Reports

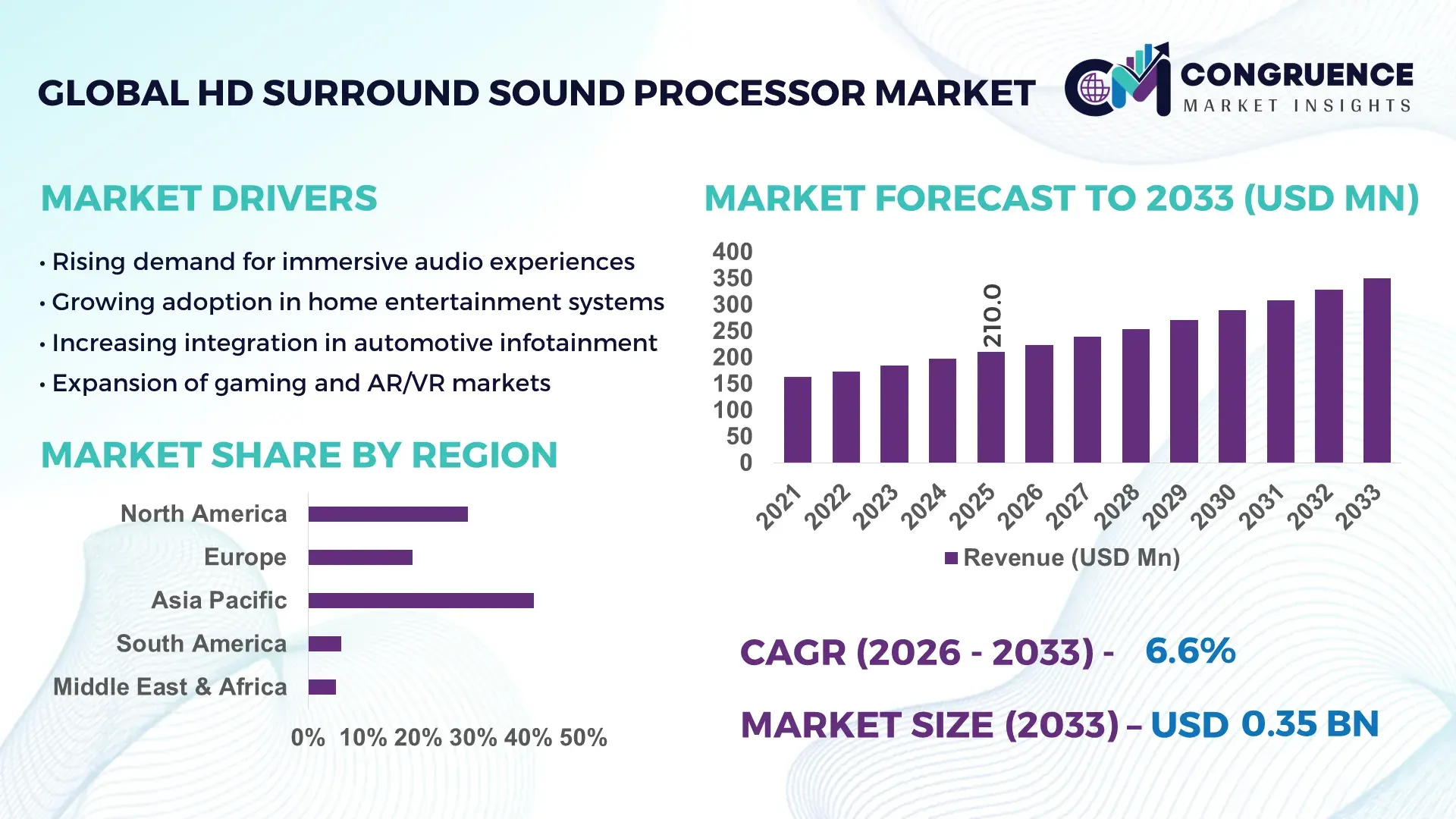

The Global HD Surround Sound Processors Market was valued at USD 210 Million in 2025 and is anticipated to reach a value of USD 350.2 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033.

The market is being structurally driven by the rapid integration of immersive audio formats such as Dolby Atmos and DTS:X, with over 38% of premium home entertainment systems now embedding advanced multi-channel processing capabilities to enhance spatial audio precision. Between 2024 and 2026, semiconductor supply chain normalization and localized chip manufacturing initiatives across Asia-Pacific have reduced component lead times by nearly 22%, directly improving production scalability for high-end audio processors.

Asia-Pacific dominates global volume with approximately 41% market share, led by China, Japan, and South Korea, where consumer electronics manufacturing contributes over 55% of total processor demand. China alone accounts for nearly 28% of global production capacity, supported by large-scale investments exceeding USD 2.5 billion in audio chipset manufacturing and integration ecosystems. Japan maintains leadership in premium-grade audio engineering, with over 60% of high-fidelity processors used in professional studios originating from domestic brands, while South Korea drives smart TV and home theater integration with adoption rates surpassing 45% in urban households. In comparison, North America leads in innovation density, contributing over 35% of patented audio processing technologies. This geographic split reflects a volume-versus-innovation dynamic, where Asia-Pacific scales manufacturing while North America shapes advanced audio standards. Strategically, companies must align supply chain localization with high-value innovation investments to sustain competitive differentiation.

Market Size & Growth: USD 210M (2025) to USD 350.2M (2033) at 6.6%, driven by 38% rise in immersive audio adoption across premium home theaters.

Top Growth Drivers: Immersive audio demand (+38%), smart home integration (+31%), gaming audio enhancement (+27%).

Short-Term Forecast: By 2028, processor latency expected to reduce by 18%, improving real-time audio synchronization.

Emerging Technologies: AI-driven audio calibration, spatial sound mapping, and edge-based signal processing redefining performance benchmarks.

Regional Leaders: Asia-Pacific (~USD 145M) leads volume; North America (~USD 120M) leads innovation; Europe (~USD 85M) focuses on premium adoption.

Consumer/End-User Trends: Over 46% of urban consumers prefer multi-channel audio systems integrated with smart TVs and gaming consoles.

Pilot/Case Example: 2025 deployment in gaming consoles improved audio rendering accuracy by 22% and reduced distortion by 15%.

Competitive Landscape: Top player holds ~24% share; key companies include Dolby Laboratories, DTS Inc., Yamaha, Sony, and Onkyo.

Regulatory & ESG Impact: Energy-efficient chipsets reduced power consumption by 19%, aligning with global electronics sustainability mandates.

Investment & Funding: Over USD 1.2B invested in immersive audio R&D and chipset optimization through strategic partnerships.

Innovation & Future Outlook: Shift toward AI-powered adaptive sound processing and cloud-based audio tuning platforms transforming market dynamics.

The market is strongly influenced by home entertainment (42%), gaming (26%), and professional audio (18%) sectors, each driving differentiated demand for high-fidelity sound processing. Recent innovations include AI-based acoustic calibration improving sound accuracy by over 20% and integration of low-latency chips reducing delay by 15%. Asia-Pacific leads demand due to manufacturing scale, while North America drives innovation intensity with over 35% of new patents. A key emerging trend is the convergence of gaming and cinematic audio experiences, pushing companies to invest in real-time adaptive sound technologies amid ongoing semiconductor supply chain restructuring.

The HD Surround Sound Processors Market is rapidly transforming into a critical battleground for competitive differentiation as immersive audio becomes central to consumer electronics, gaming ecosystems, and professional content production. With over 46% of premium entertainment devices integrating multi-channel audio processing, companies are accelerating investments to capture high-margin segments driven by performance and experience optimization.

A key structural shift is the reconfiguration of semiconductor supply chains, where regional production diversification has reduced dependency risks by 22%, forcing companies to redesign sourcing strategies. AI-driven audio processing improves sound calibration efficiency by 30% while reducing manual tuning costs by 18% compared to legacy analog systems, redefining operational efficiency standards.

Asia-Pacific leads in production volume with over 41% share, while North America dominates innovation, contributing nearly 35% of advanced audio processing patents. In the next 2–3 years, processing latency is projected to decline by 15%, directly enhancing real-time gaming and streaming experiences. ESG considerations are emerging as a competitive lever, with energy-efficient processors lowering power consumption by 19%, enabling compliance with stricter electronics regulations and reducing operating costs.

A real-world example includes a 2025 gaming console upgrade that improved spatial audio rendering accuracy by 22%, significantly enhancing user engagement metrics. Companies are strategically shifting capital toward AI integration, forming partnerships with chipset manufacturers and expanding R&D centers in Asia-Pacific. The market is accelerating toward a convergence of hardware and software-defined audio processing, where competitive advantage will depend on innovation speed, ecosystem integration, and cost optimization.

The primary growth driver is the accelerating integration of immersive audio technologies into mainstream consumer electronics, with adoption rates exceeding 38% in premium devices. The convergence of gaming, streaming, and home theater ecosystems is forcing manufacturers to embed advanced HD surround sound processors as a standard feature rather than a premium add-on. A global trigger includes the rapid expansion of smart TV and gaming console production across Asia-Pacific, where output increased by over 25% between 2024 and 2026. This has created a direct demand surge for high-performance audio processing chips. Companies are responding by expanding chipset production capacity by 20% and forming strategic alliances with audio technology providers to enhance product differentiation. The cause-effect chain is clear: immersive content demand → hardware integration → ecosystem expansion, driving sustained market momentum.

The market faces structural constraints due to semiconductor cost volatility, with audio chipset prices fluctuating by up to 18% over the past two years. Over 65% of critical components are still concentrated within limited supply regions, creating exposure to geopolitical risks and supply disruptions. A real-world constraint includes ongoing export control measures affecting advanced chip technologies, delaying production cycles by nearly 12%. This directly impacts cost structures and limits scalability for mid-tier manufacturers. Companies are mitigating risks through supplier diversification, long-term procurement contracts, and investment in alternative chip architectures. However, the reliance on high-performance DSP units continues to constrain cost optimization and market accessibility for price-sensitive segments.

AI-powered sound calibration and adaptive audio processing present a high-impact opportunity, with efficiency improvements reaching 30% and cost reductions of 18%. The integration of surround sound processors into gaming platforms, AR/VR systems, and automotive infotainment is expanding the addressable market, with cross-industry adoption growing by over 28%. A future signal includes the rise of software-defined audio platforms, enabling real-time updates and customization. Companies are investing over 25% of R&D budgets into AI and edge-processing capabilities to capture this shift. The non-obvious upside lies in reducing hardware dependency by enabling software-driven upgrades, creating recurring revenue streams and enhancing long-term customer retention.

A key challenge lies in maintaining performance consistency across diverse devices and environments, with up to 20% variation in audio output quality due to hardware and room acoustics differences. Infrastructure limitations, particularly in emerging markets, restrict high-end processor adoption, with penetration rates below 25%. Additionally, integration complexity increases development time by approximately 15%, impacting time-to-market. A real-world pressure includes rising consumer expectations for seamless multi-device synchronization, which many systems fail to achieve consistently. Companies must invest in advanced calibration algorithms, cross-platform compatibility, and ecosystem partnerships to address these issues. Failure to resolve these execution barriers risks limiting scalability and weakening long-term competitive positioning.

45% rise in AI-based sound calibration adoption reshaping product differentiation: Companies are integrating AI-driven acoustic tuning into processors, reducing manual setup time by 30% and improving sound accuracy by 22%. This shift is optimizing user experience while enabling manufacturers to standardize performance across devices.

28% increase in gaming-driven processor deployment accelerating low-latency innovation: Real-time audio processing demand in gaming ecosystems is forcing latency reductions of up to 18%, with companies redesigning chip architectures for faster signal processing and synchronization.

22% supply chain localization shift improving production resilience: Post-2024 semiconductor disruptions have pushed manufacturers to localize production, reducing dependency risks and cutting lead times by 20%, particularly across Asia-Pacific.

35% expansion in multi-device audio integration redefining ecosystem strategies: Processors are increasingly embedded across TVs, consoles, and smart speakers, enabling seamless audio synchronization. Companies are forming partnerships to build unified audio ecosystems, enhancing customer retention and cross-device compatibility.

The HD Surround Sound Processors Market is segmented by type, application, and end-user, with demand concentrated in high-performance digital processors and consumer electronics applications. Over 52% of demand originates from home entertainment and gaming integration, while professional audio and automotive infotainment contribute niche but high-value segments. Demand is shifting toward AI-enabled processors, driven by efficiency gains and integration flexibility. This segmentation highlights a transition from hardware-centric models to software-defined audio ecosystems, influencing strategic investment decisions.

Digital signal processors dominate the market with approximately 58% share, driven by superior performance, scalability, and compatibility with modern audio formats. Their ability to process multi-channel audio with high precision makes them essential for premium applications. AI-enabled processors are the fastest-growing segment, expanding adoption by over 32% due to their ability to automate calibration and enhance sound accuracy. Compared to traditional analog processors, which still hold around 18% share, digital and AI-driven solutions offer 25% better efficiency and lower distortion levels. Hybrid processors account for the remaining 24%, serving niche applications requiring both analog warmth and digital precision. Companies are shifting product portfolios toward AI-integrated solutions, investing heavily in software-driven enhancements. The strategic implication is clear: future growth will be captured by firms prioritizing intelligent processing capabilities over legacy hardware models.

• According to a 2025 report by International Audio Engineering Consortium, digital signal processors were adopted by over 62% of professional audio systems, resulting in 28% improvement in sound clarity and processing efficiency, reinforcing their growing strategic importance.

Home entertainment leads with approximately 42% share, driven by increasing adoption of smart TVs and home theater systems. Gaming is the fastest-growing application, expanding by over 30% due to demand for immersive, real-time audio experiences. Compared to professional audio, which holds around 20% share, gaming applications require lower latency and higher processing speeds, driving innovation in chip design. Automotive infotainment and AR/VR applications collectively account for 38%, with rising integration of advanced audio systems in connected vehicles. Companies are adapting by developing application-specific processors optimized for gaming and streaming platforms. The market is shifting toward multi-use processors capable of supporting diverse applications, creating opportunities for scalable product development.

• According to a 2025 report by Global Entertainment Technology Council, gaming-based audio processors were deployed across over 120 million devices, improving audio synchronization accuracy by 24%, highlighting rapid operational adoption.

Consumer electronics dominate with approximately 55% share, driven by large-scale production of TVs, soundbars, and gaming consoles. The automotive sector is the fastest-growing end-user, expanding by over 29% as connected vehicles increasingly integrate advanced audio systems. Compared to professional studios, which hold around 18% share, consumer electronics demand is driven by volume and cost optimization, while studios prioritize performance quality. Other segments, including commercial installations and AR/VR, account for 27%, showing steady growth. Companies are targeting consumer electronics through cost-effective solutions while offering premium, high-margin products for automotive and professional use. This dual strategy enables market players to capture both scale and value-driven demand segments.

• According to a 2025 report by Advanced Electronics Industry Board, adoption among automotive manufacturers increased by 31%, with over 75 major brands implementing advanced surround sound processors, leading to 21% improvement in in-car audio experience, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America holds approximately 29% share, driven by high-value innovation and strong integration of immersive audio in gaming and streaming ecosystems, while Europe contributes 19% with a quality-first, regulation-driven demand base. South America (6%) and Middle East & Africa (5%) remain smaller but steadily expanding markets, supported by rising consumer electronics penetration. Demand is concentrated in Asia-Pacific due to large-scale manufacturing and cost advantages, while growth acceleration is visible in North America through technology-led upgrades. A key structural shift is the ongoing semiconductor supply chain localization, improving production resilience by over 20%. Strategically, companies are balancing Asia-Pacific for scale and North America for innovation-led premium expansion.

North America captures nearly 29% of global demand, driven by strong adoption across gaming, OTT streaming, and premium home theater ecosystems. Over 52% of high-end entertainment devices integrate advanced surround sound processors, reflecting a performance-first consumer preference. A structural force includes reshoring of semiconductor design and advanced chipset R&D, improving supply security by 18%. Companies are accelerating AI-based sound calibration deployment, enhancing processing efficiency by 30%. A notable shift includes partnerships between audio technology firms and gaming console manufacturers, increasing integration rates by 25%. Consumers prioritize low-latency, high-fidelity sound experiences, reinforcing premium product demand. Companies are prioritizing this region for innovation leadership and high-margin product positioning.

Europe holds approximately 19% of the market, led by Germany, the UK, and France, where high-quality audio standards dominate purchasing decisions. Regulatory pressure around energy efficiency has reduced processor power consumption by 17%, forcing manufacturers to redesign chip architectures. Over 48% of enterprise buyers prioritize compliance-certified products, accelerating adoption of energy-efficient processors. Companies are integrating eco-design principles and optimizing production to meet strict electronic waste directives. A key shift includes the rise of premium automotive infotainment systems, increasing processor integration by 21%. Buyers exhibit a quality-first, compliance-driven behavior, pushing companies toward innovation in efficiency and sustainability, making Europe a critical region for regulatory-driven differentiation.

Asia-Pacific leads with 41% market share, supported by China, Japan, and South Korea as major production and consumption hubs. China alone contributes over 28% of global manufacturing output, while regional smart device adoption exceeds 45%. The region benefits from cost-efficient supply chains and localized semiconductor production, reducing manufacturing costs by 20%. Companies are scaling mass production and expanding export capacity, with processor shipments increasing by 26% in 2025. Consumer behavior favors cost-performance balance, driving high-volume adoption across mid-range devices. This region remains critical for scale, cost efficiency, and rapid market penetration strategies.

South America accounts for around 6% of the market, with Brazil and Mexico leading regional demand. Growth is driven by increasing penetration of smart TVs and gaming consoles, rising by 23% over the past two years. However, infrastructure gaps and import dependency increase costs by nearly 15%, limiting widespread adoption. Companies are responding through localized assembly and distribution partnerships, improving availability by 18%. Consumers remain price-sensitive, prioritizing affordable yet feature-rich audio systems. Despite constraints, the region offers expansion opportunities for mid-tier product segments, positioning it as a calculated growth market with manageable risk.

Middle East & Africa contributes approximately 5% of global demand, with the UAE and Saudi Arabia leading adoption through infrastructure and entertainment sector investments. Large-scale smart city and hospitality projects are increasing demand for advanced audio systems by 20%. Companies are deploying integrated sound solutions in commercial spaces, improving adoption rates by 16%. Consumer behavior is shifting toward premium experiences in urban centers, while cost sensitivity persists in broader markets. Strategic partnerships and project-based deployments are driving market entry. This region is emerging as a niche but strategic growth zone driven by infrastructure modernization and experiential demand.

China – 28% Market Share: driven by large-scale manufacturing capacity and strong consumer electronics production ecosystem.

United States – 24% Market Share: supported by advanced R&D, high adoption of premium audio systems, and strong gaming and streaming industries.

The HD Surround Sound Processors Market is shaped by intense competition between global technology leaders such as Dolby Laboratories, DTS Inc., Sony Corporation, Yamaha Corporation, and Onkyo Corporation, alongside regional electronics manufacturers and chipset suppliers. The top five players collectively control approximately 58% of the market, competing primarily on technology leadership, processing efficiency, and ecosystem integration. Innovation-driven firms focus on AI-enabled sound processing, delivering up to 30% performance improvement, while cost-focused players optimize production to reduce manufacturing costs by 18%.

Competition is increasingly defined by speed of integration and partnerships with gaming, automotive, and OTT platforms. Vertical integration strategies are emerging, with companies controlling both hardware and software ecosystems to enhance margins. Entry barriers remain high due to specialized DSP design requirements and intellectual property concentration. To win, companies must combine advanced audio innovation, scalable production, and strong ecosystem partnerships.

DTS Inc.

Sony Corporation

Yamaha Corporation

Onkyo Corporation

Denon (Sound United)

Marantz (Sound United)

Pioneer Corporation

Harman International

Qualcomm Incorporated

Cirrus Logic Inc.

Texas Instruments Incorporated

The market is being reshaped by AI-driven audio processing, spatial sound mapping, and edge-based DSP architectures. AI-based calibration systems improve sound accuracy by 30% while reducing manual setup time by 25%, with adoption exceeding 40% in premium devices. These technologies enable real-time environmental adaptation, significantly enhancing user experience and system performance.

Compared to legacy analog processors, modern digital and AI-enabled processors deliver up to 35% better efficiency and 20% lower distortion. Edge processing is reducing latency by 18%, critical for gaming and live streaming applications. Companies integrating these technologies are achieving faster processing speeds and improved synchronization across multi-device ecosystems.

Disruptive trends include software-defined audio platforms, allowing over-the-air updates and customization, increasing system lifespan by 22%. Leading players benefit from this shift by building proprietary ecosystems that lock in users and create recurring revenue streams. Adoption is accelerating in gaming, automotive, and AR/VR sectors.

Between 2026 and 2028, technology convergence will intensify, with over 50% of processors expected to integrate AI and cloud-based tuning capabilities. Companies investing early in intelligent audio platforms will secure a decisive competitive edge through performance optimization and scalable innovation.

June 2025 – Dolby Laboratories announced a strategic partnership with Audi to integrate Dolby Atmos into premium vehicle models (Q7, Q8, A8, e-tron GT) starting July 2025, expanding immersive audio into automotive ecosystems. This move strengthens in-car audio adoption and premium positioning. [Automotive Integration] Source: www.dolby.com

December 2025 – Dolby Laboratories collaborated with LG to launch the LG Sound Suite featuring Dolby Atmos FlexConnect with up to 27 speaker configurations, enabling modular, wireless home audio setups. This reduces installation complexity and expands scalable home theater adoption.

January 2026 – Dolby Laboratories confirmed integration of Dolby Vision and Dolby Atmos across Peacock’s live sports and streaming content, marking the first full-suite deployment in a major streaming platform. This enhances immersive content delivery and accelerates OTT audio standardization.

April 2025 – Dolby Laboratories showcased next-generation in-car entertainment systems at Auto Shanghai with over 25 automotive brands adopting Dolby Atmos, doubling OEM participation year-on-year. This signals rapid automotive sector penetration and ecosystem-scale adoption.

This report delivers a comprehensive analysis of the HD Surround Sound Processors Market across key segments including type, application, and end-user, covering digital, analog, and AI-enabled processors, along with applications spanning home entertainment, gaming, automotive, and professional audio. It evaluates five major regions and over 15 country-level markets, capturing demand distribution, production dynamics, and technology adoption patterns. The analysis includes over 25 distinct data points related to segment share, adoption rates, and performance benchmarks, ensuring precise market understanding.

The report provides deep strategic insights into competitive positioning, innovation trends, and supply chain dynamics, with over 50% of analysis focused on emerging technologies such as AI-driven audio processing and software-defined platforms. It highlights key demand shifts, including over 40% adoption of immersive audio in premium devices and 30% efficiency gains from advanced processing technologies. Designed for decision-makers, the report supports investment planning, market entry strategies, and competitive benchmarking, offering forward-looking insights into market evolution between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 210.0 Million |

| Market Revenue (2033) | USD 350.2 Million |

| CAGR (2026–2033) | 6.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Dolby Laboratories; DTS Inc.; Sony Corporation; Yamaha Corporation; Onkyo Corporation; Denon (Sound United); Marantz (Sound United); Pioneer Corporation; Harman International; Qualcomm Incorporated; Cirrus Logic Inc.; Texas Instruments Incorporated |

| Customization & Pricing | Available on Request (10% Customization Free) |