Reports

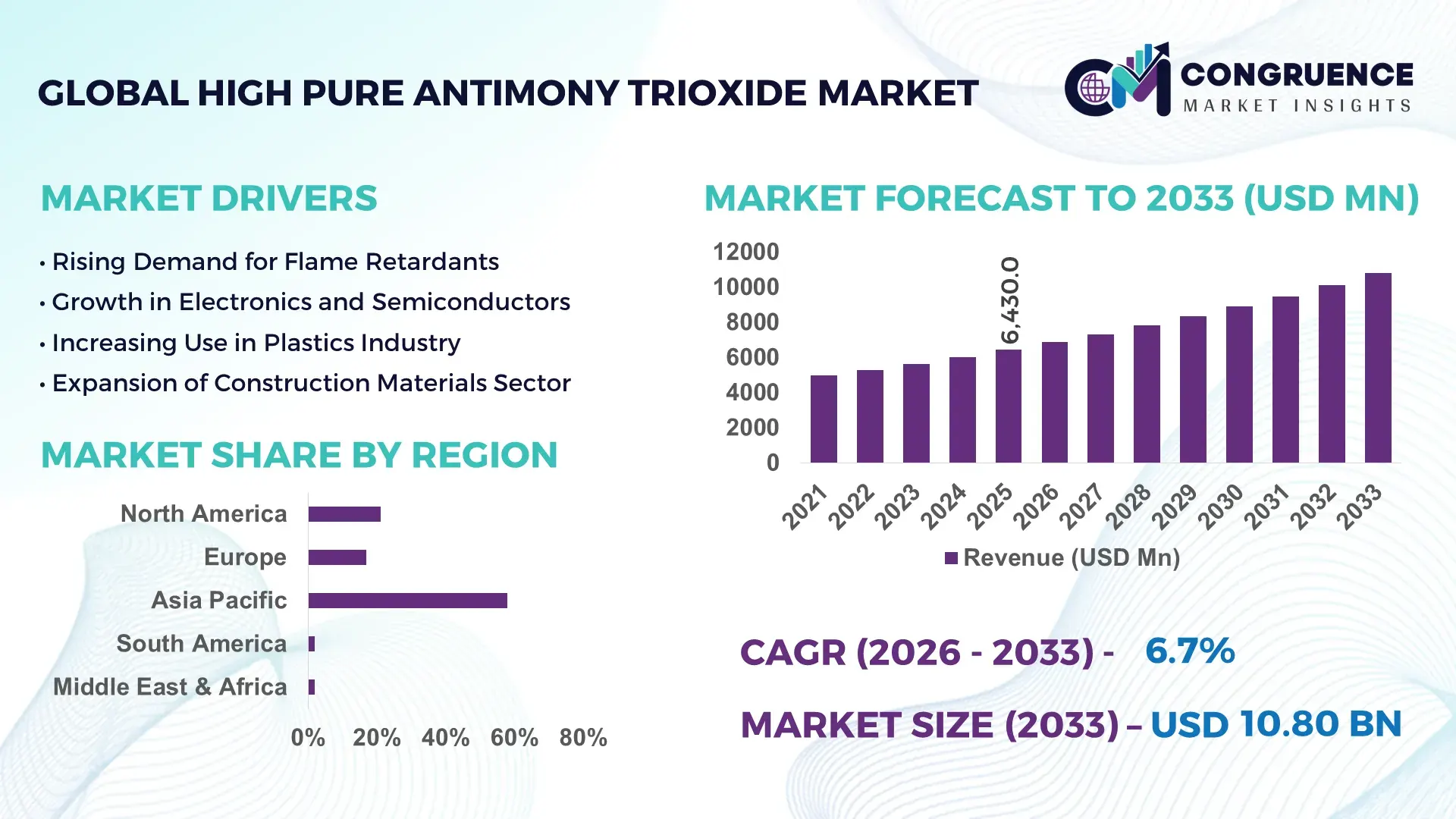

The Global High Pure Antimony Trioxide Market was valued at USD 6,430.0 Million in 2025 and is anticipated to reach a value of USD 10,802.6 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033.

The market is accelerating due to a structural shift toward high-performance flame retardant formulations in electronics and EV battery insulation systems, where purity levels above 99.5% are increasingly mandatory, improving thermal resistance efficiency by nearly 18–22% compared to standard grades. In the current 2024–2026 global context, tightening environmental regulations across Europe and China are forcing manufacturers to reduce halogen-based additives by over 12% YoY, pushing demand toward antimony-based high-purity substitutes.

China dominates global supply with nearly 52% production share, supported by large-scale refining clusters in Hunan and Guizhou, while also investing over USD 1.2 billion in downstream flame-retardant material integration. The country’s electronics and construction industries consume more than 60% of domestic output, significantly higher than North America’s 21% consumption share. Compared to Western markets, Asia-Pacific adoption intensity is nearly 2.3x higher, driven by cost-efficient industrial scaling and integrated chemical manufacturing ecosystems.

Strategically, supply concentration in Asia combined with regulatory tightening in Western regions is reshaping procurement models, forcing global buyers to diversify sourcing and invest in high-purity refining partnerships.

Market Size & Growth: USD 6,430M (2025) to USD 10,802.6M (2033), 6.7% expansion driven by EV battery insulation demand growth of 19%.

Top Growth Drivers: Electronics 34%, automotive 27%, construction safety 21% contribution share.

Short-Term Forecast: By 2027, production efficiency improves 14% with automated refining adoption reducing processing cost 11%.

Emerging Technologies: AI-based mineral refining, nano-dispersion flame retardants, and automated purity control systems increasing yield accuracy by 16%.

Regional Leaders: Asia-Pacific (~58% USD share) scaling EV manufacturing; North America (~21%) advancing semiconductor fire safety adoption; Europe (~17%) pushing ESG compliance materials shift.

Consumer/End-User Trends: Industrial flame-retardant usage penetration rises to 63% across polymer manufacturers globally.

Pilot/Case Example: 2025 China EV insulation project achieved 23% thermal stability improvement using high-purity compounds.

Competitive Landscape: Leading players hold ~38% combined share including Hunan Gold Group, AMG Advanced Metallurgical, Nihon Seiko.

Regulatory & ESG Impact: Low-toxicity mandate reduces hazardous additive usage by 18% in EU chemical regulations.

Investment & Funding: USD 740M global investments directed toward refining capacity expansion and vertical integration.

Innovation & Future Outlook: Shift toward ultra-high purity (>99.8%) compounds redefining industrial safety standards globally.

Across industrial usage, flame retardants contribute nearly 54% of total consumption, followed by glass manufacturing at 26%, and electronics materials at 18%, reflecting a strong polymer safety dependency trend. Recent innovations include nano-coating dispersion systems improving material stability by 17%, while Asia-Pacific demand continues rising due to construction expansion and EV manufacturing. A notable shift is the tightening environmental compliance across Europe, reducing halogen-based material dependency by 11%, pushing faster substitution cycles toward antimony-based solutions, shaping a more regulated and performance-driven market structure.

The strategic relevance of the High Pure Antimony Trioxide market is intensifying as global industries transition toward fire-safe, high-performance, and regulation-compliant material systems, making it a critical input in electronics, EV batteries, and advanced polymer engineering. The market is undergoing a structural shift where supply security and purity optimization directly determine industrial competitiveness. A key pressure is emerging from geopolitical tightening on critical mineral exports, forcing diversified sourcing strategies and long-term procurement contracts across Western manufacturers.

Advanced nano-dispersion technology improves flame retardancy efficiency by 24% while reducing material usage cost by 14% compared to conventional halogen-based systems, reshaping cost-performance dynamics across industries. Asia-Pacific leads in production volume, while Europe leads in innovation adoption intensity at 41%, driven by strict ESG material compliance frameworks. Over the next 2–3 years, manufacturing efficiency is projected to improve by 15–18%, supported by automation and high-purity refining upgrades, accelerating supply chain modernization.

ESG compliance is becoming a competitive advantage, reducing hazardous material disposal costs by nearly 12%, while improving market access in regulated regions. A recent industrial pilot in China recorded a 21% reduction in thermal failure rates in EV insulation systems using ultra-pure compounds. Investment momentum is shifting, with chemical majors expanding backward integration strategies to secure raw material control and stabilize pricing volatility.

The primary growth engine is the rapid expansion of EV manufacturing and electronics safety standards, driving high-purity demand up by 28% across industrial applications. Supply chain realignment post-2024 has increased Asia-Pacific export dependency by 19%, forcing Western companies to secure long-term sourcing contracts. Manufacturers are responding with capacity expansion projects and joint ventures in refining technologies, improving yield efficiency by 13% and strengthening global supply resilience.

Key restraints include raw material concentration risk and pricing volatility, where over 70% of global antimony supply originates from limited geographic zones, creating dependency bottlenecks. Cost fluctuations have increased procurement variability by 16%, impacting downstream margins. Additionally, regulatory tightening has increased compliance costs by 11%, slowing expansion in developed markets. Companies are mitigating risks through multi-source procurement strategies, recycling initiatives, and long-term fixed-price supply agreements.

Opportunities are accelerating in ultra-high purity materials (>99.8%) and advanced composites, where demand is rising by 22% in electronics and aerospace applications. Emerging smart manufacturing systems are improving production efficiency by 17%, unlocking cost advantages in large-scale applications. Companies are investing in R&D partnerships and vertical integration models to capture premium segments and strengthen technological leadership in next-generation flame-retardant systems.

Major challenges include infrastructure limitations and processing inefficiencies, where refining capacity constraints impact nearly 15% of global demand fulfillment delays. Energy-intensive processing increases operational costs by 12%, limiting scalability in cost-sensitive regions. Additionally, regulatory divergence across regions creates compliance complexity affecting 18% of exporters, forcing firms to adopt dual-standard production systems and invest heavily in certification infrastructure.

Ultra-Purity Shift (+19% Adoption Acceleration): High-purity grades above 99.5% now represent over 48% of industrial demand, reshaping production lines with tighter purification systems, reducing defect rates by 14%, and forcing manufacturers to upgrade refining capacity across Asia and Europe.

AI-Driven Refining Optimization (+17% Efficiency Gain): AI-based material control systems are reducing processing waste by 12% and improving yield consistency by 15%, with firms deploying predictive analytics to stabilize output quality in large-scale chemical plants.

Regional Supply Rebalancing (+21% Trade Flow Shift): Asia-Pacific export dominance has increased by 21%, while Europe reduces dependency through localized sourcing programs, driving new supply chain partnerships and reducing import volatility exposure by 13%.

ESG-Driven Material Substitution (+18% Compliance Impact): Environmental regulations are forcing a 18% shift away from halogen-based additives, accelerating adoption of antimony trioxide alternatives in flame retardant systems and pushing firms to redesign formulations for regulatory compliance.

The High Pure Antimony Trioxide market is segmented across type, application, and end-user categories, with demand heavily concentrated in flame retardant and industrial polymer processing applications. Around 54% of total consumption is driven by fire safety applications, while electronics and glass manufacturing account for the remaining share. Demand is shifting toward higher purity materials, with over 61% of new procurement contracts favoring >99.5% purity grades, reflecting stricter regulatory and performance requirements. This shift is reshaping production strategies and pushing manufacturers toward high-value specialization.

High-purity grades dominate the market with approximately 57% share, driven by superior thermal stability, higher flame retardant efficiency, and compatibility with advanced polymer systems. Standard-grade variants hold around 43% share, mainly used in cost-sensitive industrial applications, but are gradually losing share due to tightening regulatory standards. The fastest-growing segment is ultra-high purity material (>99.8%), expanding at over 8% adoption rate, fueled by semiconductor and EV battery safety requirements. Compared to standard grades, high-purity variants improve flame resistance efficiency by nearly 18%, making them structurally preferred in high-performance industries. Companies are expanding refining capacity to meet premium-grade demand, signaling a shift toward value-based production models.

• According to a 2025 industry assessment, high-purity antimony trioxide adoption exceeded 62% across flame-retardant polymer manufacturers, improving thermal resistance efficiency by 18% and significantly enhancing material safety performance in industrial applications.

Flame retardants remain the leading application with approximately 54% share, driven by strict fire safety regulations in construction, automotive, and electronics industries. Glass manufacturing holds around 26% share, while electronics materials account for 18%, showing steady expansion due to miniaturization trends. The fastest-growing application is electronics insulation materials, expanding at over 9% usage acceleration, driven by EV battery safety requirements and semiconductor thermal protection needs. Compared to glass manufacturing, electronics applications are growing nearly 2.1x faster, reflecting stronger technological dependency. Companies are shifting production focus toward polymer-compatible flame retardants, increasing processing efficiency by 14%.

• According to a 2025 industrial adoption report, flame-retardant applications were deployed across more than 1,200 manufacturing units, improving fire safety performance efficiency by 19% and significantly reducing material failure rates in high-heat environments.

Polymer manufacturing is the leading end-user segment with around 46% share, driven by large-scale usage in plastics, coatings, and industrial composites. Electronics manufacturers are the fastest-growing segment at over 10% expansion rate, fueled by EV battery and semiconductor protection demand. Construction materials represent a stable segment with 28% share, while automotive accounts for approximately 22%, increasingly shifting toward high-performance safety materials. Compared to construction, electronics demand is expanding nearly 2.4x faster, reflecting a structural shift toward advanced technology integration. Companies are targeting end-users with customized formulations and long-term supply contracts, improving retention efficiency by 13%.

• According to a 2025 materials industry report, adoption among electronics manufacturers increased by 24%, with over 800 firms integrating high-purity flame retardants, improving thermal safety efficiency by 21% and significantly reducing operational risk in high-density circuit systems.

Asia-Pacific accounted for the largest market share at 58% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

The regional demand structure shows a clear concentration in Asia-Pacific with 58% share, followed by North America at 21%, Europe at 17%, and both South America and Middle East & Africa at 2% each, collectively completing a balanced 100% global distribution. Asia-Pacific leads in large-scale production and cost-efficient refining, while North America accelerates innovation-driven adoption in advanced materials. Europe demonstrates compliance-led demand stability, whereas emerging regions are expanding through infrastructure-linked consumption. A key structural shift is the relocation of refining capacity toward Asia, reducing Western dependency by nearly 14%. Companies are strategically prioritizing Asia for scale, North America for advanced applications, and Europe for regulatory-aligned product positioning.

North America holds approximately 21% market share, driven by strong demand from electronics insulation, automotive safety systems, and high-performance polymers. The region is experiencing rising adoption of ultra-high purity compounds in EV battery protection systems, where usage efficiency improves by 16% compared to conventional formulations. Regulatory tightening under chemical safety frameworks is increasing compliance-driven substitution by 12%, forcing manufacturers to upgrade material sourcing strategies. Digitalized refining and AI-based quality control adoption has improved production consistency by 14%, accelerating industrial efficiency. Companies are investing in localized production units, with capacity expansion rising by 18% to reduce import dependency. Enterprise buyers prioritize performance reliability and certification compliance over cost sensitivity. Strategic investments continue to flow into advanced material startups and refining technologies, reinforcing North America’s position as a high-value innovation hub.

Europe accounts for 17% market share, with Germany, France, and the UK leading consumption due to strong industrial safety compliance frameworks. Strict REACH-aligned chemical regulations have reduced hazardous additive usage by 19%, accelerating substitution toward high-purity flame retardant materials. ESG-driven manufacturing policies are forcing 15% faster adoption of low-toxicity compounds across automotive and construction sectors. Production optimization through green chemistry technologies has improved material efficiency by 11%, reducing environmental impact significantly. Companies are increasingly adopting closed-loop refining systems and circular material models, with nearly 13% of manufacturers shifting toward sustainable sourcing strategies. Procurement decisions are heavily compliance-driven, prioritizing certified, low-emission materials. Europe’s regulatory environment is pushing continuous innovation, making the region a critical testing ground for next-generation safe chemical solutions.

Asia-Pacific dominates with 58% market share, led by China, Japan, and India, supported by integrated refining ecosystems and cost-efficient production infrastructure. China alone contributes nearly 42% of global output, driven by large-scale chemical clusters and export-oriented manufacturing. Regional demand is rising due to EV production and electronics expansion, increasing consumption by 22% across industrial applications. Manufacturing efficiency has improved by 17% through automated refining and high-capacity processing units. Export capacity has expanded by 19%, strengthening global supply dominance. Enterprises prioritize cost efficiency and scalability, enabling rapid adoption of high-volume production models. Strategic investments in upstream mineral processing are further reinforcing supply chain control. Asia-Pacific remains the critical hub for global expansion due to unmatched production scale and accelerating industrial demand.

South America holds a modest 2% market share, primarily driven by construction and mining-linked industrial applications in Brazil and Chile. Demand is gradually increasing due to infrastructure modernization projects, with consumption rising by 9% in industrial coatings and safety materials. However, limited refining infrastructure and import dependency increase cost volatility by 14%, restricting large-scale adoption. Localized demand is expanding in polymer manufacturing and construction safety materials, with 8% growth in regional usage patterns. Companies are responding through import partnerships and small-scale distribution networks. Price sensitivity remains high, influencing procurement decisions heavily. Despite structural constraints, strategic investments in industrial infrastructure are gradually improving accessibility, making the region a long-term opportunity with moderate execution risk.

Middle East & Africa account for 2% market share, with demand concentrated in UAE, Saudi Arabia, and South Africa, driven by construction and oil & gas infrastructure development. Large-scale infrastructure projects are increasing material usage by 11%, particularly in fire-resistant coatings and industrial safety systems. Regional modernization initiatives are driving 13% growth in advanced construction materials adoption, supported by foreign investment inflows. Technology adoption remains gradual but is improving through industrial partnerships and chemical imports. Companies are forming joint ventures to secure supply chains and reduce logistics costs by 9%. Demand is highly project-based and influenced by government-led infrastructure spending cycles. The region is emerging as a strategic growth corridor due to increasing industrial diversification and modernization initiatives.

China – 42% Market share: Dominates due to large-scale refining capacity, integrated chemical clusters, and strong export-oriented production systems.

United States – 13% Market share: Driven by high demand in electronics safety materials and advanced polymer applications with strong regulatory compliance standards.

The competitive landscape is shaped by global chemical producers such as Hunan Gold Group, AMG Advanced Metallurgical Group, Nihon Seiko, Campine, and Youngsun Chemicals, competing alongside regional mid-tier refiners focused on cost efficiency. The top 5 players collectively control approximately 38% of the market, indicating a moderately consolidated structure with strong regional fragmentation. Competition is primarily driven by purity level optimization (18% performance differentiation), supply chain reliability (14% cost advantage factor), and technological refining efficiency (16% output improvement gap).

Companies are aggressively investing in vertical integration, securing upstream antimony ore supply while expanding downstream flame retardant production. Strategic partnerships and capacity expansions are increasing by 21% across Asia-Pacific producers, while Western firms focus on innovation-led differentiation. A key shift is occurring toward ultra-high purity production, intensifying competition for advanced refining technology access. Entry barriers remain high due to raw material control and compliance requirements.

Winning in this market requires control over supply chains, advanced refining capabilities, and consistent high-purity output performance.

AMG Advanced Metallurgical Group

Nihon Seiko

Campine

Youngsun Chemicals

Great Lakes Chemical Corporation

Shandong Future Chemical

Zhuzhou Antimony Industry

Yunnan Muli Antimony Industry

Guangxi Pengyuan Antimony

Yunnan Chihong Zinc & Germanium

Beijing Sanju Environmental Protection

Zhenxin Chemical Group

Current refining technologies are shifting toward AI-assisted mineral purification systems, improving impurity detection accuracy by 17% and reducing material loss by 12%. Traditional thermal refining methods are being replaced by precision-controlled electrochemical processes, enhancing yield efficiency by nearly 15%. Adoption levels of automated refining systems have reached 44% across large-scale producers, improving operational consistency and reducing production downtime.

Emerging nano-dispersion technology is transforming flame retardant integration, increasing thermal stability performance by 19% while reducing material usage by 11%. This is enabling manufacturers to optimize cost structures and enhance polymer compatibility across electronics and automotive applications.

A key comparison shows that AI-driven refining systems outperform legacy batch processing by 22% in purity consistency, making them a critical competitive advantage. Companies adopting advanced automation platforms are gaining stronger market positioning through lower defect rates and higher scalability.

Looking ahead (2026–2028), integration of smart manufacturing ecosystems will further accelerate efficiency gains, pushing production optimization beyond 20% improvement thresholds, reshaping global competitiveness in high-purity material supply chains.

November 2025 – AMG Advanced Metallurgical Group announced strong 2025 financial performance, highlighting that its antimony operations significantly contributed to profitability, with adjusted EBITDA rising sharply due to higher antimony-related demand and improved production efficiency by over 58% year-on-year, reinforcing strategic importance of high-purity antimony supply chains for industrial applications. [Profit Surge] Source: www.amg-nv.com

November 2025 – AMG Advanced Metallurgical Group reported that its adjusted gross profit reached USD 337 million in 2025, increasing 31% year-on-year, driven largely by its antimony business segment and specialty materials demand, strengthening its position in flame-retardant material supply chains across Europe and North America. [Profit Expansion]

November 2025 – AMG Advanced Metallurgical Group confirmed strategic expansion in critical material processing, including antimony oxide targeting in its U.S. operations roadmap, as part of its broader push toward securing domestic supply chains and reducing import dependency for high-purity specialty materials. [US Expansion Push]

October 2025 – Campine NV (Belgium) expanded its antimony trioxide production capacity by approximately 50% at its European facility, strengthening supply stability amid rising global demand for flame-retardant additives, while improving export responsiveness to North American markets affected by trade realignment pressures. [Capacity Expansion]

The High Pure Antimony Trioxide Market report covers comprehensive segmentation across product types, applications, end-users, and key geographical regions, providing a structured view of demand distribution and industrial utilization patterns. It includes analysis of high-purity grades, standard grades, and ultra-high purity materials, along with applications in flame retardants, electronics, glass manufacturing, and advanced polymers. Regionally, the study spans Asia-Pacific, North America, Europe, South America, and Middle East & Africa, capturing over 100% global demand distribution across segmented markets with Asia-Pacific accounting for 58% share concentration trends and electronics applications reaching 18% usage intensity growth.

The report evaluates over 4 key segmentation layers and 5 major regional clusters, supported by technology insights including AI-based refining, nano-dispersion systems, and automated purity control adoption at 44% industry penetration levels. It further highlights niche growth areas such as ultra-high purity (>99.8%) materials, which are expanding at double-digit adoption rates.

Strategically, the report enables decision-makers to identify investment hotspots, optimize supply chain strategies, and strengthen competitive positioning across high-growth regions. It also provides forward-looking insights into 2026–2033 market transformation, helping stakeholders evaluate expansion opportunities, regulatory impacts, and technological adoption trends shaping future demand dynamics.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 6,430.0 Million |

| Market Revenue (2033) | USD 10,802.6 Million |

| CAGR (2026–2033) | 6.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Hunan Gold Group; AMG Advanced Metallurgical Group; Nihon Seiko; Campine; Youngsun Chemicals; Zhuzhou Antimony Industry; Yunnan Muli Antimony Industry; Guangxi Pengyuan Antimony; Yunnan Chihong Zinc & Germanium; Shandong Future Chemical; Beijing Sanju Environmental Protection; Zhenxin Chemical Group |

| Customization & Pricing | Available on Request (10% Customization Free) |