Reports

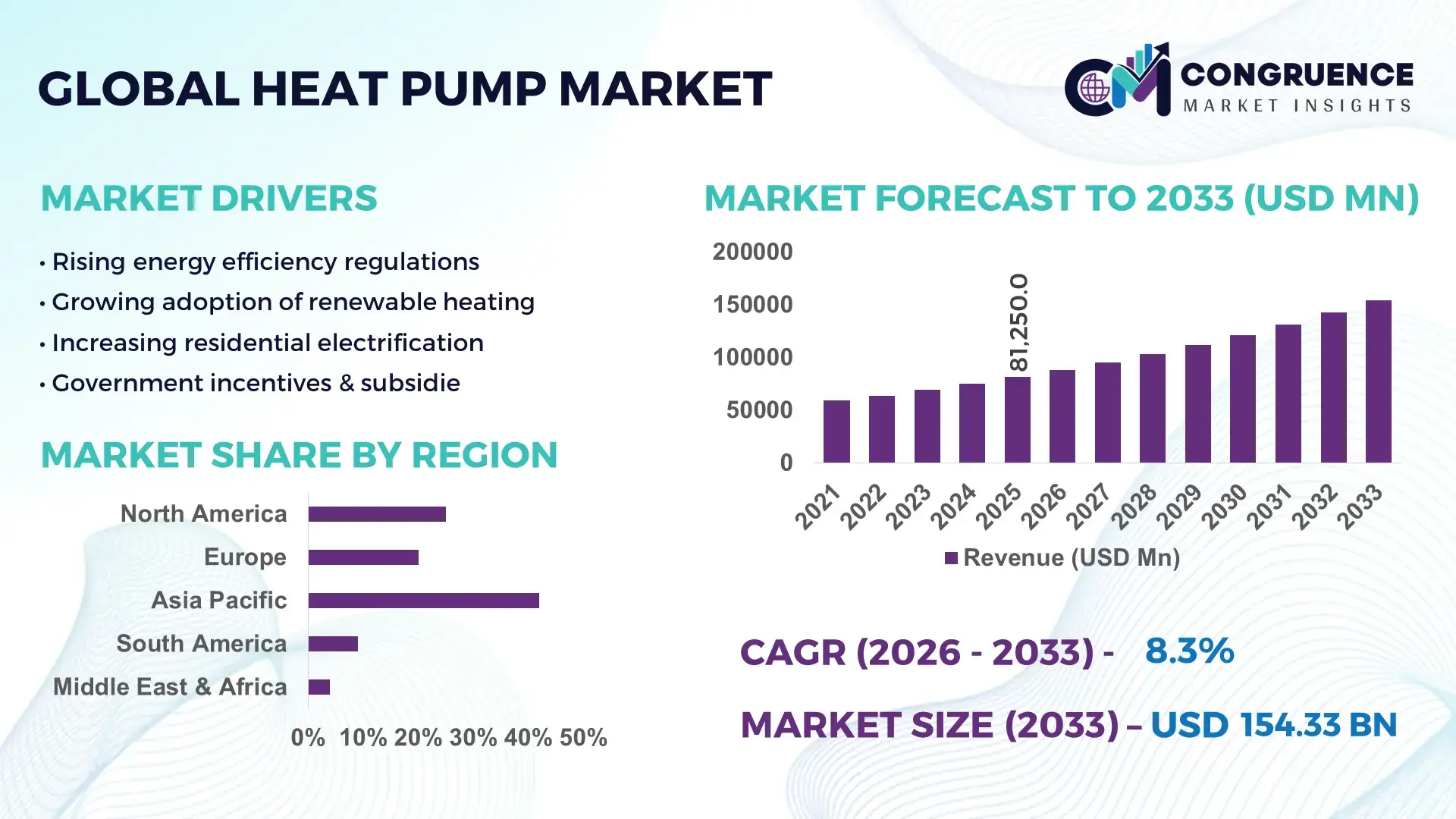

The Global Heat Pump Market was valued at USD 81250 Million in 2025 and is anticipated to reach a value of USD 154331.5 Million by 2033 expanding at a CAGR of 8.35% between 2026 and 2033. This growth is primarily driven by increasing demand for energy-efficient heating and cooling solutions across residential and industrial sectors.

China stands at the forefront of the global heat pump market, supported by large-scale manufacturing capacity and strong domestic deployment. The country produces over 40 million heat pump units annually, backed by extensive industrial clusters in provinces such as Guangdong and Zhejiang. Government-backed electrification initiatives have led to adoption across more than 30% of newly constructed residential buildings. Industrial applications, including district heating and food processing, contribute significantly to utilization rates. China has also invested over USD 10 billion in heat pump-related infrastructure and R&D programs, focusing on high-temperature heat pumps and low-GWP refrigerants. Advanced inverter-driven compressors and smart control systems are increasingly integrated, enhancing operational efficiency by up to 25% compared to conventional systems.

Market Size & Growth: USD 81250 Million in 2025, projected to reach USD 154331.5 Million by 2033, growing at 8.35%, driven by energy efficiency mandates and electrification trends.

Top Growth Drivers: Energy efficiency adoption (45%), carbon emission reduction initiatives (38%), smart home integration (32%).

Short-Term Forecast: By 2028, system efficiency is expected to improve by 20% due to advanced compressor technologies and digital monitoring.

Emerging Technologies: AI-driven energy optimization, low-GWP refrigerants, and hybrid heat pump systems integrating solar energy.

Regional Leaders: Asia-Pacific projected at USD 62 billion by 2033 with rapid urban deployment; Europe at USD 48 billion driven by policy mandates; North America at USD 35 billion with strong retrofit demand.

Consumer/End-User Trends: Residential sector accounts for over 55% of installations, with growing preference for air-to-water systems in colder climates.

Pilot or Case Example: In 2024, a Scandinavian district heating project achieved 28% energy savings using large-scale heat pump systems.

Competitive Landscape: Market leader holds approximately 18% share, followed by major players including diversified HVAC manufacturers and regional specialists.

Regulatory & ESG Impact: Carbon neutrality targets and building efficiency codes are driving adoption, with incentives covering up to 30% of installation costs in key regions.

Investment & Funding Patterns: Over USD 15 billion invested globally in clean heating technologies, with increasing venture funding in smart HVAC startups.

Innovation & Future Outlook: Integration with IoT platforms, predictive maintenance, and high-temperature industrial heat pumps are shaping future demand.

The heat pump market continues to evolve across key industry sectors including residential housing, commercial infrastructure, and industrial heating, contributing approximately 55%, 25%, and 20% respectively to total demand. Technological advancements such as variable-speed compressors, CO₂-based refrigerants, and AI-enabled energy management systems are improving system efficiency by up to 30%. Regulatory frameworks promoting decarbonization and phasing out fossil fuel-based heating systems are accelerating market penetration, particularly in Europe and Asia-Pacific. Urbanization and electrification trends are boosting demand in emerging economies, while retrofit installations are expanding in developed regions. The market outlook remains robust with increasing integration of renewable energy sources and digitalized HVAC ecosystems.

The strategic relevance of the heat pump market lies in its central role in global decarbonization and energy transition strategies. As governments intensify carbon reduction targets, heat pumps are becoming a preferred alternative to fossil fuel-based heating systems, particularly in residential and commercial applications. Advanced inverter-driven heat pump technology delivers nearly 35% improvement in energy efficiency compared to traditional electric resistance heating systems, significantly reducing operational costs and emissions. Asia-Pacific dominates in volume due to large-scale production and deployment, while Europe leads in adoption, with over 40% of households in certain countries integrating heat pump systems.

By 2028, AI-enabled predictive maintenance and smart grid integration are expected to reduce system downtime by 25% while optimizing energy consumption patterns. Companies are increasingly aligning with ESG commitments, targeting up to 50% emission reduction in building operations by 2030 through heat pump adoption. In 2024, a leading European utility achieved a 22% reduction in energy consumption by deploying AI-integrated heat pump networks across urban districts, demonstrating measurable operational benefits.

From a strategic standpoint, investments in hybrid systems combining heat pumps with solar and thermal storage are gaining traction, enabling flexible and resilient energy systems. Regulatory frameworks such as zero-emission building mandates and financial incentives are further accelerating adoption. The heat pump market is poised to become a cornerstone of sustainable infrastructure, offering scalable, efficient, and environmentally compliant solutions that align with long-term energy transition goals.

Energy efficiency regulations are playing a pivotal role in driving the growth of the heat pump market by mandating reductions in building energy consumption and emissions. Governments across Europe and North America have introduced policies requiring new constructions to meet near-zero energy standards, significantly boosting demand for efficient heating solutions. Heat pumps can achieve efficiency levels exceeding 300%, meaning they generate three units of heat for every unit of electricity consumed. This efficiency advantage is compelling for both residential and commercial users seeking to lower energy costs. Additionally, subsidy programs covering up to 30% of installation costs are making heat pumps more financially viable. The electrification of heating systems is further supported by carbon pricing mechanisms, encouraging industries to transition away from fossil fuels and adopt heat pump technologies.

Despite long-term energy savings, high initial installation costs remain a significant barrier to widespread heat pump adoption. Installation expenses can be 2 to 3 times higher than conventional heating systems due to equipment complexity, system design requirements, and skilled labor needs. In retrofit scenarios, additional costs arise from infrastructure modifications such as insulation upgrades and electrical system enhancements. In developing regions, limited access to financing options further restricts adoption. Moreover, fluctuating raw material prices, particularly for components like compressors and heat exchangers, contribute to cost variability. While operational savings can offset initial investments over time, the lack of immediate affordability continues to deter price-sensitive consumers and small businesses.

The integration of renewable energy sources with heat pump systems presents significant growth opportunities for the market. Hybrid systems combining heat pumps with solar photovoltaic and thermal systems are gaining popularity, enabling users to achieve higher energy independence and reduced operational costs. In regions with high solar irradiance, such systems can reduce electricity consumption by up to 40%. Additionally, advancements in thermal energy storage technologies are allowing excess renewable energy to be stored and utilized efficiently. Industrial applications are also exploring high-temperature heat pumps for waste heat recovery, improving energy utilization by up to 25%. These developments are opening new avenues for innovation and investment, particularly in smart energy systems and decentralized heating networks.

Technical limitations and climate variability pose notable challenges to heat pump performance, particularly in extremely cold regions. Efficiency tends to decline at temperatures below -10°C, requiring supplementary heating systems to maintain performance levels. This can increase overall energy consumption and system complexity. Additionally, improper system sizing and installation can lead to reduced efficiency and higher maintenance costs. The availability of skilled technicians for installation and servicing is another constraint, especially in emerging markets. Refrigerant regulations and the transition to low-GWP alternatives also present technical and compliance challenges for manufacturers. Addressing these issues requires continuous innovation in compressor technology, system design, and workforce training to ensure reliable and efficient operation across diverse climatic conditions.

• Rapid Electrification Driving 48% Increase in Residential Installations:

The shift toward electrified heating solutions is significantly influencing heat pump adoption, particularly in residential sectors. In 2024, over 48% of newly constructed homes in developed markets integrated heat pump systems as primary heating solutions. Electrification initiatives supported by government incentives and energy transition policies have accelerated installations by more than 35% compared to conventional systems. Air-to-water heat pumps are gaining traction due to their ability to reduce household energy consumption by up to 30%, while maintaining consistent thermal output. This trend is further reinforced by increasing consumer preference for low-emission heating technologies.

• Expansion of High-Temperature Heat Pumps Improving Industrial Efficiency by 25%:

Industrial adoption of high-temperature heat pumps is expanding rapidly, particularly in sectors such as food processing, chemicals, and district heating. These systems can achieve output temperatures exceeding 120°C, enabling replacement of fossil fuel-based boilers. Industrial facilities deploying advanced heat pumps have reported efficiency improvements of approximately 25% and energy savings exceeding 20%. Around 18% of industrial heating processes in Europe have already transitioned to heat pump-based systems, highlighting growing acceptance in heavy-duty applications. This trend reflects a broader move toward decarbonizing industrial heat demand.

• Integration of Smart and IoT-Enabled Systems Enhancing Performance by 22%:

Smart heat pump systems equipped with IoT connectivity and AI-based control algorithms are becoming increasingly prevalent. These systems enable real-time monitoring, predictive maintenance, and automated energy optimization, improving operational efficiency by up to 22%. Approximately 40% of newly installed heat pumps in advanced markets now include smart control features, allowing integration with home automation and energy management platforms. The use of cloud-based analytics is also enabling users to reduce maintenance costs by nearly 15% while improving system lifespan through proactive fault detection.

• Adoption of Low-GWP Refrigerants Reducing Environmental Impact by 35%:

The transition toward environmentally sustainable refrigerants is reshaping product innovation in the heat pump market. Low-global warming potential refrigerants such as R-290 and CO₂ are being widely adopted, reducing greenhouse gas emissions by up to 35% compared to traditional refrigerants. Regulatory mandates in Europe and Asia have led to over 50% of new heat pump models incorporating low-GWP alternatives. Manufacturers are investing heavily in redesigning systems to accommodate these refrigerants while maintaining performance standards, resulting in improved compliance with environmental regulations and enhanced sustainability profiles.

The heat pump market is segmented across types, applications, and end-user categories, each contributing distinctively to overall demand patterns. Air-source, ground-source, and water-source heat pumps dominate the product landscape, with varying adoption levels depending on climate conditions and infrastructure availability. In terms of applications, residential heating leads the market due to widespread electrification initiatives, followed by commercial and industrial uses driven by energy efficiency requirements. End-user segmentation highlights residential consumers as the largest segment, while industrial users are rapidly increasing adoption for process heating and waste heat recovery. Approximately 55% of installations are concentrated in residential settings, with commercial and industrial sectors accounting for 25% and 20% respectively. Regional consumption patterns also vary, with colder climates favoring high-capacity systems and urban areas driving demand for compact, energy-efficient solutions.

Air-source heat pumps currently account for approximately 62% of total installations, making them the leading segment due to lower installation complexity and cost-effectiveness. These systems are widely adopted in both residential and light commercial applications, particularly in regions with moderate climates. Ground-source heat pumps represent around 23% of the market, offering higher efficiency levels but requiring significant upfront investment and land availability. Water-source heat pumps and hybrid systems collectively contribute nearly 15%, serving niche applications such as district heating and large commercial facilities. Ground-source heat pumps are the fastest-growing segment, expanding at an estimated CAGR of 9.8%, driven by their superior efficiency, which can exceed 400% under optimal conditions. Increasing adoption is supported by government incentives and rising awareness of long-term energy savings. Hybrid systems integrating solar thermal and heat pump technologies are also gaining momentum, particularly in regions aiming for net-zero building standards.

Residential heating dominates the application segment, accounting for approximately 55% of total usage, driven by increasing electrification and demand for energy-efficient home heating systems. Commercial applications, including office buildings, retail spaces, and hospitality, represent about 25% of the market, benefiting from regulatory requirements for energy-efficient infrastructure. Industrial applications contribute around 20%, focusing on process heating and waste heat recovery. Industrial applications are the fastest-growing segment, with an estimated CAGR of 10.2%, supported by the rising need for decarbonizing industrial operations. High-temperature heat pumps are enabling industries to replace conventional boilers, improving energy efficiency by up to 25%. District heating systems are also integrating large-scale heat pumps to enhance energy utilization.

Residential users lead the market with approximately 55% share, driven by rising consumer awareness, government incentives, and increasing adoption of smart home technologies. Commercial end-users account for about 25%, with growing demand for sustainable HVAC systems in office complexes, healthcare facilities, and retail environments. Industrial end-users contribute nearly 20%, focusing on energy-intensive processes and waste heat recovery. Industrial end-users represent the fastest-growing segment, expanding at an estimated CAGR of 10.5%, fueled by regulatory pressure to reduce emissions and improve energy efficiency. Adoption rates in sectors such as food processing and chemicals have increased by over 18% in recent years. Additionally, smart heat pump systems are being deployed in commercial buildings, enhancing energy management capabilities and reducing operational costs by up to 20%.

Region Asia-Pacific accounted for the largest market share at 42% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 9.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high manufacturing output exceeding 45 million units annually, with China and Japan contributing over 70% of regional production. Europe holds approximately 30% share, driven by policy-driven adoption, with over 3 million units installed annually across residential and commercial sectors. North America captures nearly 18% of the market, with more than 4.5 million operational heat pump systems, particularly in the United States and Canada. South America accounts for around 5%, with Brazil contributing nearly 60% of regional demand, while the Middle East & Africa holds close to 5%, supported by infrastructure development and increasing cooling demand. Installation density in colder European countries exceeds 120 units per 1,000 households, compared to 45 units per 1,000 households in Asia-Pacific, indicating varying adoption maturity across regions.

How is rapid electrification transforming heating system adoption across key industries?

North America holds approximately 18% of the global heat pump market share, with strong demand driven by residential retrofits and commercial infrastructure upgrades. Over 60% of installations are concentrated in the residential sector, while commercial applications such as healthcare and retail contribute nearly 25%. Government initiatives, including tax credits covering up to 30% of installation costs, are accelerating adoption. Electrification policies and building efficiency standards are encouraging replacement of fossil fuel-based heating systems. Technological advancements such as cold-climate heat pumps capable of operating at temperatures below -20°C are enhancing performance reliability. A leading regional manufacturer has expanded production capacity by 35% to meet increasing demand for inverter-based systems. Consumer behavior shows a growing preference for energy-efficient and smart-enabled HVAC systems, with nearly 40% of new installations integrating IoT-based controls.

What role do stringent energy policies play in accelerating sustainable heating adoption?

Europe accounts for nearly 30% of the global heat pump market, with countries such as Germany, France, and the UK leading adoption. Over 3 million units are installed annually, supported by strict environmental regulations and carbon reduction targets. Regulatory frameworks promoting zero-emission buildings and phasing out fossil fuel boilers are significantly influencing market growth. Approximately 50% of new residential constructions in Northern Europe now include heat pump systems. Advanced technologies such as CO₂-based refrigerants and hybrid heating systems are widely adopted, improving efficiency by up to 28%. A prominent European manufacturer has introduced next-generation heat pumps with integrated energy storage, increasing operational efficiency by 20%. Consumer behavior reflects strong environmental awareness, with over 45% of households prioritizing low-emission heating solutions.

Why is manufacturing scale and urban expansion driving unprecedented system deployment?

Asia-Pacific leads the market in volume, producing over 45 million heat pump units annually and accounting for approximately 42% of global demand. China, Japan, and India are the top consuming countries, with China alone contributing more than 60% of regional installations. Rapid urbanization and infrastructure expansion are driving demand, particularly in residential and district heating applications. Industrial adoption is also increasing, with over 20% of manufacturing facilities integrating heat pump systems for process heating. Technological innovation hubs in Japan and South Korea are advancing high-efficiency compressors and smart control systems, improving performance by up to 25%. A major regional manufacturer has scaled production by 40% to support export demand. Consumer behavior highlights strong adoption in urban households, with increasing preference for compact and energy-efficient systems.

How are energy diversification efforts shaping demand for efficient heating solutions?

South America accounts for approximately 5% of the global heat pump market, with Brazil and Argentina as key contributors. Brazil represents nearly 60% of regional demand, driven by growing construction activities and energy diversification initiatives. The adoption of heat pumps is increasing in commercial and hospitality sectors, which account for nearly 35% of installations. Government incentives aimed at reducing energy consumption are encouraging adoption, particularly in urban areas. Infrastructure development projects are also supporting market growth, with over 20% of new commercial buildings integrating energy-efficient HVAC systems. A regional manufacturer has introduced cost-effective heat pump models tailored for local climate conditions, improving accessibility. Consumer behavior shows rising awareness of energy efficiency, with adoption increasing by over 15% in residential segments.

What factors are driving the transition toward energy-efficient climate control systems?

The Middle East & Africa region holds close to 5% of the global heat pump market, with demand driven by construction, oil & gas, and commercial sectors. Countries such as the UAE and South Africa are leading adoption, supported by infrastructure modernization and sustainability initiatives. Over 25% of new commercial buildings in urban areas are incorporating heat pump systems for climate control. Technological advancements include integration with smart building management systems, improving energy efficiency by up to 18%. Trade partnerships and government regulations promoting energy-efficient technologies are further supporting market growth. A local player has launched solar-integrated heat pump systems, reducing electricity consumption by nearly 30%. Consumer behavior reflects increasing demand for sustainable cooling solutions, particularly in high-temperature regions.

China – 38% market share in the Heat Pump market, driven by large-scale manufacturing capacity and extensive residential adoption.

Germany – 12% market share in the Heat Pump market, supported by strong regulatory frameworks and widespread deployment in energy-efficient buildings.

The heat pump market is moderately fragmented, with over 120 active global and regional players competing across residential, commercial, and industrial segments. The top five companies collectively account for approximately 45% of the total market share, indicating a balanced mix of consolidation and competitive diversity. Leading players are focusing on product innovation, particularly in inverter-driven systems and low-GWP refrigerants, to enhance efficiency and meet regulatory standards. Strategic partnerships and joint ventures are increasingly common, with over 25 major collaborations recorded in the past three years aimed at expanding manufacturing capacity and technological capabilities.

Product launches remain a key competitive strategy, with more than 150 new heat pump models introduced globally in 2024 alone, featuring advanced digital controls and smart connectivity. Companies are also investing heavily in R&D, with average annual spending accounting for nearly 6% of operational budgets. Regional manufacturers are gaining traction by offering cost-effective solutions tailored to local markets, intensifying competition. Additionally, mergers and acquisitions are shaping the competitive landscape, with over 10 notable deals completed recently to strengthen market positioning and expand geographic reach. The increasing focus on sustainability and energy efficiency is driving continuous innovation, making competition highly dynamic and technology-driven.

Daikin Industries Ltd.

Mitsubishi Electric Corporation

Panasonic Corporation

Bosch Thermotechnology

Carrier Global Corporation

Trane Technologies plc

NIBE Industrier AB

Viessmann Group

Johnson Controls International plc

LG Electronics Inc.

Fujitsu General Limited

Samsung Electronics Co., Ltd.

Technological advancements in the heat pump market are significantly enhancing system efficiency, operational flexibility, and environmental compliance. One of the most impactful innovations is the adoption of variable-speed inverter compressors, which improve energy efficiency by up to 30% compared to fixed-speed systems by adjusting output based on real-time demand. These systems are now integrated in nearly 65% of newly installed residential heat pumps, reducing electricity consumption and improving temperature consistency.

The transition toward low-global warming potential refrigerants such as R-290 and CO₂ is another critical development, with over 50% of new models in Europe and Asia incorporating these alternatives. These refrigerants reduce greenhouse gas emissions by up to 35% while maintaining high thermal performance. High-temperature heat pumps are also gaining traction, capable of delivering output temperatures exceeding 120°C, enabling industrial applications such as chemical processing and district heating. Approximately 20% of industrial heating systems in advanced economies are now exploring heat pump integration for waste heat recovery.

Digital transformation is reshaping system management through IoT-enabled monitoring and AI-driven optimization. Smart heat pump systems can reduce maintenance costs by nearly 15% and improve operational uptime by over 20% through predictive analytics. Around 40% of commercial installations now feature cloud-based energy management platforms, allowing real-time performance tracking and remote diagnostics.

Additionally, hybrid heat pump systems combining solar photovoltaic and thermal technologies are improving overall system efficiency by up to 25%, particularly in regions with high solar irradiance. Thermal energy storage integration is also advancing, enabling load shifting and improved grid stability. These technological innovations are positioning heat pumps as a central component of smart, sustainable energy systems across residential, commercial, and industrial applications.

• In January 2025, Daikin Industries Ltd. announced the expansion of its European heat pump production capacity with a new manufacturing facility in Poland. The plant is expected to produce over 1 million units annually, strengthening supply chain resilience and supporting increasing demand for energy-efficient heating systems. Source: www.daikin.com

• In March 2025, Mitsubishi Electric Corporation launched a new series of residential air-to-water heat pumps featuring advanced inverter technology and low-GWP refrigerants. The system delivers up to 25% higher energy efficiency and supports smart home integration, targeting growing demand for sustainable residential heating solutions. Source: www.mitsubishielectric.com

• In September 2024, Carrier Global Corporation introduced a high-temperature heat pump solution designed for industrial applications, capable of achieving output temperatures above 120°C. The system demonstrated energy savings of up to 20% in pilot industrial installations, supporting decarbonization efforts in manufacturing sectors. Source: www.carrier.com

• In November 2024, Bosch Thermotechnology expanded its portfolio of CO₂-based heat pump systems for commercial buildings across Europe. These systems reduce carbon emissions by approximately 30% and are optimized for large-scale heating applications, aligning with stringent regional energy efficiency regulations. Source: www.bosch-thermotechnology.com

The Heat Pump Market Report provides a comprehensive analysis of industry dynamics across multiple dimensions, including product types, applications, end-user segments, and geographic regions. The report covers key product categories such as air-source, ground-source, and water-source heat pumps, which collectively account for over 90% of global installations. It also evaluates emerging segments such as hybrid systems and high-temperature industrial heat pumps, which are gaining traction due to their ability to improve energy efficiency by up to 25% in specialized applications.

From an application perspective, the report examines residential, commercial, and industrial usage, with residential installations representing approximately 55% of total demand. Commercial and industrial sectors are analyzed in terms of their adoption of advanced heating technologies, including district heating integration and waste heat recovery systems. The report also highlights sector-specific trends, such as increasing use of heat pumps in healthcare facilities, data centers, and manufacturing plants.

Geographically, the report spans key regions including Asia-Pacific, Europe, North America, South America, and the Middle East & Africa, with detailed insights into regional consumption patterns, installation density, and regulatory frameworks. Asia-Pacific leads in production volume with over 40 million units annually, while Europe demonstrates high adoption rates driven by stringent environmental policies.

The scope further includes technological advancements such as AI-enabled energy management, IoT-based monitoring systems, and low-GWP refrigerants, which are transforming system performance and compliance standards. Additionally, the report assesses competitive positioning, supply chain developments, and investment trends, providing decision-makers with actionable insights into current market conditions and future growth opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8.35% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Daikin Industries Ltd., Mitsubishi Electric Corporation, Panasonic Corporation, Bosch Thermotechnology, Carrier Global Corporation, Trane Technologies plc, NIBE Industrier AB, Viessmann Group, Johnson Controls International plc, LG Electronics Inc., Fujitsu General Limited, Samsung Electronics Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |