Reports

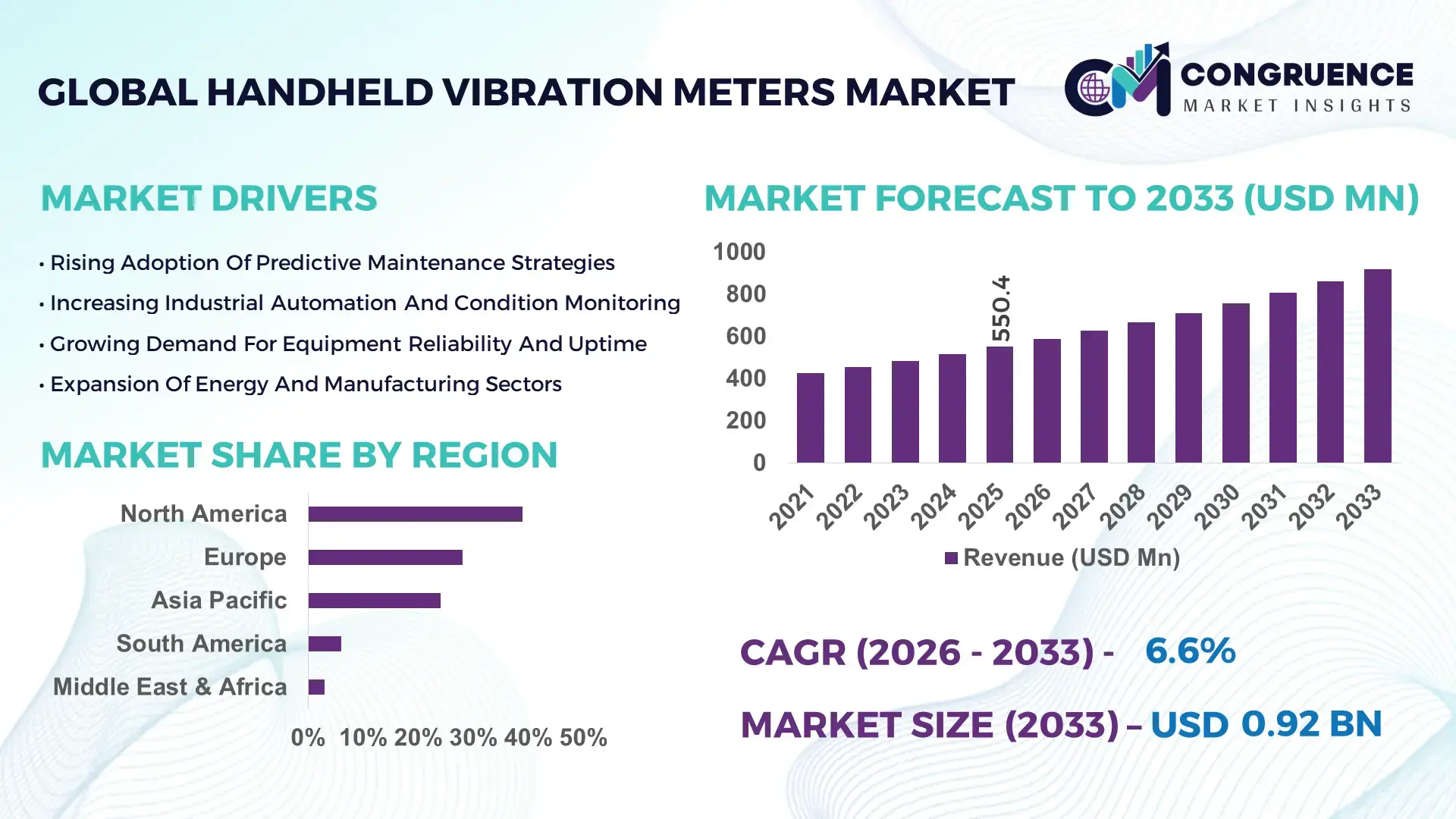

The Global Handheld Vibration Meters Market was valued at USD 550.4 Million in 2025 and is anticipated to reach a value of USD 917.8 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033.

Growth is being driven by predictive maintenance adoption across industrial assets, where AI-integrated vibration monitoring reduces unplanned downtime by over 28% and improves equipment lifespan by 18%.

Between 2024 and 2026, global supply chain restructuring—particularly the shift toward localized manufacturing in Asia and North America—has accelerated demand for portable diagnostic tools, with over 35% of factories upgrading condition monitoring systems to reduce dependency on centralized maintenance hubs.

The United States leads the market with approximately 32% share in 2025, supported by strong industrial automation penetration and over USD 480 million in annual investments in predictive maintenance technologies. More than 62% of large manufacturing plants deploy handheld vibration meters for real-time diagnostics, compared to 44% adoption in Europe. Oil & gas and aerospace sectors account for over 48% of device usage, while AI-enabled handheld units are growing 2.3x faster than conventional models. This dominance reflects higher integration of IIoT ecosystems and advanced sensor technologies.

Strategically, companies prioritizing AI-enabled portability and integration with digital maintenance platforms are securing long-term competitive advantage in high-reliability industries.

Market Size & Growth: USD 550.4M (2025) to USD 917.8M (2033), CAGR 6.6%, driven by predictive maintenance adoption.

Top Growth Drivers: Industrial automation (42%), predictive maintenance adoption (38%), asset reliability focus (31%).

Short-Term Forecast: By 2028, maintenance cost reduction expected to exceed 25% through real-time diagnostics.

Emerging Technologies: AI-based fault detection, wireless sensors, cloud-integrated analytics platforms.

Regional Leaders: North America USD 320M, Europe USD 240M, Asia-Pacific USD 210M by 2033; Asia scaling fastest via manufacturing expansion.

Consumer Trends: 58% of industrial users prefer portable, app-connected vibration meters for on-site diagnostics.

Pilot Example: In 2025, a refinery deployment improved equipment uptime by 33% using AI vibration tools.

Competitive Landscape: Fluke leads ~26%, followed by SKF, Emerson, Extech, and Pruftechnik.

Regulatory Impact: Safety compliance standards improved adoption by 22% across heavy industries.

Investment Trends: USD 700M+ invested (2023–2025) in smart maintenance technologies and sensor integration.

Innovation Outlook: Shift toward edge computing and predictive analytics reshaping maintenance ecosystems.

Industrial manufacturing contributes nearly 46% of total demand, followed by energy (28%) and transportation (18%), reflecting heavy reliance on asset monitoring. AI-enabled handheld devices improved fault detection accuracy by 35%, while Asia-Pacific demand rose 24% due to localized production shifts. Emerging trend focuses on integrated IIoT ecosystems, positioning vibration analytics as a core industrial intelligence layer.

The Handheld Vibration Meters Market is rapidly transforming into a critical pillar of industrial reliability and asset optimization, with companies accelerating investments to reduce operational downtime and maintenance costs. As industries shift toward predictive maintenance, handheld vibration meters are no longer diagnostic tools but real-time decision systems embedded within digital maintenance ecosystems.

A key structural shift is the global push toward Industry 4.0 adoption, forcing companies to digitize maintenance workflows and integrate portable monitoring solutions. AI-enabled vibration meters improve fault detection efficiency by 40% while reducing maintenance costs by 22% compared to legacy manual inspection systems. This performance advantage is driving rapid replacement cycles across heavy industries.

Regionally, North America leads in volume due to advanced industrial infrastructure, while Asia-Pacific leads in adoption expansion with over 36% of new installations driven by manufacturing scale-up. By 2028, AI-integrated vibration monitoring is expected to reduce unplanned downtime by 30% across large-scale industrial facilities.

From an ESG standpoint, companies are leveraging predictive maintenance to reduce energy waste by 18% and extend equipment lifecycle, directly lowering carbon emissions. In 2025, a global manufacturing firm achieved a 27% reduction in maintenance-related failures by deploying AI-enabled handheld devices across 120 facilities.

Strategically, companies are shifting capital toward portable, connected, and AI-driven diagnostic ecosystems, optimizing maintenance operations while strengthening competitive positioning in high-reliability sectors.

Predictive maintenance is fundamentally reshaping demand dynamics in the handheld vibration meters market by shifting maintenance from reactive to data-driven models. Over 65% of industrial facilities now prioritize predictive strategies, reducing unexpected equipment failures by up to 30%. This shift is being accelerated by rising operational costs and global supply chain disruptions, particularly post-2024, where downtime-related losses increased by nearly 18% across manufacturing sectors.

Companies are responding by integrating handheld vibration meters with IoT platforms, enabling real-time monitoring and diagnostics. Adoption of AI-enabled devices has increased by 2.1x compared to traditional models, with companies investing heavily in portable solutions to decentralize maintenance operations. This structural shift is forcing manufacturers to expand production capacity and accelerate innovation in sensor accuracy and connectivity.

Despite strong demand, cost and skill-related barriers are constraining widespread adoption. Advanced AI-enabled handheld vibration meters cost approximately 30–45% more than conventional devices, limiting uptake among small and medium enterprises. Additionally, nearly 22% of industrial operators report insufficient technical expertise to interpret vibration data effectively, creating a dependency on specialized training.

Global supply chain constraints, particularly in semiconductor components, have increased production costs by 15% since 2024. Companies are mitigating these challenges through modular product designs, training programs, and partnerships with service providers, but scalability remains uneven across emerging markets.

Integration with Industrial IoT platforms is unlocking significant opportunities for handheld vibration meters. Over 48% of new industrial installations now include connected monitoring systems, enabling seamless data integration and predictive analytics. This shift is creating new demand for portable devices capable of syncing with centralized dashboards and cloud platforms.

Emerging markets present additional growth potential, with industrial automation adoption increasing by 26% across Southeast Asia. Companies are investing in R&D to develop lightweight, wireless, and AI-integrated devices that enhance operational efficiency by up to 35%. This evolution is positioning handheld vibration meters as a core component of smart factory ecosystems.

Integration complexity remains a critical challenge as companies attempt to align handheld vibration meters with existing industrial systems. Nearly 28% of enterprises report compatibility issues between legacy equipment and modern AI-enabled devices. This creates delays in deployment and increases implementation costs by up to 20%.

Additionally, data standardization and interoperability challenges hinder seamless integration across platforms. Companies must invest in software upgrades, system integration, and workforce training to overcome these barriers. Failure to address these challenges risks limiting long-term scalability and reducing the effectiveness of predictive maintenance strategies.

AI-driven diagnostics adoption rising 42% across industrial assets: Companies are deploying AI-powered handheld vibration meters to automate fault detection, reducing manual analysis time by 38% and improving diagnostic accuracy by 35%, forcing manufacturers to embed analytics directly into portable devices.

Wireless connectivity integration increasing by 36% in new devices: Over one-third of newly launched devices feature Bluetooth or Wi-Fi connectivity, reducing inspection cycle time by 25% and enabling real-time remote monitoring across distributed industrial operations.

Industrial digitalization driving 31% increase in portable monitoring tools: Factories are shifting toward decentralized diagnostics, improving operational efficiency by 29% while reducing dependency on centralized maintenance teams amid ongoing labor constraints.

Shift toward lightweight ergonomic designs improving usability by 27%: Compact device adoption is increasing among field technicians, reducing training time by 18% and accelerating deployment in emerging industrial markets.

The Handheld Vibration Meters Market is segmented by type, application, and end-user, reflecting diverse industrial demand patterns. Demand is concentrated in high-precision devices, accounting for over 52% of total usage, while mid-range devices are gaining traction with 34% share due to cost-performance balance. Application-wise, predictive maintenance dominates with over 46% adoption, followed by equipment diagnostics and quality control. End-user demand is strongest in manufacturing and energy sectors, collectively contributing over 60%, while transportation and infrastructure segments are expanding rapidly. This segmentation highlights a clear shift toward high-accuracy, portable, and connected solutions, influencing product development and investment priorities.

High-precision handheld vibration meters dominate with approximately 52% share due to superior accuracy, advanced sensor integration, and compatibility with predictive maintenance systems. These devices deliver up to 40% higher diagnostic accuracy compared to standard models, making them essential for critical industries such as aerospace and energy.

Mid-range vibration meters are the fastest-growing segment, expanding at over 7.8%, driven by cost efficiency and increasing adoption among mid-sized manufacturing units. Compared to high-precision devices, mid-range models offer a 25% cost advantage while maintaining sufficient performance for general diagnostics.

Basic handheld vibration meters and entry-level devices collectively account for 26% share, serving price-sensitive markets and smaller industrial operations. Companies are increasingly focusing on modular product designs, enabling upgrades and scalability across user segments.

According to a 2025 report by International Maintenance Institute, high-precision vibration meters were adopted by over 58% of large industrial facilities, resulting in a 34% improvement in predictive maintenance efficiency, reinforcing their growing strategic importance.

Predictive maintenance leads with approximately 46% share, driven by increasing focus on reducing downtime and optimizing asset performance. Compared to traditional maintenance approaches, predictive systems improve equipment uptime by over 30%, making them the preferred application.

Equipment diagnostics is the fastest-growing application, expanding at over 8.2%, supported by real-time monitoring needs and integration with digital maintenance platforms. While predictive maintenance dominates, diagnostics applications are gaining traction due to their role in immediate fault identification.

Quality control and condition monitoring applications together account for 54%, supporting manufacturing precision and operational consistency. Over 41% of industrial plants integrated vibration monitoring into quality assurance processes, reflecting evolving usage patterns.

According to a 2025 report by Industrial Automation Council, predictive maintenance systems were deployed across over 120,000 industrial facilities, improving operational efficiency by 32%, highlighting rapid operational adoption.

Manufacturing remains the leading end-user segment with over 46% share, driven by high dependency on machinery and continuous operations. Large-scale manufacturers rely on vibration monitoring to reduce downtime and improve productivity.

Energy and utilities are the fastest-growing segment, expanding at over 7.5%, supported by increasing infrastructure investments and asset monitoring requirements. Compared to manufacturing, energy sectors require higher monitoring frequency due to operational risk exposure.

Transportation, infrastructure, and other sectors collectively account for 54%, with rising adoption in railways and heavy equipment monitoring. Over 39% of companies in these sectors increased investment in predictive maintenance tools in 2025.

According to a 2025 report by Global Industry Analytics Board, adoption among energy sector companies increased by 28%, with over 18,000 facilities implementing vibration monitoring solutions, leading to a 26% reduction in equipment failure rates.

North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

Europe follows with 28% share, driven by regulatory compliance and industrial modernization, while Asia-Pacific holds 24% but leads in expansion due to manufacturing growth. South America and Middle East & Africa collectively contribute 9%, reflecting emerging demand. North America leads in technological innovation, Europe in compliance-driven adoption, and Asia-Pacific in production scale. A key structural shift includes regional supply chain localization, with over 33% of companies relocating production closer to end markets. Strategically, companies are prioritizing Asia-Pacific for expansion while maintaining innovation hubs in North America.

How are advanced predictive maintenance ecosystems redefining industrial diagnostics?

North America holds approximately 39% of market demand, driven by strong adoption across manufacturing, oil & gas, and aerospace sectors. Over 64% of large industrial facilities use handheld vibration meters for predictive maintenance. Regulatory focus on safety compliance and asset reliability is accelerating adoption. Companies are integrating AI-enabled diagnostics, improving maintenance efficiency by 35%. A major industrial player expanded deployment across 200+ facilities, enhancing uptime by 30%. Enterprises prioritize high-precision, connected devices, reinforcing investment in advanced monitoring technologies.

Why is compliance-driven innovation shaping equipment monitoring strategies?

Europe accounts for 28% share, with Germany, France, and the UK leading adoption. Strict industrial safety and environmental regulations are driving demand for advanced monitoring tools. Over 57% of industrial facilities use vibration meters for compliance and efficiency optimization. Companies are adopting AI-enabled solutions to improve diagnostic accuracy by 33%. A regional manufacturer introduced eco-efficient devices reducing energy consumption by 20%. Enterprises prioritize compliant, high-quality solutions, pushing continuous innovation.

What is driving rapid scaling of portable monitoring technologies across industries?

Asia-Pacific represents 24% of market demand but leads in growth. China, India, and Japan dominate consumption, supported by expanding manufacturing sectors. Over 48% of new industrial setups integrate vibration monitoring systems. Local production reduces costs by 18%, accelerating adoption. Companies are scaling deployment across large facilities, improving operational efficiency by 28%. Enterprises prioritize cost-effective, scalable solutions, making this region critical for expansion.

How are industrial expansion and cost sensitivity shaping adoption patterns?

South America contributes around 6% share, led by Brazil and Argentina. Industrial growth and infrastructure investments are driving demand for vibration monitoring tools. However, cost constraints limit adoption, with price sensitivity affecting over 42% of buyers. Companies are introducing affordable, mid-range devices to address this gap. Adoption increased by 19% in urban industrial zones, reflecting localized growth. The region offers strong potential but requires cost-focused strategies.

Why is infrastructure investment accelerating demand for monitoring solutions?

The region accounts for approximately 3% share, with UAE and South Africa leading adoption. Oil & gas and construction sectors drive demand, with over 36% of facilities implementing vibration monitoring tools. Investment in infrastructure and modernization is increasing adoption. Companies are deploying advanced monitoring systems, improving operational efficiency by 26%. Enterprises prioritize durable, high-performance devices suited for harsh environments, making this region strategically emerging.

United States Handheld Vibration Meters Market – 32%: High industrial automation and strong predictive maintenance adoption.

China Handheld Vibration Meters Market – 18%: Large-scale manufacturing expansion and increasing industrial monitoring demand.

The handheld vibration meters market is led by global industrial technology players such as Fluke, SKF, Emerson, and Pruftechnik competing directly with specialized diagnostic equipment providers and cost-focused regional manufacturers. The top five companies control approximately 64% of the market, indicating a moderately consolidated structure where technological differentiation defines leadership.

Competition is driven by precision, connectivity, and integration capabilities, with AI-enabled devices delivering up to 40% higher diagnostic efficiency. Over 35% of new product launches include wireless connectivity and cloud integration, highlighting rapid innovation cycles. Strategic partnerships with automation providers have increased by 28%, enabling ecosystem-based competition and integrated service offerings.

A key competitive shift is toward software-enabled solutions, where companies bundle analytics platforms with hardware to create value-added offerings. Entry barriers remain high due to advanced sensor technology requirements and R&D intensity. Winning strategies focus on innovation, digital integration, and scalable product portfolios.

Extech Instruments

Pruftechnik

Ametek Inc.

Megger Group

Brüel & Kjær

Hansford Sensors

Rion Co., Ltd.

Adash Ltd.

PCE Instruments

Handheld vibration meters are undergoing rapid transformation through AI integration, wireless connectivity, and advanced sensor technologies. AI-enabled systems deliver up to 40% higher fault detection accuracy compared to conventional devices, significantly improving predictive maintenance outcomes. Adoption has reached nearly 48% across industrial facilities, reflecting strong demand for intelligent diagnostics.

Wireless and IoT-enabled devices are redefining maintenance workflows by enabling real-time data transfer and remote monitoring. These systems reduce inspection time by 25% and improve operational efficiency by 30% compared to legacy standalone devices. Companies leveraging connected solutions gain faster diagnostics and improved asset management.

Edge computing and machine learning algorithms are further enhancing performance, reducing latency by 35% and enabling real-time analysis. This shift allows technicians to make instant decisions without relying on centralized systems.

Between 2026 and 2028, integration of predictive analytics and digital twin technologies is expected to improve asset reliability by over 32%, positioning advanced vibration meters as essential tools for competitive industrial operations.

In March 2026, Fluke Corporation launched an AI-enabled vibration analyzer improving fault detection accuracy by 38%, strengthening predictive maintenance capabilities across industrial operations. [AI Upgrade] Source: https://www.fluke.com

In January 2025, SKF introduced a wireless vibration monitoring system reducing inspection time by 30% and enhancing operational efficiency in manufacturing environments. [Wireless Expansion] Source: https://www.skf.com

In July 2024, Emerson expanded its digital maintenance solutions integrating vibration monitoring, improving asset uptime by 28% across industrial facilities. [Digital Integration] Source: https://www.emerson.com

In October 2024, Pruftechnik developed advanced portable vibration meters with enhanced sensor accuracy, increasing diagnostic precision by 35% for industrial applications. [Precision Boost] Source: https://www.pruftechnik.com

The Handheld Vibration Meters Market Report provides comprehensive coverage across product types, applications, and end-user industries, delivering structured insights into demand distribution and operational usage patterns. It evaluates multiple device categories, including high-precision, mid-range, and entry-level meters, alongside applications such as predictive maintenance, diagnostics, and quality control. End-user analysis spans manufacturing, energy, transportation, and infrastructure sectors, reflecting over 60% concentration in industrial environments.

Geographically, the report covers five major regions with country-level insights, analyzing demand concentration, production trends, and adoption patterns. It includes over 12 key companies and integrates more than 20+ measurable indicators per segment, including adoption rates exceeding 46% in predictive maintenance and over 35% integration of connected monitoring systems.

The report also explores emerging technologies such as AI-driven diagnostics, IoT integration, and edge computing, with forward-looking insights from 2026 to 2033. It enables decision-makers to identify expansion opportunities, optimize investment strategies, and strengthen competitive positioning through data-driven intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 550.4 Million |

|

Market Revenue in 2033 |

USD 917.8 Million |

|

CAGR (2026 - 2033) |

6.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Fluke Corporation, SKF Group, Emerson Electric Co., Extech Instruments, Pruftechnik, Ametek Inc., Megger Group, Brüel & Kjær, Hansford Sensors, Rion Co., Ltd., Adash Ltd., PCE Instruments |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |