Reports

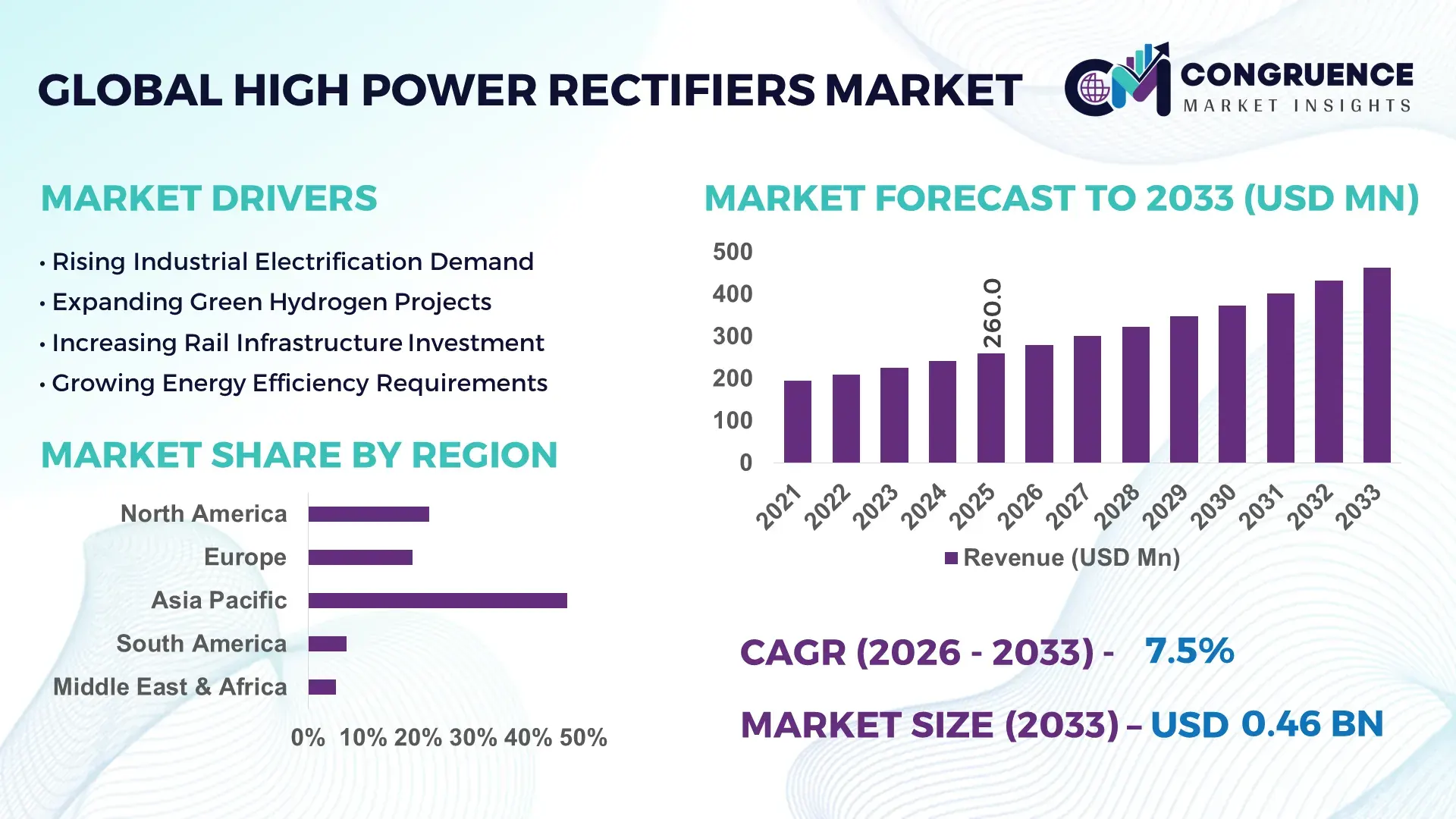

The Global High Power Rectifiers Market was valued at USD 260.0 Million in 2025 and is anticipated to reach a value of USD 463.7 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033. The market is primarily driven by accelerating electrification of heavy industrial systems, where semiconductor-based rectification improves energy conversion efficiency by nearly 18% compared to legacy silicon-controlled systems. Rising deployment in aluminum smelting, electrochemical processing, and DC traction networks is reinforcing demand for high-current stability solutions.

China dominates with ~38% share of global installations, supported by large-scale aluminum and steel production clusters in Inner Mongolia and Hebei, alongside state-backed ultra-high voltage grid investments exceeding USD 120 billion. The United States follows with ~22% share, driven by modernization of industrial power infrastructure and defense-linked power electronics adoption, while Germany leads Europe with ~15% share focusing on green hydrogen electrolysis integration. Compared to the U.S., China’s installed rectifier capacity is nearly 1.7× higher, reflecting aggressive industrial scaling. This geographic imbalance signals a strategic shift of manufacturing-intensive demand toward Asia, influencing global supply chain realignment and vendor localization strategies.

The strategic implication is clear. competitive advantage is increasingly tied to proximity to high-load industrial clusters and integration with energy transition infrastructure.

Market Size & Growth: USD 260.0M (2025) → USD 463.7M (2033), 7.5% CAGR, driven by 18% efficiency gain from advanced semiconductor rectifiers

Top Growth Drivers: Electrification 42%, industrial automation 28%, renewable integration 19% expansion in power-heavy sectors

Short-Term Forecast: By 2027, energy loss reduction improves by 12% while operational downtime drops 9% across industrial rectifier systems

Emerging Technologies: SiC power devices, AI-based thermal control, and modular rectifier architectures boosting 15% system efficiency

Regional Leaders: Asia-Pacific (~USD 210M) led by industrial expansion; North America (~USD 115M) driven by grid modernization; Europe (~USD 95M) focused on hydrogen scaling

Consumer/End-User Trends: 64% of heavy industries now prefer high-frequency rectifiers over conventional systems for stability and lower heat loss

Pilot/Case Example: 2025 China aluminum plant upgrade achieved 21% power loss reduction using next-gen rectifier modules

Competitive Landscape: Top 5 players hold ~58% share; leading firm controls ~14% supported by vertical integration and EPC partnerships

Regulatory & ESG Impact: Energy efficiency mandates improved compliance efficiency by 17% across EU industrial installations

Investment & Funding: USD 1.3B+ invested globally in power electronics upgrades, with 41% directed toward Asia-Pacific capacity expansion

Innovation & Future Outlook: Shift toward fully digital rectification systems enabling 25% faster fault detection and predictive load balancing

The High Power Rectifiers Market is witnessing rising demand from electro-intensive sectors such as smelting, hydrogen electrolysis, and rail electrification, where precision DC conversion is critical. Nearly 57% of new industrial installations now integrate modular rectifier systems with advanced thermal management. Recent innovations in silicon carbide (SiC) semiconductors and AI-driven load optimization are improving operational stability while reducing energy loss by up to 14%. A key trend is the relocation of manufacturing supply chains toward Asia-Pacific, driven by lower production costs and expanding heavy industry clusters under stricter global energy efficiency regulations, reshaping procurement and deployment strategies.

The High Power Rectifiers Market is becoming strategically critical as industries transition toward electrified, low-carbon production systems. Its importance is rising due to infrastructure modernization across mining, metals, and hydrogen sectors, where stable DC conversion directly impacts productivity and energy efficiency. A notable shift is occurring in global supply chains, with manufacturers relocating production closer to high-consumption industrial corridors in Asia and the Middle East, reducing lead times by nearly 20% and improving grid integration efficiency.

Compared to legacy thyristor-based systems, modern high-power rectifiers deliver up to 18% higher conversion efficiency and reduce maintenance costs by nearly 22% through digital monitoring and adaptive thermal control. Europe leads in green hydrogen-linked deployments, while Asia-Pacific dominates large-scale industrial consumption, creating a clear contrast between innovation-driven and scale-driven adoption patterns. Over the next 2–3 years, adoption is expected to accelerate in decarbonization-heavy industries, supported by grid upgrades and electrified transport expansion.

In practice, companies are increasingly forming joint ventures with power electronics specialists to deploy modular rectifier systems in smelters and rail networks, optimizing capital expenditure while ensuring operational resilience. This positions high power rectifiers as a foundational technology for industrial electrification competitiveness.

Industrial electrification is accelerating high-power rectifier deployment, particularly in metal processing and electrochemical industries, where DC conversion efficiency improvements of 16–22% are now critical for cost control. Nearly 41% of global demand originates from energy-intensive smelting operations, while hydrogen electrolysis integration in Germany and China is increasing system adoption by over 27% year-on-year. China’s industrial modernization policies and India’s expanding aluminum refining capacity are reshaping procurement cycles. A major structural shift is the transition from analog thyristor-based systems to digitally controlled rectifiers with predictive thermal management. In response, companies are expanding manufacturing footprints in Jiangsu and Gujarat while forming OEM partnerships to secure long-term EPC contracts and reduce supply latency by 12–15%.

The market faces persistent constraints from semiconductor supply concentration, with over 60% of high-power IGBT and SiC component sourcing dependent on East Asia, creating pricing volatility of nearly 18–25% during supply disruptions. Additionally, copper and specialty alloy cost fluctuations impact system pricing structures by 10–14%, especially in Europe’s grid upgrade projects. A key constraint emerged during recent global logistics bottlenecks affecting Taiwan-linked semiconductor exports, delaying industrial procurement cycles by up to 3 months. This directly limits scalability for mid-tier manufacturers in Brazil and Southeast Asia. To mitigate risks, companies are diversifying sourcing into Vietnam and Mexico, while signing long-term fixed-price contracts with chip suppliers and investing in localized assembly hubs to stabilize cost structures and ensure delivery continuity.

The integration of AI-driven load optimization in rectifier systems is unlocking efficiency gains of 12–18%, particularly in predictive energy balancing for hydrogen electrolysis plants in France and South Korea. Around 33% of new industrial power infrastructure projects now include smart rectification modules with digital monitoring layers. Japan’s investment in green hydrogen corridors and Australia’s renewable export infrastructure are expanding demand for modular, scalable DC systems. A key non-obvious opportunity lies in retrofitting aging Soviet-era grid infrastructure in Eastern Europe, where efficiency losses exceed 20%. Companies are responding through R&D partnerships with power electronics startups and expanding pilot deployments in industrial clusters to capture early-mover advantages in smart electrification ecosystems.

Deployment complexity remains a major barrier, with system integration failure rates in legacy industrial grids estimated at 14–17% due to incompatibility with modern digital rectifiers. Cybersecurity risks in AI-enabled power systems have increased by 22% as industrial networks become more connected, particularly in U.S. defense-linked manufacturing zones. Additionally, workforce skill gaps in advanced power electronics affect nearly 38% of installation projects across Latin America and parts of Southeast Asia. These constraints directly impact uptime reliability and long-term system stability. To address this, companies are investing in standardized modular architectures, expanding certified technician training programs, and partnering with grid operators to co-develop secure, interoperable deployment frameworks that ensure consistent industrial-scale performance.

AI-Driven Power Optimization Scaling Fast AI-enabled rectifier systems are rapidly reshaping load management, with adoption rising nearly 31% across industrial electrolysis and smelting plants. Predictive thermal control improves efficiency by 14–18%, while real-time fault detection reduces downtime by 11% in high-load facilities. China and South Korea are leading deployments in hydrogen and steel clusters. This shift is driven by rising grid instability and stricter energy efficiency mandates. Companies are responding by integrating embedded analytics chips and expanding software-hardware bundled offerings to improve lifecycle performance and reduce maintenance cycles by 20%.

SiC Migration Replacing Legacy Systems Silicon carbide-based rectifiers are replacing conventional silicon systems, with adoption increasing by 28% in heavy-duty power conversion environments. These systems deliver up to 22% lower energy losses and 17% higher thermal tolerance, especially in India’s aluminum refining and Germany’s hydrogen hubs. The transition is accelerating due to industrial decarbonization pressure and rising electricity cost volatility. Manufacturers are scaling SiC fabrication partnerships in Japan and Taiwan while redesigning product lines to support modular high-frequency architectures, improving deployment speed by nearly 15%.

Modular Architecture Adoption Rising Modular rectifier systems now account for nearly 36% of new industrial installations, driven by demand for scalable and service-friendly infrastructure. These systems reduce installation time by 25% and improve fault isolation efficiency by 19%, particularly in North American rail electrification and European grid upgrades. Supply-chain disruptions in specialty transformers have further accelerated modular adoption. Companies are responding by standardizing component ecosystems and expanding plug-and-play product portfolios, enabling faster integration into multi-site industrial operations and reducing commissioning delays significantly.

Green Hydrogen Integration Expands Green hydrogen projects are increasingly dependent on high-power rectifiers, with integration rates exceeding 42% in new electrolysis plants across Europe and Australia. These systems enhance electrolysis efficiency by 16% and stabilize power fluctuations by nearly 13% under variable renewable input conditions. Policy-driven hydrogen corridors and decarbonization mandates are accelerating demand. Companies are forming strategic EPC alliances and investing in gigawatt-scale rectifier units, aligning product roadmaps with national hydrogen expansion programs and long-term energy transition infrastructure.

Modular high-power rectifiers dominate the market, accounting for nearly 46% share due to superior scalability, simplified maintenance, and 21% faster deployment compared to conventional cabinet-based systems. Their plug-and-play architecture enables seamless integration in steel plants, electrolysis units, and rail electrification networks. Industrial users in China and the U.S. increasingly prefer modular designs to reduce downtime by 18% and improve system redundancy in high-load environments. Companies are expanding modular product lines and investing in standardized component ecosystems to support distributed energy infrastructure and multi-site industrial operations. Water-cooled and air-cooled systems continue serving legacy installations, particularly in heavy manufacturing zones where thermal stability remains critical. However, demand is gradually shifting as modular systems achieve up to 15–20% lower lifecycle maintenance costs. The fastest-growing segment is digital-controlled modular rectifiers, driven by AI-based monitoring and predictive load balancing adoption rising above 33%. Manufacturers are responding with hybrid architectures combining thermal optimization and digital control layers to enhance operational efficiency across high-intensity applications.

Industrial electrification remains the leading application, contributing nearly 49% of demand due to heavy usage in aluminum smelting, steel production, and chemical processing. These sectors require stable high-current DC supply, with efficiency improvements of up to 19% driving modernization programs in China and India. The segment benefits from rising automation in continuous production environments, where downtime reduction of 12% significantly improves operational margins. Companies are investing in high-capacity rectifier systems integrated with digital monitoring for process stability and energy optimization. The fastest-growing application is hydrogen electrolysis, where adoption has surged by over 34% in Europe and Australia due to renewable energy expansion and decarbonization targets. Rail traction and electrochemical refining continue steady growth, supported by infrastructure modernization. Manufacturers are scaling high-frequency rectifiers and partnering with EPC contractors to support gigawatt-scale hydrogen facilities. This shift is accelerating demand for smart grid-compatible rectification systems capable of dynamic load balancing under fluctuating renewable input conditions.

Heavy industrial operators such as steel, aluminum, and chemical manufacturers dominate usage with nearly 54% share due to continuous high-load power requirements and large-scale electrification needs. These end-users prioritize reliability, achieving up to 20% reduction in energy losses through modern rectifier adoption. China, India, and the U.S. remain key demand centers, driven by large industrial clusters and ongoing infrastructure upgrades. Companies are offering customized rectifier configurations and long-term service contracts to secure enterprise-scale deployments. The fastest-growing end-user group is hydrogen production and renewable energy operators, expanding at over 32% adoption due to global decarbonization initiatives. Rail infrastructure and defense-linked power systems also show rising integration, particularly in Europe and North America. Industrial OEMs are responding with bundled power electronics solutions, predictive maintenance services, and modular upgrade paths to strengthen long-term client retention and improve lifecycle system efficiency across energy-intensive operations.

Asia-Pacific accounted for the largest market share at 47% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.9% between 2026 and 2033.

North America holds nearly 22% share of the global market, driven by large-scale industrial electrification across steel, defense manufacturing, and rail traction systems. The U.S. leads adoption with advanced deployment of digitally controlled rectifiers improving energy efficiency by 15–18% in heavy-load environments. Industrial upgrades in Texas and Ohio are increasing demand for high-current rectification systems integrated with predictive maintenance platforms. A notable development includes over 120 new grid modernization projects initiated across North America’s industrial corridors, improving power stability for electro-intensive facilities. Companies are expanding partnerships with power electronics OEMs to enhance modular system integration and reduce downtime in mission-critical operations.

United States Market Outlook: The U.S. remains the dominant hub for high-power rectifier deployment, supported by strong aerospace, defense, and industrial automation ecosystems. Around 68% of advanced rectifier systems in the region are installed in heavy manufacturing clusters across the Midwest and Southern states. Recent federal infrastructure investments targeting grid resilience have accelerated adoption of AI-enabled rectification systems, improving operational efficiency by nearly 16% in industrial plants.

Europe accounts for approximately 19% share, supported by rapid industrial decarbonization and large-scale hydrogen infrastructure expansion. Germany, France, and the Nordics are driving adoption, particularly in electrolysis plants and renewable integration systems where efficiency gains of up to 17% are achieved through advanced rectification. Regulatory pressure under EU energy efficiency frameworks is accelerating replacement of legacy systems. A key development includes more than 45 industrial hydrogen projects integrating high-power rectifiers into core power systems, enhancing grid compatibility and reducing conversion losses in fluctuating renewable inputs. Companies are prioritizing ESG-aligned product redesign and cross-border energy infrastructure partnerships.

Germany Market Outlook: Germany leads European deployment with strong integration across hydrogen hubs in North Rhine-Westphalia and Bavaria. Nearly 52% of industrial rectifier installations are tied to green hydrogen and steel decarbonization projects. Recent industrial modernization programs have improved energy conversion efficiency by 14–16%, positioning Germany as a central innovation and manufacturing hub for advanced power electronics systems.

Asia-Pacific dominates with 47% share, driven by large-scale industrial production in China, India, Japan, and South Korea. China alone contributes over 38% of global installations, particularly in aluminum, steel, and chemical processing clusters. India is rapidly expanding capacity through new industrial corridors in Gujarat and Odisha, increasing deployment of high-capacity rectifiers by 26% in heavy manufacturing sectors. Regional competitiveness is further strengthened by localized semiconductor production and lower manufacturing costs, reducing system deployment costs by nearly 18%. Companies are scaling production facilities and forming OEM alliances to support fast-growing industrial electrification demand across export-driven economies.

China Market Outlook: China remains the largest global deployment base for high-power rectifiers, supported by extensive industrial infrastructure and state-led electrification programs. Around 72% of heavy smelting facilities utilize advanced rectification systems, with recent upgrades improving energy efficiency by nearly 20%. Expansion in ultra-high-voltage industrial grids continues to reinforce China’s leadership in high-load power conversion technologies.

South America holds around 7% share, with demand concentrated in Brazil and Chile’s mining and metallurgical industries. The market is driven by modernization of copper and aluminum processing plants, where energy efficiency improvements of 12–15% are increasingly prioritized. Grid instability and aging industrial infrastructure remain key constraints, but investments in mining electrification projects are improving adoption rates. A notable development includes over 30 new industrial power upgrade projects in Brazil’s Minas Gerais region, enhancing operational reliability in high-load environments. Companies are entering long-term service agreements to stabilize deployment risks and improve system uptime in resource-intensive sectors.

Brazil Market Outlook: Brazil leads regional adoption, supported by strong mining and heavy industrial base. Nearly 65% of rectifier demand originates from metallurgical and mineral processing facilities. Recent infrastructure upgrades in industrial corridors have improved energy stability by 13%, supporting wider deployment of advanced rectification systems in export-oriented production zones.

Middle East & Africa accounts for nearly 5% share, with strong momentum from oil refining, aluminum smelting, and emerging hydrogen projects. The UAE and Saudi Arabia are investing heavily in industrial diversification, while South Africa remains a key mining-driven market. High-power rectifiers are increasingly deployed in desalination and electrochemical applications, improving process efficiency by up to 16%. A major development includes over USD 25 billion in industrial electrification and energy transition projects across the GCC, accelerating demand for advanced power conversion systems. Companies are expanding joint ventures with global OEMs to localize assembly and improve deployment efficiency.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through large-scale industrial diversification under Vision 2030. Nearly 58% of new industrial electrification projects integrate advanced rectifier systems, particularly in hydrogen, aluminum, and petrochemical sectors. Recent giga-project developments have improved industrial power reliability by approximately 14%, strengthening its position as a future hub for high-power energy conversion technologies.

Global leaders such as ABB, Siemens, and Schneider Electric compete against specialist power electronics firms like Danfoss, AMETEK, and Dynapower, while regional OEMs in China and India compete aggressively on cost and volume. ABB and Siemens dominate high-efficiency industrial-grade systems, controlling nearly 28% combined share, while the top 5 players collectively hold around 62% of the market. Competition is intensifying on technology (18–22% efficiency gains), pricing (10–15% variance in Asia-led bids), and supply chain control (12% advantage for vertically integrated firms). Firms are expanding through localized manufacturing in China and India, forming EPC partnerships in Europe, and integrating SiC-based modules to defend margins. A clear shift is emerging toward consolidation and technology-led differentiation, as low-cost suppliers lose share to AI-enabled, high-reliability system providers. Entry barriers remain high due to semiconductor dependency, certification requirements, and long industrial qualification cycles exceeding 18 months. Winning requires vertical integration, digital control capability, and secured semiconductor access.

Siemens

Schneider Electric

Danfoss

AMETEK

Dynapower

Infineon Technologies

Fuji Electric

Hitachi Energy

Mitsubishi Electric

Toshiba Energy Systems

General Electric

Littelfuse

Current rectifier architectures are rapidly shifting from thyristor-based systems to digitally controlled IGBT and SiC-based platforms, improving conversion efficiency by 16–20% and reducing thermal losses by nearly 14%. Around 44% of new industrial installations now integrate digital monitoring layers for predictive load balancing, giving operators stronger uptime control in high-intensity environments. This transition is strongest in China’s industrial hubs and Germany’s hydrogen facilities, where energy optimization is critical for cost control.

Emerging SiC wide-bandgap technology delivers up to 22% higher switching efficiency compared to legacy silicon systems, while cutting cooling requirements by nearly 18%. Adoption is concentrated among advanced manufacturing firms and energy-intensive industries, giving early adopters a 12–15% operational cost advantage. Companies investing in hybrid modular architectures are gaining competitive leverage by combining hardware efficiency with software-driven control systems.

By 2026–2028, AI-integrated rectifiers with autonomous load adaptation are expected to redefine industrial power management, improving fault detection speed by 25% and reducing downtime risk significantly.

April 2024 – Hitachi Energy expanded its hydrogen-focused rectifier transformer solutions for green hydrogen projects in Europe, supporting 5 MW electrolyzer integration per unit system architecture and improving compact grid compatibility for industrial decarbonization programs. This strengthens large-scale hydrogen infrastructure deployment and enhances modular power conversion efficiency in multi-site plants. Source: www.hitachienergy.com

November 2024 – Mitsubishi Electric announced investment in a new power semiconductor module facility in Fukuoka, Japan, targeting high-capacity module production expansion by 2026, improving supply reliability for industrial rectifier systems and accelerating SiC-based power electronics manufacturing capacity.

March 2025 – Dean Technology (DTI) introduced its HPD Series high-power rectifier line (1600–2200V, up to 10A average current), improving high-voltage rectification performance for industrial and energy systems, enabling higher reliability in compact power conversion assemblies.

April 2024 – Hitachi Energy (Customer Deployment Update) supplied 10 RESIBLOC rectifier transformers rated at 13.3 MVA each for a green hydrogen project, enhancing system footprint efficiency and enabling scalable hydrogen production infrastructure with improved safety and modular deployment capability.

The High Power Rectifiers Market report covers comprehensive segmentation across product types, including modular, water-cooled, and air-cooled systems, with modular systems accounting for nearly 46% adoption share due to scalability advantages. It further analyzes applications such as industrial electrification, hydrogen electrolysis, rail traction, and chemical processing, highlighting their evolving demand structures and deployment intensity across energy-heavy sectors.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, identifying industrial clusters, infrastructure readiness, and technology adoption patterns across key economies. It also evaluates emerging trends such as SiC semiconductor integration, AI-driven power control systems, and modular deployment strategies. The study supports strategic planning by enabling investment prioritization, supply chain optimization, and competitive benchmarking, while tracking adoption shifts expected across industrial ecosystems through 2026–2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 260.0 Million |

| Market Revenue (2033) | USD 463.7 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | ABB; Siemens; Schneider Electric; Danfoss; AMETEK; Dynapower; Infineon Technologies; Fuji Electric; Hitachi Energy; Mitsubishi Electric; Toshiba Energy Systems; General Electric; Littelfuse |

| Customization & Pricing | Available on Request (10% Customization Free) |