Reports

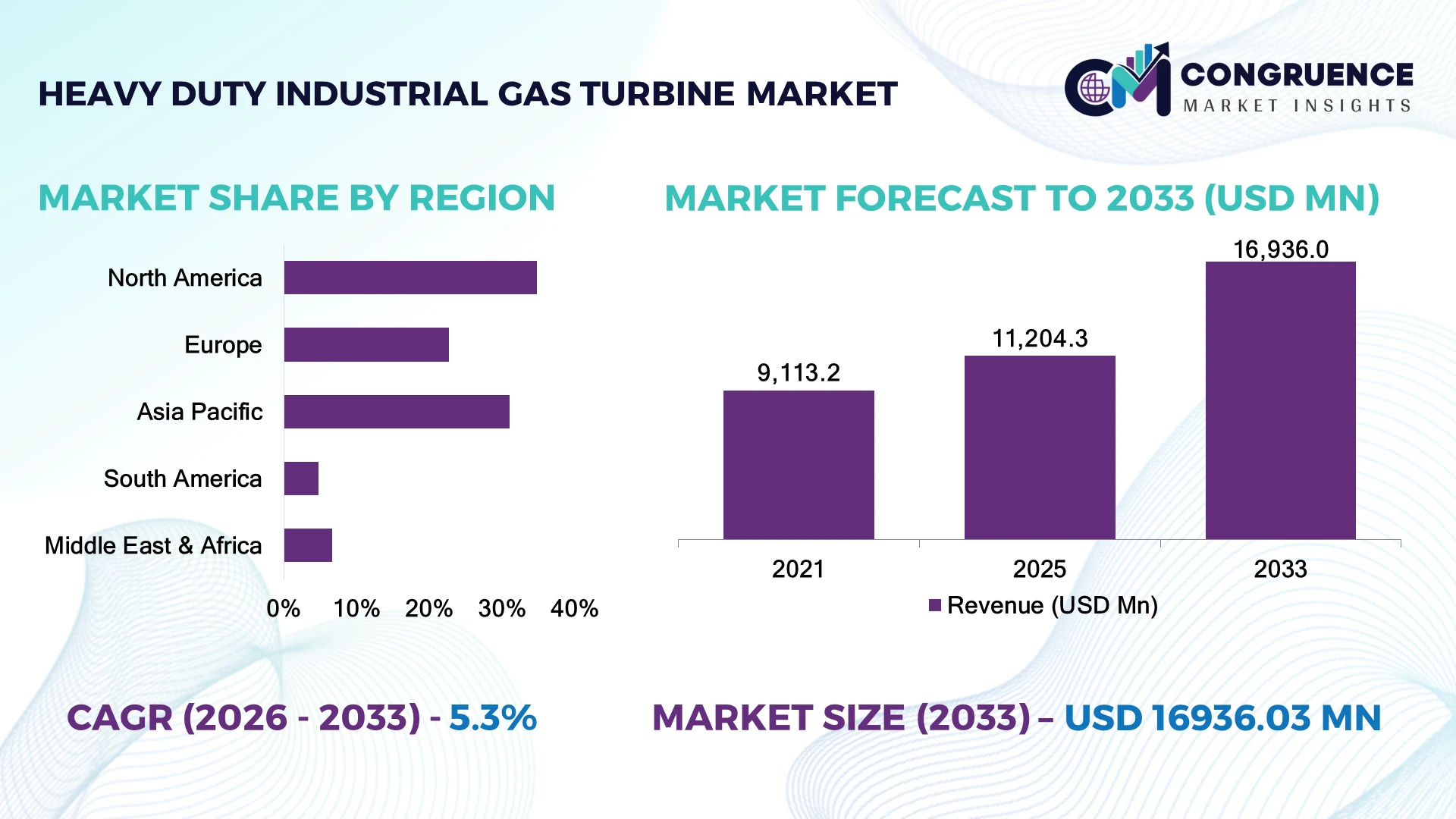

The Global Heavy Duty Industrial Gas Turbine Market was valued at USD 11,204.3 Million in 2025 and is anticipated to reach a value of USD 16,936.0 Million by 2033 expanding at a CAGR of 5.3% between 2026 and 2033. Growth is being driven by combined-cycle power plant expansion, grid reliability investments, and increasing deployment of hydrogen-ready gas turbines for flexible low-emission electricity generation.

The United States accounts for approximately 28% of global heavy-duty industrial gas turbine installations, supported by extensive combined-cycle power generation, LNG infrastructure expansion, and modernization of aging thermal assets. Compared with Japan's high-efficiency gas-fired fleet, the U.S. operates nearly 2.5 times greater installed heavy-duty gas turbine capacity. Following global energy security priorities after the Russia-Ukraine conflict, advanced turbine utilization has increased by approximately 18% across flexible baseload and peak-load generation assets.

Utilities and industrial operators investing in hydrogen-compatible turbines, digital asset management, and high-efficiency combined-cycle technologies will strengthen long-term operational resilience and competitive energy performance.

Market Size & Growth: USD 11,204.3 Million in 2025, projected to reach USD 16,936.0 Million by 2033 at a CAGR of 5.3%, supported by grid modernization and flexible power generation.

Top Growth Drivers: Combined-cycle deployment (42%), hydrogen-ready turbines (34%), and power infrastructure upgrades (31%).

Short-Term Forecast: By 2028, advanced turbine efficiency is expected to improve plant heat rates by nearly 8%.

Emerging Technologies: Hydrogen combustion, AI predictive maintenance, and digital twin optimization are reshaping turbine operations.

Regional Leaders: North America exceeds USD 4.6 Billion, Asia-Pacific approaches USD 4.2 Billion, and Europe surpasses USD 3.1 Billion through infrastructure modernization.

Consumer/End-User Trends: Nearly 61% of new utility procurements prioritize high-efficiency combined-cycle turbines.

Pilot/Case Example: A 2026 turbine modernization project increased output by 7% while reducing maintenance downtime by 15%.

Competitive Landscape: The leading manufacturer controls approximately 24% market share alongside GE Vernova, Siemens Energy, Mitsubishi Power, and Ansaldo Energia.

Regulatory & ESG Impact: Low-emission combustion technologies reduce NOx emissions by over 30% compared with conventional designs.

Investment & Funding: More than USD 14 Billion is supporting gas-fired power modernization, hydrogen readiness, and digital upgrades.

Innovation & Future Outlook: Flexible fuel capability, carbon capture integration, and autonomous turbine diagnostics are strengthening long-term competitiveness.

Heavy Duty Industrial Gas Turbine Market demand remains concentrated in utility-scale electricity generation, petrochemical processing, LNG terminals, and energy-intensive manufacturing. Hydrogen-capable combustion systems, AI-driven predictive maintenance, and advanced cooling technologies are improving operational efficiency and asset reliability. Approximately 46% of newly commissioned heavy-duty turbines are designed for future hydrogen blending, reflecting evolving decarbonization strategies and power system flexibility requirements, setting the stage for the strategic outlook.

Heavy-duty industrial gas turbines have become strategically important as governments and utilities prioritize reliable dispatchable power alongside expanding renewable electricity generation. Grid modernization, energy security planning, and industrial electrification are driving investment toward high-efficiency combined-cycle facilities capable of balancing intermittent renewable resources while maintaining system stability.

Modern H-class and J-class gas turbines deliver approximately 12% higher efficiency than previous-generation units while reducing fuel consumption by nearly 8% through advanced combustion systems, digital controls, and optimized cooling technologies. North America continues leading replacement demand through aging power infrastructure modernization, whereas Asia-Pacific is expanding deployment to support industrial growth, LNG development, and electricity demand. Over the next two to three years, hydrogen co-firing capability, AI-assisted predictive maintenance, and digital asset optimization are expected to become standard procurement priorities across utility-scale installations.

Power producers are increasingly integrating hydrogen-ready turbines with carbon capture strategies and renewable generation to improve operational flexibility and reduce emissions intensity. Equipment manufacturers are strengthening regional manufacturing, expanding long-term service agreements, and investing in combustion innovation through strategic partnerships. Organizations combining fuel flexibility, digital performance optimization, and lifecycle service capabilities will secure stronger competitive positioning and long-term relevance within the evolving global power generation landscape.

Grid modernization and rising electricity demand are accelerating deployment of heavy-duty industrial gas turbines for flexible baseload and peak-load generation. More than 63% of newly commissioned utility-scale gas-fired projects utilize advanced combined-cycle configurations, while H-class turbines improve plant efficiency by approximately 12% and reduce fuel consumption by nearly 8% compared with earlier platforms. The United States continues replacing aging coal-fired assets with high-efficiency gas turbine facilities to strengthen grid reliability and renewable energy integration. This transition improves operational flexibility while supporting decarbonization objectives. Manufacturers are expanding hydrogen-ready turbine portfolios, investing in advanced combustion technologies, and strengthening long-term service partnerships to improve lifecycle performance and secure utility procurement opportunities.

Heavy-duty industrial gas turbine deployment remains constrained by volatile raw material costs, specialized component availability, and uncertainty in natural gas pricing. High-temperature alloys and precision turbine blades account for nearly 24% of manufacturing costs, while project lead times have increased by approximately 18% because of global supply-chain constraints. Germany and other European markets continue facing procurement challenges for critical turbine components and fluctuating fuel economics, affecting investment decisions for new power generation assets. These pressures influence project profitability and procurement schedules. Equipment suppliers are mitigating risks through regional manufacturing expansion, long-term supplier contracts, localized sourcing strategies, and modular component standardization that improves production resilience and delivery reliability.

Hydrogen-compatible combustion technology is creating significant long-term opportunities for heavy-duty industrial gas turbine manufacturers and power producers. More than 46% of newly commissioned heavy-duty turbines are designed for future hydrogen blending, while advanced combustion systems reduce carbon intensity by approximately 20% when operating with low-carbon fuel mixtures. Japan is accelerating investment in hydrogen infrastructure and gas-fired power modernization to support long-term energy transition strategies. Manufacturers are expanding research partnerships, developing flexible-fuel turbine platforms, and investing in advanced combustion testing facilities. A particularly valuable opportunity lies in retrofitting existing turbine fleets for hydrogen co-firing, enabling operators to extend asset life while lowering emissions without replacing core generation infrastructure.

Balancing reliable power generation with increasingly stringent emissions requirements presents a major execution challenge for heavy-duty industrial gas turbine operators. Carbon capture integration can increase project complexity by approximately 22%, while hydrogen combustion requires advanced materials capable of withstanding higher operating temperatures. The United Kingdom continues strengthening emissions performance requirements for thermal generation assets, increasing engineering and operational complexity for new installations. Manufacturers must invest in advanced materials, digital combustion controls, and predictive asset management while coordinating carbon capture compatibility and fuel flexibility. Successfully integrating multiple decarbonization technologies without compromising reliability or lifecycle economics will determine long-term competitiveness across utility-scale power generation.

Hydrogen Fuel Capability Expansion Manufacturers are accelerating deployment of hydrogen-ready turbines capable of operating with fuel blends exceeding 50% hydrogen, while advanced combustion systems reduce NOx emissions by approximately 30%. National decarbonization policies are driving utilities to prioritize flexible fuel platforms, encouraging strategic investments in combustion research, testing facilities, and long-term technology partnerships.

Digital Turbine Performance Analytics AI-powered diagnostics, digital twins, and predictive maintenance platforms improve equipment availability by nearly 16% while reducing unplanned maintenance events by approximately 21%. Operators are integrating real-time operational analytics across generating fleets, enabling optimized maintenance schedules, lower lifecycle costs, and improved dispatch reliability through enterprise-wide digital asset management.

Combined-Cycle Efficiency Upgrades Utilities are modernizing existing power stations with advanced heavy-duty turbine technology to increase generation efficiency and operational flexibility. High-efficiency upgrades improve plant output by approximately 9% while reducing heat rates by nearly 7%. Equipment suppliers are expanding long-term service agreements and modernization programs to extend plant life while supporting renewable energy integration.

Localized Manufacturing Strategies Manufacturers are strengthening regional production networks for turbine blades, combustion systems, and hot gas path components to reduce supply-chain risk. Localized sourcing has shortened equipment delivery timelines by approximately 19% while improving procurement resilience by nearly 15%. Companies are expanding strategic supplier partnerships and regional manufacturing capabilities to strengthen execution certainty for large utility-scale projects.

Combined cycle heavy-duty industrial gas turbines account for approximately 68% of the market owing to their superior thermal efficiency, lower fuel consumption, and suitability for large utility-scale power plants. Their integration with heat recovery steam generators enables higher output and lower operating costs, making them the preferred choice for utilities and independent power producers. Hydrogen-ready combined cycle systems represent the fastest-growing segment as energy transition strategies encourage flexible low-emission generation. Open cycle gas turbines continue serving peak-load and emergency applications because of rapid start-up capability, while cogeneration (CHP) configurations remain strategically important for industrial facilities requiring simultaneous electricity and process steam.

Manufacturers are investing in advanced combustion chambers, digital monitoring platforms, and flexible-fuel turbine technologies to strengthen lifecycle performance. Approximately 58% of newly ordered heavy-duty turbines support future hydrogen blending, while next-generation combined cycle plants improve overall plant efficiency by nearly 10% compared with previous installations. Investment continues shifting toward high-efficiency, low-emission turbine platforms capable of supporting grid flexibility and long-term decarbonization objectives.

According to 2026 deployment findings released by the International Energy Agency (IEA), combined cycle gas turbine facilities remain the preferred technology for new large-scale gas-fired generation because of their superior efficiency, operational flexibility, and compatibility with future low-carbon fuels.

Power generation accounts for approximately 74% of Heavy Duty Industrial Gas Turbine demand, reflecting extensive deployment across utility-scale electricity generation, combined-cycle plants, and grid stabilization projects. The segment benefits from rising electricity consumption, renewable energy balancing requirements, and replacement of aging coal-fired generation assets. Combined Heat and Power (CHP) applications represent the fastest-growing segment as industrial operators seek greater energy efficiency and lower operating costs through integrated electricity and steam production. Mechanical drive applications remain strategically important for LNG terminals, oil and gas pipelines, and petrochemical operations, while district heating projects continue expanding in selected developed economies.

Manufacturers are strengthening turbine flexibility through AI-assisted controls, hydrogen-ready combustion systems, and digital asset optimization. Nearly 52% of new heavy-duty turbine installations now feature integrated digital monitoring, while CHP systems improve overall fuel utilization by approximately 25% compared with standalone electricity generation. Companies continue expanding service agreements and application-specific engineering to strengthen long-term operational value.

According to 2025 industry assessments published by the Gas Turbine World Market Survey, utility-scale combined-cycle power generation continues accounting for the majority of new heavy-duty industrial gas turbine orders because of efficiency gains and operational flexibility.

Utilities account for approximately 66% of global heavy-duty industrial gas turbine procurement, supported by continuous investment in grid modernization, flexible generation assets, and replacement of aging thermal power infrastructure. Large utility operators require high-capacity turbines capable of supporting renewable integration while maintaining stable baseload and peak-load generation. Independent Power Producers (IPPs) represent the fastest-growing end-user segment as private investment in merchant power plants and long-term power purchase agreements continues expanding. Oil & gas companies, industrial manufacturers, and district energy operators maintain steady demand through captive power generation, mechanical drive systems, and combined heat and power installations.

Manufacturers are responding through customized long-term service agreements, lifecycle maintenance contracts, hydrogen-ready turbine configurations, and strategic regional partnerships. Approximately 48% of newly awarded utility projects specify digital performance monitoring, while predictive maintenance solutions reduce planned maintenance costs by nearly 18%. Companies are increasingly differentiating through lifecycle support, fuel flexibility, and operational optimization services rather than equipment supply alone.

According to a 2026 global power infrastructure assessment published by the International Energy Agency (IEA), electric utilities remain the largest purchasers of heavy-duty industrial gas turbines, while independent power producers continue recording the fastest expansion in new combined-cycle generation projects.

North America accounted for the largest market share at 34.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

Grid Modernization Drives High-Efficiency Turbine Deployment

North America remains the largest Heavy Duty Industrial Gas Turbine market through extensive combined-cycle power generation, LNG infrastructure expansion, and modernization of aging thermal assets. The region contributes approximately 34.8% of global market demand, supported by increasing electricity consumption, renewable energy integration, and investment in flexible generation capacity. Nearly 64% of newly approved gas-fired projects incorporate hydrogen-ready turbine technology, while digital asset monitoring improves plant availability by approximately 15%. Utilities continue upgrading existing generating fleets with high-efficiency turbines and advanced combustion systems. Equipment suppliers are expanding regional manufacturing, strengthening long-term service agreements, and collaborating with utilities to optimize lifecycle performance and operational reliability.

United States Market Outlook: The United States dominates the regional market through its extensive combined-cycle generation fleet, advanced gas transmission infrastructure, and strong replacement demand for aging coal-fired plants. Utility operators increasingly procure hydrogen-compatible turbines and digital maintenance platforms to improve operational flexibility. More than 45% of recent utility-scale gas-fired projects emphasize future hydrogen co-firing capability, positioning the country as a leader in next-generation thermal power modernization.

Decarbonization Policies Reshape Thermal Power Infrastructure

Europe continues transforming its heavy-duty gas turbine market through decarbonization initiatives, hydrogen infrastructure development, and modernization of flexible power generation assets. The region represents approximately 26% of global market activity, with utilities prioritizing low-emission combustion systems and digital performance optimization. Around 57% of new procurement programs now require hydrogen-compatible turbine designs, supporting long-term emissions reduction objectives. Manufacturers continue strengthening engineering partnerships, advanced materials development, and combustion technology innovation to improve operational efficiency while complying with increasingly stringent environmental standards.

Germany Market Outlook: Germany leads the regional market through advanced engineering capabilities, strong industrial power demand, and continued investment in hydrogen-ready thermal generation. Utilities are modernizing combined-cycle facilities with advanced turbine technologies capable of supporting future low-carbon fuels. Industrial operators also invest in high-efficiency cogeneration plants to improve energy security and operational reliability across manufacturing sectors.

Industrial Expansion Strengthens Regional Demand

Asia-Pacific represents the fastest-growing Heavy Duty Industrial Gas Turbine market, driven by rapid industrialization, rising electricity demand, LNG infrastructure expansion, and large-scale utility investments. The region contributes approximately 31% of global market demand, supported by continued deployment of high-capacity combined-cycle power stations. Nearly 61% of newly commissioned heavy-duty turbines feature advanced digital control systems and improved combustion technologies. Manufacturers are expanding localized production, engineering services, and regional supply chains to support increasing procurement across utility and industrial applications.

China Market Outlook: China leads regional deployment through large-scale electricity generation projects, expanding industrial infrastructure, and continuous investment in energy security. Utilities increasingly install high-efficiency heavy-duty turbines capable of balancing renewable generation while maintaining reliable grid operation. Domestic manufacturing expansion and localized component production continue strengthening project execution efficiency and long-term equipment availability.

Energy Infrastructure Investment Supports Market Growth

South America continues expanding heavy-duty gas turbine deployment through electricity infrastructure upgrades, industrial modernization, and increasing natural gas utilization. The region contributes approximately 4.8% of global market demand, with utilities replacing aging thermal assets using higher-efficiency combined-cycle technologies. Modern turbine installations improve generating efficiency by approximately 9% while supporting greater operational flexibility. Equipment suppliers are strengthening regional service networks, engineering support, and maintenance partnerships despite financing constraints and transmission infrastructure limitations that continue influencing project execution.

Brazil Market Outlook: Brazil remains the largest regional market because of expanding natural gas availability, industrial electricity demand, and modernization of thermal generation assets. Utilities continue investing in flexible gas-fired capacity to complement hydropower variability and improve supply security. Growing LNG infrastructure and industrial energy demand further strengthen procurement opportunities for advanced heavy-duty gas turbine technologies.

Large-Scale Power Investments Accelerate Modernization

The Middle East & Africa market continues expanding through utility-scale power generation projects, industrial diversification, and increasing investment in efficient thermal infrastructure. The region accounts for approximately 15% of global market activity, supported by natural gas availability and rising electricity demand. More than 59% of recently announced thermal generation projects prioritize high-efficiency heavy-duty turbines capable of future hydrogen integration. Manufacturers are strengthening regional partnerships, expanding service capabilities, and supporting localization initiatives to improve project execution and long-term operational performance.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through large-scale electricity expansion, industrial development, and strategic investment in advanced gas-fired generation. National energy diversification programs continue supporting procurement of high-capacity combined-cycle turbines with improved combustion efficiency. Utilities are also integrating digital asset management and predictive maintenance technologies to maximize plant reliability while preparing for future hydrogen-based power generation.

Competition is dominated by GE Vernova, Siemens Energy, Mitsubishi Power, Ansaldo Energia, and Harbin Electric, with global OEMs competing against regional turbine manufacturers, while engineering service providers challenge through lifecycle maintenance, modernization, and performance upgrades. The top five companies collectively account for approximately 72% of the market. Competition is driven by turbine efficiency, hydrogen capability, lifecycle costs, and service response rather than equipment pricing alone. Advanced H-class turbines improve combined-cycle efficiency by nearly 12%, AI-enabled predictive maintenance reduces unplanned outages by approximately 18%, and localized manufacturing shortens delivery timelines by almost 20%. Companies compete through hydrogen-ready product development, long-term service agreements, strategic EPC partnerships, and digital asset management platforms. Competitive momentum is shifting toward flexible-fuel turbines, digital lifecycle services, and localized supply chains. High certification requirements, complex manufacturing capabilities, and extended order backlogs remain major entry barriers. Sustainable leadership depends on efficiency, fuel flexibility, reliable execution, and comprehensive lifecycle support.

GE Vernova

Siemens Energy AG

Mitsubishi Power

Ansaldo Energia S.p.A.

Harbin Electric Corporation

Dongfang Electric Corporation

Kawasaki Heavy Industries, Ltd.

MAN Energy Solutions

Baker Hughes

Solar Turbines Incorporated

Bharat Heavy Electricals Limited (BHEL)

Doosan Enerbility

Rolls-Royce Holdings plc

Heavy Duty Industrial Gas Turbine technology is advancing through hydrogen-ready combustion systems, AI-enabled predictive maintenance, digital twins, and advanced thermal barrier coatings integrated with high-efficiency combined-cycle plants. Approximately 61% of newly ordered heavy-duty turbines now incorporate digital monitoring platforms, while predictive analytics improve equipment availability by nearly 16%. Smart combustion controls and real-time performance optimization reduce maintenance requirements while enhancing operational reliability across utility-scale power generation and industrial applications.

Compared with previous-generation F-class turbines, modern H-class platforms improve combined-cycle efficiency by approximately 12% while lowering fuel consumption by nearly 8% through advanced cooling systems, optimized aerodynamics, and higher firing temperatures. Utilities deploying hydrogen-compatible turbines gain a competitive advantage by extending asset life while preparing for future low-carbon fuel adoption. Digital twins also enable faster operational diagnostics and improve maintenance planning across complex power generation fleets.

Between 2026 and 2028, hydrogen combustion exceeding 50% fuel blends, carbon capture integration, additive manufacturing for turbine components, and AI-assisted autonomous plant optimization will reshape turbine competitiveness. Manufacturers investing in advanced materials, flexible-fuel combustion systems, and digital lifecycle management will strengthen long-term market leadership. Early technology adoption enables utilities and industrial operators to improve operational flexibility, reduce emissions intensity, and maximize lifecycle asset performance.

March 2025 – GE Vernova launched the TM2500 Dry Low Emissions mobile gas turbine, delivering 34 MW with up to 39% efficiency while eliminating water injection requirements, improving deployment flexibility for utilities and emergency power applications. Source: GE Vernova

April 2025 – GE Vernova introduced the AGP XPAND upgrade for 9E.03 heavy-duty gas turbines, increasing global fleet output potential by approximately 5 GW through enhanced Advanced Gas Path technology, strengthening modernization opportunities for existing combined-cycle plants. Source: GE Vernova News

July 2025 – GE Vernova secured an agreement with Crusoe to supply 29 LM2500XPRESS gas turbine packages delivering nearly 1 GW of electricity for AI data center infrastructure, reinforcing growing demand for flexible gas-fired generation. Source: GE Vernova

August 2024 – Global Energy Monitor reported GE Vernova, Siemens Energy, and Mitsubishi Power collectively supplied nearly two-thirds of gas turbine capacity under construction worldwide, highlighting increasing market concentration around advanced heavy-duty turbine manufacturers. Source: Global Energy Monitor (Global Energy Monitor)

This report provides comprehensive analysis of the Heavy Duty Industrial Gas Turbine Market across combined-cycle, open-cycle, and cogeneration turbine configurations. It evaluates deployment across utility-scale power generation, combined heat and power, mechanical drive, district energy, LNG infrastructure, and industrial processing while assessing demand from utilities, independent power producers, oil & gas companies, industrial manufacturers, and district energy operators. Regional analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering more than 20 strategically significant country markets and profiling leading turbine manufacturers.

The study examines hydrogen-ready combustion systems, digital twins, AI-enabled predictive maintenance, advanced turbine materials, carbon capture compatibility, and flexible-fuel technologies shaping market evolution between 2026 and 2033. It highlights deployment trends, modernization strategies, technology adoption, lifecycle service models, competitive positioning, and procurement priorities, enabling stakeholders to strengthen investment planning, expansion strategies, operational optimization, and long-term decision-making across the global heavy-duty gas turbine industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 11,204.3 Million |

|

Market Revenue in 2033 |

USD 16,936.0 Million |

|

CAGR (2026 - 2033) |

5.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GE Vernova, Siemens Energy AG, Mitsubishi Power, Ansaldo Energia S.p.A., Harbin Electric Corporation, Dongfang Electric Corporation, Kawasaki Heavy Industries, Ltd., MAN Energy Solutions, Baker Hughes, Solar Turbines Incorporated, Bharat Heavy Electricals Limited (BHEL), Doosan Enerbility, Rolls-Royce Holdings plc |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |