Reports

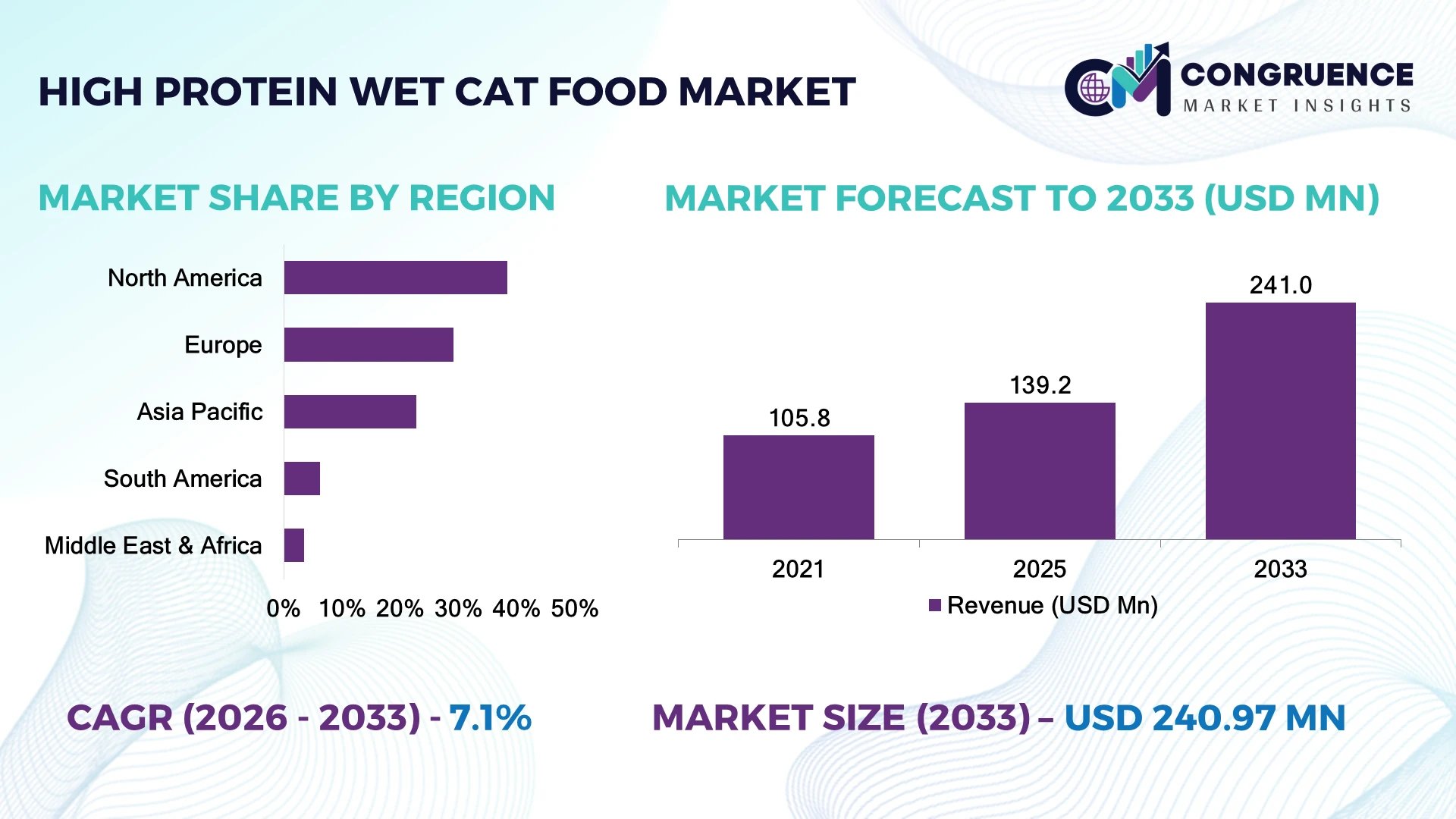

The Global High Protein Wet Cat Food Market was valued at USD 139.2 Million in 2025 and is anticipated to reach a value of USD 241.0 Million by 2033 expanding at a CAGR of 7.1% between 2026 and 2033. Rising premium pet nutrition preferences, increasing demand for meat-rich functional formulations, and expanding humanization of companion animals are accelerating product innovation and premium retail penetration worldwide.

The United States leads the global High Protein Wet Cat Food Market with approximately 34% market share, supported by advanced pet food manufacturing, more than 46 million cat-owning households, and strong premium product adoption across specialty retail and e-commerce channels. Japan follows with one of the world's highest wet cat food consumption rates, while Germany continues expanding premium protein formulations through strict quality standards and sustainable ingredient sourcing, strengthening international competitiveness.

Manufacturers prioritizing premium protein sourcing, resilient ingredient supply chains, and science-backed nutritional innovation are positioned to strengthen long-term competitive advantage across mature and emerging pet care markets.

Market Size & Growth: USD 139.2 Million in 2025, projected to reach USD 241.0 Million by 2033 at 7.1% CAGR, driven by premium protein nutrition and clean-label product innovation.

Top Growth Drivers: Premium pet food adoption (+31%), high-protein diet preference (+27%), e-commerce penetration (+24%) continue reshaping purchasing behavior.

Short-Term Forecast: By 2028, automated wet food production is expected to improve manufacturing efficiency by approximately 18% while reducing formulation waste by nearly 12%.

Emerging Technologies: AI-driven nutrition formulation, automated ingredient traceability, and precision protein processing enhance product consistency and manufacturing performance.

Regional Leaders: North America (~USD 82 Million), Europe (~USD 68 Million), and Asia-Pacific (~USD 54 Million) benefit from premiumization, retail expansion, and digital pet-care ecosystems.

Consumer/End-User Trends: More than 41% of premium cat owners actively prefer high-protein wet food formulated with natural animal-based ingredients.

Pilot/Case Example: In 2024, smart production optimization projects improved batch consistency by approximately 16% while lowering production downtime by 11%.

Competitive Landscape: Mars Incorporated holds roughly 19% market share alongside Nestlé Purina PetCare, Hill's Pet Nutrition, Wellness Pet Company, and Blue Buffalo.

Regulatory & ESG Impact: Sustainable packaging adoption increased by approximately 22% as manufacturers aligned with stricter environmental compliance and responsible sourcing initiatives.

Investment & Funding: More than USD 580 Million has been invested globally in production expansion, premium ingredient processing, and supply-chain modernization.

Innovation & Future Outlook: Functional nutrition, alternative protein blends, and personalized pet nutrition platforms are redefining competitive differentiation across global premium pet food markets.

High Protein Wet Cat Food Market demand continues expanding across premium retail, veterinary nutrition, and digital pet-care platforms as manufacturers introduce functional ingredients, digestibility enhancements, and minimally processed meat formulations. More than 38% of newly launched premium wet cat food products now emphasize high-protein positioning. Ongoing animal protein sourcing optimization and stricter ingredient traceability standards are strengthening product consistency while supporting broader international market expansion and strategic portfolio development.

The High Protein Wet Cat Food Market has become strategically important as premium pet nutrition transforms from a niche category into a mainstream purchasing priority. Companies are restructuring protein sourcing networks, strengthening regional manufacturing capabilities, and expanding digital retail partnerships to improve product availability and supply resilience. Increasing ingredient transparency requirements are also encouraging investment in traceability and quality assurance systems.

Modern AI-assisted formulation platforms reduce product development cycles by nearly 25% compared with conventional formulation processes while improving nutritional consistency across production batches. North America remains the largest innovation hub through premium brand concentration and advanced manufacturing, whereas Asia-Pacific records faster adoption through expanding urban pet ownership, modern retail infrastructure, and growing online pet food purchases. Over the next two to three years, automated quality inspection and digital inventory management are expected to become standard across leading manufacturing facilities.

Manufacturers are expanding premium product portfolios through partnerships with ingredient suppliers, veterinary nutrition specialists, and specialty retailers. For example, advanced manufacturing facilities integrating automated filling and quality monitoring have significantly reduced operational waste while improving production efficiency. Businesses that combine premium nutrition, resilient sourcing, and continuous product innovation will secure stronger competitive positioning and long-term operational advantages in the evolving global pet nutrition industry.

Premium pet nutrition has become the primary structural catalyst for the High Protein Wet Cat Food Market as consumers increasingly prioritize biologically appropriate diets and ingredient transparency. More than 43% of premium cat owners actively purchase protein-rich wet food, while over 36% of new product launches feature functional ingredients such as probiotics, omega fatty acids, and taurine. The United States has accelerated adoption through veterinary nutrition partnerships, while stricter ingredient traceability standards across the European Union have encouraged higher manufacturing quality. This shift has improved consumer confidence and strengthened premium brand positioning. In response, manufacturers are expanding domestic production, investing in advanced meat-processing technologies, and collaborating with animal nutrition specialists to accelerate premium product development. Companies integrating nutritional science with transparent sourcing are securing stronger retailer relationships and higher customer retention.

Volatility in premium animal protein supply continues to constrain production planning and operational efficiency. Approximately 58% of manufacturing costs remain linked to meat-based raw materials, while fluctuations in poultry and seafood availability have increased ingredient procurement costs by nearly 18% during recent supply disruptions. Export restrictions and livestock disease outbreaks in several producing countries have further complicated procurement schedules for premium manufacturers. These conditions reduce production flexibility, compress operating margins, and create pricing pressure across competitive retail channels. To minimize exposure, companies are diversifying supplier networks, increasing localized sourcing in countries such as Canada and Poland, and adopting long-term procurement contracts. Strategic ingredient diversification has become a critical operational priority for maintaining stable product availability and protecting premium brand positioning.

Digital nutrition technologies are creating new commercial opportunities by enabling personalized feeding recommendations and science-based product differentiation. More than 32% of premium pet owners regularly use mobile pet-health platforms, while AI-supported nutrition analytics can reduce formulation development time by approximately 24%. Japan and South Korea are expanding digital pet-care ecosystems that integrate veterinary guidance with customized nutrition planning, creating stronger customer engagement and repeat purchases. Manufacturers are investing in research partnerships, precision formulation platforms, and advanced ingredient analytics to develop targeted high-protein recipes for different life stages and health conditions. A less obvious advantage is the ability to optimize inventory through demand forecasting, reducing production waste while improving premium product availability across omnichannel retail networks.

Maintaining consistent product quality across expanding production networks remains a significant long-term execution challenge. High-protein wet formulations require strict moisture control, sterilization precision, and cold-chain integrity, while nearly 21% of manufacturers report production bottlenecks during premium product scale-up. Labor shortages in food processing facilities and increasingly rigorous food safety audits have extended production validation timelines in countries including Germany and the United States. These operational pressures affect manufacturing consistency, retailer confidence, and international expansion capability. Companies are responding through automated inspection systems, digital quality monitoring, workforce training, and investments in smart manufacturing infrastructure. Achieving standardized production across multiple facilities will remain a decisive competitive factor as premium pet nutrition continues evolving toward higher quality expectations.

Premium Protein Formula Expansion: Premium meat-first formulations now account for approximately 46% of new wet cat food launches, while single-animal protein recipes have grown by nearly 29% over the past two years. Retailers in the United States and the United Kingdom are expanding premium shelf allocation as consumers increasingly select minimally processed nutrition. Manufacturers are scaling fresh-meat sourcing partnerships and modernizing production workflows to improve formulation consistency and reduce ingredient variability amid tighter quality requirements.

Smart Manufacturing Gains Momentum: Automated filling, vision-based quality inspection, and digital batch monitoring have improved production efficiency by around 18% while reducing packaging defects by nearly 15%. Labor shortages across food manufacturing facilities have accelerated investment in robotics and predictive maintenance. Leading producers are restructuring manufacturing operations, integrating real-time process analytics, and deploying automated traceability systems to increase throughput, strengthen food safety compliance, and minimize production downtime.

Functional Nutrition Differentiation: More than 37% of newly introduced products now combine high-protein content with digestive health, immune support, or skin and coat nutrition. Veterinary-endorsed formulations and life-stage-specific recipes are becoming standard across premium portfolios. Companies are expanding research collaborations with animal nutrition specialists, accelerating functional ingredient development, and introducing targeted product ranges that strengthen consumer loyalty while supporting premium pricing strategies.

Sustainable Packaging Integration: Recyclable packaging adoption has increased by approximately 26%, while lightweight packaging formats have reduced transportation weight by nearly 14%. Packaging regulations and supply-chain optimization initiatives are encouraging manufacturers to redesign packaging without compromising shelf stability. Companies are investing in recyclable pouches, localized packaging operations, and digital inventory planning, with the added benefit of lowering logistics costs while improving retail replenishment efficiency.

Chicken-based High Protein Wet Cat Food remains the leading segment, representing approximately 44% of total market demand due to its high digestibility, broad feline acceptance, stable raw material availability, and cost-efficient manufacturing. Its compatibility with functional ingredients and veterinary nutrition formulations further strengthens its commercial position. Fish-based products rank second, benefiting from strong demand for omega-rich nutrition, while beef formulations continue serving premium specialty categories. Mixed protein products are expanding steadily by offering balanced nutritional profiles and greater formulation flexibility for premium brands. Mixed protein formulations are the fastest-growing segment as manufacturers increasingly combine poultry, fish, and organ proteins to improve amino acid balance and product differentiation. Nearly 34% of newly introduced premium recipes now feature blended protein sources. Companies are expanding premium product portfolios, investing in advanced protein processing technologies, and introducing grain-free and limited-ingredient formulations to capture evolving consumer preferences. Product innovation is increasingly shifting toward functional nutrition while maintaining ingredient transparency and consistent product quality.

Daily complete nutrition represents the dominant application, accounting for approximately 57% of total product usage as cat owners increasingly replace dry food with nutritionally balanced wet diets. Complete nutrition products deliver consistent protein intake, hydration support, and essential micronutrients, making them the preferred option for everyday feeding. Weight management and digestive health applications continue expanding as veterinary recommendations encourage specialized nutritional support for aging and indoor cats. Therapeutic and functional nutrition is emerging as the fastest-growing application, supported by increasing diagnosis of digestive sensitivity, urinary tract concerns, and food allergies. Around 31% of premium product launches now target specific health conditions through enhanced protein formulations and functional ingredients. Manufacturers are expanding veterinary partnerships, improving formulation precision, and strengthening specialized distribution channels to address growing demand for condition-specific nutrition while maintaining premium product differentiation.

Household pet owners remain the largest end-user segment, contributing approximately 81% of total market consumption as premium pet ownership continues expanding across developed economies. Rising awareness of species-appropriate nutrition, ingredient transparency, and preventive pet healthcare has increased demand for premium high-protein wet food. Independent pet specialty retailers and e-commerce platforms continue strengthening consumer access through subscription models and personalized product recommendations. Veterinary clinics and animal healthcare providers represent the fastest-growing end-user segment as prescription nutrition and preventive dietary management gain wider acceptance. Nearly 28% of premium therapeutic nutrition purchases now originate through veterinary recommendations. Animal shelters and professional breeders continue adopting premium wet nutrition to improve feline health outcomes, although at comparatively smaller volumes. Companies are developing customized veterinary product lines, strengthening professional partnerships, and expanding educational initiatives that support science-based nutrition and long-term customer retention.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.3% between 2026 and 2033.

North America maintains its leadership through high premium pet food penetration, advanced manufacturing infrastructure, and widespread adoption of science-based feline nutrition. The region contributes approximately 38.4% of global demand, supported by strong retail distribution, established veterinary nutrition networks, and expanding e-commerce channels. More than 62% of premium wet cat food launches in the region emphasize high-protein formulations and functional health benefits. Manufacturers continue modernizing production facilities with automated filling, digital quality monitoring, and ingredient traceability systems that improve production consistency and operational efficiency. Strategic investments in localized meat sourcing and packaging optimization are reducing procurement risks while strengthening supply resilience. Enterprise partnerships between nutrition specialists and pet food manufacturers continue accelerating premium product commercialization and expanding specialty retail presence.

United States Market Outlook: The United States represents the largest national market owing to its mature pet care ecosystem, advanced manufacturing capabilities, and high premium food adoption. More than 46 million households own cats, while premium nutrition products account for nearly 48% of wet cat food purchases. Domestic manufacturers continue investing in automated processing facilities, functional nutrition research, and omnichannel retail expansion. Strong veterinary collaboration and advanced cold-chain logistics enable rapid commercialization of innovative protein-rich formulations while maintaining strict product quality standards.

Europe remains a strategically important market driven by premium pet nutrition, strict ingredient regulations, and sustainable manufacturing practices. The region accounts for approximately 29.1% of global consumption, supported by advanced food safety standards and growing demand for clean-label formulations. Nearly 44% of premium wet cat food packaging now utilizes recyclable or reduced-plastic formats as manufacturers align with environmental objectives. Investments in traceability technologies and regional protein sourcing continue improving supply-chain transparency and manufacturing reliability. Companies are strengthening partnerships with certified ingredient suppliers while expanding production capacity for premium formulations designed to meet evolving consumer expectations and regulatory requirements.

Germany Market Outlook: Germany leads the European market through its strong pet food manufacturing base, sophisticated retail infrastructure, and emphasis on nutritional quality. Premium formulations represent more than 45% of new product introductions, while manufacturers continue expanding automated production lines and sustainable packaging operations. Robust regulatory compliance and advanced ingredient testing capabilities enable companies to strengthen export competitiveness and accelerate premium product innovation across international markets.

Asia-Pacific is experiencing the strongest market expansion as rising disposable income, urban pet ownership, and digital commerce reshape purchasing behavior. The region represents approximately 22.8% of global demand, with premium wet food adoption increasing rapidly across metropolitan markets. Online pet food sales have expanded by nearly 34% over recent years, encouraging manufacturers to strengthen direct-to-consumer distribution and localized production. Companies are investing in regional manufacturing facilities, advanced packaging technologies, and customized nutritional formulations tailored to local feeding preferences. Expansion of veterinary care networks and premium retail channels continues supporting sustained market development and operational scale.

China Market Outlook: China has become the region's most influential market through rapid premiumization, expanding domestic manufacturing, and strong digital retail infrastructure. Premium pet nutrition purchases continue increasing across major cities, while online platforms account for more than 55% of premium pet food sales. Domestic producers are investing in intelligent manufacturing systems, localized ingredient sourcing, and product innovation to strengthen competitiveness against international premium brands.

South America continues developing as premium pet ownership expands alongside improvements in organized retail and veterinary services. The region contributes approximately 6.2% of global market demand, with premium wet cat food adoption increasing steadily in urban centers. Modern retail formats now account for nearly 52% of premium pet food distribution, improving product accessibility and consumer awareness. Manufacturers are strengthening regional production capabilities, expanding local sourcing strategies, and introducing value-premium product portfolios suited to evolving purchasing behavior. Infrastructure modernization remains gradual, but strategic investments in logistics and packaging operations are improving product availability across key metropolitan markets.

Brazil Market Outlook: Brazil dominates the regional market due to its large companion animal population, established pet food manufacturing industry, and expanding premium consumer segment. Automated production facilities continue increasing manufacturing efficiency, while domestic brands invest in functional nutrition development and premium protein formulations. Strong retail expansion and improving veterinary awareness are supporting broader adoption of science-based feline nutrition throughout the country's growing pet care industry.

The Middle East & Africa market is gradually strengthening through premium retail expansion, increasing pet ownership, and modernization of food distribution networks. The region accounts for approximately 3.5% of global demand, supported by growing availability of imported premium brands and specialized pet retail outlets. Premium product assortment has expanded by nearly 24% across organized retail channels, improving consumer access to high-protein nutrition. Companies are investing in regional distribution partnerships, localized warehousing, and digital retail platforms to improve inventory availability and operational responsiveness. Continued modernization of supply-chain infrastructure is strengthening long-term market competitiveness despite relatively smaller production capacity.

United Arab Emirates Market Outlook: The United Arab Emirates serves as the region's leading premium pet food hub through advanced retail infrastructure, high consumer purchasing power, and efficient import logistics. Premium nutrition products continue gaining shelf space across specialty retailers, while e-commerce contributes significantly to category expansion. Distributors are investing in temperature-controlled warehousing, digital inventory management, and strategic partnerships with international manufacturers to improve product availability and strengthen premium market positioning.

The competitive landscape is led by Nestlé Purina PetCare, Mars Petcare, Hill's Pet Nutrition, Wellness Pet Company, and Blue Buffalo, competing directly against premium regional manufacturers and private-label specialists. The top five players collectively control approximately 61% of the global market, while regional brands compete through localized protein sourcing and value-oriented premium positioning. Competition centers on formulation quality, ingredient traceability, product innovation, and supply-chain efficiency rather than price alone. Around 44% of newly introduced premium wet cat food products emphasize high-protein recipes, while nearly 32% incorporate functional health ingredients and over 28% feature sustainable packaging formats. Leading companies continue expanding manufacturing capacity, strengthening veterinary partnerships, investing in advanced processing technologies, and integrating premium protein supply chains through long-term sourcing agreements. Consolidation is gradually shifting competitive advantage toward companies with stronger R&D capabilities and resilient procurement networks. High regulatory standards, premium ingredient access, and established retail distribution remain major entry barriers. Winning requires nutritional innovation, manufacturing excellence, trusted branding, and dependable global supply execution.

Mars Petcare

Hill's Pet Nutrition

Wellness Pet Company

Blue Buffalo

Diamond Pet Foods

Champion Petfoods

Farmina Pet Foods

Nulo Pet Food

Ziwi Peak

Tiki Pets

Weruva International

The Honest Kitchen

Artificial intelligence, precision formulation software, and digital ingredient traceability are transforming premium wet cat food manufacturing. AI-assisted nutritional modeling reduces formulation development time by approximately 24%, while digital quality monitoring improves batch consistency by nearly 18%. More than 42% of premium manufacturers now utilize automated production analytics to optimize protein utilization, reduce ingredient losses, and accelerate product commercialization. Companies adopting integrated digital manufacturing achieve stronger quality assurance and faster product adaptation to changing consumer preferences.

Advanced retort sterilization, automated filling systems, and machine-vision inspection are replacing conventional manual quality control. Modern automated production lines improve packaging efficiency by around 21% and reduce defect rates by approximately 16% compared with traditional processing methods. Premium global manufacturers benefit most through higher production consistency, improved food safety compliance, and reduced operational downtime. Integrated manufacturing platforms also strengthen inventory visibility and supplier coordination across multiple production facilities.

Between 2026 and 2028, predictive maintenance, intelligent production scheduling, and digital twin technologies are expected to become mainstream across premium pet food manufacturing. Adoption is projected to exceed 55% among large-scale producers seeking greater operational flexibility. Early technology adopters will strengthen competitive positioning through lower production costs, faster product launches, enhanced ingredient transparency, and more resilient premium protein supply chains.

February 2025 Nestlé Purina PetCare expanded its patented pyramid-shaped premium wet cat food range across Europe and the United States, adding new jelly variants across 15 European markets. The launch strengthened premium product differentiation and manufacturing scale. Source: www.nestle.com

August 2025 Wellness Pet Company introduced more than 20 new wet cat food products at SUPERZOO, expanding its portfolio to 93 varieties with new protein sources and packaging formats. The launch reinforced premium portfolio diversification and retail competitiveness. Source: www.prnewswire.com

March 2026 Nestlé Purina India launched Felix Gravy Lover and Pro Plan Cat, expanding its premium cat portfolio with four wet food variants designed for hydration and high-quality protein nutrition. The expansion strengthened its presence in India's growing premium cat food segment. Source: www.nestle.in

June 2026 Nestlé Purina Europe relaunched and expanded the Gourmet Perle range across nearly 30 European markets, introducing Ocean Flakes recipes featuring MSC-certified fish. The initiative strengthened premium positioning, responsible sourcing, and category expansion across multiple international retail markets.

This report provides comprehensive analysis across the High Protein Wet Cat Food value chain, covering product types, applications, end-users, competitive positioning, technology trends, and regional market performance. The assessment evaluates demand patterns across household consumers, veterinary nutrition, and specialized premium pet care channels while examining evolving manufacturing practices, ingredient sourcing strategies, and sustainable packaging adoption. More than 60% of market activity is concentrated within premium protein formulations, reflecting continued product differentiation and nutritional specialization.

The report delivers strategic coverage across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting operational developments, competitive intensity, deployment trends, and enterprise expansion strategies between 2026 and 2033. It also evaluates automation, digital manufacturing, ingredient traceability, precision nutrition technologies, and premium product innovation. The analysis supports investment prioritization, market entry planning, competitive benchmarking, partnership evaluation, product portfolio optimization, and long-term business decision-making across established and emerging market segments.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 139.2 Million |

| Market Revenue (2033) | USD 241.0 Million |

| CAGR (2026–2033) | 7.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Nestlé Purina PetCare; Mars Petcare; Hill's Pet Nutrition; Wellness Pet Company; Blue Buffalo; Diamond Pet Foods; Champion Petfoods; Farmina Pet Foods; Nulo Pet Food; Ziwi Peak; Tiki Pets; Weruva International; The Honest Kitchen |

| Customization & Pricing | Available on Request (10% Customization Free) |