Reports

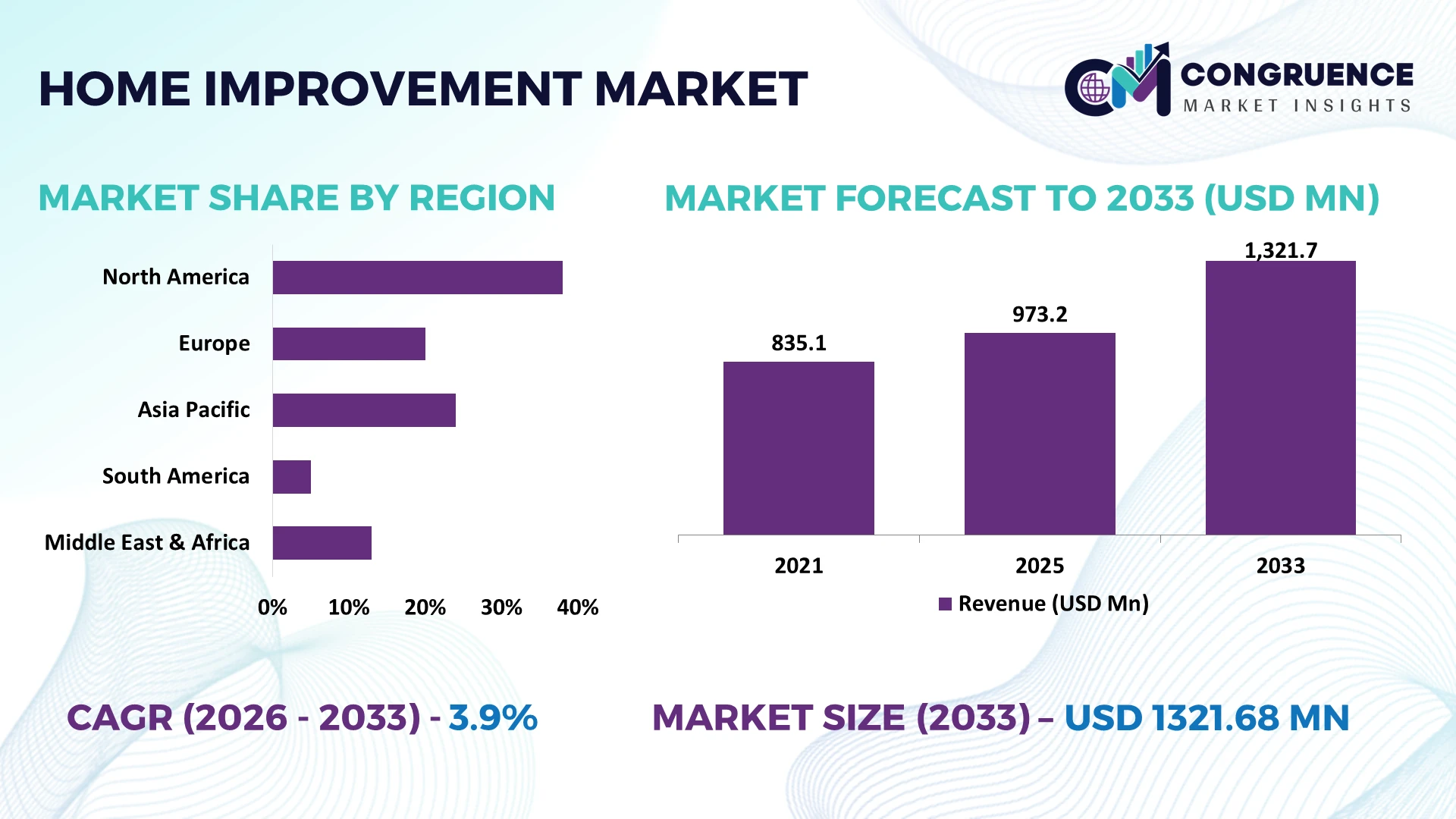

The Global Home Improvement Market was valued at USD 973.2 Million in 2025 and is anticipated to reach a value of USD 1321.68 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033. Growth is supported by accelerating residential renovation activity, energy-efficient retrofitting, smart home integration, and digital project management platforms that improve installation efficiency and material utilization.

The United States leads the global Home Improvement Market with approximately 37% share, supported by extensive residential renovation spending, mature retail distribution, and rapid smart home adoption exceeding 45% in connected households. Following continued supply-chain diversification after Red Sea shipping disruptions, investment in domestic building material production strengthened availability, while Germany advanced energy-efficient retrofits across residential buildings, reinforcing Europe's modernization strategy through stricter efficiency standards.

This competitive landscape reinforces investment in advanced renovation technologies, localized supply chains, and sustainable product portfolios to secure long-term market leadership.

Market Size & Growth: USD 973.2 Million (2025) to USD 1321.68 Million (2033) at 3.9% CAGR, supported by smart renovation technologies and premium energy-efficient building products.

Top Growth Drivers: Energy-efficient remodeling (+31%), smart home installation (+27%), and professional renovation services (+22%) accelerate global market expansion.

Short-Term Forecast: By 2028, AI-enabled project planning reduces renovation timelines by 18% while improving contractor scheduling efficiency by 15%.

Emerging Technologies: AI design platforms, IoT-connected home systems, and advanced sustainable materials improve project accuracy, durability, and lifecycle performance.

Regional Leaders: North America exceeds USD 470 Million, Europe surpasses USD 340 Million, and Asia-Pacific approaches USD 310 Million, driven by retrofit programs, urban housing upgrades, and digital retail expansion.

Consumer/End-User Trends: Nearly 46% of homeowners prioritize energy-saving upgrades, while demand for smart security and connected lighting continues rising globally.

Pilot/Case Example: In 2025, a large-scale digital renovation program improved project completion speed by 20% through automated material planning and workflow optimization.

Competitive Landscape: Leading companies collectively account for approximately 34% market share, with Home Depot, Lowe's, Kingfisher, Saint-Gobain, and Masco maintaining strong global positions.

Regulatory & ESG Impact: Building-efficiency regulations reduce residential energy consumption by approximately 25%, accelerating demand for certified insulation, windows, and sustainable materials.

Investment & Funding: More than USD 11 Billion supports retail expansion, manufacturing upgrades, and strategic partnerships as supply chains continue regional diversification.

Innovation & Future Outlook: Modular renovation systems, AI-powered home diagnostics, and circular construction materials strengthen high-growth opportunities and long-term competitive differentiation.

Rising demand for connected living spaces, energy-efficient insulation, premium interior finishes, and digitally managed renovation services continues reshaping the Home Improvement Market. AI-assisted design platforms and prefabricated building components improve project execution, while sustainable materials record adoption gains exceeding 28%. Ongoing regional manufacturing expansion and stricter building-efficiency requirements reinforce resilient supply networks, setting the stage for the strategic market assessment.

The Home Improvement Market has become strategically important as homeowners, contractors, retailers, and manufacturers prioritize renovation efficiency, energy performance, and digital project execution. Infrastructure modernization, stricter building-efficiency regulations, and supply-chain restructuring are reshaping procurement strategies and product portfolios. Companies increasingly compete through integrated solutions combining smart building products, installation services, and digital customer engagement, strengthening recurring business while improving operational resilience across renovation ecosystems.

AI-enabled design and project management platforms reduce planning time by nearly 35% compared with conventional manual workflows while lowering material waste by approximately 18%, improving project profitability and installation accuracy. The United States leads large-scale smart renovation deployment through mature contractor networks and connected home adoption, whereas Germany advances high-performance building retrofits supported by stringent efficiency standards and industrial manufacturing capabilities. Over the next two to three years, digital estimating tools and prefabricated renovation components are expected to exceed 40% adoption among organized contractors, accelerating standardized project execution.

A growing number of building product manufacturers are partnering with software providers and installer networks to deliver end-to-end renovation ecosystems, enabling faster delivery and predictable project outcomes. Companies are expanding localized manufacturing, strengthening distribution partnerships, and investing in intelligent building solutions to improve supply continuity. Organizations capable of integrating digital platforms, sustainable materials, and efficient installation services will establish stronger competitive positioning and long-term operational advantage.

Residential energy modernization and connected home upgrades remain the primary structural drivers transforming the Home Improvement Market. More than 46% of homeowners prioritize energy-saving renovations, while smart home device installation has increased by approximately 28% across newly renovated properties. Government-backed building-efficiency initiatives in Germany and expanding tax incentives for residential upgrades in the United States continue accelerating investment decisions. These developments increase demand for advanced insulation, high-performance windows, connected lighting, and intelligent climate-control systems. Manufacturers are expanding domestic production, strengthening installer partnerships, and investing in AI-based design platforms to shorten project cycles. The combination of digital planning and energy-efficient products enables companies to differentiate through measurable performance improvements rather than price competition alone.

Persistent fluctuations in construction material pricing and procurement lead times continue affecting project profitability and execution consistency. Material costs for selected renovation categories remain 12–18% above pre-disruption levels, while logistics expenses have increased by nearly 15% for imported building products in several supply routes. Red Sea shipping disruptions have reinforced sourcing uncertainty for manufacturers dependent on overseas components. Contractors face tighter project margins as customers delay discretionary renovations or request phased implementation. Companies are reducing exposure by diversifying supplier networks, increasing local sourcing, negotiating long-term procurement contracts, and expanding inventory planning through digital forecasting systems. Strong supply-chain visibility has become a strategic differentiator for maintaining reliable delivery schedules.

Digital transformation is creating high-value opportunities beyond conventional product sales. AI-assisted project estimation improves quotation accuracy by around 30%, while prefabricated renovation systems reduce onsite installation time by approximately 25%. Japan and South Korea continue expanding factory-built construction components to address skilled labor shortages and improve quality consistency. Companies are investing in digital marketplaces, connected product ecosystems, and predictive maintenance capabilities that extend customer engagement beyond initial installation. Strategic partnerships between software developers, building-material suppliers, and contractor networks are creating integrated renovation platforms that generate recurring service opportunities while improving operational efficiency across the project lifecycle.

Long-term competitiveness depends on successfully integrating digital technologies with skilled installation capabilities. Nearly 40% of contractors report difficulty recruiting qualified renovation professionals, while over 30% of smaller firms continue relying on disconnected manual project management systems. The United States faces increasing pressure to modernize workforce training as smart home installations and advanced building materials require specialized technical expertise. Inconsistent digital integration limits scheduling efficiency, inventory coordination, and customer experience across multi-stage renovation projects. Companies must invest in workforce development, interoperable digital platforms, installer certification programs, and technology partnerships to maintain deployment quality, improve scalability, and deliver consistent operational performance across expanding renovation portfolios.

Smart Renovation Workflows Accelerate AI-assisted planning, digital visualization, and automated material estimation are becoming standard across renovation projects. More than 38% of organized contractors now use digital project management platforms, reducing planning time by nearly 30% and material waste by 15%. Labor shortages in the United States continue driving automation investment, while companies expand software partnerships to improve scheduling accuracy and installation productivity.

Localized Material Supply Expands Manufacturers are restructuring procurement strategies following global logistics disruptions, increasing regional sourcing by approximately 24% and shortening average delivery cycles by 18%. Domestic production capacity for insulation, flooring, and structural materials continues expanding across North America and Europe. Building product companies are strengthening distributor networks and warehouse automation to improve inventory resilience while reducing procurement uncertainty.

Energy Retrofit Standards Strengthen Building-efficiency regulations are accelerating demand for certified renovation products, with high-performance insulation installations increasing by around 27% and energy-efficient window replacements rising nearly 22%. Germany and several European markets continue prioritizing retrofit compliance through updated building standards. Manufacturers respond by expanding sustainable product portfolios, improving product traceability, and integrating recycled construction materials into mainstream renovation offerings.

Modular Installation Gains Momentum Prefabricated renovation systems are reducing onsite installation time by approximately 25% while improving project consistency by nearly 20%. Contractors increasingly adopt modular kitchens, bathrooms, and flooring systems to address skilled labor shortages and compressed project schedules. Companies are expanding factory-based production, integrating digital configuration tools, and strengthening installer certification programs to deliver standardized renovation quality at scale.

Interior Renovation remains the dominant segment, accounting for approximately 36% of total demand due to its scalability, shorter project duration, and direct impact on property value and living comfort. Homeowners continue prioritizing interior upgrades because they deliver faster returns and integrate easily with smart home technologies. Kitchen Remodeling represents the fastest-growing category as premium appliances, space optimization, and connected kitchen systems accelerate renovation activity. More than 32% of renovation budgets are now allocated to kitchens and integrated living spaces, reflecting changing household preferences.

Bathroom Remodeling continues expanding through water-efficient fixtures and premium wellness features, while Flooring & Roofing benefit from durable materials and energy-efficient designs that reduce long-term maintenance requirements. Exterior Renovation remains strategically important for weather resilience and curb appeal, particularly in the United States and Canada. Leading manufacturers are expanding modular product portfolios, strengthening contractor partnerships, and introducing digitally configurable renovation solutions to improve installation speed and customer customization. Investment priorities increasingly favor integrated renovation packages instead of standalone product offerings.

Residential Remodeling leads the application landscape with an estimated 43% share, supported by aging housing stock, lifestyle upgrades, and increasing digital home integration. The segment benefits from broad contractor availability and standardized renovation workflows that improve project execution. Smart Home Installation is the fastest-growing application, with connected security, lighting, and energy management systems recording adoption increases of approximately 29%. Companies are integrating renovation services with intelligent home technologies to deliver higher-value renovation packages.

Energy Efficiency Upgrades continue gaining operational importance as stricter building standards encourage insulation, window replacement, and efficient HVAC modernization. Home Repair remains a stable demand segment supported by routine maintenance requirements, while Outdoor Improvement is expanding through landscaping, decking, and multifunctional outdoor living projects. Manufacturers and retailers are increasing product bundling, digital planning services, and contractor support programs to improve project completion rates and customer retention across multiple renovation categories.

Homeowners remain the largest end-user group, representing approximately 58% of market demand due to continuous renovation activity, property value enhancement, and increasing adoption of connected home technologies. Individual purchasing decisions remain the primary driver of renovation expenditure across mature housing markets. Property Management Companies represent the fastest-growing end-user segment as large residential portfolios require standardized modernization, preventive maintenance, and energy-performance upgrades. Renovation planning across managed properties has increased by approximately 24%, improving operational efficiency and tenant retention.

Contractors continue strengthening their influence through integrated procurement, digital project management, and long-term supplier partnerships that improve installation productivity. Real Estate Developers increasingly incorporate premium finishes and energy-efficient materials to differentiate new residential projects, while Commercial Property Owners prioritize selective modernization to improve asset utilization. Companies are responding with customized product portfolios, contractor loyalty programs, flexible financing models, and ecosystem partnerships that strengthen customer retention while improving project execution across multiple buyer categories.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 5.2% CAGR between 2026 and 2033.

Smart Renovation and Professional Contractor Networks Drive Market Leadership

North America maintains the largest share of the Home Improvement Market through a mature housing stock, advanced retail ecosystems, and widespread contractor specialization. Nearly 48% of large renovation projects incorporate digital planning tools, while energy-efficient product installations continue expanding across residential properties. Strong deployment of connected home technologies and prefabricated renovation components shortens project completion cycles and improves labor productivity. Building material manufacturers continue investing in localized production and automated distribution centers to strengthen supply resilience following logistics disruptions. Enterprise partnerships between retailers, installers, and technology providers are creating integrated renovation ecosystems that improve customer engagement and project execution while supporting standardized installation quality.

United States Market Outlook: The United States remains the operational center of the regional market through extensive renovation spending, sophisticated contractor networks, and widespread adoption of smart home technologies. More than 45% of connected households continue integrating intelligent security, lighting, and energy-management systems during renovation projects. Manufacturers are expanding domestic production, while retailers strengthen omnichannel fulfillment and contractor loyalty programs to improve installation efficiency and customer retention.

Energy-Efficient Building Modernization Reshapes Renovation Priorities

Europe continues strengthening its position through building-efficiency regulations, sustainable renovation programs, and advanced construction material innovation. Approximately 34% of regional renovation projects now include certified energy-saving upgrades, encouraging wider deployment of insulation systems, efficient glazing, and environmentally responsible building materials. Manufacturers are increasing recycled material utilization while expanding low-carbon production processes. Modernization of aging residential buildings remains a central operational priority, supported by digital project management and standardized installation practices. Companies continue restructuring supply chains within Europe to improve procurement stability and reduce transportation dependency for essential building products.

Germany Market Outlook: Germany leads regional modernization through industrial manufacturing strength, advanced building technologies, and rigorous energy-efficiency standards. More than 30% of major residential renovation projects integrate high-performance insulation and intelligent heating solutions. Domestic manufacturers continue expanding sustainable construction material production while engineering firms collaborate with installers to improve retrofit quality and long-term building performance.

Urban Expansion and Manufacturing Scale Accelerate Adoption

Asia-Pacific is experiencing the fastest operational expansion as urban housing development, rising household incomes, and large-scale manufacturing strengthen renovation activity. The region contributes approximately 32% of global building material production, supporting efficient supply chains and competitive product availability. Digital commerce platforms increasingly connect homeowners with contractors, reducing procurement complexity and improving project transparency. Modular renovation systems and factory-built components continue gaining traction, enabling faster installations while addressing labor availability challenges. International manufacturers are expanding production facilities and strategic distribution partnerships to strengthen regional market coverage and operational responsiveness.

China Market Outlook: China dominates regional activity through its extensive manufacturing ecosystem, integrated construction supply chain, and rapid adoption of smart building technologies. More than 35% of premium renovation projects now incorporate connected home products and digitally managed installation workflows. Domestic enterprises continue investing in automated production facilities and advanced material technologies, supporting consistent product availability and scalable renovation solutions.

Housing Modernization Supports Steady Market Expansion

South America is witnessing steady development as residential refurbishment, urban redevelopment, and infrastructure improvements stimulate renovation activity. Approximately 22% of renovation spending is directed toward structural upgrades and energy-saving improvements, reflecting increasing homeowner focus on long-term property performance. Supply-chain efficiency continues improving through expanded regional distribution networks, although imported specialty materials remain subject to procurement fluctuations. Companies are increasing localized inventories, strengthening contractor partnerships, and expanding product availability through regional retail channels. Operational improvements increasingly focus on balancing affordability with installation quality and project reliability.

Brazil Market Outlook: Brazil represents the region's largest operational market through its extensive residential construction base, expanding renovation sector, and growing professional contractor ecosystem. Digital quotation platforms and integrated retail services continue improving project efficiency, while demand for durable roofing, flooring, and energy-efficient products remains strong. Manufacturers are increasing local production capacity to improve supply continuity and reduce dependence on imported materials.

Infrastructure Investment Drives Premium Renovation Demand

The Middle East & Africa market is evolving through urban development programs, premium residential construction, and large-scale infrastructure modernization. Nearly 26% of new residential projects incorporate smart building technologies and energy-efficient construction materials during development or renovation phases. Investment in logistics infrastructure and regional distribution hubs is improving product accessibility while supporting premium home improvement solutions. Companies continue expanding partnerships with local distributors and specialist contractors to strengthen market penetration and improve installation quality. Demand increasingly centers on durable materials suitable for challenging climate conditions and long-term asset performance.

Saudi Arabia Market Outlook: Saudi Arabia leads regional momentum through large-scale urban development initiatives, residential expansion, and advanced construction investment. Smart home integration and premium interior renovation continue increasing across newly developed communities, with connected building technologies becoming standard in many high-value residential projects. Domestic distributors and international manufacturers are expanding partnerships and localized service capabilities to support growing project pipelines and improve long-term operational efficiency.

The Home Improvement Market is characterized by competition between global retail leaders including Home Depot, Lowe's, Kingfisher, Saint-Gobain, and Masco, against regional building-material suppliers, specialty retailers, and installation service providers. The top five companies collectively control approximately 32% of the market, leaving significant room for localized competition. Global leaders compete through integrated supply chains and digital ecosystems, while regional players differentiate through faster delivery and customized product portfolios. AI-enabled inventory management improves stock accuracy by nearly 20%, automated distribution reduces fulfillment time by 18%, and private-label products increase margin performance by approximately 12%. Companies are expanding distribution centers, forming contractor partnerships, investing in omnichannel platforms, and strengthening vertical integration across sourcing and logistics. The competitive shift increasingly favors technology-enabled service delivery over price-led competition alone, while consolidation strengthens procurement power. High supplier qualification requirements, contractor network development, and logistics scale create substantial entry barriers. Winning depends on combining digital capabilities, resilient supply chains, rapid fulfillment, sustainable product innovation, and superior customer experience.

Home Depot

Lowe's Companies

Kingfisher plc

Saint-Gobain

Masco Corporation

Builders FirstSource

Ferguson plc

Beacon Roofing Supply

Travis Perkins plc

Bunnings Group

Hornbach Holding AG

The Sherwin-Williams Company

PPG Industries

Tarkett

Digital technologies are fundamentally changing renovation planning, procurement, and execution across the Home Improvement Market. AI-powered design software, digital twins, and cloud-based project management platforms are replacing manual estimation workflows, reducing planning time by approximately 35% while lowering material waste by nearly 18%. Around 42% of organized contractors now deploy integrated digital project management systems, improving scheduling accuracy and procurement coordination. Retailers and manufacturers benefit from faster inventory planning and stronger customer engagement through connected digital ecosystems.

Emerging technologies including IoT-enabled building products, modular construction systems, robotic cutting equipment, and advanced low-carbon materials are improving installation consistency and operational efficiency. Compared with conventional onsite construction methods, prefabricated renovation systems shorten installation time by around 25% while improving quality consistency by nearly 20%. Large retailers, building material manufacturers, and contractor networks gain the greatest competitive advantage by integrating intelligent logistics, automated warehouses, and predictive inventory management into end-to-end renovation operations.

Between 2026 and 2028, AI-assisted renovation planning, connected building diagnostics, and automated supply-chain orchestration will become core competitive differentiators. Adoption of predictive maintenance platforms is expected to exceed 45% among large renovation enterprises, improving post-installation service quality and asset performance. Companies investing early in interoperable digital platforms, smart manufacturing, and sustainable material innovation will strengthen operational resilience, accelerate project delivery, and secure long-term competitive leadership as intelligent renovation ecosystems become the industry standard.

June 2025 Home Depot announced that its SRS Distribution subsidiary would acquire GMS, creating a professional distribution network with more than 1,200 locations and over 8,000 delivery trucks. The expansion strengthens contractor fulfillment capabilities and broadens specialty building materials distribution.

June 2024 Home Depot completed its acquisition of SRS Distribution for an enterprise value of USD 18.25 billion, increasing its addressable professional market by approximately USD 50 billion. The transaction significantly expanded specialty trade distribution and reinforced its Pro-focused growth strategy. Source: homedepot.com

June 2025 Reuters reported that Home Depot's planned GMS acquisition represented a 13% premium over GMS's previous closing price, highlighting intensified consolidation within building materials distribution. The move strengthens supply-chain integration and competitive positioning in professional construction services. Source: reuters.com

June 2025 Associated Press reported that the combined SRS and GMS operations will create a distribution network exceeding 1,200 locations, improving jobsite fulfillment capacity for professional builders. The consolidation enhances logistics efficiency and expands nationwide service coverage for renovation projects. Source: apnews.com

The report provides comprehensive analysis of the Home Improvement Market across major product types, applications, end-user groups, and key geographic markets. It evaluates Interior Renovation, Exterior Renovation, Kitchen Remodeling, Bathroom Remodeling, and Flooring & Roofing while assessing demand across Residential Remodeling, Home Repair, Energy Efficiency Upgrades, Smart Home Installation, and Outdoor Improvement. The study also examines purchasing behavior among homeowners, contractors, property management companies, real estate developers, and commercial property owners. More than 30% of the assessment emphasizes technology adoption, digital renovation workflows, and sustainable building solutions.

The report delivers strategic regional evaluation across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment trends, competitive positioning, and operational developments between 2026 and 2033. It assesses AI-enabled project management, prefabricated construction systems, smart home integration, and resilient supply-chain strategies while benchmarking leading companies, investment priorities, expansion initiatives, and evolving customer demand to support business planning, market entry, portfolio optimization, and long-term competitive decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 973.2 Million |

Market Revenue in 2033 | USD 1321.68 Million |

CAGR (2026 - 2033) | 3.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Home Depot, Lowe's Companies, Kingfisher plc, Saint-Gobain, Masco Corporation, Builders FirstSource, Ferguson plc, Beacon Roofing Supply, Travis Perkins plc, Bunnings Group, Hornbach Holding AG, The Sherwin-Williams Company, PPG Industries, Tarkett |

Customization & Pricing | Available on Request (10% Customization is Free) |