Reports

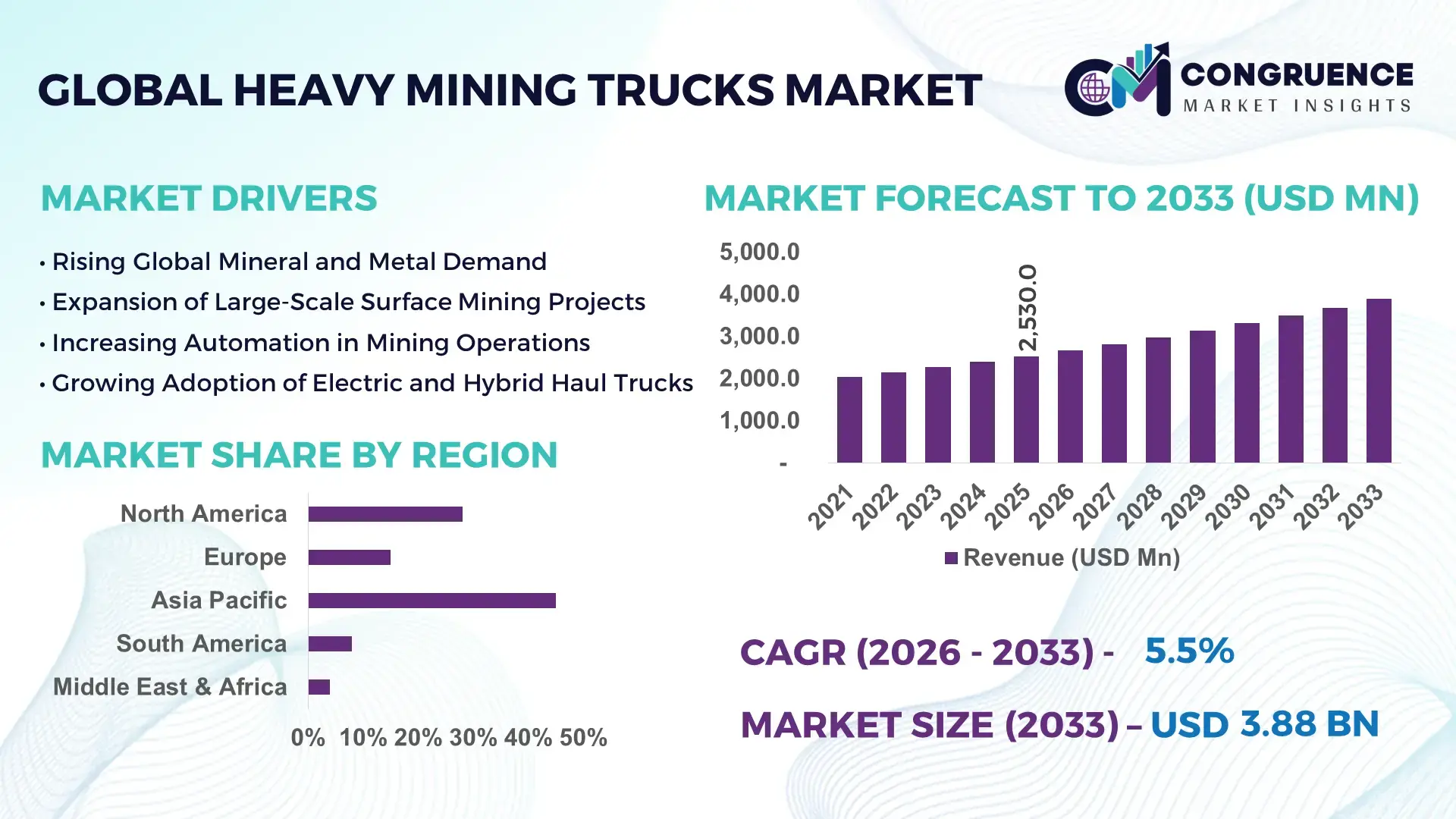

The Global Heavy Mining Trucks Market was valued at USD 2,530.0 Million in 2025 and is anticipated to reach a value of USD 3,882.8 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by rising large-scale surface mining operations, increasing mineral output requirements, and accelerated fleet modernization across major mining economies.

China dominates the global Heavy Mining Trucks marketplace in terms of industrial scale and operational deployment. The country operates more than 3,000 large open-pit mines, with annual coal production exceeding 4.6 billion metric tons, creating sustained demand for ultra-class haul trucks above 190 metric tons. Domestic manufacturers have expanded production capacities, with localized assembly lines capable of producing over 1,200 heavy mining trucks annually. Public and private mining investments exceeded USD 120 billion in recent years, supporting automation-ready fleets, electric drive systems, and autonomous haulage pilots. Adoption of GPS-enabled dispatch systems now covers nearly 65% of large mining fleets, improving utilization rates and lowering idle time across iron ore, coal, and rare earth mining operations.

Market Size & Growth: Valued at USD 2.53 billion in 2025, projected to reach USD 3.88 billion by 2033, growing at 5.5% CAGR due to increased open-pit mining depth and higher payload efficiency demand.

Top Growth Drivers: Surface mining expansion 42%, fleet automation adoption 36%, fuel-efficiency optimization 29%.

Short-Term Forecast: By 2028, autonomous haulage is expected to reduce operating costs by approximately 18%.

Emerging Technologies: Autonomous haulage systems, electric drive mining trucks, AI-based fleet optimization platforms.

Regional Leaders: Asia Pacific USD 1.62 billion by 2033 with electrification focus; North America USD 1.05 billion with autonomous adoption; Australia USD 0.58 billion driven by iron ore mining.

Consumer/End-User Trends: Mining operators increasingly favor high-capacity trucks above 220 tons for reduced haul cycles and labor dependency.

Pilot or Case Example: In 2024, an autonomous haul pilot in Western Australia improved fleet productivity by 21%.

Competitive Landscape: Caterpillar holds approximately 28% share, followed by Komatsu, Hitachi, Liebherr, and XCMG.

Regulatory & ESG Impact: Emission compliance standards are accelerating adoption of electric and hybrid haul trucks.

Investment & Funding Patterns: Over USD 6.8 billion invested globally in mining fleet electrification and automation programs.

Innovation & Future Outlook: Integration of AI dispatch systems and battery-powered ultra-class trucks will redefine operational efficiency.

Heavy Mining Trucks are critical across coal, iron ore, copper, and bauxite mining, with surface mining accounting for nearly 72% of equipment usage. Recent innovations include 300-ton electric-drive trucks and real-time payload monitoring systems. Stricter emission regulations, rising diesel costs, and increased automation investment are reshaping regional demand, particularly in Asia Pacific and Australia, while long-term outlook favors low-emission, autonomous-ready fleets.

The Heavy Mining Trucks Market plays a strategic role in ensuring raw material security for energy, infrastructure, and industrial manufacturing sectors. As global mineral extraction volumes increase, mining operators are prioritizing productivity per haul cycle, safety, and cost optimization. Autonomous haulage systems deliver nearly 20% efficiency improvement compared to conventional manned trucks by reducing idle time, optimizing routes, and minimizing human error. Asia Pacific dominates in haul truck deployment volume, while North America leads in automation adoption with over 48% of large mining enterprises integrating semi-autonomous or fully autonomous fleets.

By 2028, AI-enabled fleet management is expected to reduce fuel consumption by approximately 15% while improving asset utilization by 22%. ESG commitments are driving firms to target up to 30% emission reduction by 2030 through electrification, alternative fuels, and regenerative braking systems. In 2024, Australia achieved a 19% reduction in haulage downtime through autonomous fleet expansion across iron ore operations. The Heavy Mining Trucks Market is increasingly positioned as a pillar of operational resilience, regulatory compliance, and sustainable mining growth.

The Heavy Mining Trucks Market is shaped by increasing surface mining intensity, deeper pit designs, and rising demand for high-payload vehicles. Fleet digitization, autonomous technologies, and electrification are transforming operational models, while capital-intensive procurement cycles influence replacement demand. Mining companies are consolidating fleets to reduce maintenance complexity and improve fuel efficiency. The market is also influenced by commodity price volatility, labor shortages, and regional mining regulations, which collectively shape investment decisions and equipment specifications.

Expanding open-pit mining operations have increased demand for ultra-class haul trucks capable of moving over 200 tons per cycle. Global surface mining accounts for nearly 80% of total mineral output, requiring high-capacity trucks to manage longer haul distances and higher overburden volumes. Productivity improvements of up to 25% have been reported when replacing mid-class trucks with ultra-class fleets, directly supporting market expansion.

Heavy mining trucks require substantial upfront investment, often exceeding USD 5 million per unit. Maintenance, tire replacement, and fuel expenses contribute to high total cost of ownership. Smaller mining operators face financing challenges, while extended equipment lifecycles delay replacement cycles, limiting short-term demand growth despite rising mining activity.

Electric and hybrid haul trucks offer up to 40% lower energy costs and significant emission reductions. Battery-powered prototypes have demonstrated 18–22% energy recovery through regenerative braking. As charging infrastructure expands at mine sites, electrification presents strong long-term growth opportunities.

Advanced haul trucks require skilled technicians, software integration, and data-driven maintenance strategies. Over 35% of mining firms report workforce skill gaps in autonomous fleet management. Cybersecurity risks and system interoperability issues further complicate deployment, slowing adoption in developing mining regions.

Rapid Adoption of Autonomous Haulage Systems: Autonomous trucks now operate across more than 70 large mining sites globally, improving haul cycle efficiency by 20% and reducing safety incidents by nearly 30%.

Shift Toward Electric Drive and Hybrid Trucks: Electric-drive trucks account for approximately 38% of new fleet additions, delivering fuel savings of up to 25% and lowering emission intensity per ton hauled.

Increasing Demand for Ultra-Class Trucks: Trucks above 220-ton capacity represent nearly 46% of new procurements, enabling fewer trips and reduced labor dependency across large open-pit mines.

Integration of Digital Fleet Analytics: Over 60% of mining operators use real-time fleet analytics, achieving maintenance cost reductions of around 17% and improving equipment availability rates above 90%.

The Heavy Mining Trucks Market is structured around distinct equipment types, operational applications, and end-user industries that together determine procurement patterns, fleet strategies, and technology adoption. By type, differentiation is largely driven by payload capacity, propulsion architecture, and automation readiness, with ultra-class trucks dominating large-scale surface mining while smaller rigid trucks serve medium-depth operations and ancillary logistics. Application-wise, surface mining remains the core demand center due to longer haul distances, higher stripping ratios, and continuous production cycles, whereas underground mining and construction-related hauling represent more specialized but growing niches. From an end-user perspective, the market is concentrated among large mining companies, followed by contractors and equipment leasing firms that support project-based operations. Fleet replacement cycles, regulatory pressures on emissions, and rising automation investments vary across segments, shaping how different users prioritize payload efficiency, reliability, and digital integration.

Heavy mining trucks are broadly categorized into ultra-class (above 220 tons), large-class (150–220 tons), mid-class (100–150 tons), and smaller rigid haul trucks (below 100 tons). Ultra-class trucks lead the market, accounting for roughly 48% of installations because they reduce haul cycles, lower per-ton operating costs, and perform best in deep open-pit mines where distances regularly exceed 5–8 kilometers.

Large-class trucks currently hold about 27% of demand, favored by mines that need high capacity but face space or ramp constraints unsuitable for ultra-class units. Mid-class trucks represent approximately 15% of the market and are widely used in expanding mines in Southeast Asia, Latin America, and parts of Africa where pit geometry limits very large vehicles. Smaller rigid trucks collectively make up the remaining 10%, serving auxiliary hauling, waste removal, and construction-linked mining projects.

The fastest-growing type is electric-drive and battery-assisted ultra-class trucks, expanding at around 7% annually as operators prioritize fuel savings, lower emissions, and compatibility with autonomous systems. Growth is being driven by regenerative braking, declining battery costs, and mine-site charging investments. Conventional diesel-mechanical trucks remain important for remote sites with limited power infrastructure, while hybrid models are gaining niche traction in transitional fleets.

• In 2024, Rio Tinto deployed battery-assisted ultra-class haul trucks at its Pilbara iron ore operations, demonstrating measurable reductions in diesel use during downhill hauling cycles.

Surface mining is the dominant application, representing about 55% of total usage because large open pits require continuous high-volume material movement, long-haul operations, and equipment capable of carrying 200+ tons per trip.

Underground mining accounts for roughly 22% of demand, relying more on smaller rigid trucks and specialized low-profile vehicles that can navigate confined tunnels. Construction and quarrying applications together contribute around 13%, where haul trucks support aggregate movement, overburden removal, and large infrastructure projects. The remaining 10% comes from port logistics, mine-to-plant transport, and industrial material handling.

The fastest-growing application is autonomous surface mining logistics, rising at about 8% annually, driven by labor shortages, safety requirements, and productivity gains from AI-based dispatch systems.

Consumer and enterprise trends also reflect rising digital integration: in 2025, about 41% of major mining firms reported piloting autonomous or semi-autonomous haul systems, and nearly 58% of large operators now require real-time fleet analytics before approving new equipment purchases.

• In 2024, a large copper mine in Chile integrated AI-based dispatching across its surface fleet, cutting truck idle time by more than 20% during peak production hours.

Large mining companies are the leading end-user group, representing about 52% of total market usage because they operate the deepest pits, run the largest fleets, and have the capital to invest in automation and electrification.

Mining contractors and equipment service providers account for roughly 21%, supplying flexible fleets for short-term projects, seasonal peaks, and contract mining operations. Equipment leasing firms contribute about 12%, enabling mid-tier miners to access ultra-class trucks without full ownership. The remaining 15% is split among construction firms, government-owned mining entities, and industrial material handlers.

The fastest-growing end-user segment is contract mining operators, expanding at around 7% annually as resource companies increasingly outsource non-core hauling to specialized firms with autonomous-ready fleets.

Adoption trends show that in 2025, nearly 45% of large mining enterprises had at least one autonomous truck in operation, while 62% of new fleet tenders included digital telemetry and predictive maintenance requirements.

• In 2024, BHP expanded autonomous haulage across multiple Australian sites, reporting safer operations and higher fleet availability during extreme weather conditions.

Asia-Pacific accounted for the largest market share at 45% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

The global Heavy Mining Trucks Market is characterized by strong regional differentiation driven by mining intensity, automation readiness, infrastructure maturity, and regulatory frameworks. Asia-Pacific leads in fleet deployment volume due to large-scale coal, iron ore, and critical mineral extraction in China, Australia, and India, collectively operating more than 4,500 large surface mines. North America ranks second with approximately 28% market share, supported by automation pilots across copper, lithium, and gold mines, alongside expanding electric-drive truck adoption. Europe holds around 15% share, shaped by stringent emission standards and a shift toward low-carbon mining equipment, particularly in Sweden, Germany, and Finland. South America contributes about 8% of demand, led by Chile and Brazil’s copper and iron ore operations, while the Middle East & Africa accounts for roughly 4%, driven by expanding mining activity in South Africa, Ghana, and the UAE.

North America represents roughly 28% of global Heavy Mining Trucks deployment, with particularly strong penetration of autonomous and semi-autonomous fleets in the U.S. and Canada. Copper, gold, lithium, and oil sands mining are the core demand drivers, with several sites operating fleets exceeding 150 haul trucks each. Federal and provincial policies promoting electrification, cleaner diesel standards, and mine safety automation have accelerated investment in electric-drive and hybrid models. Real-time telemetry, AI-based dispatching, and predictive maintenance platforms are now integrated across more than 60% of large mines in the region. Local equipment integrators are partnering with software firms to retrofit legacy trucks with autonomous kits rather than replacing entire fleets, reducing capital burden while modernizing operations. Regional enterprises also show higher digital adoption compared to other markets—over 55% of North American mining firms report using cloud-based fleet analytics, reflecting a consumer behavior pattern that prioritizes data-driven decision-making and risk mitigation in heavy equipment procurement.

Europe accounts for approximately 15% of global Heavy Mining Trucks usage, concentrated in Sweden, Germany, France, Finland, and Poland. The region’s mining demand is anchored in iron ore, nickel, and battery minerals, with strong government backing for low-emission industrial equipment. Regulatory frameworks such as the EU Green Deal and Fit for 55 have pushed operators to replace diesel fleets with electric or hybrid trucks, accelerating pilot programs at several large sites. Scandinavian mines are leading in autonomous trials, integrating underground-to-surface logistics with fully digitalized control rooms. Local manufacturers are investing in modular electric drivetrains that can be retrofitted onto existing trucks, reducing waste and extending equipment lifecycles. Consumer behavior in Europe is heavily shaped by regulation—procurement teams prioritize explainability, lifecycle emissions, and traceability, often selecting suppliers that provide transparent carbon accounting alongside equipment performance metrics.

Asia-Pacific is the highest-volume market for Heavy Mining Trucks, led by China, Australia, and India. China alone operates thousands of ultra-class trucks across coal and rare earth mines, supported by extensive domestic manufacturing capacity that produces more than 1,200 heavy trucks annually. Australia’s iron ore sector relies on some of the world’s largest autonomous fleets, with multiple sites running over 200 driverless trucks each. India’s expanding coal and critical mineral extraction is boosting demand for mid- and large-class trucks, alongside new infrastructure corridors that improve mine-to-port logistics. The region is also a hub for innovation, with Japanese and Chinese firms developing battery-assisted haul trucks and advanced regenerative braking systems. Regional consumer behavior reflects rapid digital adoption—growth is increasingly tied to e-commerce supply chains for metals and mobile-based AI fleet monitoring tools that allow remote oversight of equipment performance across dispersed mine sites.

South America holds roughly 8% of the global Heavy Mining Trucks Market, with Chile and Brazil as the dominant contributors. Chile’s large copper mines operate some of the deepest open pits in the world, requiring ultra-class trucks capable of long-haul performance and high payload stability. Brazil’s iron ore sector continues to modernize fleets with higher-capacity vehicles and digital maintenance platforms to reduce downtime. Governments in both countries are offering tax incentives for cleaner mining technologies and regional manufacturing partnerships, particularly for electric-drive trucks. Improved rail and port infrastructure is also reshaping haul routes, influencing truck specifications and fleet sizing. Regional consumer behavior is closely linked to media and language localization—mining firms increasingly demand Spanish- and Portuguese-enabled digital dashboards, training modules, and AI systems for workforce adoption.

The Middle East & Africa represents about 4% of global demand, with growth concentrated in South Africa, UAE, Saudi Arabia, and Ghana. South Africa’s platinum and coal operations remain major equipment users, while the UAE and Saudi Arabia are expanding non-oil mining and construction-related mineral extraction. Regional modernization efforts include smart mine control centers, satellite-based truck tracking, and remote diagnostics to manage harsh desert conditions. Trade partnerships and local content policies are encouraging equipment assembly and maintenance hubs within the region. Governments are also promoting cleaner mining practices, pushing operators toward hybrid and electric solutions where grid infrastructure permits. Consumer behavior varies—large state-backed projects emphasize reliability and localization, while private contractors prioritize flexible leasing and modular fleet configurations for short-term projects.

China – 32% Market Share: Massive domestic mining scale, strong local manufacturing capacity, and widespread digital fleet deployment.

Australia – 18% Market Share: World-leading autonomous iron ore operations and advanced electrification pilots across major mines.

The Heavy Mining Trucks Market exhibits a moderately consolidated competitive structure, where five global OEMs control roughly 65–70% of total installed fleets worldwide, while the remaining share is fragmented across regional and specialty manufacturers. Around 25–30 active manufacturers supply heavy haulage solutions, ranging from ultra-class trucks to autonomous-ready platforms and electric-drive models. Competition centers on payload capacity, total cost of ownership, automation compatibility, and lifecycle service contracts rather than price alone.

Leading players are aggressively investing in autonomous haulage systems (AHS), electrification, and digital mine integration, with more than 120 mines globally now operating some form of autonomous or semi-autonomous trucks. Strategic partnerships with mining majors (BHP, Rio Tinto, Fortescue, Vale) have become the dominant route to scale deployment, while retrofit programs are gaining traction—over 35% of new automation projects in 2024–2025 involved upgrading existing fleets rather than purchasing new trucks.

Product launches are increasingly focused on battery-assisted and trolley-assist trucks, with at least 10 commercial electric or hybrid mining truck models announced since 2023. M&A activity remains selective, primarily targeting software, AI dispatch firms, and sensor companies rather than traditional equipment makers. After-sales services, predictive maintenance, and long-term uptime guarantees have become a key differentiator, with top firms now deriving nearly 25–30% of profitability from services rather than equipment sales.

Hitachi Construction Machinery Co., Ltd.

BelAZ (Belarusian Automobile Plant)

SANY Heavy Industry

XCMG Group

Zoomlion Heavy Industry

Volvo Construction Equipment

Sandvik Mining and Rock Solutions

Epiroc AB

Terex Corporation

Doosan Bobcat (Doosan Infracore legacy mining trucks)

Scania Mining Vehicles

Nikola Corporation (mining-focused pilots)

BYD Heavy Industries

Technological transformation in the Heavy Mining Trucks Market is being driven by automation, electrification, digitalization, and materials innovation. Autonomous haulage systems (AHS) now operate across more than 70 large mining sites globally, with real-time AI dispatch platforms optimizing routes, reducing idle time by up to 20–25%, and lowering collision risks by nearly 30%. Modern trucks are increasingly integrated with LiDAR, radar, computer vision, and satellite positioning systems that enable centimeter-level navigation accuracy in harsh environments.

Electrification is advancing rapidly. Electric-drive mining trucks represent approximately 38–40% of new large-class procurements, supported by regenerative braking systems that recover 15–22% of energy during downhill cycles. Battery-assisted and trolley-assist technologies are gaining traction in deep pits, cutting diesel consumption by 25–35% in some operations. Mine-site charging infrastructure is expanding, with fast-charging stations capable of replenishing large battery packs within 45–90 minutes.

Digital twins and predictive maintenance are reshaping fleet management. More than 60% of major mining operators now use cloud-based analytics platforms that monitor tire wear, drivetrain health, and payload stability in real time, improving equipment availability to above 90% in leading sites. Advanced composite materials and high-strength steel alloys are reducing truck weight by 8–12% without compromising payload capacity, improving fuel efficiency and structural durability.

Remote operations centers are also proliferating. Several mining regions now control entire fleets from centralized hubs hundreds of kilometers away, reducing on-site staffing by 20–30%. Cybersecurity and secure connectivity have become critical, with encrypted vehicle-to-mine networks now standard across top-tier operations. Over the next decade, software-defined mining trucks—where performance upgrades are delivered via digital updates—are expected to become mainstream, making Heavy Mining Trucks a core pillar of smart, sustainable mining ecosystems.

• In September 2024, Caterpillar announced a modular Cat® 793 large mining truck platform designed for diesel mechanical, diesel-electric, and battery-electric powertrains, enhancing flexibility for mine operators transitioning toward lower emissions and integrated fleet solutions. Source: www.cat.com

• In April 2025, Liebherr showcased its autonomous battery-electric T 264 mining truck (240 t) and the R 9400 E electric excavator at Bauma, equipped for static and dynamic charging and featuring advanced AHS integration entering field validation in 2025. Source: www.liebherr.com

• In September 2024, the companies confirmed deployment of approximately 360 autonomous battery-electric T 264 trucks supported by Fortescue’s 6 MW fast charging tech and expanding remote service capabilities for large-scale decarbonised haulage. Source: www.liebherr.com

• In 2024, Liebherr and Fortescue reached a milestone with the hydrogen-powered T 264 prototype “Europa” operating using fuel cell and battery power, advancing zero-emission haul truck technology toward future field trials. Source: www.liebherr.com

The Heavy Mining Trucks Market Report provides a comprehensive assessment of equipment types, applications, end-users, technologies, and regional dynamics shaping global demand. It covers ultra-class, large-class, mid-class, and smaller rigid haul trucks, analyzing performance, payload ranges, propulsion systems, and automation readiness across each category. The report evaluates surface mining, underground mining, construction, quarrying, and industrial logistics as key application segments, highlighting operational requirements, fleet composition, and digital integration trends within each use case.

Geographically, the scope spans Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with detailed comparisons of mining intensity, regulatory frameworks, electrification readiness, and automation penetration. Country-level insights include China, Australia, the U.S., Canada, Chile, Brazil, South Africa, and major European mining hubs such as Sweden and Germany.

Technology coverage includes autonomous haulage systems, electric and hybrid drivetrains, AI-based fleet optimization, predictive maintenance, digital twins, and remote operations centers. The report also examines supporting infrastructure such as charging networks, telemetry systems, and mine connectivity platforms.

End-user analysis encompasses large mining corporations, contract miners, equipment leasing firms, and construction-linked operators, assessing procurement behavior, adoption rates, and digital maturity. Environmental, safety, and regulatory considerations—such as emission standards, worker safety mandates, and ESG commitments—are integrated throughout the analysis.

Additionally, the report explores emerging niches such as battery-powered ultra-class trucks, trolley-assist systems, modular fleet retrofits, and software-defined vehicle upgrades. By synthesizing operational, technological, and regional trends, the report offers decision-makers a structured framework to evaluate investment opportunities, competitive positioning, and long-term strategic pathways in the evolving Heavy Mining Trucks ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,530.0 Million |

| Market Revenue (2033) | USD 3,882.8 Million |

| CAGR (2026–2033) | 5.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Caterpillar Inc., Komatsu Ltd., Liebherr Group, Hitachi Construction Machinery Co., Ltd., BelAZ, SANY Heavy Industry, XCMG Group, Zoomlion Heavy Industry, Volvo Construction Equipment, Sandvik Mining and Rock Solutions, Epiroc AB, Terex Corporation, Doosan Bobcat, Scania Mining Vehicles, Nikola Corporation, BYD Heavy Industries |

| Customization & Pricing | Available on Request (10% Customization Free) |