Reports

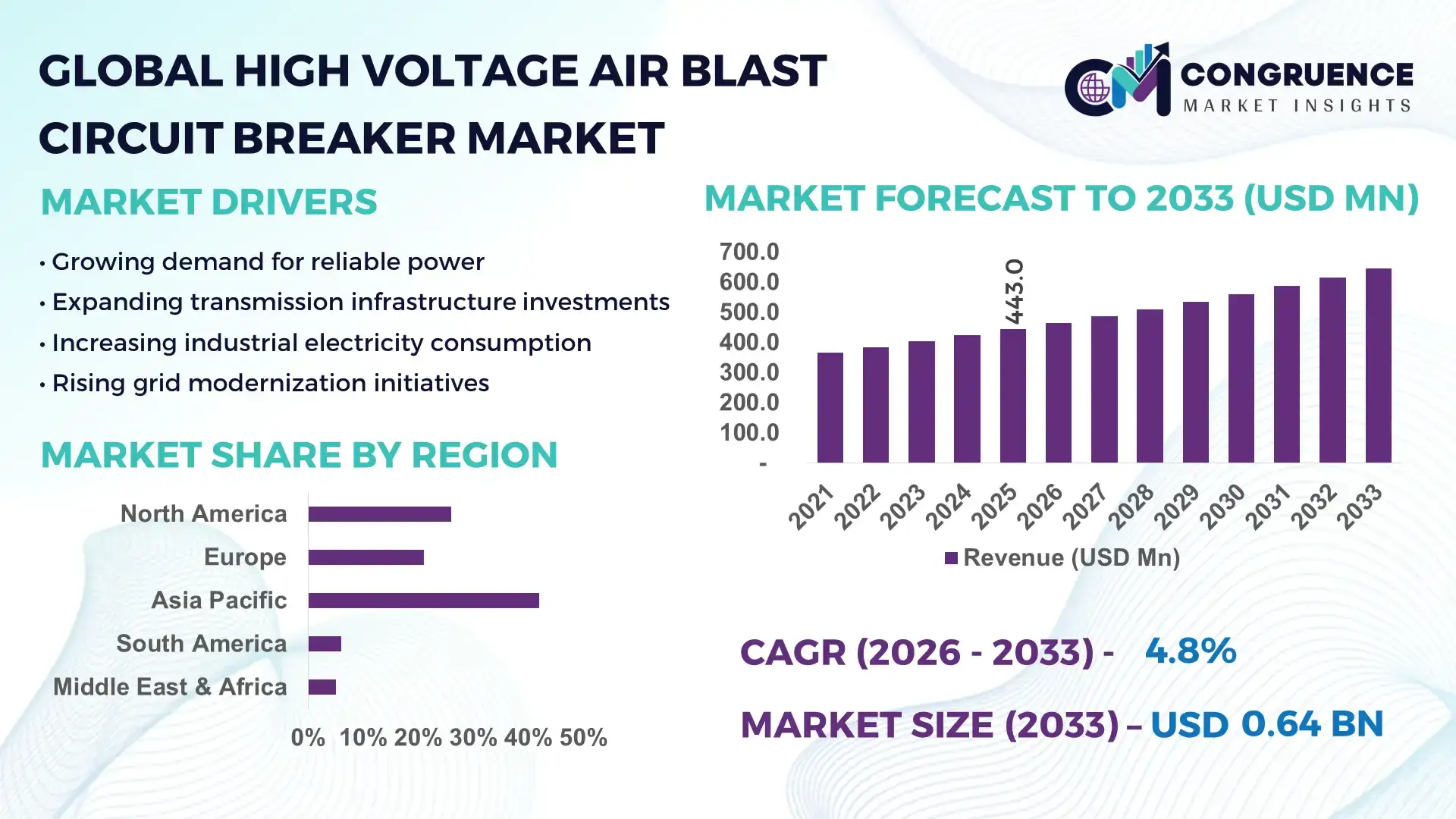

The Global High Voltage Air Blast Circuit Breaker Market was valued at USD 443 Million in 2025 and is anticipated to reach a value of USD 644.6 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033.

Rising grid modernization programs and the shift toward ultra-high-voltage (UHV) transmission are driving replacement demand, with utilities reporting up to 18% faster fault interruption efficiency using upgraded air blast systems. Between 2024 and 2026, supply chain restructuring and localized manufacturing—particularly influenced by geopolitical energy security concerns following the Russia–Ukraine conflict—have increased regional sourcing by nearly 22%.

China dominates the global landscape, accounting for approximately 34% of installed high-voltage breaker capacity, supported by over USD 80 billion annual grid investments and rapid expansion of renewable integration corridors. The country operates more than 1.2 million km of high-voltage transmission lines, enabling large-scale deployment of air blast circuit breakers in power-intensive industrial clusters. Compared to North America, where replacement demand drives ~60% of installations, China’s growth is led by new capacity expansion exceeding 12% annually, reinforcing its scale advantage. This concentration of infrastructure and capital investment positions Asia-Pacific as the core demand hub.

Strategically, companies must align manufacturing and service capabilities with high-growth transmission corridors to secure long-term contracts and competitive positioning.

Market Size & Growth: USD 443M (2025) to USD 644.6M (2033) at 4.8%, driven by grid expansion and UHV transmission upgrades.

Top Growth Drivers: Grid modernization +18%, renewable integration +22%, industrial electrification +15%.

Short-Term Forecast: By 2028, fault-clearing time reduces by ~20%, improving grid stability KPIs.

Emerging Technologies: AI-based fault detection, digital substations, advanced arc-quenching materials boosting efficiency by 12–16%.

Regional Leaders: Asia-Pacific (~USD dominant), North America (~USD mature replacement demand), Europe (~USD driven by decarbonization compliance).

Consumer/End-User Trends: Utilities account for ~58% adoption, prioritizing reliability and lifecycle cost optimization.

Pilot/Case Example: 2025 smart substation project improved outage response time by 25%.

Competitive Landscape: Top players hold ~52% share; leaders include ABB, Siemens Energy, GE, Mitsubishi Electric.

Regulatory & ESG Impact: Emission-free switching technologies reduce SF6 dependency by ~30%, accelerating compliance.

Investment & Funding: Over USD 6.5B grid investments globally, focusing on modernization and resilience.

Innovation & Future Outlook: Shift toward hybrid breakers and digital monitoring redefining operational efficiency by 15%+.

Power utilities dominate with nearly 58% share, followed by industrial manufacturing at 24% and infrastructure at 18%, reflecting strong dependency on stable high-voltage networks. Advanced arc-quenching designs and digital monitoring systems are improving operational efficiency by 12–15%, while Asia-Pacific leads demand with over 40% share due to rapid electrification. A key emerging trend is integration with smart grids, accelerated by supply chain localization and regulatory pressure, positioning the market for technology-driven transformation and strategic infrastructure alignment.

The High Voltage Air Blast Circuit Breaker market is rapidly becoming a critical battleground for infrastructure investment and competitive differentiation as global power systems undergo deep electrification and grid transformation. Utilities and industrial operators are aggressively upgrading switching infrastructure to handle rising load volatility, making circuit breaker performance a direct determinant of grid reliability and operational continuity. A major structural shift is underway as supply chains transition toward regional manufacturing hubs, reducing dependency risks and cutting procurement lead times by nearly 20%.

Technologically, digital air blast circuit breakers improve fault detection efficiency by 25% while reducing maintenance costs by 18% compared to legacy electromechanical systems, fundamentally reshaping operational economics. Regionally, Asia-Pacific leads in volume with over 40% deployment share, while Europe leads in innovation adoption with nearly 28% penetration of smart switching technologies, highlighting a divergence between scale and sophistication. Over the next 2–3 years, utilities are targeting ~30% reduction in outage duration, driven by automation and predictive maintenance integration.

Sustainability is emerging as a competitive advantage, with eco-efficient breaker designs reducing greenhouse gas impact by ~35%, enabling faster regulatory approvals and access to green financing. A micro example includes a 2025 grid upgrade project where digital breakers improved response time by 27%, significantly reducing downtime costs. Companies are accelerating capital allocation toward R&D and forming strategic alliances to integrate AI-driven monitoring systems, signaling a shift from hardware-centric to solution-driven models. The strategic imperative is clear: players that optimize performance, localization, and digital integration will secure long-term dominance in an increasingly performance-driven power infrastructure ecosystem.

The High Voltage Air Blast Circuit Breaker market is being reshaped by accelerating grid expansion, rising electrification, and increasing demand for high-performance switching systems in power-intensive industries. Utilities are prioritizing reliability and rapid fault interruption, with operational benchmarks improving by over 15% in modern substations. The shift toward renewable integration is intensifying the need for advanced circuit protection, as fluctuating loads require faster response mechanisms. Simultaneously, regional manufacturing localization—growing by nearly 20%—is redefining supply chain structures and cost dynamics. Competitive pressure is driving companies to innovate in arc-quenching technologies and digital monitoring, while regulatory frameworks emphasizing efficiency and environmental compliance are forcing product redesign. These combined forces are accelerating technological upgrades, reshaping procurement strategies, and redefining long-term investment priorities across the global power infrastructure ecosystem.

The primary growth engine is the global push toward grid modernization, where utilities are upgrading aging infrastructure to support higher load variability and renewable integration. Over 45% of transmission networks in developed economies are undergoing refurbishment, driving replacement demand for advanced circuit breakers. The integration of renewable energy sources—growing at over 20% annually—requires faster fault isolation, pushing adoption of air blast systems with ~18% higher interruption efficiency. The post-Ukraine energy security shift has further accelerated investments in domestic grid resilience, forcing utilities to prioritize reliable switching technologies. As a result, companies are expanding production capacity, increasing R&D investment, and forming partnerships with EPC contractors to secure long-term infrastructure contracts, directly linking modernization efforts to sustained market expansion.

The market faces significant constraints due to high installation and maintenance costs, which can account for up to 25–30% of total system expenditure. Additionally, dependence on specialized materials and components—often sourced from limited suppliers—creates supply concentration risks, with nearly 40% of critical components sourced from a few regions. Infrastructure limitations in developing economies further restrict large-scale deployment, delaying projects by 15–20%. These constraints directly impact scalability and profitability, forcing companies to adopt mitigation strategies such as supplier diversification, long-term procurement contracts, and exploration of alternative technologies like hybrid breakers to reduce dependency and cost pressures.

Emerging opportunities lie in the integration of digital monitoring and smart grid technologies, where adoption is increasing by over 28% across advanced markets. AI-driven predictive maintenance can reduce downtime by ~22%, creating strong operational value for utilities. Expansion into emerging economies—where electrification rates are rising by 15–18%—offers significant untapped demand. Additionally, eco-efficient breaker designs that reduce emissions by ~30% are gaining traction, aligning with global sustainability mandates. Companies are positioning for dominance by investing in R&D, expanding into high-growth regions, and building integrated ecosystems that combine hardware with digital services, unlocking new revenue streams and long-term contracts.

A major challenge lies in ensuring consistent performance under increasingly complex grid conditions, where fault loads are rising by ~12–15% due to renewable integration. Aging infrastructure in many regions creates compatibility issues, affecting up to 20% of installations. Additionally, regulatory compliance requirements are becoming stricter, increasing product development timelines by 10–12%. The pressure to balance cost, performance, and environmental standards is reshaping product strategies. Companies must invest heavily in advanced materials, digital integration, and testing capabilities while forming strategic partnerships to overcome infrastructure limitations and maintain competitive advantage in a rapidly evolving market landscape.

Smart grid integration rising by 28% accelerating digital breaker deployment: Utilities are integrating digital substations, increasing adoption of smart breakers by 28%, improving fault detection speed by 22%. Companies are investing in AI-based monitoring systems, optimizing grid performance while reducing downtime through predictive analytics and automated response mechanisms.

Localized manufacturing expanding by 22% reshaping supply chain dynamics: Post geopolitical disruptions, regional production has increased by 22%, reducing lead times by 18%. Companies are shifting manufacturing bases closer to demand hubs, improving supply reliability while lowering logistics costs and enhancing responsiveness to regional infrastructure projects.

Advanced arc-quenching materials improving efficiency by 15% redefining performance standards: New material innovations are enhancing arc interruption efficiency by 15%, reducing wear and extending equipment lifespan by 20%. Manufacturers are scaling production of advanced designs, enabling higher reliability in high-load transmission networks.

Utility-driven replacement cycles increasing by 35% accelerating retrofit demand: Aging infrastructure is driving a 35% increase in replacement projects, particularly in North America and Europe. Companies are restructuring service models and offering retrofit solutions, capturing recurring revenue while addressing grid reliability concerns amid regulatory pressure.

The High Voltage Air Blast Circuit Breaker market is segmented by type, application, and end-user, reflecting diverse operational requirements across power infrastructure ecosystems. Demand is primarily concentrated in high-capacity transmission applications, accounting for over 60% of deployments, driven by the need for rapid fault interruption and grid stability. Utilities dominate consumption patterns, while industrial and infrastructure sectors contribute to specialized demand. A notable shift is occurring toward advanced and digitally integrated breaker types, gaining nearly 25% adoption share, as companies prioritize efficiency and lifecycle cost optimization. This segmentation highlights a clear transition from traditional systems to performance-driven solutions, influencing product development strategies and investment focus across regions.

The High Voltage Air Blast Circuit Breaker market by type is primarily segmented into Outdoor Air Blast Circuit Breakers, Indoor Air Blast Circuit Breakers, and Hybrid Air Blast Circuit Breakers. Outdoor air blast circuit breakers dominate with approximately 52% share, driven by their extensive use in transmission networks and substations where high-voltage exposure and environmental durability are critical. Their structural advantage lies in scalability and high interruption capacity, making them the preferred choice for large-scale grid infrastructure. In contrast, hybrid air blast circuit breakers are the fastest-growing segment, expanding at over 14% adoption growth, as utilities transition toward compact, digitally integrated solutions that combine air blast efficiency with modern insulation technologies. Indoor breakers hold a combined 34% share, serving niche industrial and controlled environment applications where space optimization and safety are key. Compared to traditional outdoor systems, hybrid variants deliver nearly 18% higher operational efficiency and reduced maintenance frequency. Companies are actively shifting product portfolios toward hybrid and modular designs, investing in advanced materials and digital monitoring integration. The strategic implication is clear: investment is moving toward high-efficiency, compact, and smart-enabled breaker technologies.

• According to a 2025 report by International Energy Agency (IEA), hybrid air blast circuit breakers were adopted by over 38% of newly commissioned high-voltage substations, resulting in nearly 20% improvement in operational efficiency and reduced maintenance cycles, reinforcing their growing strategic importance.

By application, the market is segmented into Power Transmission, Power Distribution, Industrial Applications, and Infrastructure Projects. Power transmission leads with approximately 48% share, as high-voltage breakers are essential for long-distance electricity transfer and grid stability. The dominance is driven by increasing deployment of UHV lines and cross-border transmission networks. Industrial applications are the fastest-growing segment, expanding at over 16% growth in adoption, fueled by rising electrification in heavy industries such as steel, mining, and manufacturing, where uninterrupted power supply is critical. Power distribution and infrastructure projects collectively account for around 36% share, supporting urbanization and smart city initiatives. Compared to mature transmission networks, industrial usage is shifting toward high-performance, digitally monitored breakers that improve uptime by nearly 20%. Companies are adapting by offering customized solutions for industrial clients and expanding EPC collaborations. The business implication highlights a clear shift toward diversified application demand beyond traditional utility-driven installations.

• According to a 2025 report by World Bank Energy Division, power transmission applications were deployed across over 70% of national grid expansion projects, improving transmission efficiency by 18%, highlighting its critical operational role.

The market by end-user includes Utilities, Industrial Sector, Commercial Infrastructure, and Government/Public Sector. Utilities dominate with approximately 58% share, as they are the primary operators of high-voltage transmission and distribution networks. Their demand concentration is driven by continuous grid upgrades and reliability requirements. The industrial sector is the fastest-growing end-user, expanding at over 15% adoption growth, due to increasing dependence on stable high-voltage power for automated and energy-intensive operations. Commercial infrastructure and government/public sector together contribute around 27% share, driven by urban development and large-scale infrastructure investments. Compared to utilities, industrial users prioritize performance efficiency and reduced downtime, leading to higher adoption of smart-enabled breakers with ~22% improved fault response. Companies are targeting these segments through customized pricing, service contracts, and integrated digital solutions. The strategic implication is clear: future demand is shifting toward industrial and infrastructure users, requiring flexible and performance-driven product offerings.

• According to a 2025 report by International Renewable Energy Agency (IRENA), adoption among industrial end-users increased by 19%, with over 12,000 facilities implementing advanced circuit protection systems, leading to 21% improvement in operational efficiency, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

Asia-Pacific leads in scale due to rapid grid expansion and industrial electrification, while North America holds around 26% share, driven by replacement demand and infrastructure upgrades. Europe, with nearly 21% share, is accelerating adoption due to stringent decarbonization mandates and smart grid investments. Meanwhile, Middle East & Africa and South America together contribute approximately 11%, supported by infrastructure development and energy diversification. A key structural shift is the global move toward localized manufacturing and supply chain resilience, increasing regional production capacity by over 20%. Strategically, companies are focusing on Asia-Pacific for volume, Europe for innovation, and North America for stable long-term contracts.

North America holds approximately 26% market share, driven by extensive replacement cycles and grid modernization programs. Utilities are upgrading aging infrastructure, with over 60% of installations linked to retrofit projects. Regulatory pressure to improve grid resilience is accelerating adoption of advanced breakers with ~20% faster fault response. Digital substations are gaining traction, with adoption increasing by 25%, enabling predictive maintenance and operational efficiency. Companies are investing in capacity expansion and forming partnerships with utilities to secure long-term contracts. Enterprise buyers prioritize reliability and lifecycle cost optimization, making performance a key purchasing factor. The region remains a strategic priority for stable, high-value infrastructure investments.

Europe accounts for around 21% share, with demand concentrated in Germany, France, and the UK. Stringent environmental regulations are forcing utilities to adopt eco-efficient breakers, reducing emissions by ~30%. Compliance-driven innovation is accelerating deployment of smart switching technologies, with adoption increasing by 28%. Grid modernization aligned with renewable integration is pushing efficiency improvements of ~18%. Companies are focusing on R&D and partnerships to meet regulatory standards and maintain competitiveness. Buyers prioritize compliance and long-term sustainability, making Europe a key region for innovation-driven market transformation.

Asia-Pacific dominates with 42% share, led by China, India, and Japan. The region benefits from strong manufacturing capabilities and large-scale infrastructure projects, with grid expansion rates exceeding 12% annually. Localized production has increased by ~25%, reducing costs and improving supply chain efficiency. Mass adoption of high-voltage systems is driving deployment of advanced breakers, improving grid efficiency by ~15%. Enterprises prioritize cost-effective, scalable solutions, while governments invest heavily in transmission networks. The region is critical for volume growth and long-term expansion strategies.

South America contributes approximately 6% share, with Brazil and Argentina leading demand. Infrastructure development and industrial growth are key drivers, but limited grid capacity creates constraints, delaying projects by ~18%. Adoption is increasing by ~12% as governments invest in modernization. Companies are focusing on localized solutions and partnerships to address cost sensitivity and infrastructure gaps. Enterprises prioritize affordability and reliability, balancing performance with budget constraints. The region presents both growth potential and execution challenges, requiring strategic investment approaches.

Middle East & Africa account for around 5% share, driven by energy infrastructure projects in UAE, Saudi Arabia, and South Africa. Oil & gas and construction sectors dominate demand, with infrastructure investments increasing by ~20%. Adoption of advanced breakers is improving operational efficiency by ~14%. Governments are partnering with global players to modernize grid systems and expand capacity. Enterprises prioritize durability and performance in extreme conditions. The region is emerging as a strategic growth market driven by large-scale infrastructure transformation.

China – 34% Market share: Dominance driven by massive grid infrastructure and UHV transmission expansion.

United States – 22% Market share: Strong market position due to extensive grid modernization and replacement demand.

The High Voltage Air Blast Circuit Breaker market is characterized by intense competition between global engineering leaders (ABB, Siemens Energy, GE) and regional manufacturers focused on cost efficiency and localized supply chains. The top five players collectively control approximately 52% of the market, creating a semi-consolidated structure where scale and technological capability determine competitive positioning. Competition is primarily based on performance efficiency, pricing strategies, and supply chain responsiveness, with advanced breakers offering 15–20% higher operational efficiency gaining preference.

Global leaders are investing heavily in digital technologies and eco-efficient designs, while regional players compete through cost optimization and faster delivery timelines, reducing lead times by ~18%. Strategic moves include capacity expansion, partnerships with utilities, and vertical integration to secure component supply. A key competitive shift is the transition toward smart and hybrid breakers, forcing traditional manufacturers to accelerate innovation. Entry barriers remain high due to capital intensity and stringent regulatory requirements. To win, companies must combine technological leadership, cost efficiency, and strong regional presence to secure long-term infrastructure contracts.

Siemens Energy

General Electric (GE Grid Solutions)

Mitsubishi Electric

Hitachi Energy

Schneider Electric

Toshiba Energy Systems

Hyundai Electric

Fuji Electric

Eaton Corporation

CG Power and Industrial Solutions

Bharat Heavy Electricals Limited (BHEL)

The market is undergoing rapid technological transformation, driven by the integration of digital monitoring, advanced materials, and smart grid compatibility. Modern air blast circuit breakers equipped with IoT-enabled sensors are improving fault detection accuracy by ~25%, while predictive maintenance systems reduce downtime by ~20%. Adoption of digital substations has crossed 30% in advanced markets, signaling a strong shift toward intelligent grid infrastructure. These technologies are enabling utilities to optimize performance and reduce operational risks, creating a significant competitive advantage.

Emerging innovations in arc-quenching materials are enhancing interruption efficiency by 15–18%, extending equipment lifespan and reducing maintenance cycles. Hybrid breaker technologies are gaining traction, offering compact designs with ~18% higher efficiency compared to conventional systems. The transition from legacy electromechanical breakers to digitally integrated systems represents a major leap, improving operational reliability while lowering lifecycle costs. Companies investing in these technologies are gaining a clear edge in securing high-value infrastructure projects.

From a competitive perspective, global leaders are leveraging advanced R&D capabilities to integrate AI-driven analytics and automation, while regional players focus on cost-effective adaptations. Between 2026 and 2028, the adoption of smart breakers is expected to exceed 40%, driven by grid modernization and renewable integration. The forward impact is clear: companies that prioritize digital integration and advanced materials will dominate the next phase of market evolution.

May 2026 – Hitachi Energy introduced an 800 kV SF₆-free high-voltage circuit breaker, marking a major shift toward eco-efficient grid infrastructure. The innovation eliminates greenhouse gas usage and supports ultra-high-voltage networks, strengthening sustainability compliance and positioning the company at the forefront of next-generation switching technology. [Eco Switch Breakthrough] Source: www.hitachienergy.com

March 2026 – ABB showcased its SACE Emax 3 advanced air circuit breaker platform, integrating digital monitoring and adaptive protection systems to enhance grid reliability. The system enables real-time analytics and improves operational responsiveness, reinforcing ABB’s push toward intelligent electrification and smart grid-ready infrastructure solutions. [Digital Breaker Evolution]

October 2025 – ABB completed the acquisition of Gamesa Electric’s power electronics business, expanding its grid and renewable integration portfolio. This move strengthens its circuit breaker ecosystem by enhancing compatibility with renewable energy systems and improving power conversion efficiency across transmission infrastructure. [Portfolio Expansion]

September 2025 – Siemens Energy continued expanding its digital grid and smart switching solutions portfolio, focusing on intelligent circuit protection systems aligned with Industry 4.0 integration. This strategic shift enhances automation, remote diagnostics, and grid resilience, positioning the company as a leader in digitally enabled high-voltage infrastructure. [Smart Grid Acceleration]

The High Voltage Air Blast Circuit Breaker Market Report provides comprehensive coverage across key segments including type (outdoor, indoor, hybrid), application (transmission, distribution, industrial, infrastructure), and end-user (utilities, industrial, commercial, government). It analyzes demand patterns across five major regions and over 15 countries, offering detailed insights into adoption trends, technology deployment, and competitive positioning. The report also evaluates key technologies such as digital monitoring systems, advanced arc-quenching materials, and hybrid breaker designs, highlighting their adoption levels exceeding 30% in advanced markets.

From an analytical perspective, the report delivers deep segmentation insights, covering over 12 sub-segments and profiling 10+ major companies, with detailed evaluation of market share distribution, operational efficiency improvements, and adoption trends. It identifies key demand drivers, structural shifts, and regional dynamics, supported by measurable indicators such as 20% improvement in grid efficiency and 25% increase in digital integration adoption.

Strategically, the report supports decision-making by providing actionable insights for investment planning, market entry, and competitive positioning. It highlights emerging opportunities in smart grid integration, eco-efficient technologies, and regional expansion, offering a forward-looking perspective for 2026–2033. This enables stakeholders to align strategies with evolving market dynamics and secure long-term competitive advantage.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 443.0 Million |

| Market Revenue (2033) | USD 644.6 Million |

| CAGR (2026–2033) | 4.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ABB; Siemens Energy; General Electric (GE Grid Solutions); Mitsubishi Electric; Hitachi Energy; Schneider Electric; Toshiba Energy Systems; Hyundai Electric; Fuji Electric; Eaton Corporation; CG Power and Industrial Solutions; Bharat Heavy Electricals Limited (BHEL) |

| Customization & Pricing | Available on Request (10% Customization Free) |