Reports

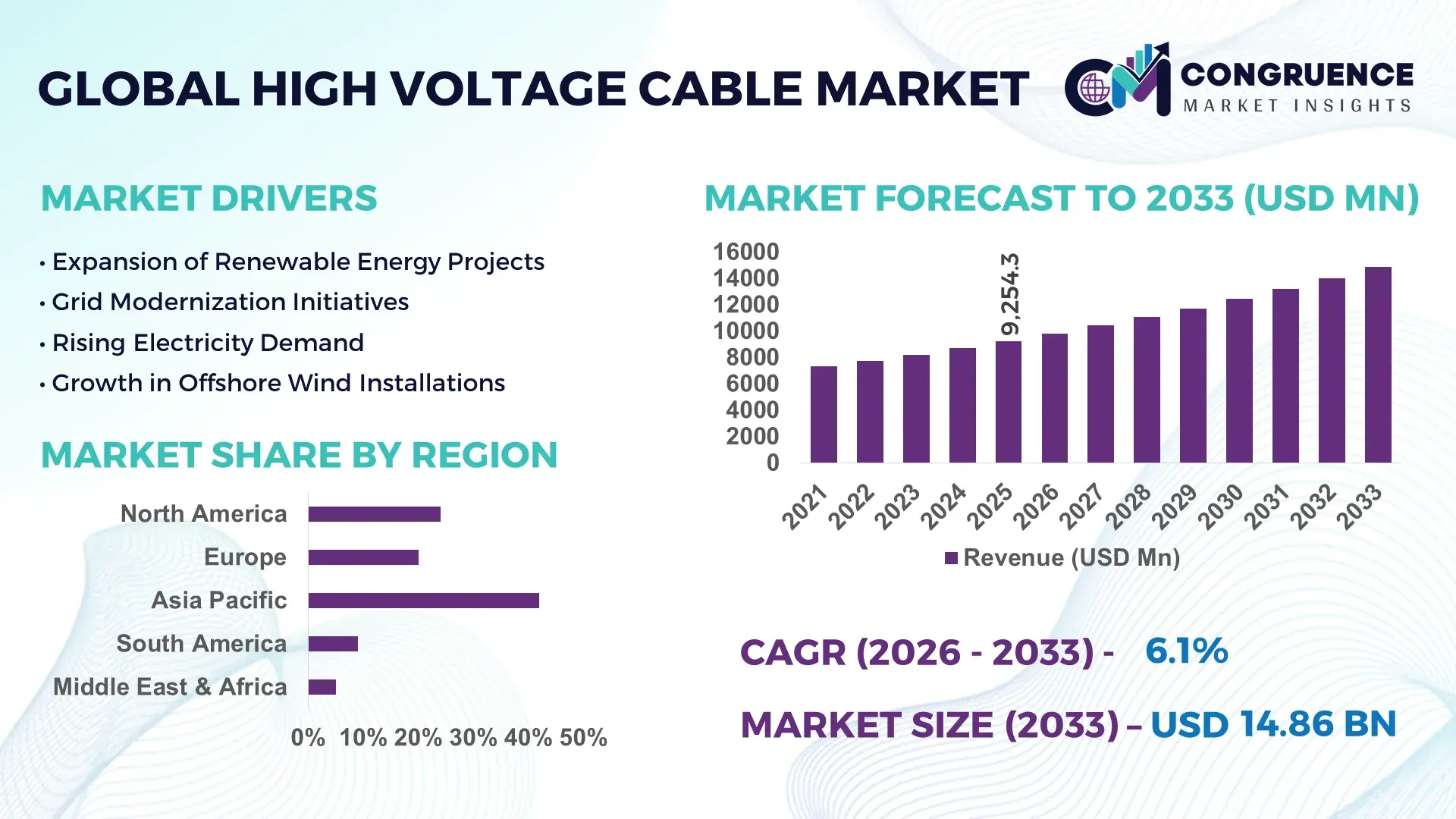

The Global High Voltage Cable Market was valued at USD 9254.32 Million in 2025 and is anticipated to reach a value of USD 14861.68 Million by 2033 expanding at a CAGR of 6.1% between 2026 and 2033. This growth is primarily driven by accelerating grid modernization and renewable energy transmission projects.

China leads global high voltage cable production, manufacturing approximately 35–40% of total output, backed by expanded manufacturing capacity across multiple provinces and extensive ultra‑high‑voltage transmission investments connecting remote renewable energy zones to major consumption centers. China’s production ecosystem supports over 460,000 kilometers of annual cable output, substantial capital expenditure in new facilities, and advanced UHV and HVDC cable technologies integrated into national energy strategies.

Market Size & Growth: Valued at USD 9254.32 Million in 2025, projected to reach USD 14861.68 Million by 2033 at a CAGR of 6.1% driven by renewable grid expansion and transmission upgrades.

Top Growth Drivers: Infrastructure modernization adoption 47%, renewable energy integration 39%, smart grid deployment 33%.

Short-Term Forecast: By 2028, average project lifecycle efficiency is expected to improve by 22%.

Emerging Technologies: Expansion of HVDC transmission, XLPE insulation innovations, digital condition monitoring systems.

Regional Leaders: Asia‑Pacific projected USD 6.0B by 2033 (rapid electrification), North America USD 4.2B (grid resilience focus), Europe USD 3.8B (offshore wind connectivity).

Consumer/End‑User Trends: Utilities increasing adoption for long‑distance transmission; industrial sectors upgrading to higher voltage capacity lines.

Pilot or Case Example: In 2025, a major HVDC corridor deployment reduced transmission losses by 15% in a grid expansion project.

Competitive Landscape: Market leader (approx. 25% share) followed by Nexans, LS Cable & System, Southwire, Sumitomo Electric.

Regulatory & ESG Impact: Stricter emissions targets and renewable mandates accelerating high‑voltage cable installations in major economies.

Investment & Funding Patterns: Over USD 12.4 billion invested in high voltage cable infrastructure, with Asia‑Pacific accounting for 41% of capital expenditure.

Innovation & Future Outlook: Lightweight conductors, smart diagnostics, and HVDC long‑haul systems shaping next‑gen grid connectivity.

China’s high voltage cable landscape features expansive utility and industrial deployment across HVAC and HVDC applications, supported by integrated smart grid technologies and continuous capacity expansion. The country’s technological developments include industry adoption of advanced XLPE and UHV cables capable of supporting long‑distance renewable power transfer, with regional consumption growth underpinned by both urban electrification and rural transmission upgrades. China’s ongoing infrastructure programs and investment in high‑precision manufacturing processes position it as a central driver of high voltage cable innovation and supply network resilience.

The strategic importance of the High Voltage Cable Market lies in its foundational role in modern power infrastructure, enabling efficient long‑distance electricity transmission and integration of distributed renewable energy sources. Adoption of advanced XLPE insulated 525 kV cables delivers approximately 15 % improvement in dielectric loss reduction compared to older oil‑insulated standards, directly improving transmission efficiency and operational reliability. Asia‑Pacific dominates in volume deployment of high voltage cable systems, while North America leads in adoption with roughly 48 % of utilities incorporating underground installations into grid modernization strategies by 2025. By 2028, integration of IoT and AI‑driven condition monitoring is expected to improve predictive maintenance outcomes, cutting unscheduled downtime by up to 20 % across utility networks. Strategic investments in HVDC infrastructure and smart grid compatibility support sector resilience amid rising electrification and renewable build outs. Firms are committing to measurable ESG metrics such as 30 % reduction in lifecycle carbon emissions through recycled materials and energy‑efficient manufacturing processes by 2030. In a micro‑scenario, a European utility achieved 12 % reduction in transmission losses in 2025 by deploying sensor‑enabled high voltage lines with automated fault detection. As global energy systems transition to low‑carbon, resilient grids, the High Voltage Cable Market will remain a critical pillar of compliance, sustainability, and future‑oriented growth.

Escalating deployment of renewable energy sources like offshore wind and large‑scale solar farms significantly increases demand for high voltage cables that can transmit power over long distances to shore and into urban grids. Modern smart grid systems require enhanced cable infrastructure capable of supporting real‑time data exchange and automated control, prompting utilities to upgrade legacy networks. Investments in smart grid technologies have resulted in a surge of cable projects incorporating IoT‑enabled sensors, reducing failure risks and streamlining maintenance. Grid modernization programs in North America and Europe prioritize underground and HVDC transmission for resilience and efficiency, further elevating demand. Urban electrification and industrial power consumption growth require reliable high voltage connectivity, reinforcing the critical role of advanced cable systems in contemporary energy ecosystems.

High voltage cable deployment involves substantial upfront costs due to specialized materials such as copper or aluminum conductors and advanced insulation systems required for high performance under extreme conditions. Underground and submarine installations further elevate expenses due to complex engineering, specialized equipment, and skilled labor demands. Regulatory compliance and environmental approvals can extend project timelines and add financial burdens, especially in regions with stringent land use and ecological standards. Additionally, volatility in raw material prices and supply chain disruptions create cost uncertainties, making budget planning more difficult for utilities and developers. These factors can delay project execution or prioritize alternative infrastructure solutions with lower immediate capital requirements.

Significant opportunities for the High Voltage Cable Market arise from expanding grid modernization initiatives and offshore renewable projects. Governments worldwide are increasing spending on smart grids that require next‑generation cable solutions with digital monitoring and advanced conductivity to support dynamic power flows and reduce losses. Electrification in emerging economies presents untapped demand for localized manufacturing and tailored deployment strategies. Integration of high voltage cables with energy storage systems and future‑oriented applications such as hydrogen‑ready corridors broadens potential use cases. Smart sensor integration and modular cable designs further create room for innovation and improved performance, attracting investment and partnerships.

The High Voltage Cable Market faces challenges from ongoing supply chain volatility, particularly in sourcing key raw materials such as copper, aluminum, and advanced polymers. Price fluctuations and distribution bottlenecks can delay production and increase project costs. Additionally, complicated regulatory frameworks regarding environmental impact and land acquisition often require extensive permitting and compliance efforts, impeding timely deployment. The shortage of skilled technicians for precise installation and maintenance further limits the speed at which new cable infrastructure can be commissioned, increasing project risk and operational costs. These hurdles necessitate strategic risk mitigation and investment in workforce development.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the High Voltage Cable market. Approximately 55% of recent projects reported cost reductions through prefabricated cable segments, with pre-bent and pre-cut elements produced off-site using automated machinery. Labor requirements decreased by nearly 30%, and project timelines shortened by an average of 18%. Europe and North America are leading in modular adoption, reflecting a focus on efficiency and precision in high-voltage installations.

• Expansion of HVDC Transmission Corridors: Ultra-high-voltage direct current (HVDC) systems are expanding rapidly to connect remote renewable energy zones. Over 42,000 kilometers of HVDC lines are now operational worldwide, with Asia-Pacific contributing roughly 60% of this infrastructure. HVDC cables reduce transmission losses by up to 15% over distances exceeding 800 kilometers, making them the preferred solution for long-distance power delivery. The technology also enables faster integration of offshore wind and solar projects.

• Integration of Smart Monitoring and IoT: Real-time condition monitoring is transforming cable network management. More than 38% of high-voltage cable operators now deploy IoT sensors to track temperature, load, and insulation health. This has led to a 22% reduction in unscheduled downtime and a 17% increase in maintenance efficiency. Predictive analytics are also facilitating timely interventions, extending cable lifecycle by approximately 12%.

• Lightweight and Advanced Insulation Materials: The use of advanced XLPE and composite insulation materials is growing, with 46% of new cable projects incorporating lightweight solutions. These materials improve handling by 25% during installation and reduce thermal losses by up to 10%. North America and Europe are rapidly implementing these technologies in urban and offshore applications, supporting higher voltage ratings and enhanced operational safety.

The High Voltage Cable Market is structured around product types, applications, and end-user segments, reflecting the diverse needs of modern power transmission networks. By type, cables are differentiated by voltage rating, insulation material, and design, influencing deployment across overhead, underground, and submarine systems. Applications range from power generation, transmission, and distribution to industrial and renewable energy projects, each requiring specific technical specifications and performance capabilities. End-users include utilities, industrial facilities, construction companies, and infrastructure developers, with adoption driven by regional electrification initiatives, grid modernization, and renewable integration. Regional consumption patterns reveal that Asia-Pacific leads in deployment volume, while Europe and North America emphasize advanced installations with integrated monitoring. Emerging trends such as HVDC expansion, modular construction, and smart sensor integration are reshaping market dynamics, supporting efficiency, reliability, and long-term operational sustainability across all segments.

High Voltage cables are categorized into XLPE insulated cables, oil‑filled cables, gas‑insulated cables, and submarine/underground specialized cables. XLPE insulated cables currently account for approximately 45% of adoption due to their high thermal stability, ease of installation, and minimal maintenance requirements. Oil‑filled cables represent around 20% of the market, mainly deployed for legacy networks requiring higher voltage ratings. Gas‑insulated cables hold 15% share, primarily in urban environments where space constraints exist. Submarine and underground cables constitute the remaining 20%, supporting offshore wind farms and intercontinental power transfer. XLPE insulation has also seen significant technological advancement, enhancing dielectric performance and environmental resilience.

The High Voltage Cable Market serves power transmission, distribution, renewable energy, and industrial sectors. Power transmission leads with a 48% adoption share due to growing long-distance energy transfer requirements and grid modernization projects. Renewable energy integration represents the fastest-growing application, supported by the expansion of offshore wind, solar farms, and HVDC corridors, capturing approximately 32% of projects by 2030. Distribution networks account for 15%, mainly upgrading urban infrastructure, while industrial applications cover the remaining 5%, primarily in heavy manufacturing and mining sectors.

Utilities remain the leading end-user segment, representing roughly 50% of high-voltage cable adoption, driven by large-scale transmission and distribution network upgrades. Industrial users, including heavy manufacturing and processing facilities, account for 20%, while construction and infrastructure developers contribute 15%. Renewable project developers represent the fastest-growing end-user segment, projected to expand to 18% adoption by 2030, fueled by global offshore and solar power initiatives. Other segments, including government and municipal projects, make up the remaining 12%, often emphasizing regulatory compliance and resilient infrastructure.

Asia-Pacific accounted for the largest market share at 42% in 2025; however, Africa & Middle East is expected to register the fastest growth, expanding at a CAGR of 6.5% between 2026 and 2033.

In 2025, Asia-Pacific deployed over 215,000 km of high voltage cables, with China contributing 120,000 km, India 55,000 km, and Japan 25,000 km. The region leads in HVDC and XLPE cable adoption, supporting urban electrification and renewable integration projects. Africa & Middle East, with 38,000 km installed in 2025, is investing heavily in new transmission networks and cross-border power projects. Technological trends such as smart monitoring, modular cable construction, and digital grid integration are reshaping regional infrastructure, while government incentives and policy reforms support accelerated adoption.

How are advanced utility networks reshaping high-voltage cable adoption?

North America accounted for 26% of the global High Voltage Cable Market in 2025, driven by large-scale utility upgrades and urban electrification projects. Key industries include utilities, heavy manufacturing, and data centers, where digital transformation and smart grid adoption are reshaping network management. Regulatory changes such as updated NERC standards and government grants for renewable integration are accelerating adoption. Technological advancements include IoT-enabled monitoring systems and predictive maintenance analytics. Local players like Southwire have implemented smart cable installations across multiple grid modernization projects, improving reliability by over 15%. Enterprise adoption is highest in healthcare and finance, where uninterrupted power delivery is critical.

What factors drive high-voltage cable adoption across major industrial hubs?

Europe accounted for 22% of the market share in 2025, with Germany, the UK, and France leading deployment. Regulatory pressures, including EU Green Deal initiatives and renewable energy mandates, have accelerated high-performance cable adoption. Emerging technologies such as UHVDC transmission, advanced insulation materials, and real-time monitoring are increasingly implemented. Local players, including Nexans, have executed large offshore wind grid integration projects, connecting over 2 GW of renewable power. Demand patterns reflect regulatory compliance, with utilities and industrial operators prioritizing explainable and safe high voltage solutions.

Why is Asia-Pacific leading the global high-voltage cable deployment?

Asia-Pacific held the largest market volume in 2025 with 42% of global deployment. Top consuming countries include China, India, and Japan, with infrastructure expansion and renewable integration driving growth. Manufacturing hubs in China and India are rapidly scaling production capacity, supporting over 460,000 km of cable output annually. Regional technology trends include XLPE insulation and smart monitoring deployment. Local players such as LS Cable & System have integrated digital condition monitoring across large transmission corridors, reducing downtime by 12%. Consumer behavior is influenced by national electrification projects, industrial growth, and high demand for efficient grid connectivity.

How are energy modernization projects influencing cable demand?

South America accounted for 7% of the market in 2025, with Brazil and Argentina as key contributors. Investments in new transmission infrastructure and renewable energy projects are driving demand. Government incentives and trade policies support local manufacturing and cross-border grid projects. Local players, including Prysmian Group operations, are installing HVDC and underground cables for hydro and solar power transmission. Regional consumer trends indicate strong utility adoption in urban centers and industrial zones, with demand closely linked to infrastructure expansion and regional energy initiatives.

What factors are fueling high-voltage cable adoption in emerging energy markets?

Middle East & Africa held 3% of the market in 2025, with UAE and South Africa leading demand. Growth is driven by oil & gas, construction, and urban electrification projects. Technological modernization includes smart grid integration, advanced insulation, and HVDC corridor development. Local regulations and trade partnerships encourage foreign investment and standardization in high-voltage deployments. Players such as Saudi Cable Company have launched large-scale UHVDC projects, reducing energy losses by 14%. Regional adoption varies, with industrial and municipal utilities leading deployments, reflecting infrastructure modernization priorities and long-term energy strategy alignment.

China – 28% market share; dominance due to massive production capacity and extensive renewable grid integration.

United States – 18% market share; driven by strong end-user demand, smart grid upgrades, and supportive regulatory incentives.

The High Voltage Cable market is moderately consolidated, with approximately 85 active global competitors operating across manufacturing, transmission, and renewable integration segments. The top five companies—Nexans, LS Cable & System, Southwire, Prysmian Group, and Sumitomo Electric—together account for roughly 62% of global market share, reflecting strong dominance in high-capacity production, technological innovation, and strategic partnerships. Competition is shaped by rapid adoption of XLPE and UHVDC technologies, integration of IoT-enabled monitoring, and digital grid solutions. In 2025, over 40 strategic product launches and cross-border collaborations were executed globally, focusing on modular, prefabricated cable systems and advanced insulation technologies. Mergers and joint ventures are also reshaping market dynamics, with at least 12 cross-region alliances reported in 2025 targeting renewable energy and urban electrification projects. Companies increasingly invest in R&D, producing lightweight, high-voltage conductors and condition-monitoring sensors that reduce transmission losses by up to 15% and installation timelines by 18%. The market remains highly competitive, with innovation, strategic partnerships, and regional deployment capabilities driving leadership positions.

Prysmian Group

Sumitomo Electric

General Cable

KEI Industries

Havells India

LS Electric

Hengtong Group

The High Voltage Cable market is experiencing significant technological transformation driven by the adoption of advanced insulation materials, digital monitoring systems, and high-capacity transmission designs. XLPE (cross-linked polyethylene) insulated cables dominate, accounting for approximately 45% of current deployments due to superior thermal stability, mechanical strength, and environmental resilience. Oil-filled and gas-insulated cables are also widely used in urban and high-voltage corridor applications, representing 35% of installations, particularly where space constraints or high reliability requirements exist. Submarine and underground specialized cables, comprising 20% of deployments, are increasingly critical for offshore wind projects and intercontinental power transfer.

Emerging technologies such as Ultra High Voltage Direct Current (UHVDC) systems are expanding global transmission capabilities, with more than 42,000 km currently operational, reducing long-distance transmission losses by up to 15% compared to traditional HVAC lines. Digital transformation trends, including IoT-enabled sensors and predictive maintenance analytics, have been deployed in over 38% of high-voltage networks, enabling real-time temperature, load, and insulation condition monitoring and reducing unscheduled downtime by 22%.

Modular and prefabricated cable construction is another innovation reshaping the market, with 55% of recent projects reporting installation cost reductions and labor savings of nearly 30%. Lightweight conductors and composite insulation materials improve handling efficiency by 25% and reduce thermal losses by 10%, supporting deployment in dense urban or offshore settings. Technological hubs in Asia-Pacific and Europe are leading research into AI-integrated monitoring, smart grid integration, and HVDC optimization, positioning high-voltage cable systems as critical enablers of resilient, sustainable energy infrastructure worldwide.

• In March 2024, Prysmian finalized a major contract to supply approximately 1,000 km of 525 kV HVDC subsea and underground high‑voltage cables for the Eastern Green Link 2 project linking Scotland and England, supporting enough clean electricity to power roughly 2 million homes.

• In March 2025, Prysmian delivered a new 245 kV HVAC dynamic high‑voltage cable system tailored for floating offshore wind projects, providing enhanced mechanical performance and reliability under harsh marine conditions. (Prysmian Corporate)

• In June 2025, Nexans introduced 525 kV DC SF₆‑free high‑voltage cable terminations worldwide, advancing environmentally responsible grid connectivity by reducing greenhouse gas emissions relative to traditional insulation approaches.

• In 2025, Sumitomo Electric began implementing its 525 kV XLPE HVDC underground cable system for Germany’s Corridor A‑Nord project, supporting the region’s energy transition strategy by boosting integration of renewable generation into the high‑voltage network.

The scope of the High Voltage Cable Market Report encompasses a multi‑dimensional analysis of product types, application areas, regional markets, and technological segments, offering decision‑makers a comprehensive view of current infrastructure dynamics and future pathways. The report covers cable types such as cross‑linked polyethylene (XLPE), oil‑filled, gas‑insulated, and specialized underground/submarine systems, detailing their technical features and deployment environments. It includes segmentation by voltage ratings and insulation designs, focusing on performance parameters like dielectric strength, thermal stability, and lifecycle durability. Application contexts encompass power transmission, distribution networks, renewable energy integration (including offshore wind and solar grid connectors), and industrial power systems. The geographic coverage spans key regions — North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa — with breakdowns of market volumes, infrastructure trends, regulatory landscapes, and adoption patterns specific to each region’s grid modernization and electrification initiatives.

Emerging and niche segments such as Ultra High Voltage Direct Current (UHVDC) corridors, smart grid integrated cable systems with real‑time monitoring, and prefabricated/modular cable assemblies are also within scope, highlighting innovation trajectories and adoption drivers. The report examines end‑use segments including utilities, industrial users, and infrastructure developers, profiling consumer behavior variations in adoption and technology preferences. Additionally, it includes insights on manufacturing capabilities and capacity expansions, digital transformation impacts, and infrastructure policies shaping future high‑voltage cable requirements. This breadth of analysis supports strategic planning, competitive benchmarking, and investment evaluation across the high‑voltage cable ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Nexans, LS Cable & System, Southwire, Prysmian Group, Sumitomo Electric, General Cable, KEI Industries, Havells India, LS Electric, Hengtong Group |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |