Reports

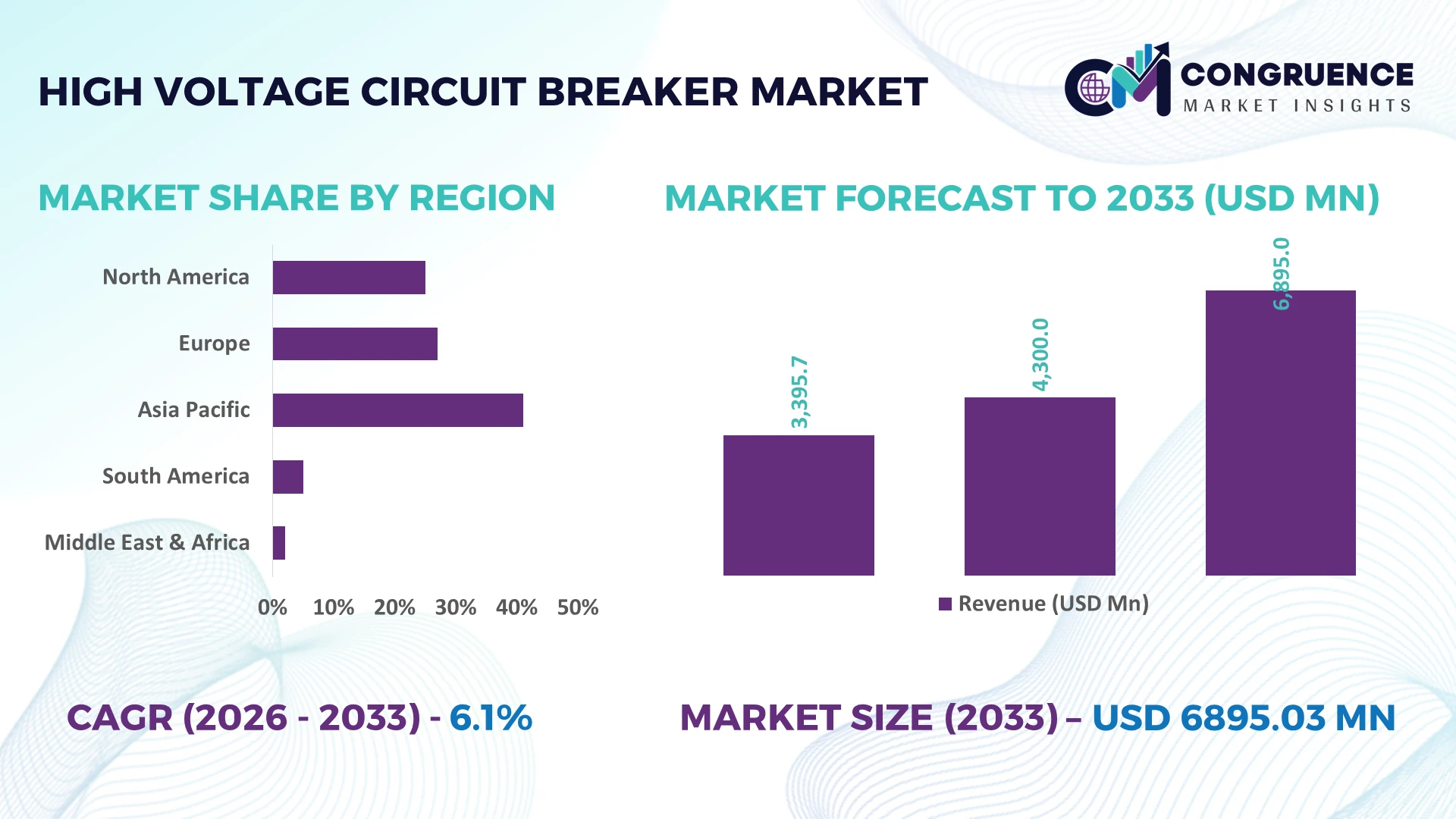

The Global High-Voltage Circuit Breaker Market was valued at USD 4300 Million in 2025 and is anticipated to reach a value of USD 6895.03 Million by 2033 expanding at a CAGR of 6.08% between 2026 and 2033. Grid modernization, ultra-high-voltage transmission expansion, renewable energy integration, and digital substation deployment are accelerating procurement of advanced high-voltage circuit breakers across utility and industrial power networks.

China remains the dominant market, accounting for approximately 34% of global high-voltage transmission infrastructure additions, supported by multi-billion-dollar grid investments and large-scale renewable integration. India is expanding transmission capacity by over 35% through nationwide corridor projects, while the United States continues digital substation upgrades driven by grid resilience priorities following ongoing energy security and supply-chain realignments since the Russia-Ukraine conflict.

For manufacturers and utilities, prioritizing intelligent switching technologies and localized production strengthens long-term competitiveness in rapidly expanding transmission networks.

Market Size & Growth: USD 4300 Million (2025) to USD 6895.03 Million (2033) at 6.08% CAGR, supported by advanced grid modernization and renewable transmission expansion.

Top Growth Drivers: Renewable grid integration (+32%), digital substation deployment (+27%), cross-border transmission investments (+24%) accelerate demand.

Short-Term Forecast: By 2028, smart monitoring reduces maintenance costs by nearly 20% while improving network reliability by 18%.

Emerging Technologies: AI diagnostics, IoT condition monitoring, and SF6-free switching technologies improve operational efficiency by over 25%.

Regional Leaders: Asia-Pacific exceeds USD 2900 Million, Europe surpasses USD 1550 Million, North America reaches USD 1450 Million, driven by transmission modernization and regional expansion.

Consumer/End-User Trends: More than 58% of new utility substations specify digitally monitored high-voltage circuit breakers for predictive asset management.

Pilot/Case Example: In 2026, a digital transmission project improved fault detection speed by 35% and reduced outage duration by 22%.

Competitive Landscape: Top manufacturers control approximately 46% market share alongside ABB, Siemens Energy, Hitachi Energy, GE Vernova, and Schneider Electric.

Regulatory & ESG Impact: SF6-emission reduction initiatives cut greenhouse gas intensity by approximately 30% across newly commissioned transmission assets.

Investment & Funding: More than USD 18 Billion supports grid expansion, strategic partnerships, manufacturing localization, and resilient supply-chain development.

Innovation & Future Outlook: Next-generation eco-efficient breakers, digital twins, and automation strengthen asset performance while enabling high-growth transmission infrastructure.

High-Voltage Circuit Breaker Market demand is increasingly concentrated in renewable energy transmission, smart substations, offshore wind integration, and high-capacity industrial grids. Eco-efficient insulation technologies and digital condition monitoring are becoming standard, with intelligent asset management improving maintenance efficiency by nearly 25%. Supply-chain localization and stricter environmental regulations are reshaping procurement priorities, setting the stage for broader strategic market developments.

The High-Voltage Circuit Breaker Market has become strategically important as utilities, industrial operators, and transmission developers prioritize resilient power infrastructure and grid stability. Infrastructure modernization, accelerated renewable integration, and stricter environmental regulations are reshaping procurement strategies, while supply-chain restructuring encourages localized manufacturing and diversified component sourcing. Companies are increasingly competing through digital capabilities, eco-efficient switching technologies, and lifecycle service offerings rather than hardware alone.

Modern digital high-voltage circuit breakers equipped with predictive diagnostics reduce unplanned maintenance by approximately 25% and lower inspection costs by nearly 18% compared with conventional equipment requiring periodic manual servicing. China continues expanding ultra-high-voltage transmission at a significantly larger scale, while Germany focuses on eco-efficient switching technologies and digital substations to comply with environmental standards. During the next two to three years, utilities are expected to increase deployment of intelligent asset-monitoring systems by over 30%, improving operational visibility and network reliability.

A recent utility transmission upgrade integrating intelligent monitoring with advanced circuit breakers reduced fault restoration time by around 20%, demonstrating measurable operational benefits. Manufacturers are strengthening strategic partnerships with grid operators, expanding localized production, and increasing investment in SF6-free technologies and digital engineering platforms. Organizations that combine advanced switching performance with sustainable product portfolios and predictive asset management will strengthen competitive positioning across evolving transmission infrastructure markets.

Large-scale transmission expansion is accelerating demand for advanced high-voltage circuit breakers as utilities reinforce grid reliability and renewable energy connectivity. More than 40% of newly commissioned transmission projects now incorporate digital substation architecture, while predictive asset management improves equipment availability by nearly 22%. India is rapidly expanding interstate transmission corridors to accommodate renewable generation, creating sustained procurement opportunities for intelligent switching equipment. In response, manufacturers are expanding domestic production, forming technology partnerships, and investing in eco-efficient breaker platforms with digital monitoring capabilities. This structural shift enables faster project execution, strengthens lifecycle service revenues, and positions suppliers to secure long-term utility contracts in increasingly performance-driven procurement environments.

The market continues to face structural constraints from volatile raw material prices, specialized component availability, and long qualification cycles for transmission equipment. Prices for selected electrical-grade metals have experienced fluctuations exceeding 15%, while delivery timelines for critical insulation and electronic components remain approximately 20% longer than pre-disruption levels. Japan and several European manufacturers continue managing sourcing challenges for advanced switching components, affecting production scheduling and inventory planning. Companies are reducing operational exposure through supplier diversification, localized manufacturing, and multi-year procurement agreements. These actions improve production stability but require disciplined capital allocation and stronger supplier collaboration to maintain delivery commitments and profitability.

Next-generation digital substations and environmentally sustainable switching technologies are creating high-value opportunities beyond conventional equipment replacement. Intelligent asset management platforms increase maintenance efficiency by nearly 25%, while eco-efficient insulation technologies reduce greenhouse gas emissions by more than 30% compared with traditional solutions. South Korea is advancing digital grid initiatives that encourage deployment of automated transmission infrastructure and intelligent protection systems. Manufacturers are expanding R&D, collaborating with software providers, and integrating AI-enabled diagnostics into high-voltage equipment portfolios. An emerging strategic advantage lies in offering integrated hardware, analytics, and lifecycle services that deliver measurable operational improvements while supporting evolving environmental compliance requirements.

Deploying advanced high-voltage circuit breakers requires seamless integration with legacy grid infrastructure, digital control systems, and cybersecurity frameworks, increasing execution complexity. Approximately 35% of utilities continue operating aging substations requiring customized integration, while demand for power system automation specialists has risen by over 20%. The United States faces growing pressure to modernize transmission assets without disrupting critical grid operations, extending implementation timelines. Companies are investing in workforce development, standardized communication protocols, digital engineering tools, and strategic partnerships with automation providers. Successfully addressing integration complexity will determine long-term deployment consistency, operational resilience, and competitive differentiation across increasingly digital transmission networks.

Digital Asset Intelligence Expansion Utilities are integrating AI-enabled monitoring and digital asset management into high-voltage substations, with intelligent diagnostics supporting over 40% of newly commissioned transmission projects and reducing unplanned maintenance by nearly 22%. China is accelerating digital grid deployment, prompting manufacturers to expand software partnerships, remote monitoring capabilities, and predictive maintenance services that improve operational continuity and lifecycle efficiency.

Rapid Shift Toward SF6-Free Designs Environmental compliance is accelerating adoption of eco-efficient circuit breakers, with deployment of SF6-free technologies increasing by approximately 28% in new high-voltage installations. Product development now emphasizes higher voltage ratings and equivalent interruption performance, while manufacturers scale production, strengthen utility collaborations, and accelerate commercialization of alternative insulation technologies.

Localized Manufacturing Networks Supply-chain resilience is reshaping procurement strategies as electrical equipment manufacturers increase regional production capacity by nearly 25% and reduce dependence on single-country sourcing. India is attracting greater manufacturing investment through transmission infrastructure programs, enabling shorter delivery cycles, stronger inventory control, and closer supplier collaboration for critical switching components.

Standards Driving Product Evolution Updated technical standards and testing requirements are accelerating redesign of high-voltage circuit breakers, improving qualification efficiency by approximately 18% while strengthening operational reliability. Engineering teams are investing in modular architectures, advanced testing procedures, and standardized components, enabling faster certification cycles, simplified maintenance planning, and improved compatibility across modern transmission infrastructure.

SF6 Circuit Breakers remain the leading segment because of their proven reliability in extra-high-voltage transmission networks, superior dielectric performance, and compatibility with large utility infrastructure. Nearly 55% of installed transmission systems continue utilizing SF6 technology due to established operational standards and dependable fault interruption capabilities. Hybrid Circuit Breakers are also gaining strategic relevance in smart grid applications by combining rapid switching with improved operational flexibility. Air Circuit Breakers and Oil Circuit Breakers continue serving legacy infrastructure, although new installations are gradually declining as utilities modernize transmission assets.

Vacuum Circuit Breakers represent the fastest-growing segment as environmental priorities and digital substation deployment reshape procurement decisions. Adoption has increased by approximately 30% in newly specified medium- and high-voltage projects because of lower maintenance requirements and reduced environmental impact. Manufacturers are expanding vacuum interruption technology portfolios, investing in advanced insulation systems, and collaborating with utilities to accelerate qualification for higher voltage classes. This transition is steadily redirecting investment toward sustainable switching technologies while preserving operational reliability across expanding transmission networks.

Power Transmission continues to dominate the market because expanding long-distance electricity networks require highly reliable switching and protection systems. Approximately 48% of new high-voltage installations are linked directly to transmission expansion and interconnection projects. Substations remain a closely aligned application as utilities deploy digital protection equipment and intelligent monitoring to improve operational continuity. Power Distribution continues upgrading aging infrastructure, although investments are generally concentrated below transmission voltage levels.

Renewable Energy is the fastest-growing application as large-scale solar, offshore wind, and hybrid power projects require advanced switching equipment capable of handling fluctuating power flows. Renewable-related transmission integration has increased by nearly 32%, encouraging manufacturers to develop intelligent circuit breakers optimized for variable generation environments. Industrial Plants continue upgrading electrical infrastructure for process reliability, while companies expand engineering partnerships, automation integration, and customized switching solutions. Investment priorities increasingly favor applications supporting flexible grid operation and renewable power integration.

Utilities remain the largest end-user group because national transmission operators and electricity distribution companies manage extensive high-voltage infrastructure requiring continuous equipment modernization. More than 60% of high-voltage circuit breaker deployments are associated with utility transmission expansion, grid reinforcement, and substation modernization. Oil & Gas and Railways maintain stable demand where uninterrupted power reliability is operationally essential, while Industrial users increasingly replace aging protection systems with digitally monitored switching equipment to improve asset availability.

Renewable Energy represents the fastest-growing end-user segment as utility-scale clean energy projects require new transmission interconnections and advanced grid protection. Deployment across renewable infrastructure has expanded by approximately 29%, supported by increasing electrification initiatives and digital grid integration. Manufacturers are introducing application-specific product configurations, strengthening engineering partnerships, and expanding after-sales service capabilities to address diverse operational requirements. Competitive positioning is increasingly determined by lifecycle performance, digital monitoring capabilities, and customized solutions tailored to individual end-user operating environments.

Asia-Pacific accounted for the largest market share at 44.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 7.12% CAGR between 2026 and 2033.

Grid Reliability and Digital Infrastructure Investment

North America maintains a strong position through extensive transmission modernization, replacement of aging grid assets, and widespread deployment of digital substations. The region contributes approximately 23% of global demand, supported by utility investment in high-voltage transmission, renewable interconnections, and grid resilience programs. More than 38% of newly commissioned transmission projects incorporate intelligent monitoring and automated protection systems, improving operational efficiency and outage response. Utilities are increasingly adopting eco-efficient circuit breakers while manufacturers expand localized engineering capabilities and lifecycle service offerings. Strategic partnerships between transmission operators and technology providers continue accelerating deployment of digitally integrated switching equipment for critical infrastructure and cross-state electricity networks.

United States Market Outlook: The United States leads the regional market through extensive transmission infrastructure, large-scale renewable integration, and continuous replacement of aging high-voltage assets. More than 70% of major transmission modernization projects incorporate advanced digital protection systems and intelligent switching technologies. Utilities are prioritizing grid resilience, cybersecurity integration, and predictive maintenance, while manufacturers expand domestic engineering, testing, and service capabilities to support faster deployment across utility-scale infrastructure.

Sustainability Regulations Accelerate Technology Transition

Europe continues strengthening its market position through transmission modernization, environmental regulations, and rapid deployment of low-emission electrical infrastructure. The region represents nearly 21% of global installations, with utilities increasingly replacing conventional equipment through eco-efficient switching technologies. More than 30% of newly approved transmission projects include SF6-free or reduced-emission solutions, reflecting stricter environmental compliance. Manufacturers are expanding research partnerships, enhancing digital asset management capabilities, and increasing production of environmentally sustainable circuit breakers. Grid operators also prioritize intelligent substations to improve operational flexibility and support renewable energy integration across interconnected transmission networks.

Germany Market Outlook: Germany remains the regional technology leader through advanced manufacturing capabilities, strong environmental regulations, and extensive transmission modernization initiatives. Utilities continue replacing legacy switching infrastructure with digitally monitored, eco-efficient systems, while engineering companies invest heavily in intelligent grid technologies. More than 35% of recent transmission equipment procurement emphasizes sustainable switching solutions designed to support renewable electricity integration and long-term operational efficiency.

Large-Scale Grid Expansion Drives Market Leadership

Asia-Pacific dominates the global market through unmatched transmission infrastructure expansion, manufacturing capacity, and electricity demand. The region accounts for approximately 44.8% of worldwide market activity, supported by extensive investment in ultra-high-voltage transmission corridors and renewable power integration. More than 45% of new high-voltage installations are concentrated across China and India, where utilities continue expanding national grid networks. Manufacturers are increasing production capacity, strengthening domestic supply chains, and investing in advanced digital circuit breaker technologies to support large-scale deployment. The combination of industrial expansion, electrification, and infrastructure modernization continues reinforcing the region's operational leadership.

China Market Outlook: China remains the largest national market because of its extensive ultra-high-voltage transmission network, domestic manufacturing ecosystem, and sustained investment in smart grid infrastructure. The country accounts for more than one-third of global transmission expansion activity, while equipment manufacturers continue scaling production, automation, and export capabilities. Integration of intelligent substations and eco-efficient switching technologies further strengthens China's competitive position in advanced high-voltage equipment manufacturing.

Transmission Expansion Supports Infrastructure Modernization

South America is strengthening its market position through transmission network expansion, renewable energy integration, and gradual modernization of aging electrical infrastructure. The region contributes approximately 6% of global demand, with investment increasingly focused on improving grid reliability across remote generation corridors. More than 26% of recent transmission upgrades are linked to renewable electricity projects requiring advanced switching equipment. Utilities continue modernizing substations despite financing and project execution constraints, while manufacturers expand local partnerships, engineering support, and maintenance services to improve long-term operational performance across developing transmission systems.

Brazil Market Outlook: Brazil leads the regional market through its extensive transmission network, hydropower infrastructure, and growing renewable energy investments. National grid operators continue expanding long-distance transmission corridors to connect new generation capacity, while utilities increase deployment of digitally monitored high-voltage circuit breakers. Infrastructure modernization and stronger operational reliability requirements continue driving procurement of advanced switching technologies across utility-scale projects.

Power Infrastructure Investment Accelerates Deployment

The Middle East & Africa is emerging as the fastest-growing regional market due to expanding transmission infrastructure, industrial diversification, and large-scale electricity network modernization. The region represents nearly 5% of global demand, while investment in high-voltage substations and cross-border transmission continues increasing. More than 30% of recently announced grid projects incorporate advanced protection systems and digital switching technologies. Utilities and industrial operators are prioritizing resilient electrical infrastructure, encouraging manufacturers to establish regional partnerships, strengthen service networks, and deliver solutions tailored to demanding operating environments.

Saudi Arabia Market Outlook: Saudi Arabia is the region's leading market through extensive investment in transmission infrastructure, industrial expansion, and national energy transformation programs. Utilities are accelerating deployment of advanced high-voltage substations supporting renewable energy integration and industrial megaprojects. More than 40% of ongoing transmission modernization initiatives incorporate intelligent protection systems, encouraging suppliers to expand local engineering support, technology partnerships, and long-term service capabilities.

The High-Voltage Circuit Breaker Market is led by ABB, Siemens Energy, Hitachi Energy, GE Vernova, and Schneider Electric, which primarily compete against regional manufacturers in China, India, and South Korea on technology leadership, delivery capability, and lifecycle performance rather than price alone. The top five companies collectively account for approximately 46% of the global market, creating a moderately consolidated competitive structure. Competition centers on intelligent monitoring, eco-efficient switching technologies, and localized manufacturing, with digital asset management improving maintenance efficiency by nearly 25% and modular production reducing delivery lead times by around 18%. Global leaders continue expanding engineering facilities, strengthening utility partnerships, and integrating software with hardware, while regional suppliers emphasize cost competitiveness and faster project execution. The competitive landscape is shifting toward SF6-free technologies, predictive diagnostics, and vertically integrated supply chains that reduce sourcing risk. High certification requirements, utility qualification cycles, and advanced testing capabilities remain major entry barriers. Sustained success depends on combining technological differentiation, localized production, reliable execution, and long-term service capabilities across transmission infrastructure projects.

ABB

Siemens Energy

Hitachi Energy

GE Vernova

Schneider Electric

Mitsubishi Electric

Toshiba Energy Systems & Solutions

Hyundai Electric

Fuji Electric

Eaton

CG Power and Industrial Solutions

Meidensha Corporation

LS Electric

Digital intelligence, eco-efficient insulation, and advanced interruption technologies are redefining high-voltage circuit breaker performance. Utilities are rapidly deploying AI-enabled condition monitoring, IoT sensors, and predictive diagnostics, with intelligent monitoring integrated into approximately 40% of newly commissioned transmission assets. These technologies reduce unexpected equipment failures by nearly 22% while improving maintenance scheduling efficiency by around 20%. Manufacturers are embedding cloud-connected asset management platforms into circuit breakers to enhance operational visibility and reduce lifecycle maintenance costs.

The transition from conventional SF6-based systems to eco-efficient and vacuum-assisted technologies is accelerating as environmental compliance becomes a procurement priority. Compared with conventional maintenance-intensive systems, digitally integrated circuit breakers improve asset availability by approximately 25% while lowering field inspection requirements by nearly 18%. Manufacturers investing in alternative insulation technologies, modular designs, and digital substations gain stronger positioning with utilities seeking sustainable infrastructure, whereas suppliers dependent on legacy platforms face increasing competitive pressure.

Between 2026 and 2028, digital substations, edge analytics, and digital twin integration will become core differentiators across transmission projects. More than 35% of utilities are expected to expand deployment of intelligent asset management platforms supporting remote diagnostics and automated maintenance planning. Companies investing early in software-enabled switching technologies, cybersecurity integration, and eco-efficient engineering will secure faster qualification, stronger lifecycle service opportunities, and greater competitiveness in large-scale transmission modernization programs.

January 2025 Siemens commissioned the world's first 24 kV blue GIS system using Clean Air insulation in Davos, replacing SF₆ technology and providing reliable electricity for up to 40,000 people. The deployment strengthens sustainable grid infrastructure and accelerates adoption of eco-efficient switching solutions. Source: Siemens

May 2026 Hitachi Energy introduced its EconiQ 800 kV SF₆-free dead tank circuit breaker rated at 63 kA for ultra-high-voltage transmission networks. The innovation enables utilities to eliminate SF₆ at the highest voltage class while improving long-term grid sustainability and transmission resilience. Source: Hitachi Energy

July 2025 Researchers introduced an explainable AI framework for high-voltage circuit breaker fault diagnostics that detects equipment anomalies without labelled fault data, improving diagnostic accuracy through vibration and acoustic analysis. The approach enhances predictive maintenance and reduces unplanned equipment outages.

June 2026 Researchers developed an optimization methodology for HVDC switching stations that determines the optimal number and configuration of DC circuit breakers, reducing fault risk while improving protection efficiency. The advancement supports more resilient multiterminal HVDC grid development and optimized infrastructure investment. Source: arXiv

This report provides a comprehensive assessment of the High-Voltage Circuit Breaker Market across major product types, applications, end-user industries, and key geographic regions. It evaluates SF6, vacuum, air, oil, and hybrid circuit breakers across power transmission, power distribution, renewable energy, industrial plants, and substations while examining demand from utilities, industrial facilities, renewable energy developers, oil & gas operators, and railway infrastructure. More than 45% of current deployment activity is concentrated in transmission modernization and digital substation projects.

The analysis examines manufacturing trends, intelligent monitoring technologies, eco-efficient switching solutions, supply-chain developments, and competitive positioning between 2026 and 2033. It highlights deployment patterns, technology adoption, regional investment priorities, and evolving procurement strategies while profiling leading industry participants. The report supports investment evaluation, market entry planning, product development, partnership strategies, capacity expansion, and long-term competitive decision-making through detailed operational and strategic market intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 4300 Million |

Market Revenue in 2033 | USD 6895.03 Million |

CAGR (2026 - 2033) | 6.08% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | ABB, Siemens Energy, Hitachi Energy, GE Vernova, Schneider Electric, Mitsubishi Electric, Toshiba Energy Systems & Solutions, Hyundai Electric, Fuji Electric, Eaton, CG Power and Industrial Solutions, Meidensha Corporation, LS Electric |

Customization & Pricing | Available on Request (10% Customization is Free) |