Reports

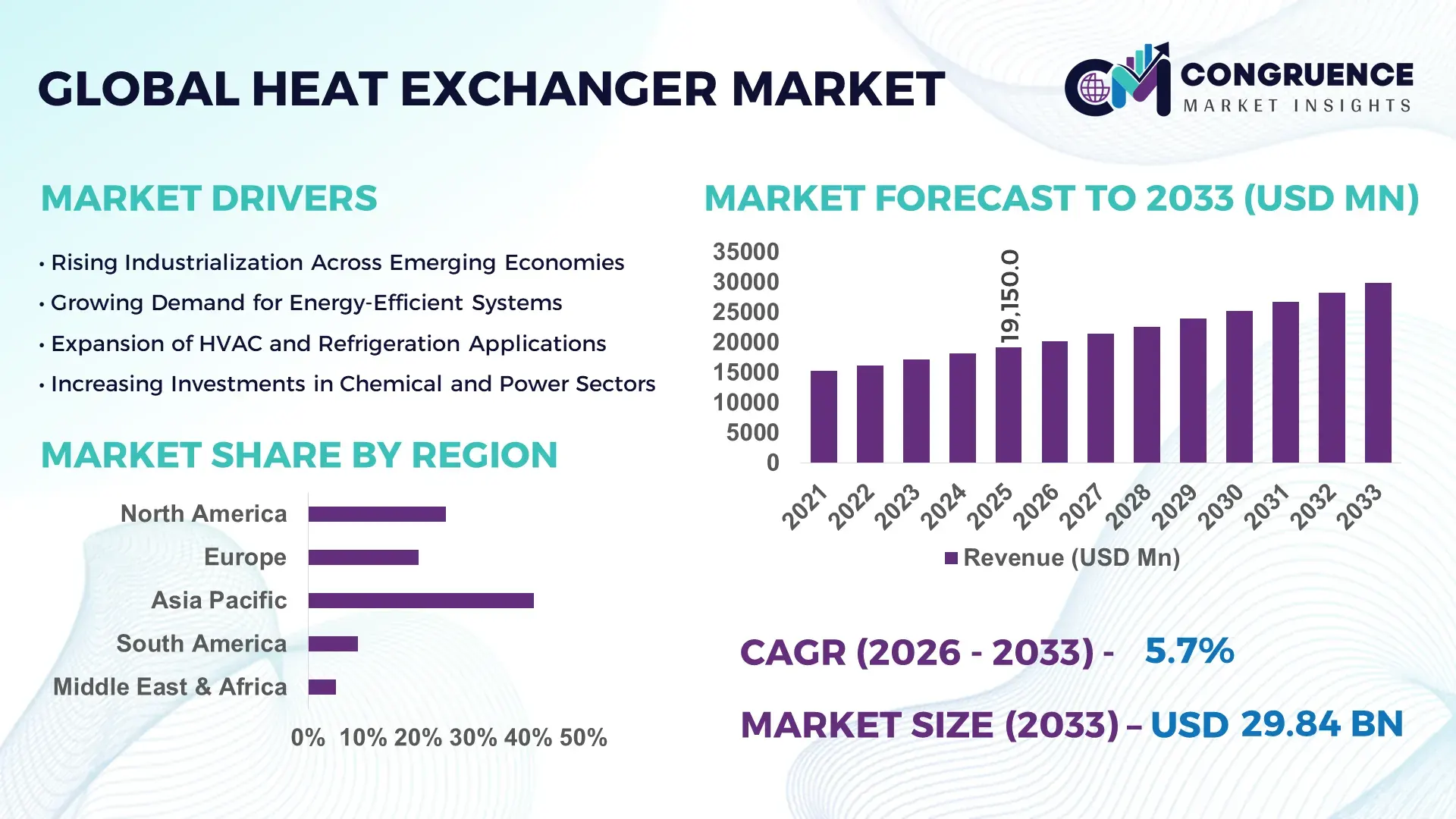

The Global Heat Exchanger Market was valued at USD 19150 Million in 2025 and is anticipated to reach a value of USD 29837.92 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. This growth is primarily driven by rising industrial energy efficiency requirements and stringent thermal management standards across key sectors.

China continues to lead the global heat exchanger landscape with robust industrial output and expanding manufacturing capabilities. The country accounts for over 35% of global heat exchanger production capacity, supported by more than 12,000 specialized manufacturers and component suppliers. Investments exceeding USD 8 billion have been directed toward thermal equipment modernization and smart factory upgrades between 2022 and 2025. The petrochemical, HVAC, and power generation sectors collectively contribute to over 60% of domestic demand. Advanced plate heat exchanger adoption has grown by nearly 18% annually, while district heating networks in major urban areas now utilize high-efficiency exchangers covering over 70% of urban households.

Market Size & Growth: Valued at USD 19150 Million in 2025, projected to reach USD 29837.92 Million by 2033 at 5.7% CAGR, driven by industrial energy optimization and emission reduction initiatives.

Top Growth Drivers: Industrial energy efficiency adoption rising by 32%, HVAC system upgrades increasing by 28%, renewable integration demand growing by 25%.

Short-Term Forecast: By 2028, advanced heat exchanger designs are expected to improve thermal efficiency by 15% and reduce operational costs by 12%.

Emerging Technologies: Microchannel heat exchangers, AI-based thermal optimization systems, and additive manufacturing for compact exchanger designs.

Regional Leaders: Asia-Pacific projected at USD 12 billion by 2033 with industrial expansion, Europe at USD 8.5 billion driven by sustainability mandates, North America at USD 7.2 billion with retrofit demand growth.

Consumer/End-User Trends: High adoption in chemical processing, HVAC, and power generation sectors with increasing focus on lifecycle efficiency.

Pilot or Case Example: In 2024, a refinery modernization project improved heat recovery efficiency by 20% using advanced plate exchangers.

Competitive Landscape: Leading player holds approximately 14% share, followed by major global manufacturers focusing on high-performance systems.

Regulatory & ESG Impact: Carbon reduction targets mandate up to 30% efficiency improvements in industrial heat recovery systems.

Investment & Funding Patterns: Over USD 10 billion invested globally in thermal system upgrades and energy-efficient infrastructure since 2023.

Innovation & Future Outlook: Integration of IoT-enabled monitoring and hybrid exchanger designs is shaping next-generation solutions.

The heat exchanger market is characterized by diversified sectoral demand, with the oil and gas industry contributing nearly 30% of total usage, followed by HVAC systems at approximately 25% and power generation at 20%. Technological advancements such as corrosion-resistant materials and compact modular designs are enhancing product lifespan and operational efficiency. Environmental regulations promoting waste heat recovery and reduced emissions are accelerating adoption across Europe and North America. Meanwhile, Asia-Pacific shows strong consumption growth due to rapid industrialization and infrastructure expansion. Emerging trends include digital twin technology for predictive maintenance and hybrid exchangers combining multiple heat transfer mechanisms, offering improved energy performance and reduced footprint for industrial applications.

The heat exchanger market holds strategic relevance as industries intensify efforts toward energy efficiency, operational cost optimization, and carbon emission reduction. Advanced thermal systems are becoming essential across sectors such as chemical processing, power generation, HVAC, and renewable energy integration. The adoption of microchannel heat exchanger technology delivers up to 25% higher heat transfer efficiency compared to conventional shell-and-tube systems, enabling compact design and reduced material usage. Asia-Pacific dominates in volume due to large-scale manufacturing and infrastructure expansion, while Europe leads in adoption with over 45% of enterprises integrating energy-efficient heat recovery systems aligned with regulatory mandates.

By 2028, AI-driven thermal optimization is expected to improve system performance by 18% through predictive analytics and real-time monitoring, significantly reducing energy losses. Firms are committing to sustainability targets, including up to 30% reduction in industrial emissions by 2030 through enhanced heat recovery and reuse technologies. In 2024, a German industrial plant achieved a 22% reduction in energy consumption by deploying AI-integrated heat exchanger networks, demonstrating measurable operational gains.

Strategically, companies are investing in modular and scalable heat exchanger systems to support flexible industrial operations and renewable energy applications such as hydrogen production and geothermal energy. The integration of IoT-enabled sensors is enabling predictive maintenance, reducing downtime by nearly 20%. As regulatory frameworks tighten and energy efficiency becomes a core operational priority, the Heat Exchanger Market is positioned as a critical pillar supporting industrial resilience, compliance, and long-term sustainable growth.

The growing need for industrial energy efficiency is a primary driver of the heat exchanger market. Industries account for nearly 40% of global energy consumption, with a significant portion lost as waste heat. Heat exchangers enable recovery of up to 60% of this wasted energy, directly reducing operational costs and emissions. In sectors such as chemical processing and refining, advanced heat exchanger systems can improve process efficiency by 20–30%. Government policies promoting energy conservation and carbon reduction are also accelerating adoption. For example, energy efficiency standards in manufacturing facilities require optimized thermal systems, leading to increased installation of high-performance exchangers. Additionally, the transition toward renewable energy systems, including solar thermal and geothermal applications, is expanding the role of heat exchangers in sustainable energy infrastructure.

Despite strong demand, high initial capital investment remains a key restraint for the heat exchanger market. Advanced systems, particularly those using corrosion-resistant alloys or compact designs, can cost 25–40% more than traditional alternatives. Installation complexity and customization requirements further increase project costs, especially in large-scale industrial applications. Maintenance challenges also impact adoption, as fouling and corrosion can reduce efficiency by up to 15% if not properly managed. Regular cleaning and component replacement add to operational expenses, particularly in industries with harsh operating environments such as oil refining and chemical processing. Small and medium enterprises often face budget constraints, limiting their ability to invest in high-efficiency systems, thereby slowing overall market penetration in cost-sensitive regions.

The integration of renewable energy systems presents significant growth opportunities for the heat exchanger market. Technologies such as solar thermal, geothermal, and hydrogen production rely heavily on efficient heat transfer mechanisms. Heat exchangers play a critical role in optimizing energy conversion processes, improving overall system efficiency by up to 25%. The global push toward decarbonization is driving investments in renewable infrastructure, creating demand for advanced thermal management solutions. Additionally, district heating systems in urban areas are expanding rapidly, with heat exchangers enabling efficient energy distribution across residential and commercial sectors. Innovations in compact and modular designs are further opening opportunities in decentralized energy systems, where space and efficiency are critical considerations.

Material limitations and stringent regulatory requirements pose significant challenges for the heat exchanger market. High-performance systems often require specialized materials such as titanium or nickel alloys to withstand extreme temperatures and corrosive environments, increasing production costs. Supply chain constraints for these materials can lead to delays and price volatility. Regulatory compliance adds another layer of complexity, as manufacturers must adhere to strict safety and environmental standards across different regions. Certification processes can extend project timelines and increase costs by up to 10–15%. Additionally, evolving environmental regulations require continuous product innovation to meet efficiency and emission standards, placing pressure on manufacturers to invest in research and development while maintaining competitive pricing.

• Digitalization and Smart Monitoring Adoption Increasing by 40%: Industrial operators are rapidly integrating IoT-enabled heat exchangers, with over 40% of newly installed systems featuring real-time monitoring capabilities. These smart systems improve predictive maintenance accuracy by nearly 25% and reduce unplanned downtime by up to 18%. Data-driven performance optimization is enabling industries to achieve 12–15% higher thermal efficiency compared to conventional systems. Adoption is particularly strong in North America and Europe, where over 60% of large-scale facilities have implemented digital thermal management solutions to enhance operational transparency and energy savings.

• Advanced Materials Enhancing Durability by 30%: The use of corrosion-resistant alloys such as titanium and stainless steel composites has increased by 35% in industrial heat exchanger production. These materials extend equipment lifespan by up to 30% while maintaining consistent performance under extreme conditions. Industries such as chemical processing and offshore oil platforms are reporting a 20% reduction in maintenance frequency due to improved material resilience. Additionally, coatings with enhanced thermal conductivity are boosting heat transfer efficiency by approximately 10–12%, making advanced material innovation a critical competitive differentiator.

• Rising Demand for Waste Heat Recovery Systems Surging by 45%: Waste heat recovery applications are expanding significantly, with adoption rates increasing by 45% across heavy industries. Heat exchangers are now capable of recovering up to 65% of industrial waste heat, contributing to a 20% reduction in overall energy consumption. Power generation and cement manufacturing sectors are leading this shift, with over 50% of facilities deploying recovery systems. Government regulations targeting emission reductions are further accelerating demand, as companies seek to meet sustainability targets through improved energy reuse and efficiency gains.

• Rise in Modular and Prefabricated Construction Driving 55% Cost Benefits: The adoption of modular construction is reshaping demand dynamics in the heat exchanger market. Around 55% of new industrial projects report cost benefits from prefabricated heat exchanger modules, which are manufactured off-site using automated systems. These solutions reduce installation time by nearly 30% and labor requirements by 25%, enabling faster project completion. Demand for high-precision, pre-engineered exchanger units is rising sharply in Europe and North America, where over 48% of infrastructure projects now incorporate modular thermal systems to improve efficiency and scalability.

The heat exchanger market is segmented based on type, application, and end-user industries, each reflecting distinct operational requirements and performance priorities. By type, shell and tube heat exchangers dominate due to their durability and suitability for high-pressure environments, while plate and frame exchangers are gaining traction for compact and energy-efficient applications. In terms of applications, HVAC systems represent a significant portion due to increasing urbanization and commercial infrastructure expansion, followed by strong demand in oil and gas and power generation sectors. From an end-user perspective, industrial manufacturing remains the primary contributor, accounting for a substantial share of installations, while emerging sectors such as renewable energy and district heating are expanding rapidly. This segmentation highlights a diversified demand structure driven by efficiency optimization, regulatory compliance, and technological advancements across global markets.

Shell and tube heat exchangers continue to lead the market, accounting for approximately 42% of total adoption due to their robust design and ability to operate under high pressure and temperature conditions. Plate and frame heat exchangers hold around 28% share, benefiting from compact design and up to 20% higher thermal efficiency in low-to-medium pressure applications. However, microchannel heat exchangers are the fastest-growing segment, expanding at an estimated CAGR of 8.5%, driven by their lightweight structure and 30% improved heat transfer performance compared to traditional designs. Air-cooled and regenerative heat exchangers collectively contribute nearly 30% of the market, serving niche applications such as power plants and heavy industrial processes where water conservation and thermal recycling are critical.

HVAC systems represent the leading application segment, accounting for nearly 35% of total heat exchanger usage, driven by rapid urbanization and increasing demand for energy-efficient building systems. Oil and gas applications follow with approximately 30% share, where heat exchangers are critical for refining, gas processing, and thermal management. Power generation accounts for around 20%, leveraging exchangers for steam condensation and heat recovery processes. However, renewable energy applications are the fastest-growing segment, expanding at an estimated CAGR of 9.2%, supported by increased investments in solar thermal and geothermal energy systems that rely heavily on efficient heat transfer technologies. Other applications, including food processing and chemical manufacturing, collectively contribute about 15% of the market, driven by process optimization and regulatory compliance requirements.

Industrial manufacturing remains the dominant end-user segment, accounting for approximately 40% of total market adoption, as heat exchangers are extensively used in chemical processing, metal production, and heavy machinery operations. The energy and power sector follows with around 30% share, driven by demand for efficient thermal management in power plants and renewable energy facilities. The HVAC and construction sector contributes nearly 20%, reflecting increased installation in commercial and residential infrastructure projects. Meanwhile, the renewable energy sector is the fastest-growing end-user, expanding at an estimated CAGR of 10.1%, fueled by global decarbonization efforts and investments in sustainable energy systems. Other end-users, including food and beverage and pharmaceuticals, collectively account for about 10%, emphasizing hygiene and process efficiency requirements.

Region Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

Asia-Pacific’s dominance is supported by strong industrial output, with China, India, and Japan collectively contributing over 60% of regional demand. North America holds approximately 24% of the global market, driven by advanced HVAC systems and retrofitting projects across more than 70% of commercial infrastructure. Europe accounts for nearly 22%, with over 65% of industrial facilities adopting energy-efficient heat recovery systems. South America contributes around 7%, primarily led by Brazil’s energy and refining sectors, while the Middle East & Africa region holds close to 6%, supported by oil and gas investments exceeding 30% of industrial expenditure. Across regions, more than 55% of installations are linked to industrial applications, while HVAC-related demand contributes approximately 30%, highlighting a diversified global adoption pattern with increasing emphasis on energy optimization and regulatory compliance.

How are industrial retrofits and energy efficiency mandates shaping advanced thermal system adoption?

North America accounts for approximately 24% of the global heat exchanger market, with strong demand from oil and gas, HVAC, and power generation sectors. Over 68% of commercial buildings in the region have implemented energy-efficient HVAC upgrades, driving significant demand for compact and high-performance heat exchangers. Regulatory frameworks promoting emission reduction and energy conservation, including federal efficiency standards, have led to a 20% increase in heat recovery system installations across industrial facilities. Digital transformation is also prominent, with nearly 55% of newly deployed heat exchangers incorporating IoT-enabled monitoring systems for predictive maintenance. A key regional player has focused on integrating smart heat exchangers into industrial plants, improving operational efficiency by up to 18%. Consumer behavior in this region shows higher enterprise adoption in sectors such as healthcare, data centers, and finance, where thermal management reliability and energy efficiency are critical performance parameters.

What role do sustainability regulations and green energy transitions play in driving innovation?

Europe holds nearly 22% of the global heat exchanger market, with Germany, the UK, and France leading in adoption. More than 65% of industrial facilities in these countries utilize energy-efficient heat exchangers to comply with stringent environmental regulations and carbon reduction targets. Regulatory bodies have enforced efficiency standards that have increased the adoption of waste heat recovery systems by over 30% in manufacturing sectors. Emerging technologies such as microchannel heat exchangers and advanced plate designs are gaining traction, improving thermal efficiency by 15–20%. A regional manufacturer has introduced eco-friendly exchanger systems using recyclable materials, reducing environmental impact by approximately 25%. Consumer behavior in Europe is heavily influenced by regulatory pressure, leading to increased demand for sustainable and energy-efficient heat exchanger solutions across industrial and commercial applications.

How is rapid industrial expansion accelerating demand for high-capacity thermal systems?

Asia-Pacific leads the global heat exchanger market in volume, contributing over 41% of total demand. China, India, and Japan are the top consuming countries, accounting for more than 60% of regional installations. Industrial manufacturing and infrastructure development projects have increased heat exchanger deployment by over 35% in the past five years. The region is witnessing strong growth in petrochemical and power generation sectors, where heat exchangers are used in over 70% of thermal processes. Technological innovation hubs in China and Japan are advancing compact and high-efficiency designs, improving performance by up to 20%. A major regional manufacturer has expanded production capacity by 25% to meet rising demand from industrial clients. Consumer behavior in Asia-Pacific is driven by large-scale industrialization and infrastructure expansion, with increasing adoption in sectors such as energy, construction, and heavy manufacturing.

How are energy sector investments and infrastructure modernization influencing adoption patterns?

South America represents approximately 7% of the global heat exchanger market, with Brazil and Argentina as key contributors. Brazil alone accounts for nearly 55% of regional demand, driven by investments in oil refining and power generation projects. Infrastructure modernization initiatives have increased the adoption of heat exchangers by over 18% in industrial facilities. Government incentives promoting energy efficiency and renewable energy integration are supporting market expansion, with nearly 25% of new projects incorporating advanced heat recovery systems. A regional player has focused on developing cost-effective heat exchanger solutions tailored for local industries, achieving a 15% increase in operational efficiency. Consumer behavior in this region is closely tied to energy sector developments, with demand influenced by industrial growth and localized infrastructure investments.

How are oil-driven economies and infrastructure expansion shaping thermal system demand?

The Middle East & Africa region accounts for around 6% of the global heat exchanger market, with strong demand from oil and gas, construction, and desalination sectors. Countries such as the UAE and South Africa are leading growth, with oil and gas projects contributing over 40% of regional demand. Technological modernization efforts have increased the adoption of advanced heat exchangers by nearly 22%, particularly in high-temperature and high-pressure applications. Trade partnerships and regulatory frameworks are supporting infrastructure development, with over 30% of industrial investments directed toward energy-efficient systems. A local manufacturer has introduced high-capacity exchangers designed for extreme environmental conditions, improving system durability by 20%. Consumer behavior in this region reflects a strong reliance on industrial and energy sector growth, with increasing demand for durable and high-performance thermal management solutions.

China – 35% Heat Exchanger Market share: High production capacity with over 12,000 manufacturers and strong demand from petrochemical and industrial sectors.

United States – 18% Heat Exchanger Market share: Advanced industrial infrastructure and widespread adoption of energy-efficient HVAC and heat recovery systems.

The heat exchanger market exhibits a moderately fragmented competitive landscape, with over 150 active global and regional manufacturers competing across various product segments. The top five companies collectively account for approximately 38% of the total market share, indicating a balanced mix of large multinational corporations and specialized regional players. Market leaders are focusing on product innovation, with over 45% of new product launches centered on high-efficiency and compact heat exchanger designs. Strategic partnerships and mergers have increased by nearly 20% between 2023 and 2025, enabling companies to expand their geographic presence and technological capabilities.

Innovation remains a key competitive factor, with more than 50% of leading firms investing in advanced materials and digital monitoring solutions to enhance product performance and lifecycle efficiency. Customization is also gaining importance, as nearly 35% of industrial clients require tailored heat exchanger solutions for specific operational needs. Additionally, companies are expanding their service offerings, including predictive maintenance and remote monitoring, to improve customer retention and operational efficiency. The competitive environment is further influenced by regulatory compliance requirements, pushing manufacturers to develop energy-efficient and environmentally sustainable products to maintain market relevance.

Alfa Laval

Kelvion Holding GmbH

Danfoss

SPX Technologies

Xylem Inc.

Hisaka Works Ltd.

API Heat Transfer

Chart Industries

Modine Manufacturing Company

SWEP International

Hamon Group

Thermax Limited

Technological advancements in the heat exchanger market are increasingly focused on improving thermal efficiency, reducing energy losses, and enabling real-time system optimization. Microchannel heat exchanger technology has gained significant traction, offering up to 30% higher heat transfer efficiency while reducing material usage by nearly 25% compared to conventional designs. These systems are particularly востребованы in HVAC and automotive applications due to their compact size and lightweight structure.

Additive manufacturing is emerging as a transformative technology, allowing the production of complex heat exchanger geometries that enhance surface area and improve heat transfer rates by 15–20%. This approach also reduces production waste by approximately 18%, making it a sustainable manufacturing solution. Additionally, advancements in nanocoatings and corrosion-resistant materials have extended equipment lifespan by up to 35%, especially in harsh industrial environments such as offshore oil and gas operations.

Digitalization is reshaping operational performance, with over 50% of new installations incorporating IoT-enabled sensors for predictive maintenance and performance monitoring. These systems can reduce unplanned downtime by up to 20% and improve operational efficiency by 12–15%. Artificial intelligence is further enhancing thermal management by optimizing heat flow and system performance in real time, delivering up to 18% efficiency improvements compared to traditional control systems.

Hybrid heat exchanger systems combining multiple heat transfer mechanisms are also gaining adoption, particularly in renewable energy applications where efficiency gains of 20–25% are critical. These technological innovations collectively position the market toward high-performance, energy-efficient, and digitally integrated thermal management solutions.

• In March 2025, Alfa Laval launched an upgraded range of gasketed plate heat exchangers featuring enhanced thermal efficiency and reduced fouling characteristics. The new design improves heat transfer performance by up to 18% and extends maintenance intervals, supporting industrial energy optimization initiatives. Source: www.alfalaval.com

• In September 2024, Danfoss introduced a next-generation microchannel heat exchanger platform designed for HVAC applications. The system reduces refrigerant usage by 30% and increases energy efficiency by 15%, aligning with global sustainability and emission reduction targets. Source: www.danfoss.com

• In January 2025, Kelvion Holding GmbH expanded its manufacturing facility in Europe to increase production capacity for industrial heat exchangers by 20%. The expansion supports growing demand from chemical processing and power generation industries across the region. Source: www.kelvion.com

• In July 2024, Modine Manufacturing Company announced the development of advanced heat exchanger systems for electric vehicle thermal management. These systems improve battery cooling efficiency by 22%, enhancing vehicle performance and supporting the transition toward sustainable mobility solutions. Source: www.modine.com

The Heat Exchanger Market Report provides a comprehensive evaluation of industry dynamics across multiple dimensions, including product types, applications, technologies, and geographic regions. The report covers key product segments such as shell and tube, plate and frame, air-cooled, and microchannel heat exchangers, which collectively account for over 90% of global installations. It also examines emerging product categories, including hybrid and additive-manufactured heat exchangers, which are gaining traction due to their efficiency and compact design advantages.

From an application perspective, the report analyzes major sectors including HVAC, oil and gas, power generation, chemical processing, and renewable energy, which together contribute more than 85% of total market demand. It further explores niche applications such as data center cooling and electric vehicle thermal management, where adoption is increasing by over 20% annually due to rising digitalization and electrification trends.

Geographically, the report provides insights into five key regions, with Asia-Pacific accounting for over 40% of global demand, followed by North America and Europe with a combined share exceeding 45%. It includes detailed country-level analysis for major markets such as China, the United States, Germany, and India, focusing on industrial output, infrastructure development, and regulatory frameworks.

The scope also encompasses technological advancements, including IoT-enabled monitoring systems, advanced materials, and energy-efficient designs, which are implemented in over 50% of new installations. Additionally, the report evaluates industry-specific adoption patterns, regulatory impacts, and innovation trends, offering decision-makers a holistic understanding of current market conditions and future growth opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Alfa Laval, Kelvion Holding GmbH, Danfoss, SPX Technologies, Xylem Inc., Hisaka Works Ltd., API Heat Transfer, Chart Industries, Modine Manufacturing Company, SWEP International, Hamon Group, Thermax Limited |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |