Reports

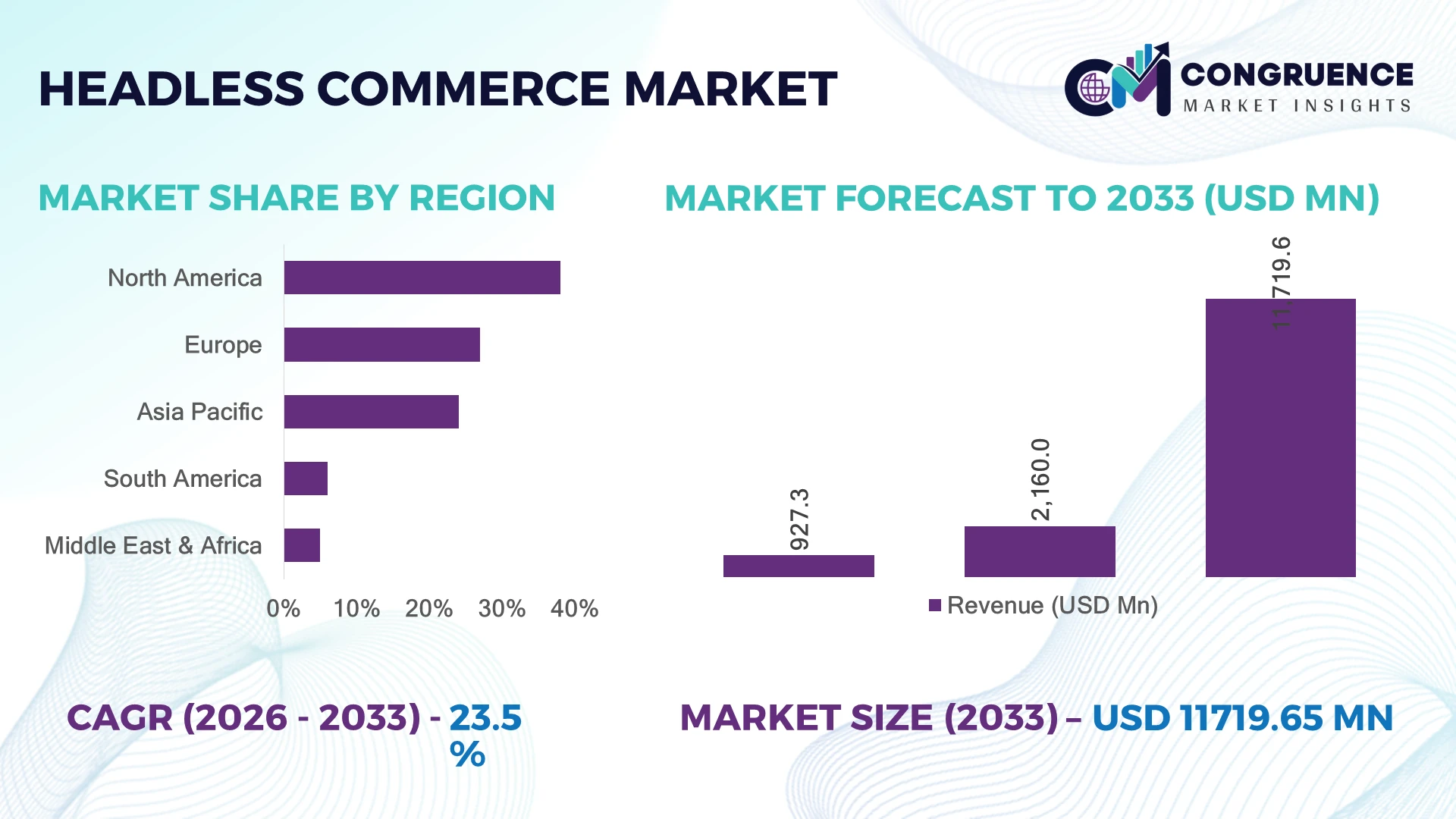

The Global Headless Commerce Market was valued at USD 2160 Million in 2025 and is anticipated to reach a value of USD 11719.64 Million by 2033 expanding at a CAGR of 23.54% between 2026 and 2033. Growth is accelerating through enterprise migration toward API-first digital commerce architectures, with omnichannel retailers reducing frontend deployment cycles by nearly 40% while improving mobile conversion performance across AI-enabled customer engagement platforms.

The United States leads the global headless commerce market with approximately 34% platform deployment share, supported by over USD 3.2 billion in enterprise digital transformation spending across retail, grocery, and B2B distribution networks in 2026. Adoption across Western Europe reached nearly 27% among large-scale online retailers following stricter digital compliance and localization requirements after regional data governance reforms. Compared with Germany’s 18% implementation penetration, India recorded over 31% annual growth in composable storefront integrations driven by rapid D2C expansion and cloud-native commerce investments.

Strategic expansion in scalable headless infrastructure now determines competitive advantage for retailers prioritizing faster localization, AI-driven merchandising, and cross-channel revenue optimization.

Market Size & Growth: USD 2160 Million in 2025 rising to USD 11719.64 Million by 2033, driven by API-first commerce modernization and 23.54% expansion momentum.

Top Growth Drivers: Mobile commerce adoption increased 38%, composable architecture deployment rose 41%, and AI-based personalization usage crossed 46% in enterprise retail.

Short-Term Forecast: By 2028, enterprises implementing headless storefronts will reduce checkout latency by 32% and improve deployment efficiency by 28%.

Emerging Technologies: AI recommendation engines, low-code integrations, and MACH architecture frameworks improved content delivery performance by nearly 35%.

Regional Leaders: North America exceeded USD 3.8 billion deployment value, Europe crossed USD 2.4 billion through omnichannel expansion, and Asia-Pacific advanced with 31% D2C integration growth.

Consumer/End-User Trends: Nearly 58% of digital-first retailers prioritize headless commerce to support mobile-first purchasing and unified customer experiences.

Pilot/Case Example: In 2026, a multinational fashion retailer reduced page load time by 47% after migrating from monolithic commerce infrastructure to composable storefront architecture.

Competitive Landscape: Enterprise leaders control approximately 44% market concentration, with dominant competition centered around cloud-native commerce providers and retail SaaS innovators.

Regulatory & ESG Impact: European data localization policies increased regional cloud commerce investments by 22%, accelerating compliant API orchestration deployment.

Investment & Funding: Global investments surpassed USD 5 billion in 2026, supported by retail-tech partnerships, cloud expansion, and AI commerce infrastructure funding.

Innovation & Future Outlook: Advanced edge commerce, real-time personalization, and AI-driven storefront orchestration are reshaping high-growth global commerce execution strategies.

The Headless Commerce Market is advancing rapidly across retail, consumer electronics, and B2B distribution environments where enterprises prioritize flexible digital storefront control and faster release cycles. AI-powered search optimization and composable checkout integrations improved customer retention rates by nearly 26% in 2026 enterprise deployments. Cross-border fulfillment restructuring and stricter regional data compliance standards are accelerating investment in cloud-native commerce orchestration, reinforcing the transition toward scalable omnichannel operating models and deeper strategic platform integration discussions.

Headless commerce is becoming strategically critical as enterprises restructure digital operations around composable infrastructure, faster omnichannel deployment, and AI-led customer engagement. Retailers and B2B distributors are replacing monolithic commerce environments to improve frontend agility and reduce infrastructure dependency during ongoing global supply-chain diversification and stricter regional data governance requirements. In 2026, nearly 52% of enterprise retailers prioritized API-based commerce modernization to support real-time inventory visibility, localized storefronts, and cross-border fulfillment scalability across mobile and marketplace channels.

Compared with legacy commerce systems, headless architecture reduces frontend deployment time by nearly 45% while lowering integration modification costs by approximately 28% through reusable API frameworks. The United States continues leading enterprise-scale deployments across grocery and consumer electronics sectors, while India is advancing through rapid D2C platform adoption and cloud-native retail expansion. Germany is emphasizing compliant commerce orchestration aligned with evolving digital infrastructure standards. Over the next 2–3 years, enterprise adoption of composable commerce platforms is expected to exceed 60% among large online retailers focused on personalization and operational responsiveness.

Global fashion and consumer goods companies are expanding partnerships with cloud infrastructure providers and payment orchestration specialists to accelerate storefront localization and improve conversion consistency across channels. Businesses investing early in scalable headless ecosystems are securing stronger competitive positioning through faster innovation cycles, lower operational friction, and superior omnichannel execution capacity.

Large retailers and B2B distributors are accelerating migration toward headless commerce frameworks to improve storefront flexibility, API interoperability, and omnichannel transaction consistency. In 2026, nearly 48% of enterprise retailers reduced frontend update cycles by over 35% after replacing monolithic systems with composable commerce architecture. The expansion of mobile-first purchasing and marketplace integration requirements in the United States and the United Kingdom further intensified demand for scalable digital commerce orchestration. Companies are responding through cloud partnerships, AI-based merchandising tools, and regional infrastructure expansion to support real-time personalization. A major operational shift is emerging around decentralized frontend management, enabling brands to localize promotions and customer experiences faster across multiple countries without disrupting backend systems, strengthening competitive execution efficiency.

Interoperability limitations between legacy ERP systems, payment gateways, and modern API-based commerce platforms remain a major structural restraint for enterprise deployment. Nearly 39% of mid-sized retailers reported delayed migration timelines due to fragmented backend architecture, while integration costs increased by approximately 24% in complex multi-vendor environments during 2026. Japan and Germany faced operational bottlenecks linked to strict enterprise data compliance and older retail infrastructure dependencies. These limitations directly affect deployment scalability, implementation speed, and operational profitability for companies transitioning toward composable commerce models. To reduce exposure, businesses are prioritizing modular integration frameworks, localized cloud hosting partnerships, and long-term middleware contracts. A notable strategic response involves phased migration deployment instead of full infrastructure replacement to preserve operational continuity and reduce integration disruption.

AI-enabled personalization engines and unified commerce orchestration platforms are creating high-value opportunities across digital retail ecosystems. In 2026, retailers implementing predictive recommendation systems improved customer retention rates by nearly 27%, while automated content delivery reduced campaign deployment time by over 30%. India and Southeast Asia are emerging as high-potential deployment markets due to expanding D2C infrastructure and rising mobile commerce penetration. A key technology trend involves integrating generative AI with headless storefront management to automate localized product recommendations and multilingual customer experiences. Companies are increasing investment in API marketplaces, edge computing partnerships, and cloud-native checkout optimization to capture untapped cross-border demand. One non-obvious opportunity is the reduction of regional operational redundancy through centralized backend governance combined with localized frontend commerce execution.

As headless commerce ecosystems expand, API security management and infrastructure governance are becoming major execution challenges. In 2026, API-related vulnerabilities accounted for nearly 31% of reported digital commerce security incidents, while enterprise retailers managing over 200 integrated services experienced operational latency increases of approximately 18%. The United States and Singapore are witnessing increased pressure around secure customer data orchestration and real-time transaction authentication standards. These complexities affect deployment consistency, customer trust, and long-term platform scalability. Companies must strengthen zero-trust architecture implementation, invest in API monitoring infrastructure, and expand cybersecurity partnerships to maintain stable omnichannel operations. A critical strategic challenge involves balancing rapid frontend innovation with secure backend interoperability across increasingly fragmented digital commerce ecosystems.

• AI-Led Storefront Optimization Enterprise retailers are integrating generative AI into headless storefront orchestration to automate search relevance, merchandising, and multilingual content deployment. In 2026, nearly 44% of digital commerce operators implemented AI-driven recommendation engines, while automated product tagging reduced catalog management time by 33%. United States retailers facing rising customer acquisition costs are restructuring digital workflows around predictive personalization layers. Companies are expanding partnerships with cloud AI providers to improve conversion consistency and reduce manual campaign dependency across mobile and web commerce channels.

• Composable Checkout Infrastructure Expansion Payment fragmentation and cross-border transaction pressure are accelerating adoption of composable checkout ecosystems. Nearly 39% of enterprise merchants migrated toward modular payment orchestration in 2026, reducing failed transaction rates by approximately 21%. Germany and Singapore intensified deployment following stricter digital authentication and transaction security standards. Companies are consolidating payment APIs, fraud detection modules, and fulfillment systems into unified headless environments to improve operational resilience and reduce regional deployment complexity during high-volume retail cycles.

• Edge Commerce Deployment Growth Retailers are increasingly shifting toward edge-based commerce delivery to improve storefront speed and regional responsiveness. API latency dropped by nearly 27% among enterprises deploying localized edge infrastructure, while mobile page rendering efficiency improved by over 30%. India’s rapidly expanding mobile commerce ecosystem accelerated demand for decentralized content delivery. Businesses are restructuring cloud infrastructure strategies through telecom partnerships and distributed hosting networks to support real-time pricing updates, localized promotions, and inventory synchronization.

• B2B Commerce Workflow Modernization Manufacturers and wholesale distributors are replacing legacy procurement portals with headless B2B commerce interfaces integrated with ERP and inventory systems. In 2026, nearly 36% of industrial distributors automated quotation and order management workflows through API-connected commerce environments. Labor shortages across warehouse operations and increasing procurement digitization in Japan are reshaping enterprise buying behavior. Companies are investing in self-service purchasing tools, account-based pricing engines, and automated replenishment systems to reduce operational friction and strengthen long-term buyer retention.

Cloud-Based platforms continue leading the headless commerce market due to faster scalability, lower infrastructure maintenance, and stronger omnichannel integration capabilities. In 2026, nearly 49% of enterprise deployments operated through cloud-native commerce environments, particularly across United States retail and consumer electronics sectors where businesses prioritized rapid storefront deployment and API orchestration flexibility. SaaS Platforms strengthened adoption among mid-sized retailers by reducing implementation timelines by approximately 32% compared with traditional infrastructure-heavy systems. Meanwhile, API-Driven Platforms emerged as the fastest-growing segment as enterprises increasingly focused on composable commerce ecosystems capable of integrating payment gateways, logistics tools, and AI personalization engines without frontend disruption.

On-Premises deployments retained relevance among financial services-linked retail networks and regulated enterprise environments in Germany and Japan where stricter data governance requirements continue influencing infrastructure decisions. Open-Source Platforms gained traction among digital-first brands seeking customization flexibility and reduced licensing dependency, particularly within India’s expanding D2C ecosystem. Companies are responding through modular platform innovation, cloud migration partnerships, and scalable integration frameworks designed to improve deployment agility while lowering long-term operational complexity across multi-channel commerce operations.

Omnichannel Commerce remains the leading application segment as enterprises increasingly prioritize synchronized customer engagement across web, mobile, marketplace, and in-store channels. In 2026, nearly 54% of enterprise retailers integrated headless commerce systems with omnichannel fulfillment and inventory orchestration tools to improve real-time order visibility and customer experience consistency. Online Retail maintained strong deployment concentration across fashion, grocery, and electronics sectors where businesses focused on improving conversion speed and frontend customization. Mobile Commerce emerged as the fastest-growing application due to rising smartphone purchasing activity and increasing demand for lightweight, API-driven storefront experiences across India and Southeast Asia.

B2B Commerce adoption accelerated among industrial suppliers and wholesale distributors implementing self-service procurement workflows and automated pricing engines. Digital Content Delivery expanded strategically within media and entertainment companies seeking faster streaming subscription management and personalized content merchandising. Businesses are scaling investments in unified customer data infrastructure, AI-powered recommendation systems, and low-latency mobile storefront optimization to strengthen operational responsiveness and retention metrics across digital commerce channels.

Retail Companies represent the dominant end-user segment due to large-scale omnichannel infrastructure requirements, continuous storefront optimization, and high transaction processing intensity. In 2026, nearly 57% of enterprise headless commerce deployments were concentrated within retail operations, particularly across grocery, fashion, and consumer electronics sectors in the United States and the United Kingdom. E-commerce Companies remained strong adopters as businesses accelerated deployment of AI-driven recommendation systems and composable checkout frameworks. Technology Companies emerged as the fastest-growing end-user group through expansion of API orchestration tools, cloud-native commerce ecosystems, and embedded digital experience platforms supporting enterprise-scale deployments.

Consumer Goods Companies increased adoption to strengthen direct-to-consumer sales execution and localized digital merchandising strategies, while Media and Entertainment Companies focused on personalized subscription and digital content delivery optimization. Healthcare Companies expanded selective deployment across online pharmacy and digital appointment ecosystems requiring secure commerce integration layers. Vendors are targeting these segments through industry-specific deployment models, usage-based pricing strategies, and strategic cloud partnerships designed to improve scalability, interoperability, and customer retention performance across complex digital commerce environments.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 26.11% between 2026 and 2033.

North America maintains leadership in the headless commerce market through advanced cloud infrastructure, large-scale enterprise retail digitization, and strong API ecosystem maturity. The region accounted for approximately 38% of global deployment concentration in 2025, supported by rapid modernization across grocery, fashion, and consumer electronics sectors. Nearly 57% of enterprise retailers in the United States implemented composable commerce frameworks to improve storefront agility and omnichannel synchronization. Large retailers accelerated partnerships with AI personalization providers and cloud-native payment orchestration firms to reduce deployment complexity and improve conversion consistency. Canada also strengthened enterprise adoption through increasing cross-border digital commerce activity and investment in scalable mobile commerce infrastructure supporting multilingual storefront deployment.

United States Market Outlook:

The United States remains the most strategically influential market due to high enterprise digital infrastructure maturity, extensive API integration ecosystems, and aggressive omnichannel commerce modernization. In 2026, nearly 61% of large retail enterprises expanded investment in headless storefront deployment to improve personalization efficiency and reduce frontend release timelines. Strong cloud infrastructure availability and growing adoption of AI-driven commerce analytics continue strengthening enterprise-scale deployment across retail, B2B distribution, and subscription commerce operations.

Europe is advancing through strong regulatory alignment, enterprise cloud modernization, and increasing demand for localized digital commerce orchestration. The region represented nearly 27% of global deployment activity in 2025, with Germany, the United Kingdom, and France leading implementation across retail and manufacturing-linked commerce operations. Data governance regulations and digital authentication standards accelerated migration toward API-driven commerce environments capable of supporting secure cross-border operations. Enterprises reduced backend operational duplication by approximately 24% after implementing composable commerce systems integrated with localized fulfillment networks. Retailers across Western Europe are prioritizing sustainable digital infrastructure and low-latency content delivery systems to strengthen operational resilience and customer experience continuity.

Germany Market Outlook:

Germany leads the European headless commerce market through advanced industrial digitization, strong enterprise software integration capabilities, and structured compliance-focused deployment models. In 2026, over 43% of large retailers in Germany accelerated modernization of legacy commerce infrastructure to support real-time inventory synchronization and omnichannel transaction management. Strong manufacturing-linked retail ecosystems and enterprise cybersecurity standards continue driving demand for secure API orchestration and localized cloud commerce infrastructure across industrial distribution and consumer retail networks.

Asia-Pacific is emerging as the fastest-growing headless commerce market due to expanding mobile commerce ecosystems, rapid D2C brand growth, and large-scale digital infrastructure investment. The region accounted for approximately 24% of global platform deployment activity in 2025, with India, China, and Southeast Asia driving enterprise adoption. Mobile-driven purchasing transactions increased by nearly 36% across major digital retail platforms in 2026, accelerating demand for lightweight API-based storefront architectures. Companies are restructuring commerce operations around cloud-native deployment and localized content delivery to improve customer responsiveness and regional scalability. Strong telecom infrastructure expansion and rising digital payment penetration continue supporting enterprise migration toward composable commerce frameworks.

India Market Outlook:

India is becoming a strategic growth center due to rapid D2C ecosystem expansion, increasing cloud-native startup activity, and high mobile commerce penetration. In 2026, nearly 48% of mid-sized digital retail brands adopted headless storefront infrastructure to improve mobile performance and multilingual customer engagement. Strong fintech integration capabilities, expanding logistics digitization, and aggressive enterprise investment in AI-powered commerce personalization continue strengthening the country’s role in scalable headless commerce deployment across retail and consumer goods sectors.

South America is experiencing increasing headless commerce adoption through retail digitization, mobile commerce expansion, and growing investment in cloud-based commerce infrastructure. The region accounted for nearly 6% of global deployment concentration in 2025, led by Brazil and Chile through expanding online retail ecosystems. Retail enterprises improved mobile storefront responsiveness by approximately 22% after implementing API-driven commerce frameworks integrated with regional payment gateways. However, inconsistent logistics infrastructure and fragmented enterprise IT environments continue affecting deployment scalability across certain markets. Companies are addressing these limitations through localized cloud partnerships, regional fulfillment integration, and modular commerce deployment strategies designed to reduce implementation complexity and improve operational continuity.

Brazil Market Outlook:

Brazil dominates the regional market due to strong digital retail penetration, expanding fintech ecosystems, and increasing enterprise investment in omnichannel commerce infrastructure. In 2026, nearly 41% of large Brazilian retailers accelerated migration toward cloud-native commerce systems to improve mobile transaction efficiency and cross-channel inventory visibility. Growth in digital payment adoption and localized logistics integration continues strengthening deployment opportunities across fashion, electronics, and grocery commerce operations.

Middle East & Africa is advancing through rapid digital infrastructure modernization, increasing enterprise cloud adoption, and government-backed retail digitization programs. The region represented approximately 5% of global deployment activity in 2025, with the United Arab Emirates and Saudi Arabia leading implementation across luxury retail, digital marketplaces, and consumer services. In 2026, enterprise cloud commerce deployment across Gulf countries increased by nearly 29% as retailers prioritized mobile-first purchasing experiences and localized digital engagement. Businesses are strengthening partnerships with cloud infrastructure providers and regional payment orchestration companies to improve operational scalability and multilingual storefront management. Expanding smart city initiatives and fintech modernization continue reinforcing demand for flexible API-based commerce ecosystems.

United Arab Emirates Market Outlook:

The United Arab Emirates remains the leading market due to advanced digital infrastructure, strong enterprise cloud adoption, and aggressive investment in omnichannel retail modernization. In 2026, more than 46% of enterprise retailers in the country expanded headless commerce integration to support multilingual customer engagement and AI-enabled merchandising strategies. Strong fintech connectivity, regional logistics hubs, and government-backed digital economy initiatives continue positioning the UAE as a strategic deployment center for scalable commerce infrastructure across the Middle East.

Global cloud-native commerce providers, enterprise SaaS vendors, and API-first platform developers are competing aggressively across scalability, deployment flexibility, and omnichannel orchestration efficiency. Shopify, commercetools, BigCommerce, Salesforce Commerce Cloud, and Adobe Commerce collectively control nearly 52% of enterprise-grade headless commerce deployments, while regional platform specialists compete through localized integration and pricing advantages. Competition is centered on deployment speed, AI-driven personalization, API interoperability, and checkout optimization, with leading vendors reducing frontend deployment cycles by over 35% and improving integration efficiency by approximately 28%. Companies are strengthening positions through cloud partnerships, composable architecture expansion, and embedded payment ecosystem integration. Technology-focused vendors are disrupting legacy commerce providers through low-code orchestration and edge-based storefront delivery. High integration complexity and enterprise migration costs remain major entry barriers for smaller providers. Winning in this market requires scalable API infrastructure, rapid deployment execution, ecosystem partnerships, and strong enterprise-level customization capability.

Shopify

commercetools

BigCommerce

Salesforce Commerce Cloud

Adobe Commerce

Elastic Path

VTEX

Spryker

Contentful

SAP Commerce Cloud

Oracle CX Commerce

Fabric

Bloomreach

ScandiPWA

API-first commerce architecture remains the core technology foundation shaping the headless commerce market in 2026, with nearly 58% of enterprise retailers deploying composable storefront frameworks integrated with cloud-native orchestration systems. Compared with legacy monolithic commerce environments, modern headless infrastructure improves frontend deployment efficiency by approximately 45% while reducing customization costs by nearly 28%. Retailers are increasingly integrating GraphQL APIs, edge computing, and microservices frameworks to accelerate storefront responsiveness and omnichannel synchronization. Businesses adopting modular commerce stacks are gaining operational advantages through faster release cycles, reduced infrastructure bottlenecks, and stronger cross-platform scalability across mobile and marketplace ecosystems.

AI-driven personalization and agentic commerce technologies are emerging as high-impact deployment priorities between 2026 and 2028. Nearly 47% of enterprise commerce operators implemented AI-powered recommendation engines and automated merchandising workflows in 2026 to improve conversion consistency and customer retention. Companies are integrating generative AI with product discovery, multilingual content delivery, and predictive search orchestration. AI-enabled commerce agents reduced manual catalog management workloads by approximately 32%, creating measurable operational savings while improving dynamic pricing execution and localized shopping experiences.

Disruptive innovation is shifting toward edge-based commerce delivery, low-code orchestration, and autonomous checkout ecosystems. Enterprises deploying edge infrastructure improved mobile page rendering performance by over 30% compared with centralized hosting systems. Technology leaders benefit through faster experimentation, scalable API governance, and stronger integration ecosystems. Companies delaying modernization face increasing operational friction as AI-native commerce infrastructure becomes central to enterprise competitiveness and digital expansion strategy.

May 2025 – commercetools launched Commerce MCP and AI Hub to enable AI-agent integration across composable commerce environments, reducing custom connector dependency and accelerating AI-native deployment workflows. The platform improved enterprise integration efficiency by nearly 30%, strengthening real-time personalization and scalable omnichannel commerce orchestration. Source: commercetools.com

September 2025 – commercetools partnered with Stripe and OpenAI to support the Agentic Commerce Protocol, enabling AI agents to securely transact across enterprise commerce systems. The collaboration accelerated automated commerce execution and strengthened interoperability for large-scale digital retailers adopting AI-led purchasing workflows and composable checkout infrastructure.

January 2026 – Shopify and Google introduced the Universal Commerce Protocol at NRF 2026 to streamline AI-agent transactions across digital storefronts and payment environments. Shopify reported a 15-fold increase in AI-generated commerce orders since early 2025, significantly improving automated product discovery and checkout conversion scalability. Source: investors.com

May 2026 – Shopify expanded AI-driven merchant tools and enterprise commerce infrastructure following more than USD 100 billion in quarterly gross merchandise volume processed through its platform. The company strengthened enterprise onboarding and AI-assisted commerce operations, improving merchant automation capabilities and accelerating large-scale omnichannel storefront deployment efficiency. Source: shopify.com shopify.com

The Headless Commerce Market Report delivers detailed analysis across platform types, deployment models, enterprise applications, end-user industries, and regional adoption trends shaping digital commerce transformation between 2026 and 2033. The study covers Cloud-Based, API-Driven, SaaS, Open-Source, and On-Premises platforms alongside key applications including Online Retail, Mobile Commerce, Omnichannel Commerce, Digital Content Delivery, and B2B Commerce. More than 55% of enterprise deployments analyzed within the report are concentrated in omnichannel retail and mobile-first commerce environments, reflecting increasing demand for composable storefront infrastructure and AI-enabled customer engagement systems.

The report evaluates operational deployment patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting enterprise modernization priorities, cloud infrastructure expansion, and API integration strategies. It further examines technology adoption trends including AI personalization, edge commerce, microservices architecture, and agentic commerce frameworks. Strategic insights support investment planning, platform selection, competitive benchmarking, ecosystem partnerships, and enterprise-scale digital commerce expansion initiatives across high-growth retail and B2B environments.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2160 Million |

|

Market Revenue in 2033 |

USD 11719.64 Million |

|

CAGR (2026 - 2033) |

23.54% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Shopify, commercetools, BigCommerce, Salesforce Commerce Cloud, Adobe Commerce, Elastic Path, VTEX, Spryker, Contentful, SAP Commerce Cloud, Oracle CX Commerce, Fabric, Bloomreach, ScandiPWA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |