Reports

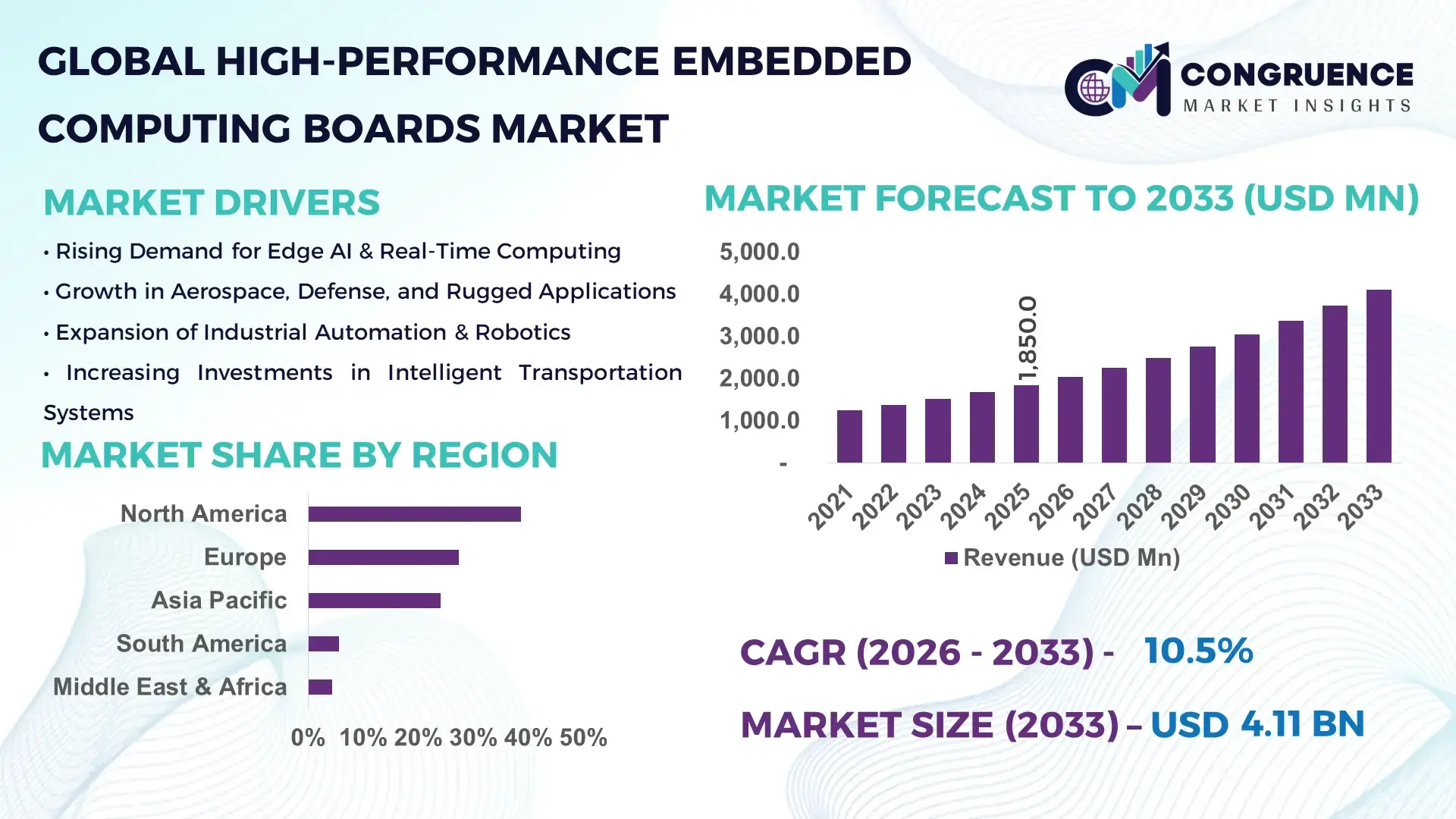

The Global High-Performance Embedded Computing Boards Market was valued at USD 1,850.0 Million in 2025 and is anticipated to reach a value of USD 4,112.2 Million by 2033 expanding at a CAGR of 10.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising deployment of compute-intensive embedded platforms across AI inference, real-time analytics, autonomous systems, and mission-critical industrial applications.

The United States dominates the High-Performance Embedded Computing Boards Market through a strong concentration of advanced manufacturing capacity, defense-grade electronics production, and semiconductor ecosystem depth. The country hosts over 35% of global high-reliability embedded board manufacturing facilities, with annual production exceeding 6.5 million high-performance units used in aerospace, defense, data center edge, and medical imaging systems. Public and private investment in embedded and edge computing hardware surpassed USD 18 billion between 2021 and 2024, accelerating adoption of PCIe Gen5, VPX, and COM-HPC standards. More than 60% of U.S. industrial automation OEMs integrate high-performance embedded boards into robotics, vision systems, and real-time control platforms, while AI-accelerated embedded deployments grew by 42% year-on-year in defense and transportation programs.

Market Size & Growth: Valued at USD 1,850.0 Million in 2025, projected to reach USD 4,112.2 Million by 2033 at a CAGR of 10.5%, driven by AI-enabled edge computing and real-time processing demand.

Top Growth Drivers: AI workload adoption (48%), real-time data processing efficiency gains (35%), and industrial automation penetration (29%).

Short-Term Forecast: By 2028, average compute density per embedded board is expected to improve by 32% through heterogeneous CPU-GPU architectures.

Emerging Technologies: COM-HPC modules, PCIe Gen5 connectivity, and embedded AI accelerators with >20 TOPS performance.

Regional Leaders: North America (USD 1,420.0 Million by 2033) driven by defense and AI edge; Europe (USD 1,060.0 Million) led by industrial automation; Asia Pacific (USD 980.0 Million) supported by manufacturing digitization.

Consumer/End-User Trends: Industrial OEMs account for ~41% usage, followed by aerospace & defense (27%) and medical systems (18%).

Pilot or Case Example: In 2024, an AI-enabled rail monitoring project achieved 38% fault detection improvement using high-performance embedded boards.

Competitive Landscape: Market leader holds ~22% share, followed by Advantech, Kontron, ADLINK, AAEON, and Curtiss-Wright.

Regulatory & ESG Impact: Defense and industrial safety standards increased certified embedded deployments by 26% since 2022.

Investment & Funding Patterns: Over USD 6.8 Billion invested globally in embedded hardware innovation and capacity expansion since 2021.

Innovation & Future Outlook: Integration of AI inference, real-time analytics, and secure boot architectures is shaping next-generation platforms.

High-Performance Embedded Computing Boards are increasingly adopted across industrial automation (41%), aerospace and defense (27%), medical imaging (18%), and transportation systems (14%). Recent innovations include COM-HPC form factors, AI accelerators exceeding 20 TOPS, and ruggedized boards supporting −40°C to 85°C operation. Regulatory emphasis on safety-certified electronics, combined with rising edge-AI workloads in North America and Europe, is reshaping consumption patterns, while Asia Pacific shows rapid growth in smart manufacturing and robotics deployments.

High-Performance Embedded Computing Boards play a strategic role in enabling real-time intelligence at the edge, supporting mission-critical operations across industrial automation, defense, transportation, and healthcare. Their relevance is increasing as enterprises shift from centralized cloud processing toward distributed, low-latency architectures. For example, COM-HPC platforms deliver up to 45% higher data throughput compared to legacy COM Express standards, enabling faster AI inference and sensor fusion in constrained environments.

From a regional perspective, North America dominates in volume, supported by defense and industrial deployments, while Europe leads in adoption, with approximately 54% of large industrial enterprises integrating high-performance embedded boards into automation and digital twin systems. By 2028, embedded AI acceleration is expected to improve predictive maintenance accuracy by 40%, reducing unplanned downtime in manufacturing and transportation networks.

Compliance and ESG considerations are also shaping future pathways. Firms are committing to energy efficiency improvements of 30% per compute cycle by 2030, supported by low-power heterogeneous architectures and advanced power management. In 2024, a U.S. defense electronics program achieved a 28% reduction in system latency by deploying AI-optimized embedded boards in autonomous surveillance platforms. Looking ahead, the High-Performance Embedded Computing Boards Market is positioned as a pillar of operational resilience, regulatory compliance, and sustainable digital infrastructure growth.

The High-Performance Embedded Computing Boards Market is shaped by rapid advancements in edge computing, AI acceleration, and real-time data processing requirements. Demand is rising as industries transition toward autonomous systems, intelligent factories, and connected infrastructure. Increased adoption of high-bandwidth interfaces, ruggedized designs, and modular architectures is influencing procurement decisions among OEMs. At the same time, tighter safety certifications and lifecycle reliability expectations are elevating technical standards. Supply chain localization, semiconductor availability, and evolving form-factor standards continue to influence competitive positioning and long-term deployment strategies.

Edge AI adoption is a primary growth driver, with over 52% of industrial AI workloads now processed locally rather than in centralized data centers. High-performance embedded boards enable sub-10-millisecond latency, essential for robotics, machine vision, and autonomous navigation. In manufacturing environments, AI-enabled embedded platforms have improved defect detection rates by 35% and reduced response times by 30%. Defense and transportation sectors increasingly rely on ruggedized embedded boards capable of sustaining high compute loads in harsh conditions, accelerating demand across certified and mission-critical deployments.

System integration complexity remains a restraint, particularly for legacy infrastructure upgrades. Over 40% of industrial operators report extended deployment timelines due to software compatibility, thermal management, and power optimization challenges. High-performance boards often require customized firmware, specialized cooling, and compliance testing, increasing engineering overhead. Additionally, shortages of skilled embedded system engineers have led to project delays averaging 18–24 weeks, limiting rapid scalability for small and mid-sized OEMs.

Industrial digitalization presents significant opportunities as smart factories expand globally. More than 65% of new production lines installed since 2023 incorporate real-time monitoring and AI-based control systems. High-performance embedded boards enable scalable deployment of digital twins, advanced robotics, and predictive analytics. Emerging economies in Asia Pacific are investing heavily in smart manufacturing, with embedded system adoption increasing by over 30% in electronics, automotive, and energy sectors.

Thermal management and power efficiency pose ongoing challenges as compute density increases. High-performance embedded boards can generate 25–40% more heat than previous generations, requiring advanced cooling solutions. In compact or sealed environments, inadequate thermal design can reduce system lifespan by up to 20%. Balancing performance with power consumption remains critical, especially in mobile, aerospace, and remote industrial applications where energy availability is limited.

Accelerated Adoption of AI-Optimized Embedded Architectures: AI-optimized boards integrating GPUs and NPUs have increased deployment rates by 46% since 2023, enabling real-time inference with latency reductions of up to 38% in industrial vision and robotics systems.

Shift Toward Modular and COM-HPC Form Factors: COM-HPC adoption has grown by 42%, allowing OEMs to scale performance without full system redesigns. Modular platforms have reduced development time by 30% and improved lifecycle flexibility.

Expansion of Ruggedized and Defense-Grade Deployments: Rugged embedded boards certified for extreme environments now account for over 28% of total demand, supporting temperatures from −40°C to 85°C and shock resistance improvements of 35%.

Increased Focus on Power Efficiency and Sustainability: Next-generation boards deliver 25% lower power consumption per compute unit, supporting ESG targets and enabling deployment in energy-constrained edge environments such as remote monitoring and transportation systems.

The High-Performance Embedded Computing Boards Market is segmented based on type, application, and end-user, reflecting the diverse technical requirements and deployment environments across industries. By type, the market spans modular compute boards, single-board computers, COM-based platforms, and ruggedized form factors, each addressing different performance, scalability, and environmental needs. Application-wise, demand is concentrated in real-time, compute-intensive use cases such as industrial automation, aerospace and defense systems, medical imaging, transportation, and edge AI analytics. End-user segmentation highlights strong adoption among industrial OEMs, defense contractors, healthcare technology providers, and system integrators, with varying expectations around lifecycle reliability, certification, and customization. Across segments, buyers increasingly prioritize heterogeneous computing, low-latency performance, and long-term availability over cost optimization, shaping procurement strategies and influencing product roadmaps. This segmentation underscores how performance requirements, deployment criticality, and regulatory constraints collectively define purchasing behavior in the market.

The market by type includes single-board computers (SBCs), computer-on-modules (COMs), VPX/OpenVPX boards, and ruggedized embedded computing boards. Computer-on-Modules (COMs) represent the leading type, accounting for approximately 38% of total adoption, driven by their modularity, scalability, and faster time-to-market for OEMs. COM platforms enable separation of compute and carrier board design, reducing redesign cycles by over 30% in industrial and defense programs. Single-board computers follow with around 27% adoption, favored for compact, cost-controlled deployments in industrial control and medical devices.

The fastest-growing type is OpenVPX and rugged high-speed backplane-based boards, expanding at an estimated 12.8% CAGR, supported by rising defense electronics modernization, radar processing, and autonomous systems requiring extreme bandwidth and reliability. Other types, including legacy form factors and application-specific custom boards, collectively account for nearly 35%, serving niche use cases where long lifecycle support or extreme environmental tolerance is critical.

In 2024, a U.S. defense research program deployed OpenVPX-based embedded boards to upgrade airborne signal processing systems, achieving a 40% increase in data throughput and reducing system latency by 25%.

By application, industrial automation and robotics lead the market with approximately 34% share, as factories deploy real-time vision processing, motion control, and predictive maintenance systems. These environments require deterministic performance and low-latency processing, making high-performance embedded boards essential. Aerospace and defense applications account for about 26%, supporting mission computers, electronic warfare, and autonomous platforms.

The fastest-growing application segment is edge AI and intelligent transportation systems, growing at an estimated 13.5% CAGR, fueled by smart mobility, autonomous vehicle testing, and real-time traffic analytics. Other applications, including medical imaging, energy infrastructure, and telecom edge systems, together contribute around 40% of demand.

Consumer and enterprise adoption trends further support this growth. In 2025, over 44% of global manufacturing enterprises reported piloting AI-enabled embedded systems for quality inspection, while nearly 39% of smart city projects integrated edge computing platforms for traffic and surveillance management.

In 2025, a national transportation authority implemented embedded AI boards across urban traffic hubs, reducing congestion-related delays by 22% through real-time signal optimization.

From an end-user perspective, industrial OEMs dominate adoption with roughly 41% share, leveraging high-performance embedded computing boards to power robotics, machine vision, and digital twin platforms. Defense and aerospace contractors follow at approximately 28%, driven by requirements for secure, rugged, and high-throughput computing in mission-critical systems.

The fastest-growing end-user segment is healthcare technology providers, expanding at an estimated 11.9% CAGR, supported by rising deployment of embedded computing in medical imaging, diagnostics, and robotic-assisted surgery. Other end-users, including transportation authorities, energy operators, and telecom infrastructure providers, collectively account for around 31% of demand. Adoption rates are accelerating, with over 46% of hospitals in developed markets evaluating embedded AI platforms for imaging and patient monitoring, and nearly 33% of utilities deploying edge computing for grid automation.

In 2024, a leading medical research institution integrated high-performance embedded boards into advanced imaging systems, improving image processing speed by 35% and supporting faster clinical decision-making.

North America accounted for the largest market share at 38.6% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.9% between 2026 and 2033.

North America’s leadership is supported by large-scale deployment of high-performance embedded computing boards across defense electronics, industrial automation, and medical imaging systems, with more than 62% of Tier-1 OEMs integrating embedded AI platforms into mission-critical workflows. Europe followed with approximately 27.4% share, driven by Industry 4.0 investments and stringent safety certifications. Asia-Pacific held nearly 24.1% share, supported by rising electronics manufacturing output and smart infrastructure projects. South America and the Middle East & Africa together accounted for about 9.9%, reflecting early-stage adoption but growing investments in transportation, energy, and smart city infrastructure.

North America accounted for approximately 38.6% of the global High-Performance Embedded Computing Boards Market in 2025, making it the leading regional contributor by volume and installed base. Demand is primarily driven by aerospace & defense, healthcare technology, industrial automation, and transportation systems, which together represent over 70% of regional deployments. Government-backed defense modernization programs and federal funding for smart manufacturing have accelerated adoption of rugged and AI-accelerated embedded platforms. Regulatory emphasis on cybersecurity compliance and functional safety standards has increased demand for certified embedded boards. Technological trends include rapid integration of edge AI, PCIe Gen5 connectivity, and heterogeneous computing architectures. A leading local player expanded its U.S. manufacturing capacity in 2024 to support high-reliability embedded boards for autonomous defense platforms. Regional consumer behavior shows higher enterprise adoption in healthcare and financial infrastructure, where low-latency processing and data security are critical.

Europe held around 27.4% share of the global market in 2025, supported by strong demand from Germany, the UK, and France, which together contribute over 65% of regional consumption. Industrial automation, railway systems, and energy infrastructure remain key application areas. Sustainability mandates and digital sovereignty initiatives have encouraged adoption of energy-efficient and locally manufactured embedded platforms. European manufacturers are increasingly deploying embedded boards supporting real-time analytics and functional safety compliance in smart factories. One regional supplier introduced low-power embedded AI boards optimized for predictive maintenance in industrial environments. Consumer behavior reflects strong preference for explainable and certifiable computing systems, with over 48% of industrial buyers prioritizing transparency and lifecycle traceability in procurement decisions.

Asia-Pacific ranked third by market share at 24.1% in 2025 but represents the largest volume growth opportunity. China, Japan, and India collectively account for nearly 72% of regional demand, driven by electronics manufacturing, robotics, and smart transportation projects. The region hosts more than 45% of global electronics production facilities, supporting rapid integration of embedded computing boards into factory automation and AI-enabled inspection systems. Innovation hubs across East Asia are accelerating adoption of modular and cost-optimized high-performance boards. A major regional manufacturer scaled production of AI-capable embedded platforms in 2024 to support robotics and logistics automation. Consumer behavior is shaped by e-commerce expansion and mobile-first AI applications, driving demand for scalable edge computing solutions.

South America accounted for approximately 5.6% of the global market in 2025, with Brazil and Argentina representing over 60% of regional demand. Embedded computing boards are increasingly used in energy management, transportation control systems, and media infrastructure. Government incentives supporting smart grid deployment and industrial modernization are improving adoption rates. Local system integrators are deploying high-performance embedded platforms in renewable energy monitoring and rail signaling projects. Regional consumer behavior indicates demand tied to media localization, surveillance, and language-adaptive systems, particularly in urban centers investing in smart infrastructure.

The Middle East & Africa region held around 4.3% market share in 2025, with the UAE, Saudi Arabia, and South Africa emerging as key growth markets. Demand is concentrated in oil & gas automation, transportation infrastructure, and smart city developments. Governments are investing heavily in digital transformation initiatives, increasing adoption of ruggedized and high-reliability embedded boards. Trade partnerships and technology localization programs support regional manufacturing and system integration. A regional technology provider deployed embedded computing platforms in smart traffic management projects, improving system response times by over 20%. Consumer behavior varies by country, with enterprise-led adoption dominating over consumer-driven demand.

United States – 32.1% Market Share: High production capacity and strong demand from defense, healthcare, and industrial automation sectors.

Germany – 11.6% Market Share: Deep integration of embedded computing in Industry 4.0 manufacturing and industrial control systems.

The competitive environment in the High-Performance Embedded Computing Boards Market is moderately fragmented, with an estimated 30–40 active global competitors offering a wide range of embedded board, module, and system solutions. The top 5 companies collectively account for approximately 46–52% of the total installed base, indicating a competitive but not highly consolidated landscape. Leading firms are intensely focused on strategic initiatives such as product innovation, partnerships, and platform ecosystem expansion, particularly around AI-accelerated edge computing and ruggedized industrial solutions. Recent product launches include advanced AI-ready embedded SBCs, modular COM modules, and high-speed PCIe Gen5 platforms, with multiple vendors enhancing support for heterogeneous CPU-GPU and NPU architectures. Collaboration strategies are also shaping the competitive landscape: major alliances between embedded platform suppliers and AI accelerator vendors are helping to streamline development cycles and broaden addressable applications. For example, several firms have formalized collaborations to integrate their embedded boards with third-party AI inference frameworks, reducing system integration complexity and improving performance benchmarks. Additionally, cross-industry partnerships—such as those between embedded board specialists and software ecosystem providers—are increasing solution stickiness and customer lock-in. Competitive differentiation increasingly revolves around certification credentials, long lifecycle support, advanced thermal management, ruggedization standards, and broad vertical market penetration, particularly in autonomous systems, industrial automation, and mission-critical sectors. As the market evolves, leaders are expected to pursue mergers, technology acquisitions, and strategic joint ventures to capture burgeoning opportunities in edge AI and connected infrastructure.

DFI Inc

IEI Integration Corp

Avalue Technology

Emerson Electric

Lanner Electronics

OnLogic

Nexcom International Co., Ltd.

Beckhoff Automation

MSI Computer Corp

Portwell, Inc.

Rugged Embedded Systems

The High-Performance Embedded Computing Boards Market is being significantly shaped by advancements in edge AI, heterogeneous computing, and ruggedized industrial designs. Current technologies emphasize heterogeneous architectures, combining multi-core CPUs, GPUs, and NPUs on a single board to support real-time AI inference, sensor fusion, and complex signal processing. Across embedded platforms, manufacturers are integrating high-bandwidth interfaces such as PCIe Gen4/5, multiple 10 GbE ports, and high-speed camera links (e.g., GMSL2 and CSI-2) to enhance data throughput and enable low-latency operations in industrial automation, smart transportation, and robotics. Modular form factors including COM-HPC, SMARC, and custom carrier board ecosystems are being widely adopted, providing scalability and design flexibility for diverse applications. Emerging trends include support for open instruction set architectures like RISC-V, which enable customizable and energy-efficient computing cores tailored to specific workloads, and the use of advanced thermal solutions that maintain performance under harsh conditions. Embedded boards are also incorporating hardware-level security features such as secure boot, trusted execution environments, and cryptographic accelerators to meet stringent safety and compliance requirements in sectors like aerospace, defense, and medical systems. Additionally, advancements in **software integration—such as containerized AI frameworks and real-time operating systems optimized for mixed-criticality tasks—facilitate easier development and deployment across heterogeneous hardware. With increasing emphasis on AI at the edge, embedded computing boards are evolving into smart nodes capable of autonomous decision-making, distributed analytics, and high-resolution sensor processing, supporting industry transformation across manufacturing, energy, healthcare, and intelligent infrastructure.

• In January 2025, Portwell launched next-generation AIoT edge computing solutions featuring Intel® Core™ Ultra Processors (Series 2), delivering up to 36 TOPS of AI performance and support for DDR5/LPDDR5x memory, PCIe Gen5, Thunderbolt™ 4, and advanced connectivity options to enhance embedded board performance across industrial automation, smart healthcare, and edge AI applications. Source: www.portwell.com

• In December 2025, Advantech unveiled its latest suite of high-performance edge AI compute solutions powered by the Qualcomm Dragonwing IQ-X platform, including AOM-6731, AIMB-293, and SOM-6820 modules with integrated AI acceleration up to 45 TOPS and support for Wi-Fi 7 and 5G connectivity, enabling robust real-time computing for industrial and embedded environments. Source: www.prnewswire.com

• In March 2025, Axiomtek introduced the AIM101 compact fanless edge AI system powered by Intel® Twin Lake N-series processors, designed for rugged industrial edge applications, and showcased its CAPA561 3.5-inch embedded SBC optimized for AI-driven automation and industrial use at key 2025 trade events. Source: www.axiomtek.com

• In November 2025, Advantech expanded its edge AI portfolio by collaborating with Qualcomm Technologies and Edge Impulse to launch AIR-055 and AFE-A503 solutions powered by the Qualcomm Dragonwing IQ-9075 processor delivering up to 100 TOPS of AI performance, tailored for robotics, automation, and large-vision/multimodal AI applications in industrial settings. Source: www.prnewswire.com

The High-Performance Embedded Computing Boards Market Report provides a comprehensive examination of product types, applications, end-users, technologies, and regional dynamics shaping today’s embedded computing landscape. It covers a broad array of form factors, including single-board computers, computer-on-modules (COMs), ruggedized embedded boards, VPX/OpenVPX platforms, and advanced modular architectures designed for harsh environments and high-throughput workloads. The report also analyzes application segments such as industrial automation, aerospace & defense, medical imaging, transportation, and edge AI analytics, providing insights into performance requirements and technology integration trends. It includes end-user profiles encompassing industrial OEMs, defense contractors, healthcare solution providers, and smart infrastructure integrators, highlighting adoption patterns and procurement criteria. Geographic breakdowns detail market dynamics across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, identifying key consumption hubs, technology clusters, and regional innovation drivers. The report further explores emerging technologies such as AI accelerators, heterogeneous computing architectures, RISC-V integration, high-bandwidth I/O interfaces, and embedded security features that influence system design decisions. Additionally, competitive analysis assesses company strategies, product portfolios, partnerships, and ecosystem developments that define competitive positioning. Niche segments, including mission-critical embedded platforms and AI-optimized edge computing solutions, are examined to understand growth vectors and technology convergence trends. Tailored for decision-makers and industry professionals, the report delivers actionable insights into evolving market requirements, technology pipelines, user expectations, and strategic investment opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,850.0 Million |

| Market Revenue (2033) | USD 4,112.2 Million |

| CAGR (2026–2033) | 10.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Advantech; Axiomtek; Kontron; DFI; IEI Integration; Avalue Technology; Emerson Electric; Lanner Electronics; OnLogic; Nexcom International; Beckhoff Automation; MSI Computer; Portwell; Rugged Embedded Systems |

| Customization & Pricing | Available on Request (10% Customization Free) |