Reports

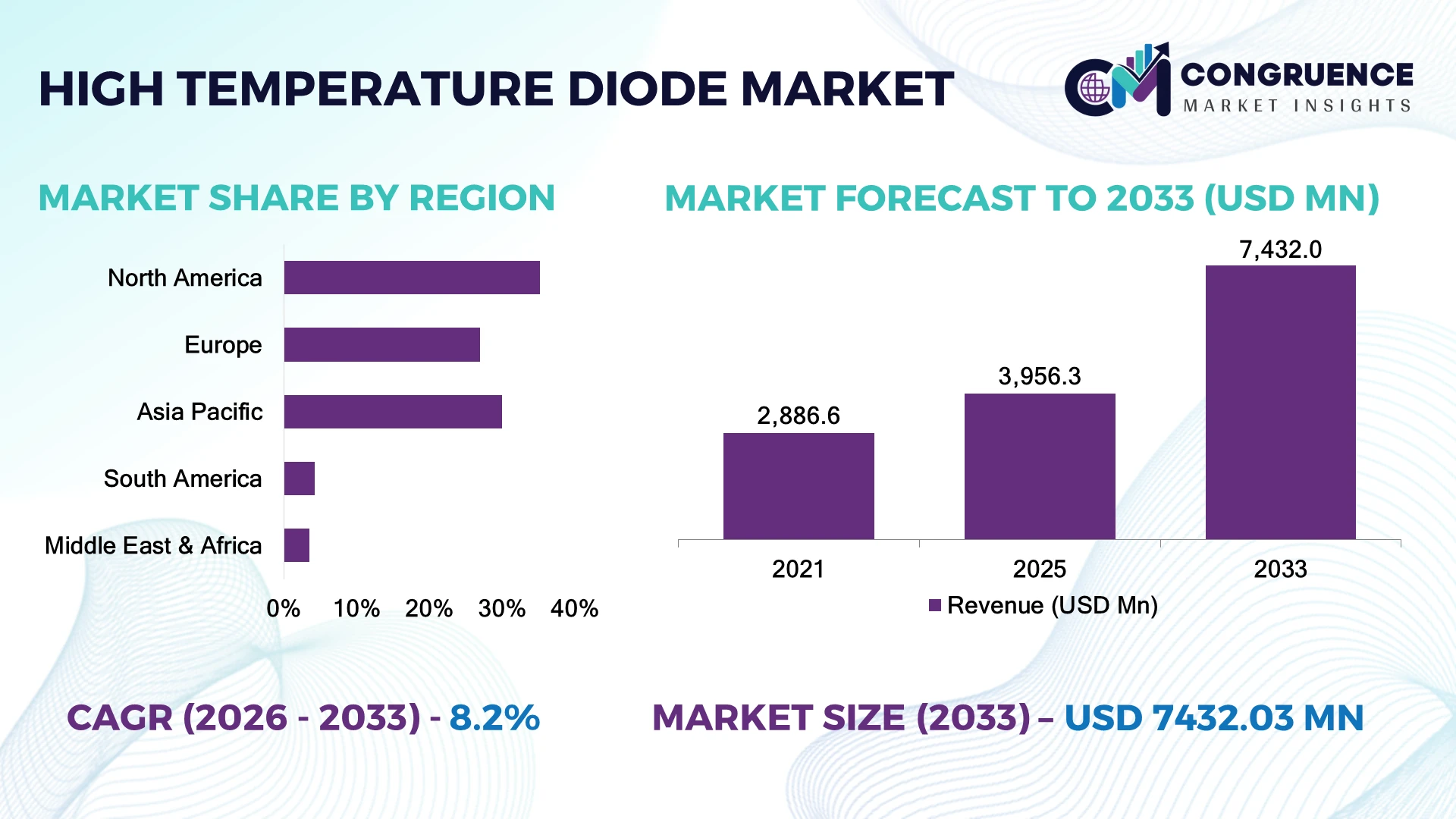

The Global High Temperature Diode Market was valued at USD 3,956.3 Million in 2025 and is anticipated to reach a value of USD 7,432.0 Million by 2033 expanding at a CAGR of 8.2% between 2026 and 2033. Growth is being driven by increasing deployment of high-temperature power electronics in electric vehicles, aerospace systems, industrial automation, and wide-bandgap semiconductor applications requiring superior thermal reliability.

The United States leads the High Temperature Diode Market with approximately 34% of advanced power semiconductor production, supported by investments exceeding USD 18 billion in domestic semiconductor manufacturing and defense electronics. Compared with China, the United States maintains stronger adoption of high-reliability aerospace and industrial power devices, while China leads high-volume electronics manufacturing. Ongoing semiconductor supply-chain realignment following global geopolitical trade policies continues accelerating regional fabrication investments.

Strategic investment in wide-bandgap semiconductor technologies and localized fabrication capabilities is becoming essential for long-term market leadership.

Market Size & Growth: Valued at USD 3,956.3 Million in 2025 and projected to reach USD 7,432.0 Million by 2033 at a CAGR of 8.2%, supported by expanding wide-bandgap semiconductor adoption.

Top Growth Drivers: Electric vehicles (+29%), industrial automation (+21%), and aerospace electronics (+18%) continue strengthening market demand.

Short-Term Forecast: By 2028, device reliability improves by 17%, while thermal management costs decline by approximately 12%.

Emerging Technologies: Silicon carbide, gallium nitride, and AI-assisted semiconductor manufacturing improve thermal efficiency by nearly 20%.

Regional Leaders: North America exceeds USD 2.35 Billion, Asia-Pacific approaches USD 2.90 Billion, and Europe surpasses USD 1.52 Billion through semiconductor expansion.

Consumer/End-User Trends: Nearly 46% of industrial power electronics manufacturers now prioritize high-temperature diode integration.

Pilot/Case Example: A 2026 industrial power module deployment improved thermal endurance by 19% while reducing system failures by 14%.

Competitive Landscape: The top five suppliers control approximately 56% market share, led by Infineon Technologies, onsemi, STMicroelectronics, Vishay Intertechnology, and ROHM Semiconductor.

Regulatory & ESG Impact: Energy-efficiency initiatives improve power conversion performance by approximately 15% across industrial applications.

Investment & Funding: Industry investments exceed USD 5.4 Billion, supported by fabrication expansion, regional semiconductor localization, and strategic partnerships.

Innovation & Future Outlook: Wide-bandgap materials, advanced packaging, and intelligent power modules are reshaping global semiconductor competition.

High temperature diodes are becoming essential components in electric mobility, renewable energy systems, aerospace electronics, and industrial power conversion where thermal stability directly influences operational reliability. Silicon carbide-based devices now represent nearly 32% of next-generation high-temperature power designs. Ongoing semiconductor localization initiatives and stricter energy-efficiency regulations continue accelerating investment in advanced power electronics, leading naturally into the market's evolving strategic landscape.

The High Temperature Diode Market has become strategically important as industries demand power semiconductor devices capable of operating reliably under extreme thermal conditions. Rapid electrification, industrial automation, and aerospace modernization are increasing dependence on high-performance semiconductor components, while semiconductor supply-chain restructuring is encouraging regional fabrication expansion and advanced materials investment to improve manufacturing resilience.

Wide-bandgap high temperature diodes deliver approximately 25% lower switching losses than conventional silicon-based devices while maintaining superior thermal stability and longer operational life. Asia-Pacific leads large-scale semiconductor manufacturing, whereas North America maintains technological leadership in aerospace, defense, and advanced industrial electronics. Over the next two to three years, adoption of silicon carbide and gallium nitride power devices is expected to exceed 45% across newly developed high-performance power electronics platforms, strengthening system efficiency and reliability.

Manufacturers are expanding wafer fabrication capacity, investing in advanced semiconductor packaging, and forming strategic partnerships with automotive and industrial OEMs to accelerate commercialization. Integrated power modules combining high-temperature diodes with intelligent thermal management are becoming standard across demanding operating environments. This transition positions high temperature diode technologies as a critical competitive differentiator for companies pursuing higher power density, greater operational efficiency, and long-term resilience in advanced electronic systems.

The rapid transition toward silicon carbide and gallium nitride power electronics is accelerating demand for high temperature diodes capable of operating under extreme thermal conditions. Nearly 49% of next-generation electric powertrain platforms now integrate high-temperature semiconductor devices, while thermal efficiency improves by approximately 21% compared with conventional silicon components. The United States continues expanding domestic semiconductor manufacturing under strategic fabrication initiatives, strengthening local production of advanced power devices. This structural shift enables higher power density, improved system reliability, and reduced cooling requirements. In response, semiconductor manufacturers are expanding wafer fabrication capacity, investing in advanced packaging technologies, and forming long-term partnerships with automotive and industrial OEMs to accelerate commercialization of next-generation high-temperature power electronics.

High production costs associated with silicon carbide substrates, gallium nitride materials, and specialized wafer processing continue restricting broader deployment across cost-sensitive applications. Wide-bandgap wafers typically increase semiconductor manufacturing costs by approximately 28%, while substrate materials account for nearly 36% of total device production expenses. Limited global availability of high-quality crystal substrates remains a supply-chain constraint following continued semiconductor localization efforts across major manufacturing countries. These structural limitations compress supplier margins and delay production scalability for emerging applications. Companies are responding by localizing wafer production, securing long-term raw material agreements, and improving manufacturing yields through process optimization to reduce dependence on constrained material supply.

Growing deployment of intelligent power electronics creates significant opportunities for high temperature diodes integrated within compact power modules for electric mobility, renewable energy, and industrial automation. More than 41% of new industrial inverter platforms now prioritize integrated power module architectures, while advanced packaging improves thermal dissipation by approximately 18% and reduces system footprint by nearly 16%. Japan continues investing in next-generation semiconductor packaging technologies supporting higher operating temperatures and greater device reliability. Manufacturers are expanding R&D collaborations, strengthening partnerships with power module suppliers, and developing application-specific semiconductor solutions. A key strategic opportunity lies in combining high-temperature diodes with intelligent power control to simplify system architecture while improving operational efficiency.

Ensuring reliable long-term performance under continuous high-temperature operation remains a major engineering challenge for semiconductor manufacturers. Around 31% of qualification activities focus on thermal reliability validation, while device testing requirements have increased by nearly 23% for advanced automotive and aerospace electronics. Germany's industrial electronics sector continues tightening functional reliability standards for power semiconductor components operating under harsh environmental conditions. These validation requirements extend development cycles and increase engineering costs across high-performance applications. Companies must strengthen simulation capabilities, invest in advanced reliability laboratories, and collaborate with OEMs on application-specific qualification programs to achieve consistent product performance across demanding operational environments.

Advanced Packaging Expansion: Semiconductor manufacturers are increasing adoption of advanced power packaging technologies, improving thermal dissipation by approximately 19% while reducing package size by nearly 14%. Growing demand for compact high-power electronics is accelerating manufacturing upgrades. Companies are expanding automated packaging lines and strengthening supply partnerships to improve production efficiency and device reliability.

Localized Wafer Manufacturing: Semiconductor fabrication is becoming increasingly regionalized as the United States, Japan, and Europe expand domestic production capabilities. Localized wafer sourcing has reduced procurement lead times by around 17% while improving supply stability by approximately 15%. Manufacturers are restructuring supplier networks and increasing fabrication investments to strengthen resilience against geopolitical semiconductor supply disruptions.

Automotive Electrification Integration: Electric vehicle manufacturers are accelerating deployment of high temperature diodes within traction inverters and onboard charging systems. Device utilization across next-generation electric power platforms has increased by nearly 24%, while improved thermal endurance extends component operating life by approximately 18%. Semiconductor suppliers are expanding automotive qualification programs and collaborative product development with vehicle manufacturers.

AI-Driven Manufacturing Control: AI-enabled semiconductor process monitoring is improving fabrication consistency by approximately 16% while reducing production defects by nearly 13%. Rather than focusing solely on capacity expansion, manufacturers are integrating intelligent process analytics to improve wafer yields, shorten production cycles, and strengthen competitive positioning across advanced power semiconductor manufacturing.

Silicon High Temperature Diodes account for approximately 61% of the market owing to their established manufacturing ecosystem, cost efficiency, and broad compatibility with industrial power electronics. Their mature fabrication processes and extensive qualification across automotive, industrial, and consumer applications continue supporting high-volume deployment. Silicon Carbide (SiC) High Temperature Diodes represent the fastest-growing segment as manufacturers prioritize higher switching efficiency, elevated operating temperatures, and lower energy losses in electric vehicles and renewable power systems. Gallium Nitride (GaN) diodes are steadily expanding across compact, high-frequency applications, while other specialty semiconductor materials retain strategic importance for aerospace and defense electronics. Companies are increasing investments in wide-bandgap semiconductor technologies, expanding wafer production capacity, and strengthening partnerships with automotive OEMs to accelerate commercialization.

Investment priorities are steadily shifting toward next-generation semiconductor materials capable of delivering higher power density and improved thermal performance. Manufacturers in the United States and Japan are expanding advanced packaging capabilities and product portfolios to support increasingly demanding high-temperature electronic applications.

According to the 2025 International Electron Devices Meeting (IEDM), wide-bandgap semiconductor technologies continue gaining momentum for high-temperature and high-power applications due to superior thermal efficiency and power conversion performance.

Power Electronics account for approximately 44% of High Temperature Diode demand as industrial drives, power supplies, traction inverters, and renewable energy converters increasingly require thermally stable semiconductor components. High-temperature diodes improve system efficiency, reduce cooling requirements, and enhance long-term operational reliability across demanding power applications. Electric Vehicle Systems represent the fastest-growing application as high-voltage powertrains, onboard chargers, and battery management systems increasingly integrate wide-bandgap semiconductor devices. Aerospace and defense electronics continue strengthening demand for extreme-environment reliability, while industrial automation and oil & gas equipment remain important users requiring consistent high-temperature operation. Nearly 38% of newly developed industrial power platforms now integrate advanced thermal semiconductor solutions to improve system durability.

Manufacturers are expanding application-specific semiconductor portfolios while strengthening collaboration with power module developers and system integrators. Product optimization, automated production, and advanced packaging technologies continue improving deployment efficiency across mission-critical power electronics.

A 2026 IEEE Power Electronics Society technical assessment highlighted that high-temperature semiconductor devices are becoming a core design priority for advanced power conversion systems requiring greater thermal reliability and operational efficiency.

Automotive manufacturers account for approximately 39% of High Temperature Diode consumption, supported by expanding electric vehicle production, increasing electronic content per vehicle, and growing adoption of high-voltage power electronics. The Renewable Energy sector represents the fastest-growing end-user group as solar inverters, wind power converters, and grid-scale energy storage systems increasingly require thermally robust semiconductor devices. Industrial manufacturing continues generating stable demand through automation and motor control systems, while aerospace and defense organizations prioritize high-temperature diodes for mission-critical electronic platforms operating in extreme environments. Nearly 34% of new industrial power conversion projects now specify high-temperature semiconductor components to improve long-term reliability and system efficiency.

Suppliers are targeting these customer groups through automotive-grade product qualification, customized packaging solutions, strategic pricing models, and long-term development partnerships. Companies are also strengthening technical support and application engineering capabilities to address increasingly specialized high-power electronic system requirements.

According to the 2025 JEDEC Solid State Technology Association, qualification standards for automotive and industrial power semiconductors continue evolving as manufacturers prioritize higher thermal endurance, reliability, and long-term device performance across advanced electronic systems.

North America accounted for the largest market share at 35.2%in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Domestic Semiconductor Expansion Reinforces Power Electronics Leadership

North America leads the High Temperature Diode Market through advanced semiconductor fabrication, strong aerospace and defense electronics production, and expanding electric vehicle manufacturing. The region contributes approximately 35% of global market demand, supported by significant investments in power semiconductor fabrication and wide-bandgap material development. Nearly 47% of newly commissioned high-power industrial electronics projects incorporate high-temperature semiconductor devices to improve thermal reliability and energy efficiency. Manufacturers continue expanding silicon carbide wafer production, strengthening packaging capabilities, and forming long-term partnerships with automotive and industrial OEMs. These initiatives improve supply resilience while accelerating commercialization of advanced power electronics for high-performance operating environments.

United States Market Outlook: The United States dominates regional demand through its leadership in semiconductor fabrication, defense electronics, electric vehicle technologies, and industrial automation. More than 52% of North America's advanced power semiconductor production is concentrated in the country, supported by continued investment in domestic wafer manufacturing and advanced packaging facilities. Strong collaboration between semiconductor manufacturers, research institutions, and automotive companies continues strengthening innovation across high-temperature diode technologies.

Wide-Bandgap Innovation Supports Industrial Electrification

Europe maintains a strong market position through advanced automotive manufacturing, industrial automation, and renewable energy infrastructure. The region accounts for approximately 27% of global demand, supported by increasing deployment of silicon carbide and gallium nitride power electronics across electric mobility and industrial power conversion. Nearly 36% of newly developed industrial power platforms integrate advanced thermal semiconductor technologies to improve operational efficiency. Manufacturers continue expanding semiconductor research, advanced packaging capabilities, and strategic collaborations to strengthen regional technological competitiveness.

Germany Market Outlook: Germany remains Europe's leading center for automotive electronics, industrial automation, and power semiconductor innovation. The country's strong electric vehicle ecosystem and advanced manufacturing infrastructure continue driving demand for high-temperature diodes in traction inverters and industrial power systems. Approximately 44% of Europe's automotive power electronics development programs are associated with German manufacturers and technology suppliers, reinforcing long-term investment in advanced semiconductor technologies.

Manufacturing Scale Accelerates Wide-Bandgap Adoption

Asia-Pacific represents the fastest-expanding High Temperature Diode Market through its extensive semiconductor fabrication network, electronics manufacturing capacity, and electric vehicle production. The region contributes nearly 49% of global semiconductor manufacturing output, supporting rapid deployment of advanced power devices across industrial and consumer applications. China, Japan, South Korea, and Taiwan continue expanding wafer fabrication capacity and advanced packaging infrastructure. Semiconductor manufacturers have improved localized production capabilities, reducing supply lead times by approximately 18% while strengthening regional manufacturing resilience.

China Market Outlook: China leads regional demand through its large-scale semiconductor manufacturing, electric vehicle production, and industrial electronics ecosystem. More than 56% of regional power semiconductor packaging capacity is concentrated within China, encouraging broader deployment of high-temperature diode technologies. Domestic manufacturers continue investing in silicon carbide wafer processing, automated fabrication, and integrated semiconductor supply chains to strengthen both domestic production and export competitiveness.

Industrial Automation Expands Semiconductor Utilization

South America is gradually increasing adoption of high temperature diodes as industrial automation, renewable energy installations, and power infrastructure modernization continue advancing. Brazil and Argentina remain the region's principal industrial manufacturing centers, supporting greater deployment of thermally robust semiconductor devices across industrial equipment and energy systems. Approximately 21% of recent industrial automation upgrades now integrate advanced power semiconductor technologies. Limited local semiconductor production remains a structural constraint, encouraging distributors and manufacturers to strengthen regional supply partnerships and technical support networks.

Brazil Market Outlook: Brazil serves as the region's largest industrial electronics market through its expanding automotive manufacturing, renewable energy development, and industrial automation initiatives. Manufacturers continue modernizing production facilities while increasing demand for reliable power semiconductor components in motor drives and energy conversion equipment. Growing investment in industrial electrification and grid modernization is creating sustained opportunities for high-temperature diode deployment.

Infrastructure Modernization Drives Power Electronics Adoption

The Middle East & Africa market is expanding steadily as industrial diversification, renewable energy deployment, and infrastructure modernization increase demand for reliable power semiconductor technologies. Gulf countries continue investing in energy infrastructure and industrial manufacturing, while South Africa remains a key engineering and industrial hub. Around 17% of newly commissioned industrial power projects now utilize advanced thermal semiconductor components to improve system reliability. Manufacturers are strengthening regional distribution partnerships and technical support capabilities to address increasing demand for high-performance electronic systems.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region's most strategically significant market through major industrial diversification initiatives, energy infrastructure investments, and expanding advanced manufacturing capabilities. Continued modernization of industrial facilities and renewable energy projects is increasing deployment of high-temperature semiconductor devices. Growing investment in localized technology ecosystems and industrial automation is strengthening long-term demand for advanced power electronics across multiple high-value industries.

Global semiconductor leaders including Infineon Technologies, onsemi, STMicroelectronics, ROHM Semiconductor, and Vishay Intertechnology compete directly on wide-bandgap technology, while integrated device manufacturers challenge fabless suppliers through manufacturing control and faster commercialization. The top five companies collectively hold approximately 56% of market share. Competition is driven by thermal performance, wafer technology, packaging innovation, and supply-chain resilience rather than pricing alone. Advanced silicon carbide platforms improve power efficiency by nearly 20%, localized wafer production shortens procurement lead times by approximately 16%, and automated packaging enhances manufacturing throughput by around 14%. Companies are expanding 200 mm wafer capacity, pursuing strategic technology partnerships, vertically integrating substrate production, and strengthening automotive OEM collaborations. Competitive momentum is shifting toward silicon carbide and gallium nitride leadership supported by advanced packaging capabilities. High fabrication costs, qualification requirements, and wafer supply constraints remain key entry barriers. Market leadership requires superior materials expertise, scalable manufacturing, and application-specific engineering excellence.

Infineon Technologies AG

onsemi

STMicroelectronics N.V.

Vishay Intertechnology, Inc.

ROHM Semiconductor

Nexperia B.V.

Littelfuse, Inc.

Diodes Incorporated

Microchip Technology Inc.

Toshiba Electronic Devices & Storage Corporation

Semikron Danfoss

Mitsubishi Electric Corporation

High temperature diode technology is rapidly advancing through silicon carbide, gallium nitride, and advanced thermal packaging solutions that enable reliable operation in harsh industrial environments. Nearly 48% of newly developed high-power electronic platforms now incorporate wide-bandgap semiconductor devices, while optimized packaging improves heat dissipation by approximately 21%. Intelligent thermal monitoring and automated semiconductor manufacturing are improving production consistency while supporting greater integration across electric vehicles, renewable energy systems, and industrial power electronics.

The most significant technology transition is the shift from conventional silicon diodes to silicon carbide power devices. Compared with traditional silicon technology, silicon carbide diodes reduce switching losses by approximately 25% while increasing thermal operating capability by nearly 30%. Automotive manufacturers, renewable energy equipment suppliers, and industrial automation companies gain the strongest competitive advantage through higher power density, lower cooling requirements, and longer component service life. Advanced wafer processing and integrated power modules are accelerating deployment across demanding high-temperature applications.

Between 2026 and 2028, 200 mm silicon carbide wafer production, AI-assisted semiconductor process control, and next-generation power packaging will reshape industry competitiveness. Wide-bandgap semiconductor adoption is expected to exceed 55% across premium power electronics platforms. Companies investing in vertically integrated wafer production, advanced packaging technologies, and intelligent manufacturing systems will improve operational efficiency, strengthen supply resilience, and secure leadership as thermal performance becomes a defining competitive differentiator.

February 2025 – Infineon Technologies released its first customer products manufactured on 200 mm silicon carbide wafers, strengthening high-volume production readiness for electric vehicles and industrial power systems while improving manufacturing efficiency through larger wafer technology. Source: Infineon Technologies

July 2025 – Infineon Technologies confirmed its 300 mm gallium nitride manufacturing roadmap, with customer samples scheduled during 2025, enabling scalable production and reinforcing leadership in next-generation high-temperature power semiconductors. Source: Infineon Technologies

September 2025 – Infineon Technologies and ROHM Semiconductor signed a strategic collaboration to standardize silicon carbide power packages, improving sourcing flexibility while ROHM's DOT-247 package reduces thermal resistance by approximately 15%. Source: Infineon Technologies

June 2024 – onsemi announced plans to invest up to USD 2 billion in a new silicon carbide semiconductor manufacturing facility in the Czech Republic, strengthening European supply resilience for electric vehicle and industrial power applications. Source: Reuters.

This report provides comprehensive analysis of the High Temperature Diode Market across semiconductor types, applications, end-users, and major geographic regions. It evaluates silicon, silicon carbide, gallium nitride, and specialty diode technologies while assessing demand across power electronics, automotive systems, aerospace, renewable energy, industrial automation, and defense applications. The study examines adoption trends, manufacturing concentration, advanced packaging technologies, thermal performance requirements, and competitive participation across more than 12 leading semiconductor companies.

The report delivers strategic insights supporting investment planning, manufacturing expansion, technology selection, and competitive positioning between 2026 and 2033. It evaluates regional fabrication capabilities, semiconductor supply-chain evolution, wafer technology, and emerging opportunities in wide-bandgap materials. Coverage extends to advanced packaging, intelligent power modules, AI-enabled semiconductor manufacturing, and high-temperature electronic systems, enabling decision-makers to identify high-value growth segments, operational priorities, and long-term competitive strategies across the global power semiconductor ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3,956.3 Million |

|

Market Revenue in 2033 |

USD 7,432.0 Million |

|

CAGR (2026 - 2033) |

8.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Infineon Technologies AG, onsemi, STMicroelectronics N.V., Vishay Intertechnology, Inc., ROHM Semiconductor, Nexperia B.V., Littelfuse, Inc., Diodes Incorporated, Microchip Technology Inc., Toshiba Electronic Devices & Storage Corporation, Semikron Danfoss, Mitsubishi Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |