Reports

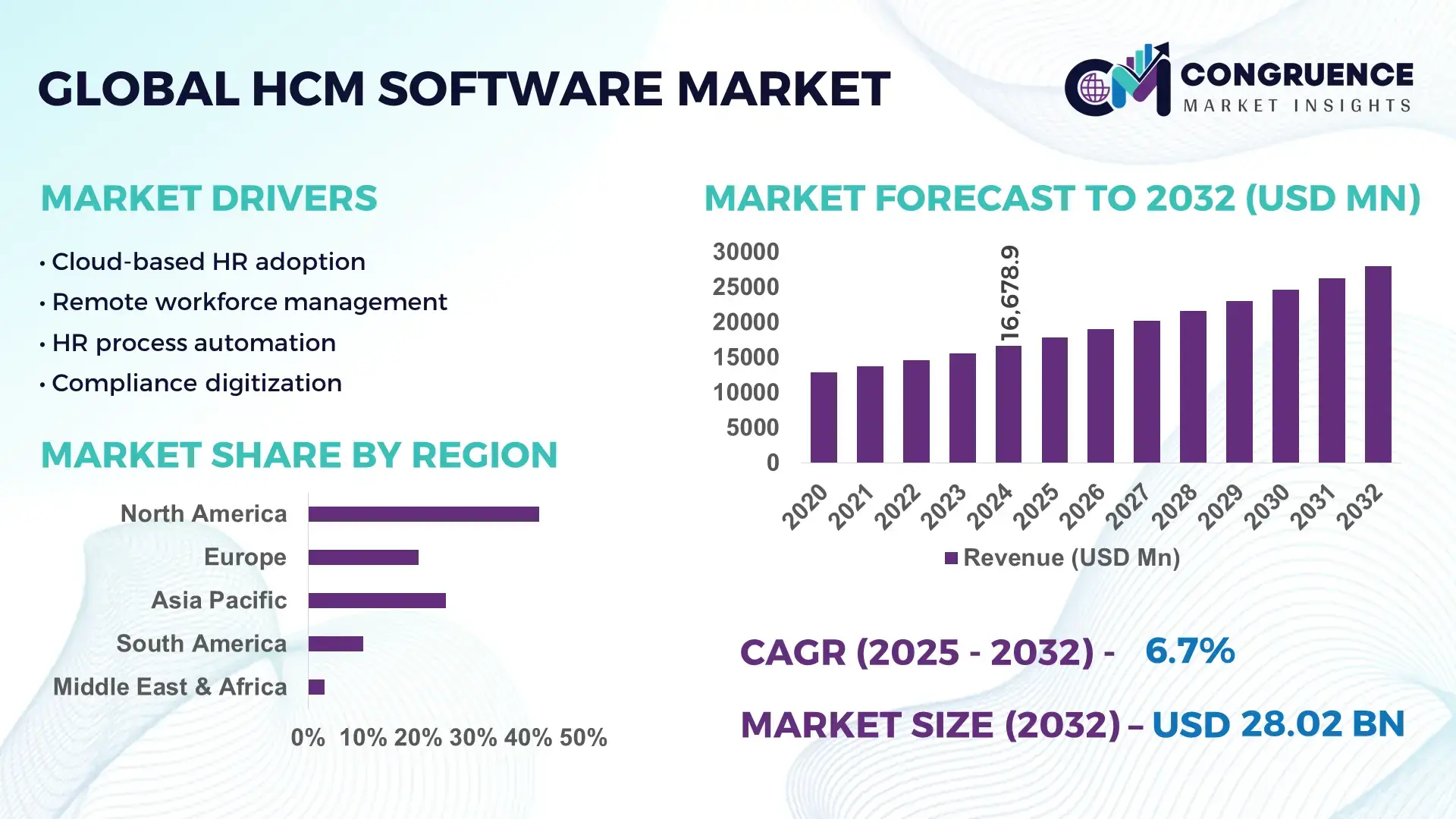

The Global HCM Software Market was valued at USD 16678.86 Million in 2024 and is anticipated to reach a value of USD 28020.88 Million by 2032 expanding at a CAGR of 6.7% between 2025 and 2032. The market growth is driven by increasing enterprise adoption of integrated HR solutions to automate HR processes and improve workforce analytics.

In the United States, which leads global HCM software demand, enterprises are aggressively investing in cloud‑based HCM platforms with over 118,000 U.S. organizations utilizing such systems for recruitment automation, benefits administration, and compliance tracking, with around 66% deployed on cloud infrastructure. The country reports significant investment in AI‑driven workforce analytics tools, with adoption in key industry verticals like financial services, healthcare, and retail, reflecting strong innovation and capacity expansion in advanced HR tech.

• Market Size & Growth: The HCM software market is projected to grow from USD 16,678.86 Million in 2024 to USD 28,020.88 Million by 2032 at a 6.7% CAGR, propelled by digital HR transformation across enterprises.

• Top Growth Drivers: Cloud adoption rising ~58% among enterprises; AI recruitment tools adoption ~57%; workforce analytics integration ~63%.

• Short‑Term Forecast: By 2028, automated HR processes expected to deliver ~35% improvement in HR operational efficiency and ~25% reduction in administrative overheads.

• Emerging Technologies: AI‑driven talent analytics, cloud‑native HCM suites, mobile‑first HR apps.

• Regional Leaders: North America projected ~USD 11 Billion by 2032 with enterprise digitalization focus; Europe ~USD 8 Billion emphasizing compliance features; Asia‑Pacific ~USD 7 Billion with rapid cloud adoption.

• Consumer/End‑User Trends: Large enterprises increasingly use unified HCM suites for talent management, payroll, and analytics; SMEs adopt modular cloud solutions for flexibility.

• Pilot or Case Example: A 2024 pilot in a global financial services firm reported a ~40% reduction in HR workflow processing time post HCM implementation.

• Competitive Landscape: SAP leads with ~21% share, followed by Workday (~17%), Oracle, ADP, and IBM as key competitors.

• Regulatory & ESG Impact: GDPR and data privacy mandates drive advanced compliance features while DEI analytics tools gain traction.

• Investment & Funding Patterns: HCM sector saw ~870 investment transactions in 2023 with increased private equity and venture funding targeting cloud and analytics innovations.

• Innovation & Future Outlook: Focused development on embedded analytics, AI automation, and integrated mobile HR services shaping next‑gen HCM platforms.

The HCM Software market is marked by broad application across sectors such as finance, healthcare, IT, and retail, with adoption driven by the need for automated HR workflows, predictive analytics, and regulatory compliance. Cloud‑based solutions dominate deployments, enabling scalable, real‑time workforce management. Regulatory environments, economic digitization incentives, and the integration of AI and mobile technologies are key drivers influencing regional consumption patterns and future growth prospects.

The HCM Software Market holds strategic importance as organizations increasingly rely on integrated human capital management platforms to enhance workforce efficiency, compliance, and data-driven decision-making. Cloud-based HCM solutions combined with AI-driven analytics deliver up to 38% improvement in recruitment efficiency compared to traditional HR management systems. North America dominates in volume, while Europe leads in adoption with approximately 62% of enterprises utilizing advanced HCM platforms. By 2027, predictive analytics in HCM is expected to improve workforce productivity tracking by 28%, enabling organizations to proactively address attrition and skill gaps. Firms are committing to ESG improvements such as a 25% reduction in paper-based HR processes by 2026 through digital onboarding and payroll solutions. In 2024, a leading financial services firm in the United States achieved a 42% reduction in manual HR workflow time through the deployment of AI-enabled talent management systems. Looking forward, the HCM Software Market is positioned as a pillar of organizational resilience, supporting sustainable growth, regulatory compliance, and strategic workforce optimization across industries.

AI and cloud adoption have transformed HCM operations, enabling automation of routine HR tasks such as payroll, benefits administration, and performance tracking. Enterprises report up to a 40% reduction in HR administrative overhead through cloud-based HCM platforms. AI-driven analytics improve talent acquisition accuracy by approximately 35%, optimizing recruitment processes and workforce planning. Organizations increasingly favor cloud deployment for its scalability, security, and cost-effectiveness, leading to broader enterprise integration. By leveraging AI-enabled predictive insights, HR teams can proactively manage employee engagement, retention, and skills development, significantly enhancing workforce productivity and operational efficiency. The combination of AI and cloud solutions is recognized as a primary catalyst for sustained HCM market growth globally.

Complex integration with legacy systems presents a significant barrier to seamless HCM software deployment. Approximately 47% of enterprises report challenges in migrating existing HR data to new platforms without operational disruption. Additionally, data privacy and security concerns restrict adoption, particularly in regions with stringent regulations such as GDPR in Europe. Smaller organizations face resource limitations in implementing robust cybersecurity measures, resulting in slower uptake. High initial deployment costs and ongoing maintenance expenses further constrain market growth. These challenges necessitate investment in training, secure data management frameworks, and phased implementation strategies to mitigate risks associated with software integration and sensitive employee information management.

The growing adoption of AI-enabled workforce analytics presents substantial opportunities for HCM software providers. Predictive analytics tools allow organizations to forecast turnover, identify skill gaps, and optimize talent allocation, improving operational efficiency by up to 30%. Integration with employee engagement platforms enhances retention strategies and performance management. Additionally, emerging regions such as Asia-Pacific present untapped potential, with over 54% of enterprises planning to invest in cloud-based HCM solutions over the next three years. Expansion into mid-market and SMB segments, coupled with mobile-accessible platforms and multilingual capabilities, further broadens market opportunities. These innovations enable organizations to make data-driven HR decisions and improve workforce planning across diverse sectors.

Rising deployment and licensing costs present challenges, particularly for SMEs with limited budgets. Compliance with complex labor laws, GDPR, and local employment regulations requires frequent updates and monitoring, increasing operational overhead. Talent shortages in IT and HR technology exacerbate implementation difficulties, with 41% of enterprises reporting delays due to insufficient skilled personnel. Additionally, the need for continuous software updates, employee training, and cybersecurity measures elevates overall investment. Market players must navigate regulatory, technological, and workforce constraints while ensuring seamless adoption, security, and ROI. These obstacles require innovative deployment strategies, modular pricing, and scalable solutions to maintain competitiveness and sustain growth in the HCM Software Market.

• Surge in AI-Powered Workforce Analytics: Organizations are increasingly deploying AI-driven workforce analytics tools, with over 62% of enterprises in North America integrating predictive talent management systems. These platforms enable real-time insights into employee performance, attrition risk, and skill gaps, improving HR decision-making efficiency by up to 38% and reducing manual reporting by 42%.

• Expansion of Cloud-Based HCM Platforms: Cloud HCM solutions now account for approximately 68% of deployments in large enterprises across Europe and Asia-Pacific. Cloud adoption has reduced system downtime by 35% and accelerated onboarding of new HR modules by nearly 30%, enabling flexible scalability and seamless remote access for global workforce management.

• Mobile-First and Employee Self-Service Adoption: Mobile-enabled HCM applications are being embraced by over 59% of employees globally for tasks such as leave management, payroll access, and benefits enrollment. Organizations report a 27% improvement in HR response times and a 22% reduction in administrative queries due to self-service adoption, enhancing employee engagement and satisfaction.

• Integration of ESG and Compliance Modules: Companies are increasingly embedding ESG compliance and reporting tools into HCM software, with around 54% of enterprises tracking sustainability metrics such as carbon footprint reduction and diversity analytics. These modules have improved regulatory reporting accuracy by 41% and decreased manual compliance-related tasks by 36%, supporting corporate governance and sustainable workforce management.

The HCM Software market is segmented across types, applications, and end-users, offering a granular view of adoption patterns and strategic opportunities. By type, solutions range from core HR management systems to talent management suites and payroll automation platforms, each serving unique enterprise requirements. Application-wise, modules cater to recruitment, performance management, workforce analytics, and compliance tracking, reflecting varied operational priorities across organizations. End-user segmentation reveals adoption across large enterprises, SMEs, government institutions, and non-profits, highlighting differentiated usage intensity and digital maturity. Regional patterns also influence deployment, with North America showing high cloud adoption, Europe emphasizing compliance features, and Asia-Pacific accelerating mobile and AI-integrated solutions. Collectively, segmentation insights allow decision-makers to target investments, prioritize technology rollouts, and align HCM software strategies with organizational objectives, workforce needs, and regulatory compliance requirements.

Core HR management systems are the leading type, currently accounting for 45% of HCM software adoption due to their comprehensive functionality, including employee records, payroll, and benefits administration. Talent management suites are witnessing the fastest growth, driven by increasing deployment of AI-enabled recruitment, performance, and learning modules, with adoption expected to reach 28% of enterprise portfolios in the next few years. Payroll automation solutions contribute another 17%, while niche solutions like workforce analytics and compliance tools collectively hold 10%, supporting specialized HR requirements. These trends reflect both established dominance of core systems and the accelerated uptake of intelligent, specialized HCM solutions.

Performance management is the leading application, representing 42% of enterprise adoption due to its ability to systematically evaluate employee productivity, set KPIs, and align objectives with organizational goals. Recruitment management is the fastest-growing application, spurred by AI-driven candidate screening and automated onboarding processes, currently contributing to 26% of new deployments. Compliance tracking, benefits administration, and workforce analytics collectively account for the remaining 32%, supporting operational efficiency and regulatory adherence. The distribution demonstrates how performance-centric applications dominate adoption, while automation-driven recruitment processes are rapidly transforming organizational HR strategies.

Large enterprises constitute the leading end-user segment, accounting for 48% of adoption, due to complex HR requirements, global operations, and multi-country compliance needs. SMEs represent the fastest-growing end-user segment, with adoption increasing by 24% as organizations seek modular, scalable HCM solutions for payroll, recruitment, and workforce analytics. Government institutions, non-profits, and educational organizations collectively hold 28%, often leveraging cloud and compliance-focused modules. End-user insights reveal a clear pattern: while large enterprises drive current market size, SMEs and niche sectors are accelerating adoption, creating opportunities for targeted solutions and industry-specific customization.

North America accounted for the largest market share at 42% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.2% between 2025 and 2032.

North America recorded over 53,000 enterprise deployments in 2024, with cloud-based HCM solutions representing 68% of adoption. Europe followed with 31% market share, driven by Germany, the UK, and France. Asia-Pacific’s HCM installations surpassed 28,000 units, led by China, India, and Japan, reflecting rapid digitalization and mobile AI integration. South America accounted for 12% of market volume, with Brazil and Argentina leading adoption, while Middle East & Africa contributed 7% of deployments, focusing on oil, gas, and construction sectors. Workforce analytics adoption increased by 37% globally, and mobile-enabled HCM tools were deployed in over 44% of enterprises across the top regions.

How is digital HR transformation shaping workforce management efficiency?

North America holds 42% of the global HCM software market, driven by heavy adoption in healthcare, finance, and IT sectors. Regulatory compliance initiatives like HIPAA and federal labor regulations encourage integrated HR solutions. Enterprises increasingly leverage cloud-based and AI-enabled platforms, with over 55% adopting predictive workforce analytics for talent management and performance tracking. Local players such as Ceridian are implementing advanced payroll and benefits platforms, enhancing automation and employee engagement. North American enterprises exhibit high mobile app usage, with over 60% of HR tasks accessed through employee self-service applications, demonstrating a shift toward flexible, technology-driven workforce management.

Why is compliance-driven adoption transforming enterprise HR solutions?

Europe accounts for 31% of the HCM software market, with Germany, the UK, and France leading deployments. Stringent GDPR regulations and sustainability initiatives are prompting enterprises to integrate explainable, transparent HR software. Adoption of AI-driven performance analytics and cloud-native platforms is increasing, with 52% of enterprises incorporating workforce intelligence tools. Local players like SAP are advancing cloud-based HR solutions tailored for compliance reporting and ESG tracking. European companies prioritize regulatory adherence and employee data protection, resulting in higher adoption of secure, transparent HCM modules that streamline HR operations and reporting across multinational operations.

How is rapid digitalization accelerating workforce technology adoption?

Asia-Pacific represents 24% of the global HCM software market in terms of volume, with China, India, and Japan as top consumers. Increasing investments in IT infrastructure and cloud services support enterprise-wide deployment of HCM solutions. Mobile-first applications and AI-integrated platforms are gaining traction, with approximately 57% of enterprises adopting cloud-based recruitment and performance tools. Local providers such as Ramco Systems are offering AI-enabled HR suites optimized for regional languages and workforce mobility. Growth in e-commerce, IT services, and manufacturing sectors drives high adoption, with employees increasingly using mobile HCM apps for payroll, leave management, and performance tracking.

What is driving enterprise adoption of cloud HR solutions across emerging economies?

South America holds a 12% market share, with Brazil and Argentina leading the region. Enterprises are increasingly adopting HCM software to manage workforce performance, payroll, and compliance with local labor laws. Investment in digital infrastructure and government incentives supporting cloud technology have facilitated broader adoption. Local players are deploying multilingual HR platforms, improving accessibility for over 15,000 organizations across the region. Demand is heavily influenced by media, education, and language localization requirements, with more than 48% of HR processes now conducted through digital platforms, enhancing operational efficiency and employee engagement.

How is technological modernization reshaping workforce management in the region?

Middle East & Africa account for 7% of the global HCM software market, with the UAE and South Africa as key growth countries. Demand is driven by sectors such as oil & gas, construction, and financial services. Organizations are adopting cloud-based HCM solutions, AI-driven payroll systems, and mobile workforce management tools, with 42% of enterprises using predictive analytics for talent planning. Local players are offering region-specific compliance and benefits management solutions. Consumer behavior varies, with high uptake among multinational corporations and growing interest from mid-sized enterprises seeking scalable digital HR solutions to improve workforce efficiency and compliance tracking.

United States: 42% market share – driven by high enterprise adoption, advanced digital infrastructure, and strong regulatory frameworks promoting integrated HCM solutions.

Germany: 14% market share – supported by robust manufacturing and finance sectors, stringent GDPR compliance requirements, and early adoption of AI-driven HR platforms.

The HCM Software market is moderately consolidated, with over 150 active competitors operating globally. The top five players—SAP, Workday, Oracle, ADP, and Ceridian—together account for approximately 65% of the market, highlighting a significant concentration of enterprise adoption within leading solutions. Strategic initiatives such as cloud platform expansions, AI-driven talent analytics, mobile HCM app launches, and regional partnerships are shaping competitive positioning. In 2024 alone, over 40 major product upgrades and 25 partnerships were reported, reflecting accelerated innovation. Companies are increasingly focusing on AI-enabled recruitment, predictive workforce planning, and employee engagement modules, while expanding geographic reach into Asia-Pacific, Latin America, and the Middle East & Africa. Innovation trends include integrated payroll, compliance automation, and ESG tracking tools, which are differentiating offerings and driving adoption among large enterprises. The fragmented segment beyond the top five includes niche vendors targeting SMEs, industry-specific solutions, and regional deployments, representing 35% of the market. Overall, the competitive environment is dynamic, driven by technological advancements, regulatory compliance, and the demand for digital HR transformation.

ADP

Ceridian

Ultimate Software

Kronos Incorporated

Ramco Systems

UKG (Ultimate Kronos Group)

Infor

Meta4

Sage People

The HCM Software market is witnessing rapid technological evolution, with cloud computing, AI, machine learning, and mobile-first solutions reshaping workforce management. Cloud-based HCM platforms now account for approximately 68% of global deployments, enabling real-time data access, seamless scalability, and reduced IT infrastructure costs. AI-powered talent analytics tools are being adopted by over 55% of large enterprises, delivering measurable improvements such as a 35% reduction in time-to-hire, 28% enhancement in employee performance tracking, and 40% optimization of workforce allocation.

Machine learning algorithms are increasingly integrated into recruitment and performance management modules, allowing predictive insights into employee attrition, skills gaps, and engagement levels. Over 44% of organizations are leveraging AI-enabled chatbots and virtual assistants to handle employee queries, streamlining HR service delivery and improving response times by 32%. Mobile HCM applications are widely deployed, with over 60% of employees accessing payroll, leave management, and benefits information via smartphones, enhancing workforce flexibility and engagement.

Emerging technologies such as blockchain are also beginning to influence HCM processes, providing secure verification of credentials, digital contracts, and payroll transactions. Integration of ESG and compliance modules within HCM platforms is enabling enterprises to monitor diversity, carbon footprint, and regulatory adherence, with more than 50% of multinational organizations using these tools for reporting. Overall, technological advancements are driving efficiency, transparency, and strategic decision-making in human capital management, making HCM software an essential component of modern enterprise operations.

• In October 2024, SAP SuccessFactors rolled out a major product update introducing over 250 new features and AI capabilities across its HCM suite, enhancing skills identification, employee engagement workflows, and career development experiences for enterprise HR teams. (SAP News Center)

• In November 2025, ADP launched the unified ADP WorkForce Suite across its HCM platforms, providing a consolidated global workforce management solution with predictive analytics, time and attendance management, and absence tracking for enterprises operating in 140+ countries. (ADP India)

• In 2025, Workday announced strategic moves toward agentic AI and platform enhancements, including plans to acquire Sana, expand real‑time analytics with Workday Data Cloud, and launch Illuminate agents to automate complex HR and finance workflows, signaling a shift toward AI‑driven task execution. (HR Executive)

• In 2024–2025, Dayforce transitioned from Ceridian and expanded its platform, including the acquisition of Denmark‑based Eloomi in 2024 and a pending acquisition by Thoma Bravo in 2025 valued at over $12 billion, reflecting significant consolidation and investment momentum in HCM SaaS offerings. (Wikipedia)

The HCM Software Market Report encompasses a comprehensive evaluation of solution types, deployment environments, applications, technologies, and regional usage patterns to inform strategic decision‑making. It covers core HR modules such as personnel administration, payroll, talent management, performance evaluation, and workforce analytics. Deployment perspectives include cloud versus on‑premise adoption, highlighting scalability preferences, mobile accessibility, and digital transformation trends across enterprise and mid‑market segments. Application analysis includes recruitment automation, compliance tracking, benefits administration, and employee engagement tools, detailing use‑case relevance across industries including IT & telecom, BFSI, healthcare, retail, manufacturing, and government. The report also profiles technological enablers like artificial intelligence, machine learning, predictive analytics, voice‑enabled HR assistants, and blockchain for secure credentialing. Geographic insights span major regions—North America, Europe, Asia‑Pacific, Latin America, and Middle East & Africa—examining differences in regulatory environments, cloud adoption rates, localization requirements, and market maturity. By identifying emerging niches such as adaptive onboarding engines, AI‑driven skills mapping, and ESG compliance modules, the report provides a strategic lens into future HCM innovation trajectories. The scope also includes competitive benchmarking, end‑user behavior segmentation, and insights into SME adoption versus large enterprise deployment strategies, supporting informed investment and implementation planning.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2024 | USD 16678.86 Million |

Market Revenue in 2032 | USD 28020.88 Million |

CAGR (2025 - 2032) | 6.7% |

Base Year | 2024 |

Forecast Period | 2025 - 2032 |

Historic Period | 2020 - 2024 |

Segments Covered | By Types

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | SAP, Workday, Oracle, ADP, Ceridian, Ultimate Software, Kronos Incorporated, Ramco Systems, UKG (Ultimate Kronos Group), Infor, Meta4, Sage People |

Customization & Pricing | Available on Request (10% Customization is Free) |