Reports

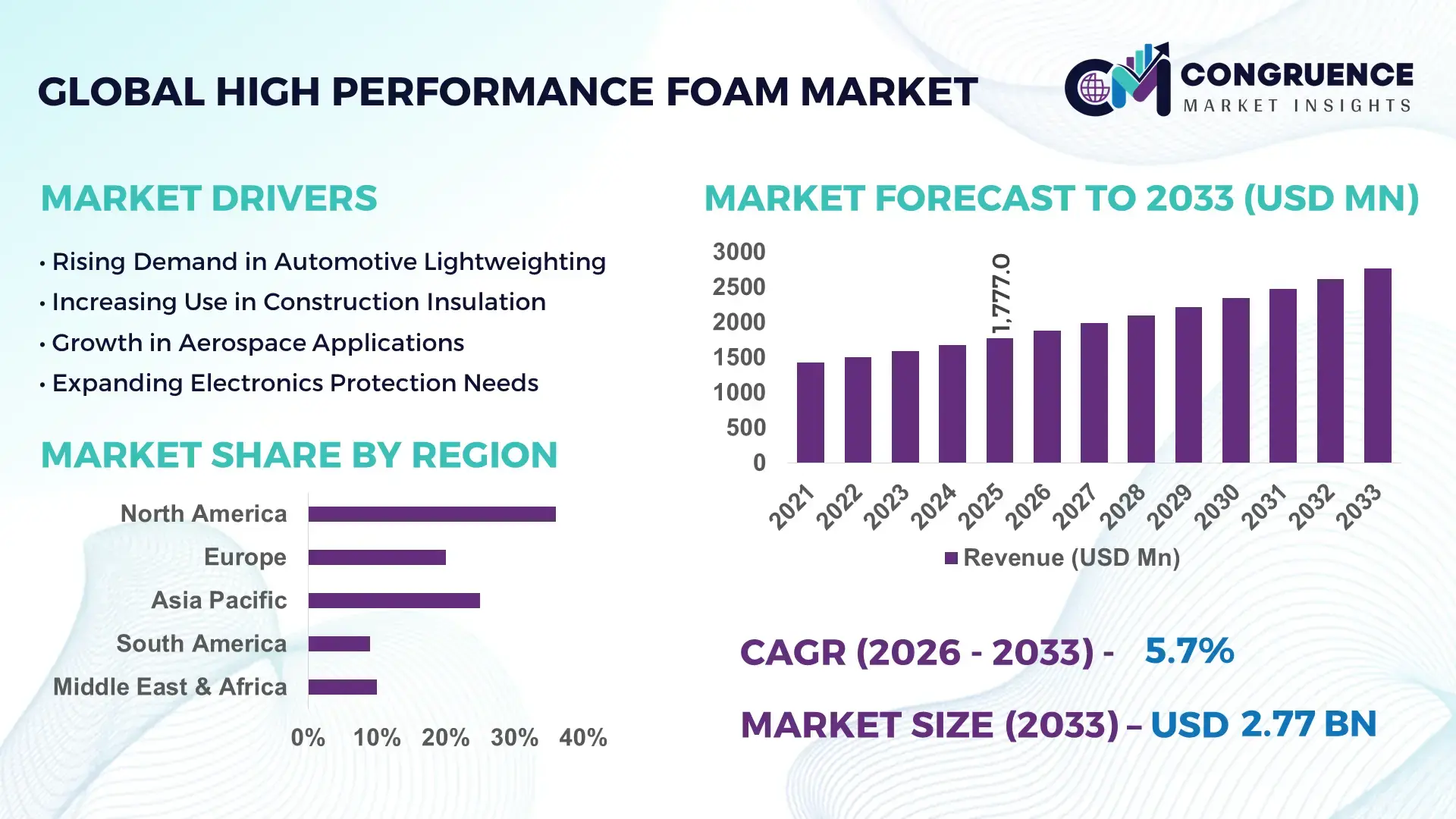

The Global High Performance Foam Market was valued at USD 1777 Million in 2025 and is anticipated to reach a value of USD 2768.77 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. Growth is primarily driven by rising demand for lightweight, durable, and energy-efficient materials across automotive, aerospace, construction, and electronics industries.

The United States stands as a dominant country in the high performance foam market, supported by advanced manufacturing capabilities and consistent industrial investments exceeding USD 20 billion annually in polymer and specialty materials. The country produces over 30% of global polyurethane-based high performance foams, widely utilized in automotive insulation, aerospace seating, and thermal management systems. Approximately 65% of electric vehicle manufacturers in the U.S. integrate high performance foam for battery insulation and vibration damping. Additionally, the construction sector contributes significantly, with over 40% adoption of rigid foam insulation in commercial buildings. Continuous innovation in nanostructured foams and bio-based formulations, alongside strong R&D spending, further enhances production efficiency and product performance.

Market Size & Growth: USD 1777 Million in 2025, projected to reach USD 2768.77 Million by 2033, growing at 5.7% CAGR driven by lightweight material demand.

Top Growth Drivers: Automotive lightweighting (42%), energy-efficient construction adoption (38%), electronics thermal insulation demand (29%).

Short-Term Forecast: By 2028, advanced foam materials are expected to reduce insulation costs by 18% and improve energy efficiency by 25%.

Emerging Technologies: Nanocellular foams, bio-based polyurethane foams, and smart memory foams with adaptive properties.

Regional Leaders: North America (USD 950 Million by 2033, EV integration growth), Europe (USD 780 Million, sustainability-driven adoption), Asia-Pacific (USD 1038 Million, manufacturing expansion).

Consumer/End-User Trends: Automotive and construction sectors account for over 60% of demand, with increasing preference for eco-friendly materials.

Pilot or Case Example: In 2024, a European automotive OEM achieved 22% weight reduction using advanced foam composites.

Competitive Landscape: Market leader holds approximately 18% share, followed by major global polymer and foam manufacturers.

Regulatory & ESG Impact: Regulations targeting 30% reduction in building energy consumption are accelerating foam insulation adoption.

Investment & Funding Patterns: Over USD 5 billion invested in advanced materials and sustainable foam technologies in recent years.

Innovation & Future Outlook: Focus on recyclable foams, AI-driven material design, and high-performance hybrid composites.

High performance foam is increasingly critical across multiple industries, with automotive contributing nearly 35% of total consumption due to its role in lightweighting and noise reduction. The construction sector follows with approximately 30% usage, driven by stringent energy efficiency standards and green building certifications. Technological advancements such as closed-cell foam structures and aerogel-infused foams are improving thermal resistance by up to 40%. Regulatory pressure to reduce carbon emissions is pushing manufacturers toward recyclable and bio-based foam solutions. Asia-Pacific is witnessing rapid consumption growth due to industrialization, while Europe focuses on sustainable innovations. Future trends indicate rising integration of smart foams in electronics and healthcare applications, supporting long-term market expansion.

The high performance foam market holds strong strategic relevance as industries increasingly prioritize lightweight, energy-efficient, and high-durability materials. Advanced foam technologies are enabling manufacturers to meet strict environmental regulations while improving product performance. For instance, nanocellular foam technology delivers 35% higher thermal insulation compared to conventional polyurethane foam, making it a preferred choice in construction and cold-chain logistics. In parallel, memory foam innovations are achieving 28% better load distribution compared to traditional cushioning materials, enhancing applications in healthcare and automotive seating.

Regionally, Asia-Pacific dominates in production volume due to large-scale manufacturing infrastructure, while Europe leads in adoption with over 55% of enterprises integrating sustainable foam solutions in construction and automotive sectors. By 2028, AI-driven material engineering is expected to improve production efficiency by 20% and reduce material waste by 15%, significantly enhancing cost-effectiveness.

From a compliance perspective, firms are committing to sustainability goals such as 25% reduction in carbon emissions and 30% recyclable material usage by 2030. In 2024, a leading automotive manufacturer in Germany achieved a 19% reduction in vehicle weight through the adoption of high performance composite foams, resulting in improved fuel efficiency and lower emissions. Strategically, the market is evolving through increased investments in bio-based materials, circular economy initiatives, and digital manufacturing technologies. These advancements position the high performance foam market as a critical pillar for industrial resilience, regulatory compliance, and sustainable growth in the coming decade.

The growing emphasis on lightweight materials across industries is a major driver of the high performance foam market. In the automotive sector, reducing vehicle weight by 10% can improve fuel efficiency by approximately 6–8%, prompting manufacturers to replace traditional materials with advanced foams. High performance foams are extensively used in vehicle interiors, seating systems, and structural components, contributing to weight reduction without compromising durability. In aerospace, foam-based materials help reduce aircraft weight, enhancing fuel efficiency and operational performance. Additionally, the construction industry is adopting lightweight foam insulation to improve building energy efficiency, with studies indicating up to 30% reduction in energy consumption. The electronics sector also benefits from foam materials for thermal management and protection of sensitive components. These applications collectively drive consistent demand, reinforcing the importance of high performance foam in modern industrial design and engineering.

Volatility in raw material prices presents a significant restraint for the high performance foam market. Key inputs such as petrochemical derivatives, including polyols and isocyanates, are subject to frequent price fluctuations due to changes in crude oil prices and supply chain disruptions. These fluctuations can lead to increased production costs, affecting profit margins for manufacturers. For instance, variations in petrochemical pricing have been observed to impact foam production costs by up to 20% annually. Additionally, supply chain constraints and geopolitical factors can disrupt the availability of essential raw materials, leading to production delays. Smaller manufacturers are particularly vulnerable, as they may lack the financial flexibility to absorb cost increases. Furthermore, the transition toward bio-based alternatives, while environmentally beneficial, often involves higher production costs and limited scalability, further complicating market dynamics and restraining growth potential.

Sustainable and bio-based foam innovations present significant opportunities for market expansion. Increasing environmental awareness and regulatory mandates are encouraging manufacturers to develop eco-friendly alternatives to traditional petroleum-based foams. Bio-based foams derived from renewable resources such as soy and plant oils are gaining traction, offering comparable performance with reduced carbon footprints. Research indicates that bio-based foam solutions can lower greenhouse gas emissions by up to 40% during production. Additionally, recyclable and biodegradable foam materials are becoming critical in packaging and construction applications, where sustainability is a key purchasing criterion. The adoption of circular economy practices is further opening new avenues for material reuse and recycling. Emerging markets in Asia-Pacific and Latin America are also presenting growth opportunities due to rapid urbanization and infrastructure development. These factors collectively create a favorable environment for innovation and long-term market growth.

Regulatory compliance and environmental standards pose considerable challenges for the high performance foam market. Governments worldwide are implementing stringent regulations aimed at reducing carbon emissions, limiting the use of hazardous chemicals, and promoting sustainable materials. Compliance with these regulations often requires significant investment in research, production upgrades, and certification processes. For example, restrictions on volatile organic compounds (VOCs) and flame retardants necessitate the development of alternative formulations, which can increase production complexity and costs. Additionally, meeting recycling and waste management requirements requires advanced infrastructure and supply chain coordination. Manufacturers must also ensure product performance is not compromised while adhering to environmental standards. These challenges can slow down innovation cycles and increase time-to-market for new products. Balancing regulatory compliance with cost efficiency and product quality remains a critical hurdle for industry participants.

• Accelerated Adoption of High-Performance Insulation in Green Buildings: The demand for high performance foam in sustainable construction has increased significantly, with over 62% of new commercial buildings integrating advanced insulation materials to meet energy efficiency standards. High-density rigid foams are delivering up to 45% improvement in thermal resistance compared to traditional materials, reducing HVAC energy consumption by nearly 30%. In Europe, approximately 58% of construction firms are prioritizing eco-friendly foam solutions to comply with strict building codes, while North America has reported a 35% rise in retrofitting projects using spray foam insulation for energy optimization.

• Growth in Electric Vehicle Lightweighting and Thermal Management: The automotive sector is witnessing a surge in high performance foam usage, with nearly 68% of electric vehicle manufacturers incorporating foam-based components for battery insulation and impact resistance. Advanced foam composites are enabling up to 20% reduction in vehicle weight while enhancing thermal stability by 25%. In Asia-Pacific, EV production facilities have increased foam material consumption by over 40% since 2023, driven by the need for improved safety and energy efficiency. Battery systems utilizing specialized foam layers have demonstrated a 15% increase in lifespan due to better thermal regulation.

• Expansion of Bio-Based and Recyclable Foam Solutions: Sustainability-driven innovation is transforming the market, with bio-based foam products accounting for approximately 28% of new product developments in 2025. These materials reduce carbon emissions by up to 38% during production compared to petroleum-based alternatives. Manufacturers are also focusing on recyclable foam systems, with over 50% of leading producers introducing closed-loop recycling processes. Adoption of biodegradable foams in packaging has grown by 33%, particularly in consumer electronics and e-commerce sectors, where regulatory pressure for sustainable materials is intensifying.

• Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the high performance foam market. Around 55% of new construction projects have reported cost savings through prefabrication techniques, where foam components are pre-cut and assembled off-site using automated systems. This approach reduces project timelines by nearly 25% and minimizes material wastage by up to 20%. Demand for precision-engineered foam panels is increasing, particularly in North America and Europe, where over 48% of contractors are integrating prefabricated insulation systems to enhance efficiency and reduce labor dependency.

The high performance foam market is segmented based on type, application, and end-user industries, each contributing uniquely to overall demand patterns. Polyurethane-based foams dominate due to their versatility and superior insulation properties, while polystyrene and polyethylene foams cater to specialized applications requiring rigidity and chemical resistance. In terms of application, building and construction leads with over 30% usage, followed by automotive and aerospace sectors driven by lightweighting requirements. End-user insights reveal strong adoption across automotive, construction, electronics, and healthcare industries, with combined industrial applications accounting for more than 75% of total consumption. Emerging demand from renewable energy and advanced electronics sectors is further diversifying market opportunities. The segmentation highlights a shift toward high-performance, sustainable, and application-specific foam solutions tailored to evolving industrial requirements.

Polyurethane foam remains the leading product type in the high performance foam market, accounting for approximately 46% of total adoption due to its superior thermal insulation, flexibility, and durability across diverse applications. Expanded polystyrene (EPS) and extruded polystyrene (XPS) collectively hold around 28%, primarily used in construction and packaging due to their rigidity and moisture resistance. However, polyethylene foam is emerging as the fastest-growing segment, expanding at an estimated CAGR of 6.4%, driven by its increasing use in protective packaging and automotive components where shock absorption is critical.

Phenolic foams and melamine foams contribute to niche applications such as fire-resistant insulation and acoustic management, together accounting for nearly 26% of the market. These materials are gaining traction in high-temperature and safety-critical environments, including aerospace and industrial facilities.

Building and construction is the leading application segment, representing approximately 34% of total usage due to the critical role of high performance foam in insulation, sealing, and structural support. Automotive applications account for nearly 27%, focusing on lightweighting, noise reduction, and thermal management. Aerospace and electronics applications together contribute around 21%, driven by demand for advanced materials that offer durability and thermal stability. The fastest-growing application segment is electric vehicles and advanced mobility systems, expanding at an estimated CAGR of 7.1%. This growth is fueled by increasing EV production and the need for efficient battery insulation and vibration control. High performance foams are enabling improved safety and energy efficiency in these systems.

Other applications, including packaging, healthcare, and renewable energy, collectively account for approximately 18% of the market. These segments are witnessing steady growth due to rising demand for protective materials and specialized insulation solutions.

The automotive industry is the leading end-user segment, accounting for approximately 32% of total market consumption, driven by the increasing integration of high performance foam in vehicle interiors, battery systems, and structural components. The construction sector follows with around 29%, leveraging foam materials for insulation and energy efficiency improvements. Electronics and electrical industries contribute nearly 18%, utilizing foam for thermal management and component protection. The fastest-growing end-user segment is the renewable energy sector, expanding at an estimated CAGR of 6.9%, supported by the increasing deployment of wind turbines and solar panels requiring advanced insulation and protective materials. High performance foams are playing a critical role in improving the durability and efficiency of these systems.

Other end-users, including healthcare, packaging, and aerospace, collectively account for approximately 21% of the market, with healthcare applications seeing increased adoption of memory foam in medical devices and patient support systems.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America’s dominance is supported by strong demand from automotive, aerospace, and construction sectors, with over 65% of commercial buildings utilizing advanced foam insulation. Europe follows with approximately 28% share, driven by sustainability regulations and energy-efficient construction mandates, where more than 58% of new projects incorporate high performance foam materials. Asia-Pacific holds nearly 26% of the market, with rapid industrialization and manufacturing expansion in China, India, and Japan contributing to increased consumption. The region has witnessed over 40% growth in foam usage in automotive and electronics manufacturing since 2022. South America and the Middle East & Africa collectively account for around 10%, with rising infrastructure investments and energy sector developments supporting demand. Increasing adoption of eco-friendly foam solutions and technological advancements across regions continue to shape global market dynamics.

North America holds approximately 36% of the global high performance foam market, driven by strong demand across automotive, construction, and aerospace industries. Over 70% of commercial construction projects in the region incorporate foam-based insulation systems to meet energy efficiency standards. Government regulations promoting energy conservation, including building codes targeting up to 30% reduction in energy consumption, are accelerating adoption. Technological advancements such as nanocellular foams and AI-driven material optimization are improving thermal performance by nearly 35%. A notable example includes a leading U.S.-based manufacturer expanding its production capacity by 18% in 2024 to meet rising demand for sustainable foam solutions. Consumer behavior in the region shows higher enterprise adoption, particularly in healthcare and automotive sectors, where demand for advanced cushioning and insulation materials continues to grow steadily.

Europe accounts for around 28% of the high performance foam market, with key countries such as Germany, the UK, and France leading adoption. More than 60% of construction projects in these countries utilize high performance foam to comply with stringent energy efficiency and environmental standards. Regulatory frameworks focused on reducing carbon emissions by up to 40% are pushing manufacturers toward eco-friendly foam solutions. The region is also witnessing increased adoption of bio-based and recyclable foams, with nearly 35% of manufacturers investing in sustainable product development. Technological advancements, including smart foam materials and advanced insulation systems, are enhancing performance across automotive and construction sectors. A major European manufacturer reported a 20% increase in production of recyclable foam products in 2025. Consumer behavior reflects strong preference for sustainable and regulatory-compliant materials, driving continuous innovation in the market.

Asia-Pacific ranks as one of the fastest-growing regions in the high performance foam market, accounting for nearly 26% of global consumption. China, India, and Japan are the top consuming countries, collectively contributing over 70% of regional demand. Rapid urbanization and infrastructure development have led to a 45% increase in foam usage in construction projects since 2023. The automotive and electronics industries are major growth drivers, with over 50% of manufacturers integrating foam materials for thermal management and lightweighting. The region is also emerging as a hub for technological innovation, with increasing adoption of automated foam production systems improving efficiency by up to 25%. A leading Asian manufacturer expanded its manufacturing facilities by 30% in 2024 to cater to growing demand. Consumer behavior in the region is driven by cost efficiency and large-scale industrial applications, particularly in e-commerce packaging and electronics.

South America holds approximately 6% of the high performance foam market, with Brazil and Argentina being the primary contributors. Infrastructure development projects have increased by nearly 20% over the past three years, driving demand for insulation and construction materials. The energy sector, particularly oil and gas, is a key consumer, accounting for over 25% of foam usage in the region. Government incentives promoting industrial growth and trade policies supporting material imports are facilitating market expansion. A regional manufacturer reported a 15% increase in production capacity in 2024 to meet rising demand from construction and energy sectors. Consumer behavior in South America is influenced by cost sensitivity and growing adoption of durable materials in infrastructure projects, supporting steady growth in the high performance foam market.

The Middle East & Africa region accounts for approximately 4% of the global high performance foam market, with the UAE and South Africa leading demand. Large-scale construction and oil & gas projects are key drivers, with over 30% of foam consumption linked to insulation in energy infrastructure. Urban development initiatives have increased demand for high performance foam in commercial buildings by nearly 22% since 2023. Technological modernization, including advanced insulation systems and fire-resistant foams, is enhancing product adoption. Trade partnerships and regulatory frameworks supporting sustainable construction are further boosting market growth. A regional supplier expanded its distribution network by 12% in 2025 to improve market reach. Consumer behavior is characterized by demand for high-durability materials capable of withstanding extreme environmental conditions.

United States – 31% share in the High Performance Foam market, driven by advanced manufacturing capacity and strong demand from automotive and construction sectors.

China – 27% share in the High Performance Foam market, supported by large-scale industrial production and rapid growth in electronics and infrastructure applications.

The high performance foam market is moderately fragmented, with over 120 active global and regional competitors operating across various product segments. The top five companies collectively account for approximately 38% of the total market share, indicating a competitive yet innovation-driven landscape. Leading players are focusing on strategic initiatives such as product innovation, mergers, acquisitions, and partnerships to strengthen their market position. Over 45% of major companies have introduced new high-performance and sustainable foam products between 2023 and 2025, targeting industries such as automotive, construction, and electronics.

Technological innovation remains a key competitive factor, with companies investing nearly 12% of their annual budgets in research and development to enhance material properties such as thermal insulation, durability, and recyclability. Strategic collaborations between manufacturers and end-user industries have increased by 25%, enabling customized foam solutions for specific applications. Additionally, capacity expansions have grown by over 20% globally, particularly in Asia-Pacific and North America, to meet rising demand. Digital transformation, including AI-driven material design and automated production processes, is further reshaping competition by improving efficiency and reducing production costs. The market continues to evolve with a strong emphasis on sustainability, performance optimization, and regional expansion strategies.

BASF SE

Covestro AG

Dow Inc.

Huntsman Corporation

Recticel NV

Rogers Corporation

Armacell International S.A.

Sekisui Chemical Co., Ltd.

Zotefoams plc

JSP Corporation

INOAC Corporation

FXI Holdings, Inc.

Trelleborg AB

UFP Technologies, Inc.

Technological advancements in the high performance foam market are significantly enhancing material efficiency, durability, and sustainability across industries. One of the most impactful innovations is the development of nanocellular foam structures, which feature cell sizes below 100 nanometers, improving thermal insulation performance by up to 40% compared to conventional foams. These materials are increasingly used in aerospace and high-end construction applications where superior insulation and lightweight properties are critical. Additionally, advancements in closed-cell foam technology are enabling moisture resistance levels exceeding 95%, making them highly suitable for marine, automotive, and infrastructure applications.

Digital manufacturing technologies, including AI-driven material design and automated production systems, are improving process efficiency by nearly 20% while reducing material waste by up to 15%. Additive manufacturing, or 3D printing of foam materials, is gaining traction, allowing manufacturers to produce complex geometries with precision and reduce production time by approximately 30%. This is particularly valuable in customized automotive and medical applications.

Sustainability-focused innovations are also reshaping the market, with bio-based polyurethane foams now incorporating up to 50% renewable raw materials, reducing carbon emissions during production by approximately 35%. Recyclable thermoplastic foams are being developed to support circular economy initiatives, with over 45% of leading manufacturers investing in recycling-compatible formulations. Furthermore, smart foams with embedded sensors are emerging, offering real-time monitoring of pressure, temperature, and structural integrity, enhancing performance in critical applications such as healthcare and aerospace. These technological advancements are positioning high performance foam as a cornerstone material in next-generation industrial solutions.

• In March 2025, BASF SE expanded its Elastoflex® polyurethane foam production capacity in North America to support growing demand from automotive and construction sectors. The expansion increased output efficiency by 15% while incorporating advanced low-emission processing technologies. Source: www.basf.com

• In September 2024, Covestro AG launched a new line of partially bio-based polyurethane foam systems under its Desmopan® range, incorporating up to 30% renewable content and reducing lifecycle emissions by approximately 20% compared to conventional materials. Source: www.covestro.com

• In January 2025, Armacell International S.A. introduced next-generation flexible elastomeric foam insulation with enhanced fire resistance and thermal performance improvements of up to 25%, targeting HVAC and industrial applications. Source: www.armacell.com

• In November 2024, Zotefoams plc announced the commercialization of its ReZorce® mono-material foam technology for sustainable packaging, achieving 100% recyclability and reducing plastic usage by nearly 50% in selected applications. Source: www.zotefoams.com

The High Performance Foam Market Report provides a comprehensive analysis of industry segments, applications, technologies, and regional trends shaping market evolution. The report covers multiple foam types, including polyurethane, polystyrene, polyethylene, phenolic, and specialty foams, which collectively account for over 90% of industrial usage. It evaluates key application areas such as construction, automotive, aerospace, electronics, packaging, and healthcare, with construction and automotive sectors contributing more than 60% of total demand.

Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing region-specific consumption patterns, industrial growth, and regulatory frameworks. Asia-Pacific is highlighted for its expanding manufacturing base, while Europe is assessed for its leadership in sustainable material adoption. The report also examines emerging niche segments such as bio-based foams, smart foams with embedded sensing capabilities, and recyclable thermoplastic foams, which are gaining traction due to environmental and performance requirements.

From a technological perspective, the report explores advancements in nanocellular foam structures, additive manufacturing, and AI-driven material engineering, which are improving product efficiency by up to 40% in certain applications. It further assesses supply chain dynamics, raw material dependencies, and production innovations that influence market competitiveness. The scope includes analysis of end-user industries, adoption rates, and performance benchmarks, providing decision-makers with actionable insights into product development, investment opportunities, and strategic expansion areas within the high performance foam market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

BASF SE, Covestro AG, Dow Inc., Huntsman Corporation, Recticel NV, Rogers Corporation, Armacell International S.A., Sekisui Chemical Co., Ltd., Zotefoams plc, JSP Corporation, INOAC Corporation, FXI Holdings, Inc., Trelleborg AB, UFP Technologies, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |