Reports

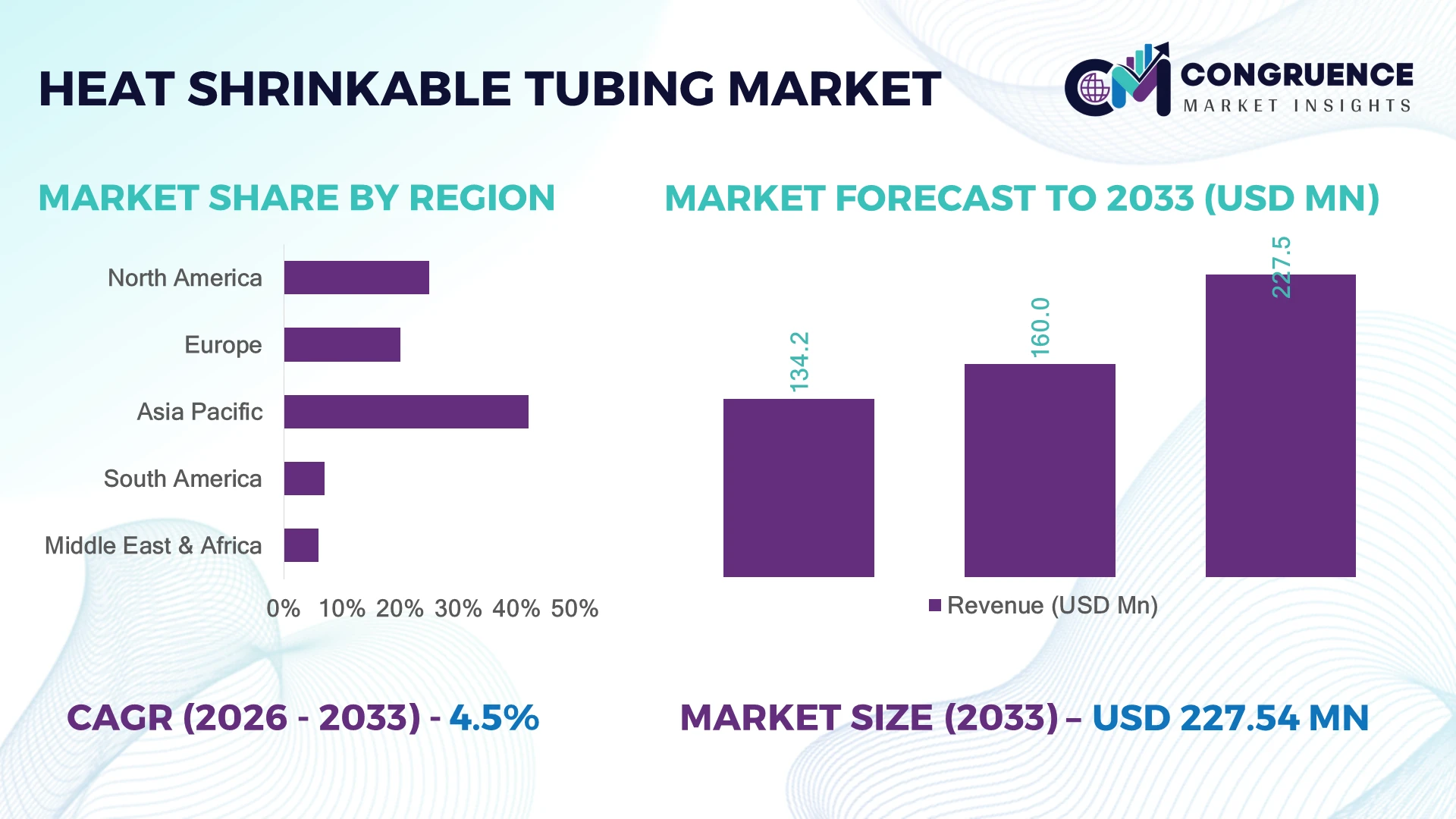

The Global Heat-Shrinkable Tubing Market was valued at USD 160.0 Million in 2025 and is anticipated to reach a value of USD 227.5 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. Growth is driven by rising adoption of heat-shrinkable insulation solutions in electric vehicles, aerospace wiring systems, renewable energy installations, and advanced electronics requiring reliable protection against moisture, corrosion, and thermal stress.

China dominates the market with nearly 32% share, supported by large-scale electronics manufacturing, EV production capacity exceeding 10 million units annually, and continued investments in semiconductor and renewable infrastructure. The United States follows with strong aerospace and defense demand, while Germany maintains advanced automotive applications with over 40% EV penetration in new passenger vehicle registrations.

Strategic investments in localized supply chains and high-performance materials will define competitive advantage.

Market Size & Growth: The market reaches USD 160.0 Million in 2025 and USD 227.5 Million by 2033 at a 4.5% CAGR, driven by EV wiring, aerospace electronics, and renewable energy systems.

Top Growth Drivers: EV adoption contributes 35%, electronics manufacturing 30%, and renewable energy infrastructure 25% of key demand acceleration.

Short-Term Forecast: By 2028, advanced tubing adoption improves installation efficiency by 20% and reduces maintenance costs by 15% across industrial applications.

Emerging Technologies: AI-enabled manufacturing, automated extrusion processes, and advanced fluoropolymer materials enhance precision and durability in next-generation tubing.

Regional Leaders: Asia Pacific reaches USD 95 Million by 2033 with EV expansion; North America reaches USD 70 Million with aerospace upgrades; Europe reaches USD 45 Million with automotive electrification.

Consumer/End-User Trends: Over 60% of demand comes from electrical and electronics applications requiring compact, lightweight, and high-temperature protection solutions.

Pilot/Case Example: A 2024 automotive wiring modernization project achieved 18% faster assembly cycles using automated heat-shrink installation technologies.

Competitive Landscape: Leading manufacturers hold approximately 45% combined market share, including TE Connectivity, 3M, Sumitomo Electric Industries, HellermannTyton, and Molex.

Regulatory & ESG Impact: Stricter vehicle safety standards and recyclable material initiatives reduce waste by up to 20% in advanced manufacturing processes.

Investment & Funding: More than USD 500 Million is directed toward specialty polymer production, regional manufacturing expansion, and supply-chain diversification.

Innovation & Future Outlook: Next-generation flame-retardant, smart-monitoring, and high-temperature tubing solutions are shifting the industry toward performance-driven applications.

Heat-Shrinkable Tubing Market demand is expanding across automotive electrification, industrial automation, telecommunications, and power distribution sectors. Recent innovations include halogen-free materials, miniaturized tubing designs, and higher-temperature resistant polymers, with premium solutions accounting for nearly 40% of new industrial installations. Supply-chain localization initiatives in Asia and North America are accelerating adoption as manufacturers seek reliable component availability and improved system protection.

Heat-shrinkable tubing is becoming strategically important as industries prioritize electrical reliability, compact system design, and protection against harsh operating environments. The transition toward electric mobility, renewable energy infrastructure, and advanced electronics is reshaping supplier strategies, while global supply-chain restructuring is encouraging regional production of specialty polymer materials.

Modern heat-shrinkable solutions provide measurable advantages over traditional insulation methods, with automated installation technologies reducing assembly time by nearly 25% compared with manual protection techniques. Asia Pacific leads through large-scale manufacturing ecosystems, while North America focuses on aerospace, defense, and semiconductor applications requiring high-performance materials. Europe emphasizes sustainable materials and regulatory compliance within automotive and energy sectors.

Operational deployments in EV battery systems and charging infrastructure demonstrate how manufacturers are integrating heat-shrinkable tubing into safety-critical applications. Companies are increasing investments in material innovation, forming technology partnerships, and expanding localized production facilities to reduce dependency on overseas supply chains. The market’s future relevance will depend on delivering durable, sustainable, and application-specific solutions that strengthen industrial competitiveness and long-term operational resilience.

The rapid expansion of electric vehicles, renewable power systems, and advanced electronics is accelerating demand for heat-shrinkable tubing as industries require enhanced insulation, sealing, and thermal protection. Electric vehicle production in China surpassed 10 million units annually, increasing demand for battery wiring protection solutions, while automotive electronics content has grown by over 20% in recent vehicle platforms. Aerospace and industrial manufacturers are shifting toward flame-retardant and high-temperature materials. Companies are responding through polymer innovation, manufacturing expansion, and strategic partnerships to supply lightweight, durable tubing solutions that improve system reliability and reduce maintenance requirements.

Fluctuations in specialty polymers such as polyolefin, fluoropolymer, and elastomer materials remain a key constraint for manufacturers, with raw material prices experiencing variations of nearly 15–20% during recent supply disruptions. Dependence on limited chemical suppliers in countries such as China and Japan increases procurement risks for global producers. Compliance requirements for halogen-free and environmentally safer materials also raise production complexity by 10–15% in some applications. Companies are mitigating these pressures through supplier diversification, localized material sourcing, long-term procurement contracts, and investments in alternative polymer technologies to stabilize margins and improve production continuity.

Growing adoption of advanced materials creates opportunities for heat-shrinkable tubing manufacturers to serve high-performance applications in EV batteries, aerospace systems, and renewable energy infrastructure. Demand for flame-retardant and high-temperature-resistant tubing is increasing, with premium solutions representing nearly 40% of new industrial installations. Automation-driven manufacturing can improve production efficiency by approximately 20% while reducing material waste. Countries such as India are expanding electronics and EV manufacturing ecosystems, creating new demand channels. Companies are investing in R&D, automated extrusion technologies, and application-specific solutions to capture emerging opportunities in next-generation electrical protection systems.

Heat-shrinkable tubing suppliers face increasing execution challenges as industries demand customized solutions for extreme temperatures, compact designs, and safety-critical applications. Advanced automotive and aerospace systems require materials capable of operating beyond 150°C, increasing testing and certification complexity by nearly 25%. Growing integration of high-voltage EV architectures also requires improved insulation reliability and specialized installation processes. Manufacturers must address workforce skill gaps, advanced testing requirements, and evolving compliance standards across countries such as Germany, the United States, and Japan. Companies are investing in engineering capabilities, certification programs, and collaborative development models to maintain deployment consistency and long-term competitiveness.

Advanced Material Adoption Rising Heat-shrinkable tubing manufacturers are increasingly shifting toward fluoropolymer, polyolefin, and halogen-free materials to meet demanding electrical protection requirements. Premium high-temperature tubing solutions now represent nearly 40% of new industrial applications, while flame-retardant variants are gaining adoption in automotive and aerospace systems. Stricter safety requirements in electric vehicles and industrial electronics are accelerating material upgrades. Companies are expanding specialty polymer portfolios and investing in localized production capabilities to improve reliability, reduce supply risks, and support customized application requirements.

EV Wiring Systems Expanding Rapidly The transition toward electric mobility is reshaping heat-shrinkable tubing demand, with EV platforms requiring approximately 20–30% more cable protection components than conventional vehicles. Battery packs, charging systems, and high-voltage connections are driving adoption of insulation and sealing solutions. China’s EV manufacturing ecosystem and growing battery production capacity are creating large-scale deployment opportunities. Automotive suppliers are responding through partnerships with EV manufacturers, automated assembly integration, and development of lightweight tubing designs for improved thermal performance.

Automation Improves Manufacturing Efficiency Heat-shrinkable tubing production is becoming increasingly automated through precision extrusion, digital quality monitoring, and intelligent inspection systems. Automated manufacturing processes improve production efficiency by around 20% and reduce material waste by nearly 15%. Labor shortages in manufacturing hubs such as Germany and Japan are accelerating investments in smart production workflows. Companies are deploying advanced machinery and digital manufacturing platforms to achieve consistent quality, faster delivery cycles, and improved operational scalability.

Localized Supply Chains Strengthening Global manufacturers are restructuring sourcing strategies as chemical supply disruptions expose dependency risks in specialty polymer availability. Regionalized production investments have increased, with suppliers targeting 10–15% reductions in logistics exposure through closer manufacturing networks. The shift toward domestic sourcing in the United States, India, and Europe is strengthening supply resilience. Companies are establishing regional partnerships, expanding production facilities, and diversifying raw material suppliers to maintain stable operations and support growing industrial demand.

Polyolefin heat-shrinkable tubing dominates the market due to its cost efficiency, broad temperature resistance, and suitability across automotive, electronics, and industrial applications. This segment accounts for nearly 55% of overall demand because of its balance between durability, flexibility, and manufacturing scalability. Polyolefin solutions remain preferred for wire harness protection, electrical insulation, and general-purpose applications, while silicone and fluoropolymer tubing serve specialized high-temperature and chemical-resistant environments. Fluoropolymer and advanced specialty tubing represent the fastest-growing type segment as aerospace, EV battery systems, and semiconductor applications require enhanced performance characteristics. Adoption of premium materials is increasing by approximately 8–10% annually as manufacturers prioritize thermal stability and safety compliance. Companies are expanding specialty product lines, developing halogen-free alternatives, and investing in advanced extrusion technologies to capture higher-value applications.

Electrical insulation represents the leading application segment due to extensive use in wire harnesses, connectors, terminals, and power distribution systems. The segment contributes nearly 50% of market demand as industries require reliable protection against moisture, vibration, and temperature fluctuations. Automotive electronics, industrial machinery, and consumer devices continue adopting heat-shrinkable tubing to improve safety and reduce maintenance requirements. Automotive and EV applications are emerging as the fastest-growing segment, supported by increasing high-voltage wiring requirements and battery system complexity. EV platforms use significantly more electrical components, creating approximately 25% higher demand for advanced insulation solutions compared with conventional vehicles. Telecommunications, aerospace, and renewable energy applications are also expanding as infrastructure modernization accelerates. Companies are responding by developing application-specific tubing, integrating automated installation systems, and forming partnerships with electrical component manufacturers.

The automotive industry remains the largest end-user segment, driven by large-scale vehicle production, expanding electronics integration, and rapid EV adoption. Automotive manufacturers account for approximately 45% of demand due to extensive use in wiring harnesses, battery systems, sensors, and electrical connections. Traditional vehicle manufacturers continue upgrading electrical architectures, while EV producers are increasing demand for high-performance insulation materials. The aerospace and renewable energy sectors represent the fastest-growing end-user groups as they require durable protection solutions for harsh operating conditions. Aerospace applications are expanding through lightweight wiring systems, while solar and wind infrastructure deployments are increasing demand for weather-resistant electrical components by nearly 10–12%. Electronics manufacturers and industrial equipment producers remain important contributors through automation and connected device growth. Companies are targeting these segments through customized engineering solutions, strategic supply agreements, and expanded manufacturing networks.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of5.2% between 2026 and 2033.

North America holds approximately 25% of global demand, supported by aerospace manufacturing, EV production, semiconductor facilities, and advanced electrical infrastructure. The United States represents the largest contributor due to strong adoption of high-temperature and flame-retardant tubing in defense, automotive, and industrial applications. Growing investments in domestic electronics and battery manufacturing are increasing demand for localized component suppliers. More than 60% of newly developed EV platforms in the region incorporate advanced cable protection solutions, encouraging manufacturers to expand specialty tubing production and strengthen partnerships with automotive and aerospace companies.

United States Market Outlook: The United States leads regional adoption through its aerospace, defense, and electric mobility industries. Domestic EV battery manufacturing investments exceeding USD 100 billion in recent years are creating additional demand for reliable insulation and protection components. Manufacturers are prioritizing advanced polymer solutions, automated production, and supply-chain localization to reduce dependency on overseas material sources.

Europe accounts for nearly 20% of global heat-shrinkable tubing demand, supported by automotive electrification, industrial automation, and renewable energy modernization. Germany, France, and the United Kingdom are major deployment centers where manufacturers require high-performance insulation materials for automotive wiring, machinery, and energy systems. Sustainability regulations and stricter vehicle safety standards are accelerating adoption of halogen-free and recyclable tubing materials. European suppliers are increasing investments in advanced polymer development, with automated manufacturing improving production efficiency by nearly 15–20% across specialized applications.

Germany Market Outlook: Germany remains the strongest European market due to its automotive manufacturing ecosystem and engineering capabilities. The country’s automotive sector produces millions of vehicles annually, creating consistent demand for electrical protection systems. Manufacturers are focusing on lightweight materials, EV-specific tubing designs, and localized supplier networks to support next-generation vehicle platforms.

Asia-Pacific dominates the global market with approximately 42% share, driven by large-scale electronics manufacturing, EV production, telecommunications expansion, and industrial automation. China, Japan, South Korea, and India represent key production and consumption centers. China’s position as the world’s largest EV manufacturing hub and electronics supplier is creating extensive demand for cable protection components. The region contributes over 50% of global electronics production capacity, strengthening the need for reliable insulation solutions. Companies are expanding manufacturing facilities, improving export capabilities, and developing cost-efficient advanced materials.

China Market Outlook: China remains the largest country market due to its extensive EV, electronics, and semiconductor manufacturing infrastructure. The country produces over 10 million electric vehicles annually, increasing demand for high-voltage cable protection systems. Domestic and international suppliers are expanding polymer production, automation capabilities, and partnerships with automotive manufacturers to capture growing industrial requirements.

South America represents nearly 7% of global demand, with Brazil and Argentina leading adoption across energy, automotive, mining, and telecommunications sectors. Infrastructure modernization and renewable energy expansion are increasing requirements for durable electrical protection solutions. Brazil’s power transmission upgrades and industrial automation investments are supporting demand growth, although limited local specialty polymer production creates supply dependency challenges. Companies are strengthening regional distribution networks and forming partnerships with industrial suppliers to improve availability. Renewable energy projects have increased electrical component demand by approximately 10% in major infrastructure developments.

Brazil Market Outlook: Brazil is the largest regional market due to its industrial base, automotive manufacturing activity, and expanding renewable energy sector. The country has one of the largest solar energy markets in Latin America, driving demand for weather-resistant electrical protection products. Suppliers are focusing on localized inventory management and partnerships to improve project delivery efficiency.

Middle East & Africa accounts for approximately 6% of global demand, supported by oil and gas modernization, renewable energy projects, telecommunications expansion, and industrial infrastructure development. Countries such as Saudi Arabia and the United Arab Emirates are increasing investments in smart infrastructure and power networks, creating demand for reliable electrical protection systems. Large-scale energy projects are accelerating adoption of advanced tubing solutions, with infrastructure spending increasing demand for industrial electrical components by more than 8% annually in key markets. Companies are expanding distribution partnerships and establishing regional supply networks.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategic market due to energy infrastructure upgrades, industrial diversification programs, and renewable energy investments. The country’s utility-scale solar projects and industrial expansion initiatives are increasing demand for durable electrical insulation solutions. Suppliers are targeting partnerships with infrastructure developers and energy companies to support large deployment programs.

The Heat-Shrinkable Tubing Market features global technology leaders such as TE Connectivity, 3M, and Sumitomo Electric Industries competing with regional specialists and cost-focused manufacturers. The top five players collectively control approximately 45% of market share. Competition is shaped by advanced materials, customization, supply reliability, and production scale, with premium tubing providers achieving 10–15% higher pricing through specialized solutions. Companies compete through polymer innovation, manufacturing expansion, partnerships, and vertical integration. Global suppliers are strengthening supply chains while regional producers compete through cost efficiency and faster delivery. Entry barriers remain high due to certification requirements, material expertise, and automotive/aerospace qualification processes. Winning players will combine material innovation, localized production, application engineering, and reliable global supply networks.

3M

Sumitomo Electric Industries

HellermannTyton

Molex

Alpha Wire

Panduit

Prysmian Group

Avery Dennison

Woer

Dasheng Group

Changyuan Group

Heat-shrinkable tubing technology is advancing through high-performance polymers, flame-retardant formulations, and adhesive-lined designs. Modern polyolefin and fluoropolymer materials improve temperature resistance, durability, and chemical protection by approximately 15–20% compared with conventional insulation methods. Adoption is increasing in EV batteries, aerospace wiring, and industrial automation systems where reliability is critical. Manufacturers are prioritizing lightweight materials and application-specific engineering.

Automation and digital manufacturing are transforming production workflows through precision extrusion, automated inspection, and quality monitoring systems. These technologies reduce material waste by nearly 15% and improve manufacturing consistency. Companies with advanced production capabilities gain advantages through faster customization, lower defect rates, and improved delivery reliability.

Between 2026 and 2028, smart materials, recyclable polymers, and integrated cable protection solutions will shape competitive positioning. Advanced tubing suppliers benefit from partnerships with EV manufacturers, aerospace companies, and electronics producers. The transition from standard insulation products toward engineered protection systems creates stronger differentiation for technology-focused manufacturers.

March 2025, HellermannTyton expanded its heat-shrink tubing portfolio with updated polyolefin solutions supporting insulation and abrasion protection applications. The range includes multiple sizes and performance options, improving industrial customization capabilities across electrical markets. Source: www.hellermanntyton.com

February 2025, TE Connectivity strengthened its heat-shrink tubing offering with advanced RAYCHEM solutions covering single-wall, dual-wall, and specialized protection requirements. Products support automotive, industrial, and connector applications with improved installation flexibility and performance.

November 2024, TE Connectivity expanded availability of medical-grade crosslinked polyolefin heat-shrink tubing products featuring 4:1 shrink capability. The development supports compact medical device assemblies requiring precise insulation and protection performance.

January 2025, HellermannTyton introduced enhanced heat-shrink tubing product specifications emphasizing mechanical protection, corrosion resistance, and industrial compliance. The portfolio supports operating temperatures up to 125°C and strengthens reliability-focused applications.

The Heat-Shrinkable Tubing Market Report covers detailed analysis across product types including polyolefin, fluoropolymer, silicone, and specialty tubing solutions. The study evaluates applications across electrical insulation, automotive wiring, aerospace systems, electronics, telecommunications, and energy infrastructure, along with end-user analysis covering automotive, industrial, aerospace, electronics, and utility sectors.

The report provides regional insights across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting manufacturing trends, technology adoption, supply-chain developments, and competitive positioning. It examines emerging areas such as EV battery protection, smart materials, recyclable polymers, and automated installation processes. The analysis supports investment planning, supplier evaluation, expansion strategies, and competitive decision-making through 2026–2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 160.0 Million |

| Market Revenue (2033) | USD 227.5 Million |

| CAGR (2026–2033) | 4.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | TE Connectivity; 3M; Sumitomo Electric Industries; HellermannTyton; Molex; Alpha Wire; Panduit; Prysmian Group; Avery Dennison; Woer; Dasheng Group; Changyuan Group |

| Customization & Pricing | Available on Request (10% Customization Free) |