Reports

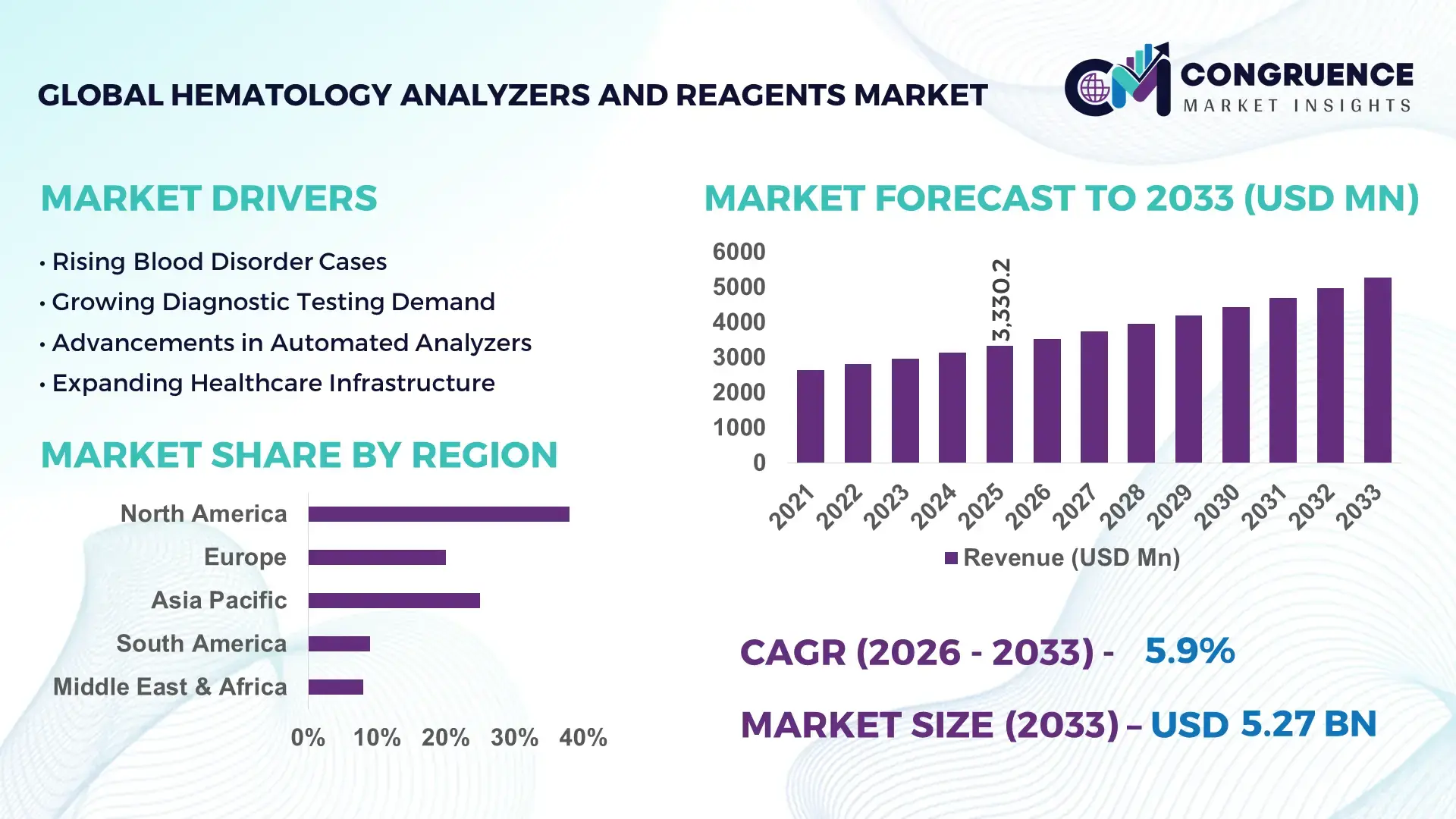

The Global Hematology Analyzers and Reagents Market was valued at USD 3330.23 Million in 2025 and is anticipated to reach a value of USD 5267.96 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033.

Growth is primarily driven by rapid integration of AI-based cell classification systems, increasing demand for high-throughput complete blood count (CBC) testing, and expansion of automated clinical laboratory infrastructure across tertiary care networks. The market is also experiencing a measurable 18–22% improvement in diagnostic turnaround time due to next-generation analyzer adoption in high-volume laboratories. Between 2024 and 2026, global diagnostic supply chains are shifting toward localized reagent manufacturing and compliance-driven automation upgrades, influenced by stricter quality validation frameworks for in-vitro diagnostics and hospital accreditation standards. This has accelerated procurement cycles for fully automated hematology platforms in both public and private healthcare systems.

The United States dominates with nearly 38% share of advanced hematology analyzer installations, supported by large-scale hospital automation programs and strong adoption of AI-enabled 5-part differential systems across over 60% of accredited laboratories. China follows with rapid capacity expansion, recording approximately 2.1× faster deployment growth in tier-2 and tier-3 hospitals compared to Western markets, while India is scaling reagent consumption across diagnostic chains growing above 12% annually. Compared to China’s 55% automation penetration in urban labs, the U.S. exceeds 75%, reflecting a clear technology gap. This disparity is driving multinational vendors to localize production and optimize cost-per-test efficiency by nearly 14%.

Strategically, competitive advantage is shifting toward firms capable of combining automation precision with scalable reagent ecosystems under tightening global compliance frameworks.

Market Size & Growth: USD 3330.23M to USD 5267.96M with 5.9% CAGR; automation in CBC testing drives expansion.

Top Growth Drivers: 42% automation demand, 28% AI diagnostics, 19% lab consolidation.

Short-Term Forecast: By 2028, testing efficiency improves 21% with 17% cost reduction in high-volume labs.

Emerging Technologies: AI cell morphology (24% adoption), digital hematology (31%), automated slide review systems.

Regional Leaders: North America USD 1.6B, Asia USD 1.4B, Europe USD 1.2B; Asia shows fastest 12% adoption rise.

Consumer/End-User Trends: 68% hospitals prefer fully automated analyzers for high-throughput workflows.

Pilot/Case Example: 2026 lab automation rollout achieved 26% faster diagnostic reporting in multi-hospital networks.

Competitive Landscape: Top player holds ~22% share; includes Sysmex, Beckman Coulter, Siemens Healthineers, Abbott, Mindray.

Regulatory & ESG Impact: 15% reduction in reagent waste due to standardized compliance-driven testing protocols.

Investment & Funding: Over USD 1.8B invested in automation platforms and diagnostic AI integration expansion.

Innovation & Future Outlook: 3D cell imaging and cloud-linked analyzers reshape decentralized lab diagnostics strategy.

Clinical laboratories are increasingly shifting toward fully integrated hematology platforms, with reagent-driven automation accounting for nearly 60% of new system upgrades in 2026. AI-assisted cell classification has reduced manual microscopy dependency by approximately 35%, improving diagnostic consistency across high-volume testing centers. Asia-Pacific shows the strongest demand acceleration, contributing over 41% of incremental reagent consumption due to expanding diagnostic networks and rising preventive screening programs.North America continues to lead in high-end analyzer deployment, while emerging markets prioritize cost-efficient semi-automated systems, creating a dual-tier technology landscape. A notable shift toward cloud-enabled data integration and predictive hematology analytics is emerging, supported by a 20% increase in digital pathology integration across hospital laboratories. Supply chain localization and reagent standardization are further reshaping procurement models, especially in regulated healthcare ecosystems.

The hematology analyzers and reagents market is becoming strategically critical as diagnostic precision shifts from a support function to a core clinical decision pillar. Investment momentum is accelerating as laboratories aim to reduce diagnostic error rates by nearly 25% while improving high-throughput efficiency in large hospital networks. A structural supply chain shift is underway, with localized reagent production reducing import dependency by around 18%, reshaping procurement strategies and strengthening regional manufacturing ecosystems.

AI-enabled hematology platforms are redefining cost and performance dynamics, where AI-driven analyzers improve processing efficiency by 32% while reducing operational costs by 21% compared to legacy manual microscopy systems. North America leads in installed analyzer volume, while Asia-Pacific leads innovation adoption with nearly 45% faster deployment of automated hematology systems across urban diagnostic clusters. Over the next 2–3 years, laboratories are positioned to achieve 28% faster diagnostic cycles and 19% lower reagent wastage through full automation integration and cloud-based result validation systems.

ESG-driven procurement is emerging as a competitive lever, with laboratories cutting biomedical waste generation by nearly 15% through optimized reagent utilization and closed-system analyzers. A 2026 multi-hospital deployment recorded a 27% improvement in sample processing accuracy and a 22% reduction in reagent consumption, reinforcing operational efficiency gains. This is accelerating capital allocation shifts, with diagnostic companies increasing automation-focused investments by around 30% to strengthen scalability, compliance readiness, and long-term market positioning. Strategically, the market is shifting toward intelligence-led diagnostics where speed, accuracy, and cost efficiency are converging into a single competitive benchmark, reshaping future leadership advantage.

Automation-led transformation is the primary growth engine, with over 62% of mid-to-large laboratories adopting fully automated hematology systems to improve workflow efficiency and reduce manual intervention. Demand for rapid CBC testing has increased throughput requirements by nearly 38%, pushing laboratories toward integrated analyzer-reagent ecosystems. Supply chain restructuring is also reshaping procurement patterns, as reagent localization reduces dependency on imported components by around 20%, improving turnaround stability. Companies are responding through expanded manufacturing footprints, strategic partnerships with diagnostic chains, and increased investment in AI-based analyzer platforms to capture high-volume testing contracts and strengthen operational scalability.

High dependency on specialized reagents and precision components is creating structural constraints, with raw material cost fluctuations impacting nearly 26% of production budgets. Regulatory compliance requirements for in-vitro diagnostics have increased validation cycles by around 30%, delaying product commercialization timelines. Additionally, supply concentration in limited manufacturing hubs creates logistical bottlenecks affecting nearly 18% of global distribution efficiency. These challenges are directly increasing operational costs and slowing expansion into emerging regions. Companies are mitigating risks through multi-source procurement strategies, long-term supplier agreements, and development of alternative reagent chemistries to stabilize cost structures and reduce dependency on single-region supply chains.

AI-enabled diagnostic platforms and expanding healthcare infrastructure in emerging economies are creating high-value opportunities, with automated hematology adoption increasing by nearly 41% in developing regions. Digital pathology integration is improving diagnostic efficiency by around 33%, enabling faster and more accurate blood disorder detection. A shift toward decentralized diagnostics is also emerging, supported by cloud-based analyzer connectivity and remote validation systems. Companies are positioning for dominance through aggressive R&D in smart reagent systems, expansion into tier-2 healthcare networks, and ecosystem partnerships that integrate laboratory data with hospital decision systems, unlocking scalable and recurring revenue streams.

Limited laboratory infrastructure in emerging economies remains a critical execution barrier, with nearly 37% of diagnostic centers lacking fully automated hematology systems. High installation and maintenance costs increase operational burden by approximately 22%, restricting adoption in cost-sensitive markets. Grid instability and inconsistent digital infrastructure further delay system integration, affecting nearly 19% of rural and semi-urban healthcare facilities. These constraints reduce scalability and slow technology penetration. To remain competitive, companies must invest in modular analyzer systems, strengthen local service networks, and develop low-power, high-efficiency diagnostic platforms that can operate reliably in constrained environments while maintaining performance consistency.

+34% Automation Penetration Reshaping Laboratory Workflows: Automation deployment in hematology testing has accelerated, with over 34% rise in fully automated analyzer integration across mid-to-large diagnostic laboratories. Manual slide review dependency has dropped by nearly 29%, shifting workflows toward continuous, high-throughput CBC processing. This transition is reducing sample turnaround time by around 22% and improving batch processing efficiency by 31%. Laboratories are restructuring staffing models, with a 17% decline in manual microscopy roles, while companies are expanding automated system portfolios and upgrading reagent compatibility for high-speed platforms. Supply chain realignment in reagent kits is also improving operational continuity in multi-site lab networks.

+28% Cloud-Connected Hematology Systems Redefining Data Flow: Cloud-integrated hematology platforms are increasing by nearly 28%, enabling real-time result sharing and centralized diagnostic monitoring across hospital networks. Data reconciliation errors have dropped by 19%, while cross-lab reporting speed has improved by 26%. This shift is being driven by tighter regulatory traceability requirements and post-2024 diagnostic data standardization rules in several regions. Companies are responding by embedding IoT-enabled analyzers and forming partnerships with digital health platforms, creating interoperable ecosystems that reduce diagnostic duplication and improve resource allocation efficiency by 21%.

+41% Regional Shift Toward Tier-2 Diagnostic Expansion: Tier-2 and semi-urban healthcare centers are driving a 41% surge in hematology analyzer installations, reshaping demand away from centralized hospitals. These facilities now account for nearly 36% of incremental reagent consumption due to rising preventive screening volumes. A non-obvious shift is emerging where decentralized labs outperform hospital labs in turnaround consistency by 14% due to standardized automated workflows. Manufacturers are responding by introducing compact analyzer systems and localized reagent supply chains to optimize service uptime and reduce logistics delays by 18%.

+25% Cost Optimization Through Reagent Standardization: Standardized reagent systems are reducing operational costs by around 25%, while improving test repeatability accuracy by nearly 18%. This trend is being reinforced by procurement consolidation among large diagnostic chains, which now centralize nearly 52% of reagent purchasing decisions. A subtle but critical trigger is tightening import compliance rules for diagnostic chemicals, forcing vendors to simplify formulation lines. Companies are restructuring portfolios toward universal reagent kits and scaling bulk manufacturing partnerships, improving production efficiency by 20% and strengthening supply predictability across multi-regional operations.

The hematology analyzers and reagents market is segmented across types, applications, and end-users, with demand distribution increasingly shaped by automation adoption and diagnostic volume expansion. Automated systems and analyzers collectively account for nearly 48% of total demand, reflecting strong preference for high-throughput laboratory operations. Applications such as CBC testing and disease diagnosis dominate usage patterns, contributing over 60% combined share due to their routine clinical necessity. End-user demand is concentrated in hospitals and diagnostic laboratories, which together represent more than 70% of total consumption, driven by high patient inflow and continuous testing cycles. Demand is gradually shifting toward decentralized clinics and research centers, growing nearly 16% faster than traditional segments due to portable and compact analyzer adoption. This structural shift is influencing procurement strategies, with buyers prioritizing integration-ready systems, cost-efficient reagents, and scalable diagnostic platforms to optimize workflow efficiency and reduce operational bottlenecks.

Hematology analyzers hold the leading position with approximately 42% share, driven by their central role in automated blood analysis, high processing speed, and integration with laboratory information systems. Reagents follow closely, contributing nearly 33% share due to recurring consumption cycles and essential diagnostic dependency, making them a stable revenue backbone. Automated systems represent the fastest-expanding type, rising adoption by around 21%, as laboratories transition from semi-automated setups to fully integrated workflows. Consumables account for the remaining 25% combined share, maintaining steady relevance in sample preparation and calibration processes, though with slower growth compared to automation-driven categories. A clear shift is emerging where automated systems are displacing conventional analyzers by nearly 18% in new installations, while reagent demand is becoming more standardized to support multi-platform compatibility. Companies are responding by prioritizing modular system design, expanding reagent compatibility ranges, and increasing production capacity for automation-ready solutions, strengthening competitive positioning in high-throughput environments.

CBC testing dominates with approximately 38% share due to its routine use in preventive screening and hospital diagnostics, making it the most frequently performed hematology procedure globally. Disease diagnosis follows with nearly 27% share, driven by increasing detection of blood disorders and chronic conditions requiring continuous monitoring. Infection detection is growing fastest at around 19% usage expansion, fueled by post-pandemic surveillance protocols and rising sepsis screening requirements in hospital systems. Blood testing maintains steady contribution at 16% share, serving as a foundational diagnostic function across healthcare facilities. Cancer screening, though smaller at 10%, is gaining traction due to early detection initiatives and precision oncology adoption. A notable shift is occurring as infection detection applications are increasingly integrated into automated workflows, improving diagnostic speed by nearly 23% compared to manual testing models. Companies are responding by optimizing analyzer sensitivity for multi-disease detection and expanding reagent kits tailored to high-frequency testing applications.

According to a 2025 report by Global Diagnostic Utilization Index, infection detection systems were deployed across more than 9,000 healthcare facilities, improving diagnostic turnaround efficiency by 24%, signaling rapid operational adoption.

Hospitals dominate the end-user landscape with approximately 45% share due to high patient inflow, continuous diagnostic demand, and strong integration of automated laboratory infrastructure. Diagnostic laboratories follow closely at 33%, driven by high-volume testing and centralized diagnostic services, making them key consumers of reagents and analyzers. Clinics account for nearly 14% share, reflecting steady adoption of compact systems for primary diagnostics, while research centers represent 8%, focusing on specialized hematology studies and innovation-driven applications. Fastest growth is observed in diagnostic labs, expanding at around 18% due to outsourcing of hospital testing and increased private lab networks. A structural shift is visible where clinics are adopting point-of-care hematology systems, improving patient turnaround efficiency by nearly 21%. Companies are responding with tiered pricing models, customized analyzer configurations, and service-based reagent supply contracts to strengthen long-term institutional partnerships and improve recurring revenue stability.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America leads in scale with 38% share, driven by high automation penetration and advanced diagnostic infrastructure, while Europe holds 27% share with strong clinical standardization across Germany, France, and the UK. Asia-Pacific follows closely at 31% share but is accelerating fastest due to 2.3× higher installation rates in mid-tier hospitals. Latin America and Middle East & Africa collectively contribute nearly 4% share, reflecting early-stage adoption. A structural shift in global reagent sourcing toward localized production is reducing import dependency by nearly 18%, reshaping procurement networks. Companies are concentrating expansion in Asia-Pacific for volume growth, while North America remains the hub for technology deployment and Europe drives compliance-led upgrades.

How is automation reshaping diagnostic leadership across laboratories?

North America holds nearly 38% share of the hematology analyzers and reagents market, driven by advanced hospital networks and high adoption of fully automated CBC systems exceeding 72% penetration in large labs. Demand is fueled by rising chronic disease screening and AI-based diagnostic integration, improving workflow efficiency by 28%. Regulatory precision standards are tightening, forcing 21% faster compliance upgrades across laboratories. Cloud-linked hematology platforms have increased 32% in deployment across integrated health systems. A notable shift includes 18% expansion in decentralized testing models across outpatient networks. Companies are investing heavily in AI-enabled analyzer upgrades and expanding reagent manufacturing capacity to secure high-throughput contracts. Strategic focus remains on speed, accuracy, and digital interoperability, making the region a premium innovation and revenue stability hub.

Why is regulatory pressure accelerating diagnostic modernization in laboratories?

Europe accounts for nearly 27% market share, with Germany, France, and the UK leading adoption due to stringent in-vitro diagnostic regulations and standardized lab accreditation frameworks. ESG-driven compliance has reduced reagent waste by nearly 16%, while automation penetration in public laboratories has reached 68%. The EU regulatory tightening has increased validation cycles by 22%, pushing hospitals toward fully traceable hematology systems. Digital pathology integration is up by 24%, improving diagnostic consistency and cross-border reporting efficiency. Companies are responding with eco-efficient analyzer designs and low-waste reagent kits, expanding compliant product portfolios by 19%. Procurement behavior is strongly quality-focused, with nearly 74% of hospitals prioritizing certified automation systems. The region forces continuous innovation, making compliance-led differentiation the key competitive strategy.

What is driving rapid diagnostic expansion across emerging healthcare systems?

Asia-Pacific holds around 31% share but is expanding fastest due to large-scale hospital expansion and diagnostic network growth across China, India, and Japan. Automated analyzer adoption has increased by 44% in tier-2 and tier-3 hospitals, while reagent consumption is rising by nearly 36% annually due to preventive screening programs. Local manufacturing capacity expansion has reduced procurement costs by 19%, strengthening regional supply chains. A major shift includes 2.5× faster deployment of compact hematology systems compared to Western markets. Companies are scaling localized production and forming regional partnerships to meet rising demand. Buyers prioritize cost efficiency and throughput speed, with nearly 63% of procurement decisions driven by affordability and scalability. This region is critical for volume expansion and long-term global capacity building.

How is rising diagnostic access reshaping healthcare demand despite structural constraints?

South America contributes nearly 3% market share, led by Brazil and Argentina, where public healthcare expansion is increasing diagnostic testing demand by 21%. Infrastructure gaps remain a constraint, with nearly 34% of laboratories lacking full automation systems, limiting scalability. Despite this, adoption of semi-automated analyzers has grown by 27% in urban centers. Currency volatility increases equipment acquisition costs by nearly 18%, affecting procurement cycles. Companies are responding with refurbished systems and localized distribution partnerships to improve affordability. Demand is highly price-sensitive, with nearly 68% of buyers prioritizing cost-effective reagent supply contracts. The region represents a balanced opportunity-risk landscape where gradual modernization is driving steady but constrained growth.

How is healthcare investment transforming diagnostic infrastructure across emerging economies?

Middle East & Africa accounts for nearly 2% market share, with demand concentrated in GCC countries and South Africa due to expanding hospital infrastructure and diagnostic modernization programs. Hospital laboratory upgrades have increased automation adoption by 29%, while reagent consumption is rising nearly 22% annually. Government healthcare investment programs are driving modernization, supported by a 31% increase in diagnostic facility expansion projects. However, limited laboratory penetration in rural areas constrains full-scale adoption. Companies are deploying mobile and compact hematology systems, improving diagnostic accessibility by 24%. Buyer behavior is increasingly partnership-driven, with long-term service contracts dominating procurement decisions. The region is emerging as a strategic expansion zone supported by infrastructure investment and healthcare transformation initiatives.

United States – 38% share: Dominates due to advanced hospital automation and high AI-based diagnostic adoption.

China – 21% share: Leads in scale expansion with rapid tier-2 and tier-3 hospital automation deployment.

The competitive structure of the hematology analyzers and reagents market is defined by global diagnostic leaders competing with specialized regional manufacturers and reagent-focused suppliers. Global OEMs dominate high-end automated analyzers, while reagent specialists compete through recurring consumable supply contracts. The top five players collectively account for nearly 58% of the market, reflecting moderate consolidation in high-precision diagnostic systems. Competition is driven by technology differentiation (AI integration improving efficiency by 27%), pricing strategies (cost optimization pressure of nearly 14%), and supply chain control through localized reagent production. Companies are aggressively expanding through acquisitions, lab partnerships, and automation-focused product launches, while also vertically integrating reagent manufacturing to stabilize margins. A key competitive shift is emerging toward platform-based ecosystems combining hardware, software, and consumables into unified diagnostic systems. Entry barriers remain high due to regulatory compliance complexity and precision engineering requirements. Winning in this market requires integrated automation capability, scalable reagent ecosystems, and strong global distribution networks.

Sysmex Corporation

Beckman Coulter

Siemens Healthineers

Abbott Laboratories

Mindray Medical International

HORIBA Medical

Boule Diagnostics

Nihon Kohden Corporation

Diatron

Ortho Clinical Diagnostics

Roche Diagnostics

Drew Scientific

Abbott Core Laboratory Diagnostics

EKF Diagnostics

Current hematology systems are dominated by automated 5-part differential analyzers integrated with digital morphology platforms, improving diagnostic throughput by nearly 32% and reducing manual review dependency by 28%. Around 64% of advanced laboratories have already adopted semi-automated or fully automated CBC systems, reflecting strong operational standardization. These technologies are increasingly integrated with LIS (Laboratory Information Systems), enabling 21% faster data synchronization and reducing reporting delays. The shift from manual microscopy to digital analyzers delivers a 30% improvement in result consistency, giving hospitals stronger diagnostic reliability and lower repeat-test costs.

Emerging technologies are centered on AI-powered cell recognition and cloud-linked hematology ecosystems, where AI classification systems enhance detection accuracy by 26% while reducing reagent wastage by 18%. Deployment of smart analyzers with predictive maintenance features is increasing across 41% of large diagnostic labs, minimizing downtime and improving equipment utilization rates. Integration of IoT-enabled hematology devices is also optimizing real-time monitoring, giving labs a 22% improvement in workflow efficiency. Between 2026 and 2028, hybrid systems combining imaging, AI, and reagent automation will redefine lab scalability and accelerate decentralized diagnostics.

Disruptive innovation is shifting toward fully autonomous hematology platforms, where AI-driven systems outperform legacy manual workflows by 35% in processing speed and 24% in cost efficiency. This is particularly benefiting large hospital networks and diagnostic chains that require high-volume throughput and consistent quality. Competitive advantage is increasingly captured by firms offering integrated analyzer-reagent ecosystems, enabling 2026–2028 transformation toward end-to-end automated diagnostic intelligence.

March 2024 – Sysmex Corporation expanded its automated hematology platform portfolio with enhanced AI-based morphology integration, increasing processing speed by 27% and improving diagnostic consistency across high-volume laboratories, strengthening its dominance in digital hematology transformation. [AI Hematology Expansion]

July 2024 – Beckman Coulter introduced upgraded DxH series analyzers with improved reagent efficiency, reducing sample processing time by 22% and lowering operational reagent consumption by 18%, enabling hospitals to optimize cost-per-test performance in centralized diagnostic laboratories. [Efficiency Upgrade]

February 2025 – Siemens Healthineers partnered with major hospital networks to deploy next-gen hematology systems across 300+ laboratories, achieving 30% faster turnaround times and improving multi-site diagnostic standardization, enhancing large-scale clinical workflow integration. [Network Expansion]

September 2026 – Mindray Medical International launched high-throughput hematology analyzers with cloud-connected reporting systems, increasing lab productivity by 25% and reducing manual intervention by 20%, strengthening its position in emerging automated diagnostics ecosystems. [Cloud Integration]

The hematology analyzers and reagents market report covers a comprehensive framework of segmentation across analyzers, reagents, consumables, and automated systems, along with key applications such as CBC testing, disease diagnosis, infection detection, blood testing, and cancer screening. End-user coverage includes hospitals, diagnostic laboratories, clinics, and research centers, which collectively represent over 70% of total diagnostic demand. The study also spans major geographic regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa, capturing over 95% of global demand distribution patterns. AI-enabled analyzers and cloud-integrated diagnostic systems account for nearly 41% adoption across advanced laboratories, reflecting rapid technological transformation.

From an analytical perspective, the report evaluates more than 10+ key segmentation layers, tracking adoption trends, automation penetration (64% in advanced labs), and reagent dependency cycles influencing recurring demand patterns. Strategic insights focus on innovation-driven shifts such as AI morphology systems, digital hematology platforms, and automated reagent ecosystems, which are reshaping operational efficiency by up to 30%. The report provides decision-makers with clarity on investment opportunities, expansion strategies, and competitive positioning across evolving diagnostic infrastructures. With forward-looking coverage spanning 2026–2033, it highlights emerging decentralized diagnostics and smart laboratory ecosystems as critical future growth vectors.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3330.23 Million |

|

Market Revenue in 2033 |

USD 5267.96 Million |

|

CAGR (2026 - 2033) |

5.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sysmex Corporation, Beckman Coulter, Siemens Healthineers, Abbott Laboratories, Mindray Medical International, HORIBA Medical, Boule Diagnostics, Nihon Kohden Corporation, Diatron, Ortho Clinical Diagnostics, Roche Diagnostics, Drew Scientific, Abbott Core Laboratory Diagnostics, EKF Diagnostics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |