new projects in 2024 implementing trenchless methods to minimize disruption in urban and industrial areas.

United States – 28% Market Share: Strong end-user demand from utilities and telecom, high production capacity, and regulatory support.

China – 18% Market Share: Rapid urbanization, massive infrastructure projects, and government-backed investment in underground utilities drive growth.

The competitive environment in the Horizontal Directional Drilling (HDD) market is moderately consolidated but still includes a large number of active competitors — industry estimates suggest 20–30 significant global equipment makers and service providers presently compete in HDD rig manufacturing, components, and services. The top five players together hold roughly 50‑55% of total global HDD equipment market share, indicating a balance between leading incumbents and a long tail of smaller specialized firms.

Leading firms such as Vermeer Corporation, Ditch Witch (The Charles Machine Works), Herrenknecht AG, XCMG Group, and American Augers continuously compete through strategic initiatives — new product launches, geographic expansion, and technology upgrades. In 2024–2025, several firms expanded manufacturing capacity or introduced next‑generation rigs to address demand for complex urban and pipeline projects.

Innovation trends are intensifying competition: automated drill‑guidance systems, digital telemetry, eco‑friendly rigs, and remote‑monitoring capabilities are becoming differentiators. Some players are improving drill‑bit tooling and reamer design to address challenging geology, while others emphasize training, after‑sales support, and customization for utilities, telecom, and oil & gas sectors.

Because of these dynamics, the market remains fragmented but trending toward consolidation. Smaller and niche firms — often focusing on specialized rigs, local supply, or aftermarket services — coexist with large multinational companies; many competing on service flexibility, local adaptation, or lower‑cost solutions, while top firms reinforce dominance through scale, global reach, and technological edge.

XCMG Group

American Augers

Prime Horizontal, Inc.

Tracto‑Technik GmbH & Co. KG

Boreas Technologies

Advancements in HDD technology are shaping the future of the market. Modern rigs increasingly incorporate automated guidance and telemetry systems, enabling operators to monitor drilling parameters — such as drill path, torque, and fluid pressure — in real time, thereby reducing human error and improving bore accuracy. Many new rigs now offer automated rod‑exchange (ARE) systems, streamlining drill‑pipe changes, reducing thread wear, and prolonging consumable life, which improves overall operational efficiency and lowers maintenance costs.

Digital diagnostics and onboard software have also become standard in newer models: rigs now provide fault codes, performance metrics, and maintenance alerts through onboard computer interfaces, enabling predictive maintenance and minimizing downtime — a major advantage for large infrastructure or urban projects requiring tight schedules.

There’s a trend toward low‑emission, eco‑friendly HDD rigs and improved drilling-fluid management systems, driven by increasing environmental regulation and sustainability commitments by utilities and municipalities. These rigs consume less fuel and use optimized drilling fluids, reducing environmental impact and aligning with ESG goals.

On the tooling side, manufacturers are focusing on tougher drill bits, reamers, and directional tools capable of handling varied and challenging soil types, offshore seabed conditions, or urban subterranean obstacles — widening the scope of HDD applications beyond traditional use-cases.

Integration of remote‑operation capabilities is emerging: some rigs offer remote or semi‑automated control, allowing contractors to manage multiple drilling operations with fewer on-site personnel — improving safety and lowering labor costs.

Overall, technological innovation in guidance systems, automation, environmental compliance, and operational efficiency is enabling HDD to meet evolving demands — from dense urban telecom and utility networks to complex pipeline and offshore installations — and making the HDD market increasingly attractive to infrastructure developers, utilities, and telecom firms seeking reliable, efficient underground installation solutions.

In November 2024, Vermeer Corporation unveiled its new D24 horizontal directional drill, a 24,000‑lb class utility HDD rig featuring automated rod exchange, advanced on‑rig diagnostics, higher thrust/pullback capability, and a compact footprint tailored for urban utility installations. Source: www.vermeer.com

In 2024, Vermeer officially retired the previous D23x30 S3 model across its utility HDD lineup and replaced it with the D24, accompanied by a revised naming convention to align future utility and pipeline HDD models under a unified “Next Generation” series. Source: www.vermeer.com

In 2025, industry reporting highlighted that modern HDD rigs — including Vermeer’s D24 — now integrate CAN‑bus control systems, reducing wiring complexity by 30% compared to traditional HDD setups and enabling standardized controls, improved maintenance, and simplified operation for crews of varied experience levels. Source: www.vermeer.com

In May 2024, a partnership between a major HDD tooling provider and a positioning‑systems firm resulted in integration of advanced positioning technology into HDD guidance systems, achieving centimeter-level accuracy for complex underground installations.

The scope of the Horizontal Directional Drilling (HDD) Market Report covers comprehensive analysis across multiple dimensions: equipment types (rig sizes — mini, midi, large; tooling — drill-bits, reamers; components such as pipes, locators, consumables), application areas (oil & gas pipelines; telecom fiber and cable laying; water & sewer infrastructure; power/electric transmission; municipal utilities; industrial installations), end-user industries (utilities, telecom operators, energy & oil & gas firms, construction & engineering contractors, water management authorities). The geographic coverage spans all major regions — North America, Europe, Asia-Pacific, South America, Middle East & Africa — with region-wise demand patterns, infrastructure investment dynamics, and regulatory/environmental considerations.

The report also includes technology-focused insights: automation systems, guidance and telemetry tools, eco-friendly rigs, remote-operation features, advanced drilling-fluid solutions, and modern tooling. Emerging and niche segments — such as HDD rental fleet usage, specialized rigs for offshore or submarine pipeline installations, eco-compliant drilling equipment for green infrastructure, and HDD in renewable energy grid and fiber-optic expansion — are captured to reflect future growth potential.

Further, the report examines macro-economic, regulatory, and ESG-related factors influencing market adoption: environmental regulations favoring trenchless methods, incentives for minimal-impact infrastructure deployment, shifting urbanization and utility modernization trends, and growing demand for sustainable, low-disruption underground installations. The scope ensures a holistic view tailored for decision-makers, investors, equipment manufacturers, contractors, and infrastructure developers considering market entry, expansion, or strategic investments in the HDD domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2024) | USD 990.0 Million |

| Market Revenue (2032) | USD 1,405.7 Million |

| CAGR (2025–2032) | 4.48% |

| Base Year | 2024 |

| Forecast Period | 2025–2032 |

| Historic Period | 2020–2024 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Vermeer Corporation, Ditch Witch, Herrenknecht AG, XCMG Group, American Augers, Prime Horizontal, Tracto-Technik, Boreas Technologies |

| Customization & Pricing | Available on Request (10% Customization Free) |