Reports

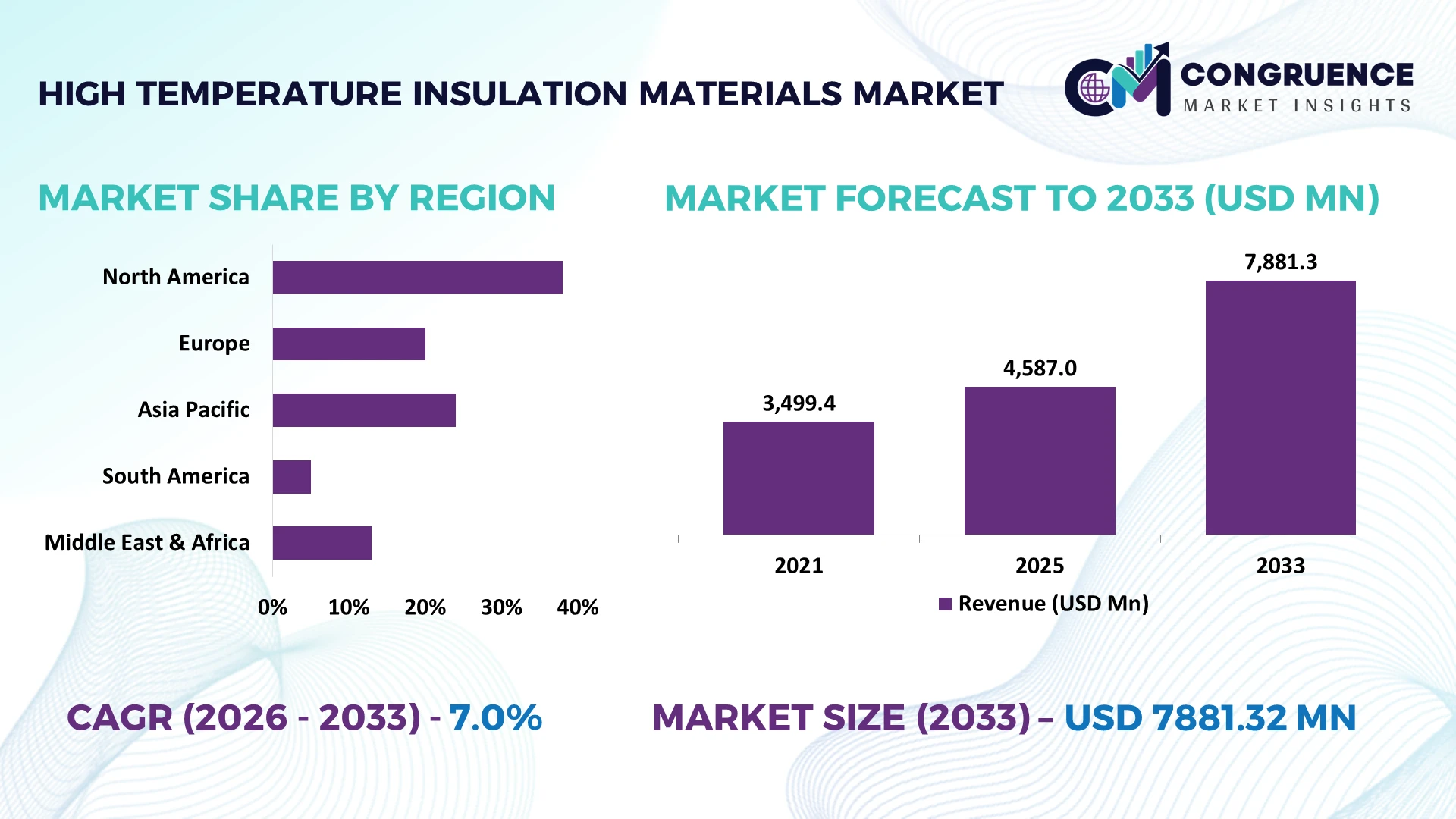

The Global High Temperature Insulation Materials Market was valued at USD 4587 Million in 2025 and is anticipated to reach a value of USD 7881.32 Million by 2033 expanding at a CAGR of 7% between 2026 and 2033. Growth is being accelerated by expanding electric arc furnace capacity, hydrogen-ready industrial infrastructure, and stricter thermal efficiency standards across metals, petrochemicals, cement, and advanced manufacturing facilities.

China remains the dominant production and consumption hub, accounting for nearly 38% of global refractory and high-temperature insulation material demand, supported by over USD 20 billion in industrial decarbonization investments and extensive steel, cement, and battery manufacturing capacity. India records industrial furnace installations growing above 9%, while Europe prioritizes energy-efficient retrofits following continued regional energy security initiatives, driving faster adoption of advanced ceramic fiber and microporous insulation systems.

For manufacturers and investors, prioritizing capacity expansion, energy-efficient product portfolios, and resilient regional supply chains offers the strongest long-term competitive advantage.

Market Size & Growth: USD 4587 million (2025) advancing toward USD 7881.32 million by 2033 at 7% CAGR, supported by industrial electrification and high-efficiency thermal process upgrades.

Top Growth Drivers: Industrial decarbonization contributes 32%, steel modernization 27%, and advanced manufacturing expansion 21% of incremental demand.

Short-Term Forecast: By 2028, advanced insulation solutions reduce industrial heat loss by up to 18% while improving furnace energy efficiency by approximately 12%.

Emerging Technologies: AI-enabled thermal monitoring, automated furnace optimization, and advanced microporous insulation improve operational reliability across high-growth manufacturing facilities.

Regional Leaders: Asia-Pacific exceeds USD 3.6 billion, Europe approaches USD 1.8 billion, and North America surpasses USD 1.5 billion, driven by industrial retrofits and regional manufacturing expansion.

Consumer/End-User Trends: More than 60% of new industrial furnace projects integrate premium insulation systems to improve lifecycle efficiency and lower operating costs.

Pilot/Case Example: In 2025, a large steel plant modernization project improved thermal efficiency by 16% and reduced energy consumption by 11% through advanced insulation upgrades.

Competitive Landscape: Leading manufacturers collectively control roughly 42% of the global market, with major competition centered on Morgan Advanced Materials, Unifrax, RHI Magnesita, Isolite, and Promat.

Regulatory & ESG Impact: Energy-efficiency regulations support over 20% lower industrial heat losses while accelerating replacement of conventional insulation across energy-intensive sectors.

Investment & Funding: More than USD 2 billion in manufacturing expansion and strategic partnerships strengthens regional supply chains and supports localized production capacity.

Innovation & Future Outlook: Next-generation ceramic fibers, aerogel composites, and digital thermal analytics accelerate performance optimization while reinforcing resilient global industrial supply networks.

High Temperature Insulation Materials Market demand continues expanding across steel production, petrochemical processing, battery manufacturing, and industrial furnace modernization, where advanced ceramic fibers and microporous products improve thermal performance. Nearly 30% of newly commissioned high-temperature industrial facilities prioritize energy-efficient insulation systems, while ongoing supply-chain localization and tightening industrial efficiency regulations strengthen adoption, creating a strong foundation for the following strategic market assessment.

High temperature insulation materials have become strategically important as manufacturers prioritize energy efficiency, process reliability, and industrial decarbonization across steel, cement, glass, petrochemicals, and battery manufacturing. Supply-chain restructuring since recent geopolitical disruptions has accelerated localization of ceramic fiber and microporous insulation production, reducing procurement risks while supporting faster project execution. Industrial operators increasingly specify advanced insulation during new furnace construction rather than retrofit stages, strengthening long-term equipment performance and lifecycle economics.

Modern microporous insulation delivers up to 35% lower thermal conductivity than conventional calcium silicate systems while reducing equipment surface temperatures by nearly 20%, enabling measurable energy savings and improved worker safety. China leads large-scale deployment through integrated heavy manufacturing clusters, whereas Germany emphasizes premium engineered insulation for high-efficiency industrial facilities and hydrogen-ready process equipment. Over the next two to three years, digital thermal monitoring is expected to be integrated into more than 40% of newly commissioned high-temperature industrial installations, improving predictive maintenance and operational stability.

A recent industrial furnace modernization project incorporating ceramic fiber modules and digital temperature monitoring reduced maintenance shutdown frequency by approximately 15% while extending service intervals. In response, manufacturers are expanding localized production, investing in advanced materials research, and forming technology partnerships to strengthen application engineering capabilities. Companies combining high-performance insulation with digital performance optimization will establish stronger competitive positioning through superior operational efficiency, regulatory compliance, and long-term customer value.

Industrial modernization programs are accelerating adoption of high-performance insulation systems across steel, cement, petrochemical, and battery manufacturing. Advanced insulation solutions reduce heat losses by nearly 18% while improving furnace efficiency by approximately 12%, supporting lower operating costs and improved process stability. India continues expanding electric arc furnace capacity, while China upgrades industrial facilities under energy-efficiency mandates, increasing demand for ceramic fiber and microporous insulation. In response, manufacturers are expanding domestic production, investing in lightweight insulation technologies, and partnering with industrial engineering firms to deliver customized thermal management solutions. A notable strategic advantage is the shift toward lifecycle-based procurement, where operating efficiency increasingly outweighs initial material cost in purchasing decisions.

Volatility in alumina, silica, and specialty ceramic raw material prices continues to pressure production economics and project planning. Input cost fluctuations of nearly 15% have affected procurement strategies, while imported specialty materials still represent around 30% of supply requirements for several advanced insulation grades. Logistics disruptions and extended delivery schedules further complicate industrial project execution, particularly for customized thermal systems. Companies are responding through supplier diversification, localized sourcing agreements, and long-term procurement contracts that improve pricing stability and inventory resilience. Organizations with vertically integrated production and regional manufacturing capabilities are achieving stronger cost control and more reliable customer delivery performance.

Next-generation insulation materials combined with intelligent monitoring technologies are creating new value beyond conventional thermal protection. AI-assisted thermal diagnostics and digital sensors improve maintenance planning, while advanced aerogel composites reduce insulation thickness by nearly 40% without sacrificing thermal performance. Japan and South Korea continue investing in high-efficiency manufacturing facilities where precision thermal control is increasingly important for semiconductor, battery, and specialty materials production. Companies are strengthening competitive differentiation through collaborative R&D programs, application engineering services, and ecosystem partnerships integrating insulation materials with industrial automation platforms. An emerging strategic opportunity lies in performance-based service models that guarantee measurable energy savings throughout equipment lifecycles.

Deploying advanced insulation materials consistently across complex industrial facilities requires specialized engineering expertise, installation precision, and continuous performance validation. Improper installation can reduce insulation effectiveness by over 20%, while skilled thermal engineering personnel remain limited in several industrial markets. Integration with digital monitoring platforms and predictive maintenance systems also increases project complexity during large-scale facility modernization. Manufacturers are investing in certified installer networks, technical training programs, and digital engineering tools to standardize deployment quality across industrial sites. Companies that successfully combine material innovation with engineering support and workforce capability development will secure stronger long-term competitiveness and sustain reliable operational performance.

Advanced Low-Thickness Insulation Adoption: Manufacturers are replacing conventional refractory linings with ceramic fiber modules and microporous insulation that reduce insulation thickness by nearly 35% while improving thermal retention by approximately 18%. Industrial energy-efficiency regulations and furnace modernization programs are accelerating deployment, prompting suppliers to expand premium product portfolios and automated manufacturing capacity.

Localized Manufacturing Supply Chains: Companies are restructuring production closer to industrial hubs as imported specialty material dependence declines by nearly 15% and domestic procurement rises above 60% in several manufacturing markets. Continued geopolitical trade adjustments and logistics uncertainty are encouraging regional partnerships, localized inventory strategies, and multi-source procurement models that improve delivery reliability and operational continuity.

Digital Thermal Performance Monitoring: Industrial operators increasingly integrate AI-enabled thermal analytics and sensor-based monitoring, reducing unplanned maintenance events by approximately 14% while improving inspection accuracy by over 20%. Enterprise digital transformation initiatives are driving insulation suppliers to collaborate with automation providers, offering integrated monitoring platforms alongside high-temperature insulation systems instead of standalone materials.

Hydrogen-Ready Industrial Infrastructure: Hydrogen-capable furnaces and next-generation process heating systems require insulation materials with improved thermal shock resistance and lower heat leakage, increasing demand for advanced products by nearly 22%. Steel producers and engineering contractors are strengthening technology partnerships, accelerating qualification programs, and redesigning insulation configurations to support evolving industrial decarbonization pathways.

Ceramic Fiber remains the leading segment with an estimated 39% market share, driven by superior thermal resistance, lightweight construction, and easier installation compared with conventional insulation materials. Its scalability across steel, petrochemical, glass, and power applications makes it the preferred solution for modern furnace systems. Calcium Silicate continues serving mature industrial facilities requiring structural durability, while Insulating Firebricks retain importance in high-load refractory environments where mechanical strength remains critical. Companies continue expanding ceramic fiber production capacity and developing low-shot formulations to improve thermal efficiency and workplace safety.

Aerogel represents the fastest-growing segment as industries prioritize thinner insulation profiles without sacrificing thermal performance. Aerogel-based solutions reduce heat transfer by nearly 30% compared with several traditional materials, while adoption in advanced manufacturing facilities continues rising above 16% annually in selected industrial projects. Mineral Wool remains strategically relevant for medium-temperature industrial applications due to cost competitiveness and acoustic performance. Manufacturers are increasing investments in advanced composite insulation technologies and application-specific product development to strengthen long-term competitive differentiation.

Furnaces account for approximately 41% of total demand because they operate continuously under extreme temperatures where thermal efficiency directly affects production costs and equipment lifespan. Industrial Kilns remain the second-largest application across cement and ceramics manufacturing, while Metal Processing increasingly specifies advanced insulation to improve process stability and reduce heat losses. Companies are integrating modular insulation systems that shorten maintenance shutdowns by nearly 15% and improve operational efficiency across high-temperature production environments.

Petrochemical Processing is emerging as the fastest-growing application as refiners and chemical producers upgrade thermal infrastructure to improve energy utilization and process safety. Adoption of advanced insulation systems has increased by approximately 19% in newly commissioned high-temperature processing units, while Power Plants continue replacing aging insulation during maintenance cycles to improve reliability. Suppliers are expanding engineering support, customized installation services, and digital inspection capabilities to strengthen customer retention and long-term operational performance.

Iron & Steel remains the dominant end-user segment with an estimated 43% market share due to continuous furnace operations, extensive refractory replacement cycles, and growing adoption of energy-efficient production technologies. Cement and Glass Manufacturing maintain steady demand because kiln efficiency and thermal stability directly influence operating costs and product quality. Suppliers increasingly offer customized insulation packages, lifecycle service agreements, and application engineering support to strengthen long-term industrial partnerships.

Petrochemical is the fastest-growing end-user segment as refinery upgrades and specialty chemical production require insulation materials capable of sustaining higher process temperatures with improved durability. Adoption of advanced insulation systems has increased by nearly 20% in newly modernized petrochemical facilities, while Power Generation continues investing in thermal efficiency improvements during scheduled maintenance programs. Manufacturers are responding through product customization, localized technical support, and collaborative engineering partnerships, positioning themselves closer to high-value industrial customers with specialized thermal management requirements.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 7.9% between 2026 and 2033.

Industrial Decarbonization Strengthens Premium Insulation Adoption

North America represents a mature high-temperature insulation materials market, supported by extensive modernization across steel, petrochemical, power generation, and advanced manufacturing facilities. The region contributes approximately 24% of global demand, with industrial retrofits increasingly replacing legacy refractory systems with ceramic fiber and microporous insulation. More than 55% of large industrial furnace refurbishment projects now incorporate energy-efficient insulation technologies to improve process stability and reduce maintenance frequency. Manufacturing reshoring initiatives and investments in battery materials, hydrogen infrastructure, and specialty chemicals continue expanding deployment opportunities. Companies are strengthening regional manufacturing capacity, increasing engineering support, and establishing long-term supply agreements to improve delivery performance and technical service across industrial customers.

United States Market Outlook: The United States remains the regional leader through its large steel, refining, aerospace, and specialty manufacturing sectors. More than 60% of advanced industrial thermal modernization projects are concentrated within the country, supported by investments in industrial efficiency and domestic manufacturing expansion. Companies continue deploying digital thermal monitoring, customized insulation systems, and localized engineering services to improve operational productivity while extending equipment lifecycle performance.

Energy Efficiency Regulations Accelerate Industrial Modernization

Europe maintains a strong position through strict industrial efficiency standards, advanced engineering expertise, and widespread replacement of aging thermal infrastructure. The region accounts for nearly 22% of global market demand, with Germany, Italy, and France leading deployment across steel, glass, and chemical manufacturing. More than 48% of newly upgraded industrial heat-processing systems incorporate advanced insulation materials to improve thermal efficiency and reduce operational emissions. Industrial operators increasingly specify lightweight ceramic fiber systems during plant modernization, while suppliers strengthen collaborative development programs with furnace manufacturers to deliver integrated thermal management solutions tailored for energy-intensive production environments.

Germany Market Outlook: Germany leads the European market through its advanced industrial equipment manufacturing, chemical processing, and engineering capabilities. Industrial modernization initiatives continue supporting deployment of premium insulation technologies across high-temperature production assets. Approximately 30% of large industrial furnace upgrades incorporate digital thermal monitoring alongside next-generation insulation systems, enabling manufacturers to improve production consistency and optimize long-term operating efficiency.

Manufacturing Scale Drives Global Leadership

Asia-Pacific dominates the global market through its extensive steel production, cement manufacturing, petrochemical processing, and expanding battery supply chain. The region contributes approximately 46% of global demand, supported by continuous industrial capacity expansion and infrastructure investment. China and India account for a significant share of newly commissioned high-temperature industrial facilities, while more than 65% of regional furnace modernization projects now integrate advanced ceramic fiber insulation. Manufacturers continue expanding domestic production, strengthening export capabilities, and investing in automated manufacturing lines to meet growing industrial requirements while improving product consistency and supply reliability.

China Market Outlook: China remains the largest individual market due to its unmatched concentration of steel, cement, petrochemical, and advanced manufacturing industries. The country produces a substantial proportion of global refractory and thermal insulation materials while continuously upgrading industrial facilities under energy-efficiency programs. More than one-third of newly installed industrial heat-processing equipment incorporates advanced insulation technologies, encouraging suppliers to expand premium product portfolios and localized research capabilities.

Industrial Upgrades Support Steady Demand

South America continues strengthening demand through modernization of mining, cement, metals, and petrochemical facilities where thermal efficiency improvements directly influence operating economics. The region represents approximately 5% of global demand, with Brazil accounting for the largest deployment activity. Industrial operators increasingly replace aging insulation systems during scheduled maintenance, while new mining and mineral processing projects support incremental adoption of advanced thermal materials. More than 18% of major industrial refurbishment programs now specify lightweight insulation solutions to reduce maintenance complexity. Suppliers are expanding regional distribution partnerships and technical support networks to improve market accessibility despite infrastructure and logistics limitations.

Brazil Market Outlook: Brazil leads regional demand through its diversified industrial base, including steelmaking, cement production, mining, and petrochemical processing. Continuous investment in industrial productivity and energy optimization supports wider adoption of premium insulation materials. Approximately 40% of large industrial maintenance projects within the country now include thermal insulation upgrades, encouraging manufacturers to strengthen local inventories, engineering expertise, and long-term industrial partnerships.

Energy Infrastructure Investment Reshapes Demand

The Middle East & Africa market is gaining momentum through large-scale investments in refining, petrochemicals, metals production, and industrial infrastructure modernization. The region contributes roughly 3% of global demand but records expanding deployment across newly commissioned industrial complexes. More than 25% of new high-temperature processing facilities integrate advanced insulation systems designed for higher operating efficiency and extended equipment durability. Industrial diversification initiatives and continued investment in downstream manufacturing encourage suppliers to establish regional partnerships, localized technical services, and application engineering capabilities that improve project execution and lifecycle performance.

Saudi Arabia Market Outlook: Saudi Arabia remains the leading country market due to extensive refinery capacity, petrochemical expansion, and industrial diversification initiatives. Large industrial projects increasingly prioritize advanced thermal management systems to improve process efficiency and equipment reliability. More than 20% of recently commissioned high-temperature industrial facilities incorporate premium insulation technologies, encouraging suppliers to expand regional manufacturing partnerships and specialized engineering support for complex industrial applications.

Competition in the High Temperature Insulation Materials Market is led by Morgan Advanced Materials, Promat, Isolite Insulating Products, RHI Magnesita, and Unifrax, competing against regional ceramic fiber manufacturers and cost-focused refractory suppliers. The top five players collectively control approximately 42% of global market activity, while regional producers compete aggressively on localized supply and faster delivery. Technology leaders differentiate through advanced ceramic fibers, microporous insulation, and engineered application support, whereas regional manufacturers emphasize pricing advantages of 10–15% and shorter lead times of nearly 20%. Global companies strengthen positions through capacity expansion, strategic partnerships with furnace OEMs, product innovation, and selective vertical integration of specialty raw materials to improve supply resilience. Competition is shifting toward performance-based solutions integrating thermal engineering with digital monitoring rather than material supply alone. Rising qualification requirements, proprietary formulations, and application-specific certification create significant entry barriers. Winning requires scalable manufacturing, superior thermal performance, localized engineering support, resilient procurement, and continuous product innovation rather than competing solely on price.

Morgan Advanced Materials

Promat

Unifrax

RHI Magnesita

Isolite Insulating Products

IBIDEN Co., Ltd.

Luyang Energy-Saving Materials Co., Ltd.

Rath Group

Zircar Ceramics

Nutec Group

BNZ Materials, Inc.

Calderys

Shandong Minye Refractory Fibre Co., Ltd.

Advanced ceramic fiber systems, microporous insulation panels, and engineered aerogel composites are replacing conventional calcium silicate and dense refractory insulation in high-temperature processing environments. Modern microporous insulation delivers nearly 35% lower thermal conductivity and reduces heat losses by approximately 18% compared with traditional solutions, while thinner profiles increase usable equipment space. More than 45% of newly designed industrial furnaces now specify lightweight insulation systems because installation time is shorter and maintenance intervals are extended, improving operational continuity across steel, petrochemical, and glass manufacturing.

Digital thermal monitoring has become an important integration trend, combining embedded sensors, AI-assisted analytics, and predictive maintenance platforms with insulation systems. Facilities deploying continuous thermal monitoring report approximately 20% better temperature consistency and nearly 15% fewer unplanned maintenance interruptions. Technology leaders and industrial OEMs benefit most because integrated thermal management packages create stronger customer retention and higher-value engineering services than standalone insulation materials.

Between 2026 and 2028, hybrid insulation architectures combining ceramic fibers, aerogel composites, and digital diagnostics will reshape industrial heat management. Companies investing early in automated manufacturing, application engineering, and intelligent thermal performance platforms will strengthen competitive positioning through faster deployment, lower lifecycle costs, higher energy efficiency, and differentiated industrial service capabilities.

January 2024 Morgan Advanced Materials announced the commercial start-up of its expanded Yixing insulating firebrick facility in China, increasing production capacity by more than 50% to support petrochemical, steel, aluminium, and battery-material customers while strengthening regional manufacturing resilience.

June 2025 Morgan Advanced Materials completed its first real-time ceramic sintering research using advanced synchrotron imaging, enabling direct observation of ceramic microstructure formation and accelerating development of higher-performance thermal insulation materials for industrial applications.

March 2025 Morgan Advanced Materials reported that its Thermal Products business delivered £348.2 million in annual sales, with management maintaining investment in advanced thermal solutions despite challenging industrial conditions, reinforcing long-term product development and operational optimization priorities.

April 2026 Morgan Advanced Materials highlighted high-growth thermal management markets as a strategic priority, emphasizing continued portfolio optimization and operational expansion to strengthen competitiveness across energy-intensive industries requiring advanced high-temperature insulation technologies. Source:(Morgan Advanced Materials)

The report provides a comprehensive assessment of the global High Temperature Insulation Materials Market across Ceramic Fiber, Calcium Silicate, Insulating Firebricks, Aerogel, and Mineral Wool, evaluating performance across furnaces, industrial kilns, power plants, petrochemical processing, and metal processing applications. It further analyzes demand from iron & steel, petrochemical, power generation, cement, and glass manufacturing industries while covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of the assessment focuses on industrial modernization, energy-efficiency deployment, and technology adoption patterns.

The study delivers strategic insights into competitive positioning, supply-chain developments, manufacturing expansion, digital thermal management technologies, and emerging high-performance insulation solutions. It evaluates company strategies, regional deployment trends, product innovation, and industrial investment priorities between 2026 and 2033, enabling stakeholders to identify high-potential application areas, optimize expansion planning, strengthen procurement strategies, and improve long-term competitive decision-making across evolving industrial heat management markets.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 4587 Million |

Market Revenue in 2033 | USD 7881.32 Million |

CAGR (2026 - 2033) | 7% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Morgan Advanced Materials, Promat, Unifrax, RHI Magnesita, Isolite Insulating Products, IBIDEN Co., Ltd., Luyang Energy-Saving Materials Co., Ltd., Rath Group, Zircar Ceramics, Nutec Group, BNZ Materials, Inc., Calderys, Shandong Minye Refractory Fibre Co., Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |