Reports

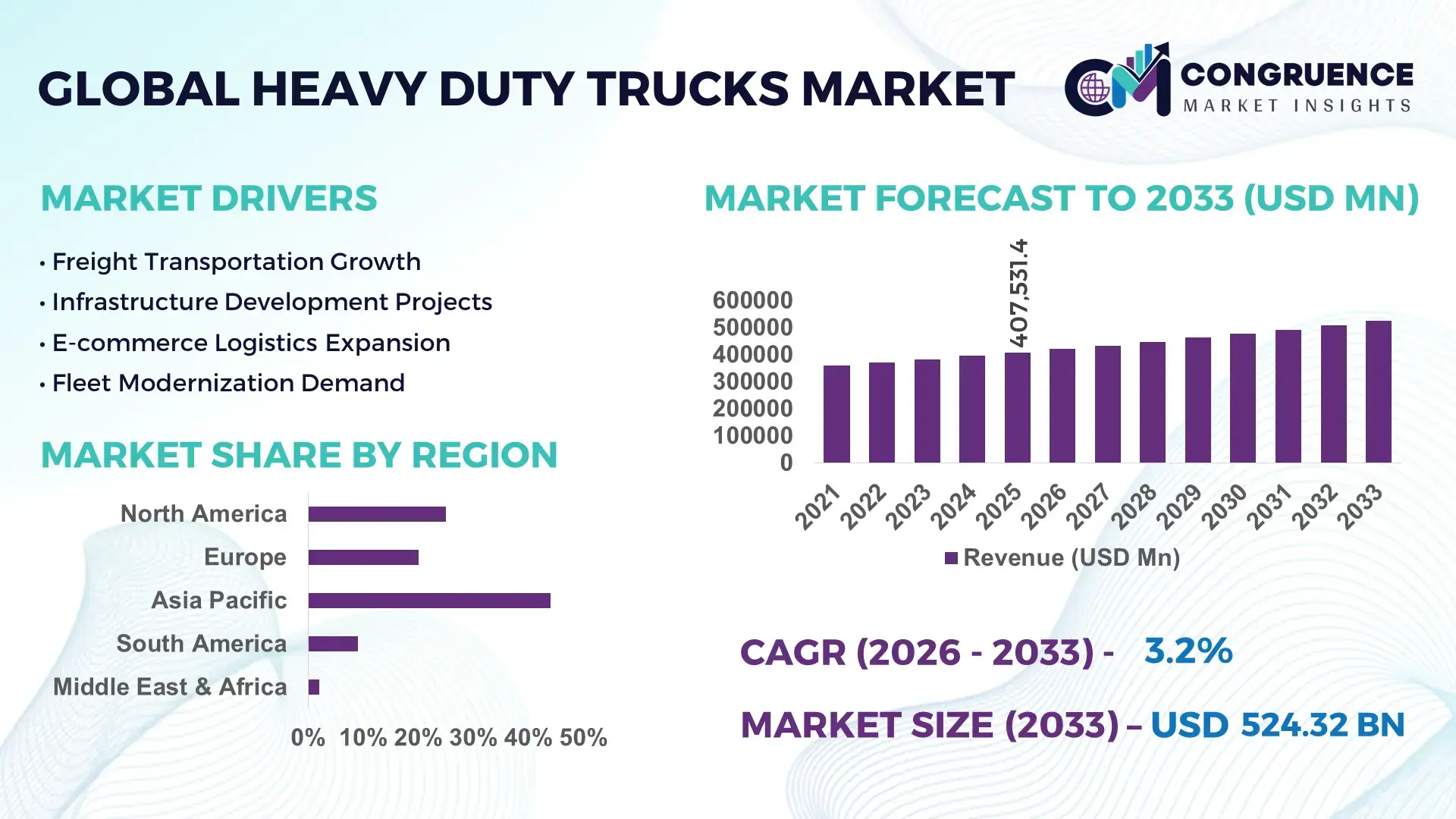

The Global Heavy Duty Trucks Market was valued at USD 407531.43 Million in 2025 and is anticipated to reach a value of USD 524322.73 Million by 2033 expanding at a CAGR of 3.2% between 2026 and 2033.

Market expansion is being driven by fleet digitization, LNG and electric truck deployment, and AI-based logistics optimization, with connected fleet systems reducing fuel consumption by nearly 14% across long-haul freight operations. Between 2024 and 2026, Euro VII emission regulations, U.S. clean transport incentives, and Red Sea shipping disruptions accelerated investment in localized manufacturing and fuel-efficient commercial vehicle platforms.

China dominated the global heavy duty trucks market in 2025 with nearly 34% production share and over USD 1 trillion allocated toward industrial infrastructure and logistics modernization projects. More than 62% of newly deployed premium fleets in China integrated telematics and driver-assistance technologies, compared with approximately 41% adoption across North America. India recorded over 14% growth in heavy commercial vehicle manufacturing due to mining expansion and national highway projects exceeding 25,000 km, while the United States strengthened autonomous freight testing and LNG truck adoption across regional logistics corridors. Compared with traditional diesel fleets, next-generation connected trucks improved operational efficiency by nearly 16% and lowered maintenance downtime by 11%. Manufacturers investing in intelligent fleet ecosystems and regional supply resilience are securing stronger long-term positioning in the competitive heavy duty trucks market.

Market Size & Growth: USD 407531.43 Million in 2025 reaching USD 524322.73 Million by 2033 at 3.2% CAGR, supported by AI-enabled fleet optimization and logistics modernization.

Top Growth Drivers: Connected fleet adoption increased 21%, LNG truck deployment rose 19%, and cross-border freight activity expanded 13% during 2025.

Short-Term Forecast: By 2028, predictive maintenance systems are projected to reduce fleet downtime by 22% and improve route efficiency by 15%.

Emerging Technologies: AI telematics, autonomous driving assistance, and lightweight composite materials improved fuel efficiency by nearly 14% in advanced fleets.

Regional Leaders: Asia-Pacific exceeded USD 172 Billion, North America crossed USD 108 Billion, and Europe surpassed USD 94 Billion with strong low-emission truck adoption.

Consumer/End-User Trends: Nearly 58% of logistics operators prioritized connected heavy-duty fleets with real-time diagnostics and fuel monitoring systems.

Pilot/Case Example: In 2025, an Australian mining logistics project improved hauling productivity by 17% through autonomous heavy-duty truck deployment.

Competitive Landscape: Top five manufacturers controlled nearly 46% market share, led by Daimler Truck, Volvo, PACCAR, Scania, and FAW.

Regulatory & ESG Impact: Euro VII and U.S. clean transportation policies accelerated low-emission fleet procurement by over 24% during 2025.

Investment & Funding: Global investments exceeded USD 48 Billion across battery-electric trucks, localized production expansion, and digital fleet infrastructure.

Innovation & Future Outlook: Hydrogen-powered heavy-duty platforms and AI-driven autonomous freight systems are reshaping next-generation logistics competitiveness.

Mining, construction, and long-haul logistics collectively contributed more than 63% of global heavy-duty truck demand in 2025, supported by rising infrastructure spending and industrial freight activity. Advanced telematics and autonomous driver-assistance systems improved fleet utilization by nearly 18%, while lightweight composite components reduced vehicle weight by approximately 9%. Asia-Pacific remained the strongest demand center due to manufacturing expansion and highway development programs, while Europe accelerated low-emission fleet replacement under stricter transport regulations. Increasing regional supply chain localization and investment in hydrogen-powered truck platforms are expected to reshape competitive strategies and operational efficiency across the global heavy duty trucks market over the next several years.

The heavy duty trucks market is rapidly transforming into a strategic control point for global freight mobility, industrial supply continuity, and infrastructure-driven economic expansion. Fleet modernization is no longer limited to vehicle replacement cycles; it is becoming a competitive investment race centered on digital logistics optimization, low-emission transport capability, and autonomous freight scalability. Large logistics operators are accelerating procurement of connected heavy-duty fleets as route intelligence platforms improve delivery efficiency by nearly 18% and reduce idle fuel consumption by 13%. Simultaneously, mining, construction, and cross-border transportation sectors are shifting toward high-capacity smart trucks capable of operating within predictive maintenance ecosystems that increase fleet uptime beyond 95%.

Global supply chain restructuring, stricter transport emission regulations, and regional manufacturing localization are forcing truck manufacturers to redesign sourcing and production strategies between 2024 and 2026. Battery-electric and LNG-powered platforms are reshaping operational economics across freight corridors where fuel costs represent over 30% of total fleet expenditure. AI-enabled telematics improves operational efficiency by 21% while reducing maintenance costs by 16% compared to legacy fleet management systems dependent on reactive servicing models. Asia-Pacific leads in production volume with nearly 48% of global manufacturing activity, while Europe leads in low-emission adoption and smart fleet integration with connected commercial vehicle penetration exceeding 44%.

Over the next two to three years, autonomous route optimization and predictive diagnostics are projected to reduce long-haul delivery delays by 19% while improving asset utilization by approximately 14%. ESG compliance is also emerging as a measurable competitive advantage, as low-emission fleet operators are securing preferential access to urban freight corridors and reducing regulatory compliance costs by nearly 11%. In 2025, a Scandinavian logistics operator deploying AI-integrated electric heavy-duty fleets improved route productivity by 17% and lowered annual fuel expenditure by 22% across regional distribution operations.

Rapid infrastructure expansion, industrial freight growth, and fleet digitization are accelerating heavy duty truck demand across logistics and construction sectors. Global freight transportation activity increased by nearly 12% in 2025, while mining and infrastructure cargo movement expanded by 9%, forcing operators to modernize aging fleets. AI-enabled telematics improved fuel efficiency by 14% and reduced maintenance downtime by 18%, creating measurable operational gains for logistics companies. Following Red Sea shipping disruptions and regional supply chain restructuring, manufacturers increased regional production capacity and expanded strategic partnerships focused on connected fleet technologies and alternative fuel platforms to strengthen delivery reliability and operational flexibility.

Battery supply concentration, semiconductor dependency, and uneven charging infrastructure remain major structural restraints for the heavy duty trucks market. Commercial electric truck production costs increased by approximately 18% between 2024 and 2025 due to lithium and nickel price volatility, while delivery timelines extended by nearly 11% from component shortages. Less than 15% of industrial freight corridors in emerging economies currently support high-capacity charging systems, constraining electric fleet deployment. In response, manufacturers are diversifying supplier networks, securing long-term mineral contracts, and investing in hybrid LNG-electric platforms to reduce infrastructure dependency and improve operational scalability.

Autonomous logistics systems, hydrogen fuel platforms, and software-defined fleet ecosystems are creating high-impact opportunities across the heavy duty trucks market. Predictive fleet analytics improved asset utilization by nearly 15%, while autonomous route optimization reduced freight turnaround time by 17% in large logistics networks during 2025. Hydrogen-powered trucks are gaining strategic importance in long-haul freight operations where battery weight limits cargo efficiency. Manufacturers are accelerating investment in modular energy systems, AI-based transport analytics, and regional hydrogen partnerships to secure future competitive advantage and establish recurring service-based revenue ecosystems beyond traditional vehicle sales.

Infrastructure scalability, regulatory fragmentation, and technology integration complexity continue challenging long-term heavy duty truck market transformation. Fewer than 20% of major freight hubs currently support megawatt-scale charging infrastructure for heavy commercial vehicles, limiting large-scale electric fleet deployment. Advanced battery systems also increase vehicle weight by nearly 12%, affecting cargo efficiency and route economics. Different emission standards across North America, Europe, and Asia are increasing engineering and certification costs for manufacturers. To maintain competitiveness, companies are accelerating investment in charging alliances, digital fleet ecosystems, and software-defined vehicle architectures capable of improving deployment speed and operational consistency.

18% Growth in AI Fleet Systems. Logistics operators rapidly expanded AI-enabled telematics deployment during 2025, with connected truck integration rising 18% across large freight fleets. Automated route optimization reduced idle fuel consumption by 13% and improved scheduling accuracy by 16%. Companies are restructuring fleet operations around centralized digital monitoring systems to counter labor shortages and rising freight complexity across regional logistics networks.

24% Rise in LNG and Electric Trucks. Commercial fleet operators accelerated LNG and battery-electric truck deployment by 24% across urban freight and regional transport routes. Low-emission trucks reduced operating expenses by nearly 17% in high-mileage applications while supporting compliance with stricter emission regulations. Manufacturers are scaling localized battery partnerships and modular production systems to reduce sourcing dependency and improve manufacturing flexibility.

21% Expansion in Refrigerated Fleets. Refrigerated truck utilization increased 21% across pharmaceutical, food, and cold-chain logistics sectors as supply chain reliability became operationally critical after regional shipping disruptions. IoT-enabled monitoring systems improved temperature management efficiency by 14% and reduced cargo spoilage risks. Companies are prioritizing smart refrigeration integration and regional fleet expansion to capture rising demand in high-value cargo transportation.

15% Increase in Fleet Subscription Models. Logistics companies increasingly shifted toward fleet-as-a-service structures, with subscription-based heavy-duty vehicle usage increasing 15% during 2025. Flexible leasing systems lowered upfront capital burden by approximately 19% while improving fleet replacement speed. Manufacturers are responding through bundled maintenance ecosystems, software-driven fleet monitoring, and strategic financing partnerships designed to strengthen recurring operational revenue streams.

The heavy duty trucks market is segmented by type, application, and end-user, with demand concentrated around freight transportation, infrastructure development, and industrial logistics operations. Semi-trailer trucks and freight transport applications collectively account for over 45% of operational deployment due to their scalability across long-haul commercial supply chains. Demand is increasingly shifting toward refrigerated and tanker trucks as temperature-controlled logistics and energy transportation networks expand globally. Construction and mining segments continue strengthening procurement activity due to infrastructure modernization and resource extraction projects across Asia-Pacific, the Middle East, and Latin America. Logistics companies remain the dominant end-user group, while mining and oil and gas operators are accelerating adoption of connected heavy-duty fleets to improve route efficiency and reduce downtime by nearly 15%. Manufacturers are responding through specialized vehicle customization, modular platform expansion, and intelligent fleet integration strategies designed to capture sector-specific operational demand.

Semi-trailer trucks dominated the heavy duty trucks market with nearly 39% share in 2025 due to their superior freight scalability, lower per-ton transportation costs, and compatibility with cross-border logistics networks. Their operational flexibility across industrial cargo, container transport, and retail distribution continues reinforcing structural dominance among large logistics operators. Refrigerated trucks emerged as the fastest-growing segment, recording approximately 17% growth due to expanding pharmaceutical distribution and temperature-controlled food logistics demand. Compared with dump trucks, refrigerated fleets generate higher route utilization efficiency and stronger long-haul deployment consistency, particularly in export-driven supply chains.

Dump trucks and tanker trucks collectively accounted for nearly 43% of market deployment, supported by construction, mining, fuel transportation, and industrial material handling operations. Dump truck demand remains concentrated in infrastructure-intensive economies, while tanker trucks are gaining strategic relevance through rising LNG and industrial liquid transport requirements. Manufacturers are increasingly prioritizing lightweight trailer systems, smart cargo monitoring technologies, and modular fleet platforms to improve operational efficiency and reduce maintenance intensity. Investment focus is rapidly shifting toward connected semi-trailer ecosystems and refrigerated fleet expansion, while conventional standalone hauling platforms face slower modernization cycles.

Freight transport remained the leading application segment with approximately 42% share due to the heavy dependency of global supply chains on long-haul commercial trucking networks. Rising e-commerce distribution, industrial cargo movement, and cross-border logistics activity continue concentrating deployment within freight transportation fleets. Logistics-focused heavy-duty trucks improved route efficiency by nearly 16% through AI-enabled fleet monitoring and predictive dispatch systems. Construction emerged as the fastest-growing application, expanding by nearly 15% during 2025 as infrastructure modernization and highway expansion projects accelerated across developing economies.

Compared with mature freight transport operations, construction fleets are experiencing stronger short-cycle procurement growth due to rising demand for dump trucks and high-capacity hauling systems. Mining, oil and gas, and logistics applications collectively accounted for approximately 48% of heavy-duty truck deployment, supported by energy transportation, raw material extraction, and industrial supply continuity requirements. Companies are increasingly repositioning fleets around fuel-efficient platforms, telematics integration, and specialized hauling systems designed for sector-specific operating conditions. Demand is shifting toward application-specific smart trucks capable of optimizing uptime, payload management, and operational safety in high-intensity industrial environments.

Logistics companies dominated the heavy duty trucks market with nearly 44% share due to continuous freight movement requirements, high fleet utilization intensity, and increasing dependence on digitally connected transportation systems. Large logistics operators are aggressively modernizing fleets with AI-enabled telematics and predictive maintenance technologies capable of reducing downtime by nearly 18%. The mining industry emerged as the fastest-growing end-user segment, recording approximately 16% expansion during 2025 as global mineral extraction and industrial commodity transportation activity accelerated across Asia-Pacific, Latin America, and Africa.

Compared with the construction industry, logistics companies prioritize operational efficiency and fuel optimization, while mining operators focus on high-load durability and autonomous hauling capability. Construction and oil and gas industries collectively represented nearly 41% of market demand, driven by infrastructure projects, energy transportation, and industrial material movement requirements. Manufacturers are increasingly targeting these end-users through customized financing structures, application-specific truck platforms, and long-term maintenance partnerships designed to improve lifecycle operating performance. Demand is steadily shifting toward connected fleets with integrated diagnostics and centralized fleet management ecosystems capable of optimizing productivity across large industrial transport networks.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.1% between 2026 and 2033.

Asia-Pacific continues dominating heavy duty truck production and demand due to large-scale manufacturing capacity, mining activity, and infrastructure expansion across China and India. Europe accounted for nearly 24% of market demand and leads in low-emission fleet adoption, with connected commercial vehicle penetration exceeding 44% under tightening transport regulations. North America represented approximately 21% share, driven by LNG truck deployment, autonomous freight testing, and digital logistics transformation. Supply chain localization and stricter emission compliance are reshaping regional procurement strategies, forcing manufacturers to expand localized production and smart fleet ecosystems. Global companies are increasingly prioritizing Asia-Pacific for scale, Europe for technology adaptation, and North America for operational innovation and advanced fleet deployment.

North America accounted for approximately 21% of global heavy duty truck demand in 2025, supported by strong freight transportation, construction logistics, and energy sector activity across the United States and Canada. Fleet operators are accelerating LNG and connected truck deployment, with smart fleet integration increasing by nearly 19% during 2025. Tightening emission regulations and rising long-haul operating costs are forcing companies to optimize fuel efficiency and predictive maintenance systems. Autonomous freight testing expanded across major logistics corridors, while regional manufacturers increased localized battery and component partnerships to reduce supply chain dependency. Enterprise buyers increasingly prioritize uptime, route optimization, and lifecycle operating costs over conventional acquisition-focused purchasing decisions. Companies continue prioritizing North America for advanced fleet deployment, digital logistics scaling, and autonomous transport commercialization.

Europe represented nearly 24% of global heavy duty truck demand in 2025, driven by strict emission regulations and accelerated low-emission fleet replacement across Germany, France, and the Nordic region. Euro VII compliance requirements increased electric and LNG heavy-duty truck adoption by approximately 22% during 2025, while connected fleet deployment surpassed 44% among large logistics operators. Fleet operators are prioritizing lightweight vehicle platforms and AI-based route optimization systems to reduce operational emissions and improve transport efficiency. Manufacturers expanded hydrogen truck partnerships and regional charging infrastructure investments to strengthen long-haul electrification capability. Enterprise buyers increasingly favor compliance-driven fleet modernization strategies focused on operational sustainability and urban freight access. Europe continues forcing rapid innovation in low-emission transport systems and intelligent fleet management technologies.

Asia-Pacific dominated the heavy duty trucks market with nearly 48% share in 2025, led by China, India, Japan, and Southeast Asian manufacturing economies. Rapid infrastructure construction, mining activity, and export-driven logistics expansion continue strengthening regional fleet demand. Connected truck deployment increased by approximately 21% across premium commercial fleets, while localized heavy-duty vehicle manufacturing capacity expanded by nearly 16% during 2025. China remains the largest production hub, while India accelerated highway expansion and mining logistics deployment across industrial corridors. Fleet operators increasingly prioritize scalable, fuel-efficient truck platforms capable of supporting high-volume freight movement at lower operating cost. Manufacturers continue expanding regional production facilities, supplier ecosystems, and modular truck platforms, making Asia-Pacific the critical global center for heavy-duty truck scale, manufacturing speed, and demand concentration.

South America accounted for nearly 7% of global heavy duty truck demand in 2025, supported primarily by mining, agriculture, and cross-border freight activity across Brazil, Argentina, and Chile. Infrastructure modernization and commodity transportation demand increased heavy commercial vehicle deployment by approximately 11% during 2025. However, high financing costs and uneven charging infrastructure remain major operational constraints for fleet modernization. Logistics operators increasingly shifted toward fuel-efficient diesel and LNG truck platforms to manage rising freight expenses and regulatory pressure. Regional manufacturers expanded localized assembly operations and aftermarket service networks to improve delivery timelines and reduce import dependency. Enterprise buyers remain highly price-sensitive, prioritizing durability, payload efficiency, and low maintenance intensity. South America presents strong logistics expansion potential but requires infrastructure and financing improvements to unlock larger-scale fleet transformation.

The Middle East & Africa represented approximately 9% of global heavy duty truck demand in 2025, driven by large-scale infrastructure, mining, and oil and gas transportation projects across Saudi Arabia, the UAE, and South Africa. Industrial logistics deployment increased by nearly 13% during 2025 as governments accelerated economic diversification and construction modernization programs. Fleet operators increasingly adopted connected monitoring systems and high-capacity hauling platforms to improve operational reliability across long-distance transport routes. Regional investments in logistics corridors and smart industrial zones strengthened heavy commercial vehicle procurement activity, while manufacturers expanded regional partnerships and service networks to improve fleet support capability. Enterprise buyers prioritize durability, high-load performance, and operational resilience under harsh environmental conditions. The region is rapidly emerging as a strategic growth zone for infrastructure-linked heavy-duty transportation deployment.

China – 34% market share: China dominates the heavy duty trucks market through massive manufacturing capacity, infrastructure expansion, and large-scale industrial freight demand.

United States – 18% market share: The United States leads in advanced fleet digitization, autonomous freight testing, and LNG-powered heavy-duty truck deployment across logistics networks.

The heavy duty trucks market is characterized by intense competition between global OEM leaders, regional manufacturing specialists, and technology-driven fleet solution providers. Daimler Truck, Volvo, PACCAR, Scania, and FAW collectively controlled nearly 46% of global market activity in 2025, competing aggressively across fuel efficiency, fleet intelligence integration, production scalability, and low-emission vehicle deployment. European manufacturers are competing through hydrogen and electric platform innovation, while North American players focus on autonomous freight systems and LNG-powered fleet optimization. Chinese manufacturers continue strengthening cost competitiveness and export scalability through localized supply chain integration.

Competitive differentiation increasingly depends on operational efficiency, connected fleet ecosystems, and manufacturing flexibility. AI-enabled telematics improved fleet utilization by nearly 18%, while predictive maintenance systems reduced downtime by approximately 20%, forcing manufacturers to integrate software-driven transport solutions into core vehicle platforms. Companies are accelerating strategic partnerships involving battery suppliers, logistics software providers, and charging infrastructure developers to strengthen ecosystem control and regional expansion capability.

Rising compliance costs, battery sourcing concentration, and infrastructure investment requirements remain major entry barriers. Companies capable of combining intelligent fleet technologies, regional manufacturing resilience, and scalable low-emission transport platforms are securing long-term competitive leadership in the evolving heavy duty trucks market.

Daimler Truck

Volvo Group

PACCAR Inc.

Scania AB

MAN Truck & Bus

FAW Group

Dongfeng Motor Corporation

Tata Motors

Ashok Leyland

Isuzu Motors

Navistar International

Hyundai Motor Company

Iveco Group

Hino Motors

AI-enabled telematics, predictive maintenance systems, and software-defined fleet platforms are currently transforming operational execution across the heavy duty trucks market. Connected fleet deployment surpassed 44% among large logistics operators during 2025, while predictive diagnostics reduced unplanned downtime by nearly 20% and improved fuel efficiency by 14%. Cloud-integrated fleet management systems are also optimizing route allocation and driver scheduling in real time, allowing freight operators to lower idle time by approximately 13%. Compared with legacy reactive maintenance models, AI-based fleet intelligence platforms improve operational efficiency by nearly 21% while reducing maintenance costs by 16%, creating measurable competitive advantages for high-volume logistics providers.

Battery-electric drivetrains, hydrogen fuel-cell systems, and autonomous freight technologies are emerging as the next major technology shift between 2026 and 2028. LNG and electric heavy-duty truck deployment increased by 24% during 2025 as transport operators accelerated low-emission fleet modernization under tightening emission regulations. Hydrogen-powered truck pilots expanded across Europe and North America, particularly in long-haul freight corridors where liquid hydrogen systems support driving ranges exceeding 1,000 kilometers. Manufacturers are increasingly integrating modular battery systems, intelligent energy management software, and autonomous assistance technologies to improve scalability and reduce operational transition costs.

Disruptive technologies are reshaping competitive positioning across the industry. Autonomous truck testing programs improved freight route productivity by nearly 17%, while lightweight composite materials reduced vehicle weight by approximately 9%, increasing payload efficiency. Global OEMs and fleet technology firms are accelerating software partnerships, battery alliances, and digital ecosystem integration to secure long-term control over connected transport infrastructure. Companies capable of scaling intelligent fleet ecosystems, alternative fuel systems, and autonomous logistics platforms between 2026 and 2028 will capture stronger operational margins, regulatory advantages, and premium commercial fleet contracts.

January 2026 – Daimler Truck launched customer deployment plans for the Mercedes-Benz GenH2 hydrogen truck, targeting operational ranges above 1,000 km and expanded hydrogen freight testing across Europe. The initiative strengthens zero-emission long-haul logistics capability while accelerating hydrogen infrastructure partnerships and fleet transition programs. [Hydrogen Freight Scale] Source: Daimler Truck

May 2024 – Volvo Autonomous Solutions introduced the production-ready Volvo VNL Autonomous platform integrated with Aurora technology for U.S. freight corridors. The autonomous system improves route productivity and supports scalable commercial deployment for logistics operators seeking higher fleet utilization and reduced driver dependency. [Autonomous Logistics Rollout] Source: Volvo Group

May 2024 – Volvo Group and Daimler Truck announced a 50/50 joint venture focused on software-defined vehicle architecture for heavy-duty commercial fleets. The collaboration accelerates connected fleet integration, digital transport ecosystems, and centralized software deployment across next-generation truck platforms. [Software Platform Alliance] Source: Volvo Group JV Announcement

May 2026 – Mercedes-Benz Trucks and Buses Argentina inaugurated a manufacturing facility with annual production capacity reaching 10,000 vehicles, strengthening regional supply resilience and export-focused heavy-duty truck manufacturing across South America. The expansion improves localized production flexibility and delivery responsiveness for industrial fleet operators. [Regional Capacity Expansion] Source: Reuters

The Heavy Duty Trucks Market Report provides detailed analysis across vehicle types, applications, end-users, regional markets, and emerging transportation technologies shaping global commercial freight operations. The report covers Semi-Trailer Trucks, Dump Trucks, Tanker Trucks, and Refrigerated Trucks, alongside key applications including freight transport, construction, mining, oil and gas, and logistics. End-user analysis evaluates procurement behavior across logistics companies, construction operators, mining firms, and energy transportation providers. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional production shifts, fleet modernization activity, and infrastructure-led demand acceleration.

The report delivers strategic evaluation of connected fleet systems, AI-enabled telematics, predictive maintenance technologies, autonomous freight platforms, LNG-powered trucks, battery-electric vehicles, and hydrogen fuel-cell deployment trends between 2026 and 2033. More than 44% of large logistics operators now integrate connected fleet management systems, while low-emission truck adoption increased by nearly 24% during 2025. The study also analyzes operational efficiency metrics, deployment patterns, supply chain localization, and competitive positioning across leading manufacturers and regional operators.

The report supports investment planning, regional expansion strategy, fleet modernization decisions, technology adoption prioritization, and competitive benchmarking for manufacturers, logistics providers, infrastructure developers, and institutional stakeholders operating within the evolving heavy duty trucks market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 407531.43 Million |

|

Market Revenue in 2033 |

USD 524322.73 Million |

|

CAGR (2026 - 2033) |

3.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Daimler Truck, Volvo Group, PACCAR Inc., Scania AB, MAN Truck & Bus, FAW Group, Dongfeng Motor Corporation, Tata Motors, Ashok Leyland, Isuzu Motors, Navistar International, Hyundai Motor Company, Iveco Group, Hino Motors |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |