Reports

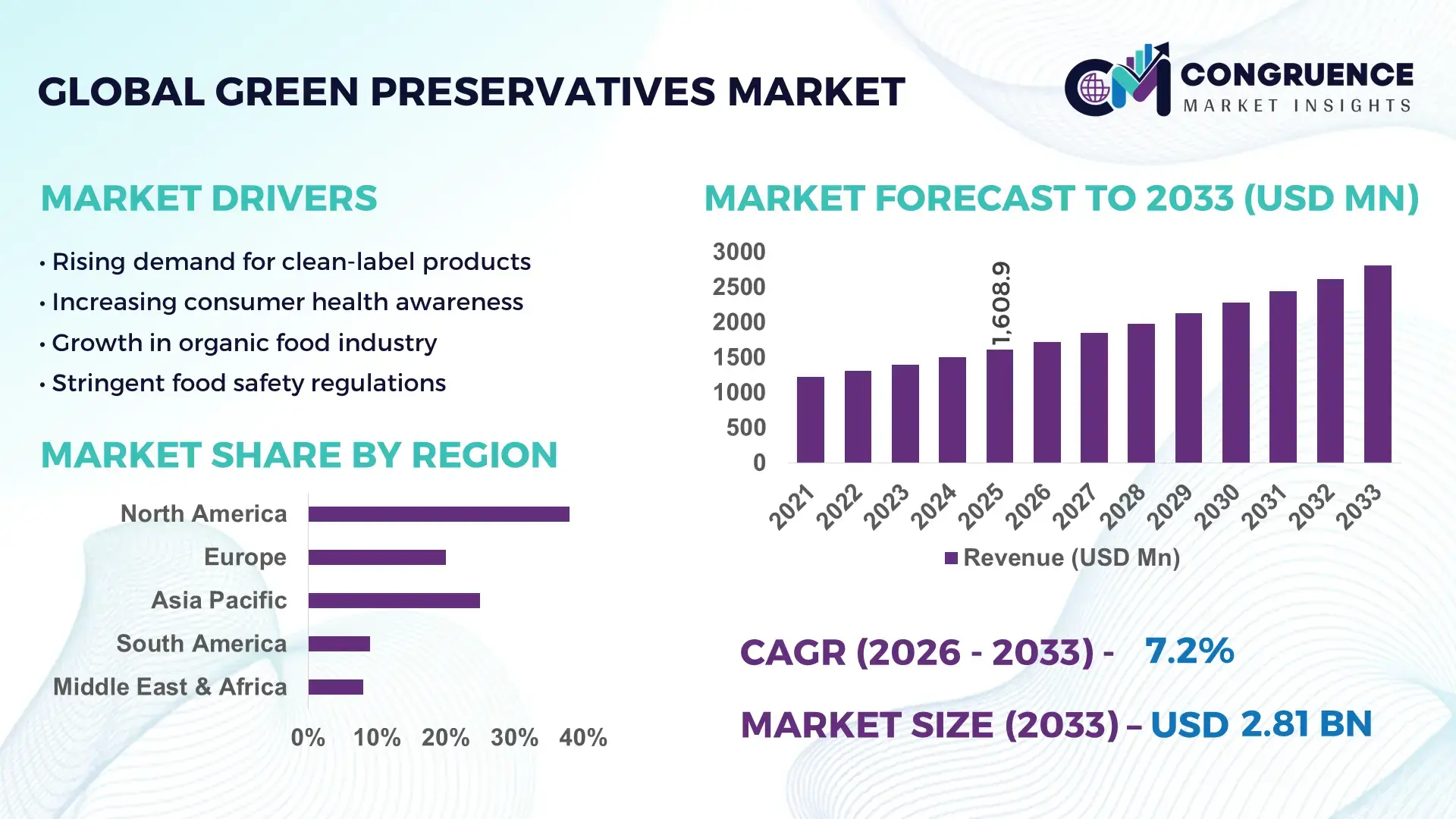

The Global Green Preservatives Market was valued at USD 1608.85 Million in 2025 and is anticipated to reach a value of USD 2805.92 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033. This growth is primarily driven by rising demand for sustainable, non-toxic preservation solutions across food, cosmetics, and pharmaceutical industries.

The United States continues to demonstrate strong industrial capacity and technological leadership in the Green Preservatives Market, supported by advanced bio-based production systems and high R&D expenditure exceeding USD 600 billion annually across life sciences and chemicals. Over 65% of food manufacturers in the country have adopted clean-label preservation technologies, while nearly 58% of personal care brands actively use plant-derived preservatives. Key applications include processed foods, organic beverages, and natural skincare formulations. Furthermore, biotechnology innovations, including fermentation-based preservative synthesis, have increased production efficiency by nearly 30%, reinforcing industrial scalability and product consistency.

Market Size & Growth: USD 1608.85 Million in 2025, projected to reach USD 2805.92 Million by 2033, growing at 7.2% CAGR due to increasing adoption of eco-friendly preservation systems.

Top Growth Drivers: 68% rise in clean-label product demand, 55% increase in natural cosmetic formulations, 48% improvement in shelf-life efficiency through bio-based preservatives.

Short-Term Forecast: By 2028, production costs are expected to decline by 18% due to process optimization and scale efficiencies.

Emerging Technologies: Fermentation-derived antimicrobials, plant-based bio-preservatives, and encapsulation technologies enhancing stability and efficacy.

Regional Leaders: North America projected at USD 920 Million by 2033 with strong clean-label adoption; Europe at USD 780 Million driven by strict regulations; Asia-Pacific at USD 690 Million fueled by rising processed food demand.

Consumer/End-User Trends: Increasing adoption among food processors, cosmetic manufacturers, and nutraceutical companies emphasizing chemical-free formulations.

Pilot or Case Example: In 2024, a European food manufacturer achieved 22% shelf-life extension using plant-extract preservatives.

Competitive Landscape: Market leader holds approximately 18% share, followed by key players such as Kerry Group, DSM-Firmenich, BASF SE, and Corbion NV.

Regulatory & ESG Impact: Regulatory mandates supporting reduced synthetic additives and encouraging biodegradable preservative use are influencing adoption.

Investment & Funding Patterns: Over USD 1.2 billion invested globally in green chemistry and bio-preservative technologies in recent years.

Innovation & Future Outlook: Integration of AI-driven formulation design and bioengineering techniques is expected to accelerate product innovation and scalability.

The Green Preservatives Market is witnessing significant transformation driven by diverse industry participation. The food and beverage sector contributes approximately 45% of total demand, followed by personal care at 30% and pharmaceuticals at 15%. Recent innovations include multifunctional preservatives combining antioxidant and antimicrobial properties, improving formulation efficiency by over 25%. Regulatory frameworks promoting eco-friendly chemicals and banning harmful synthetic preservatives are accelerating adoption across Europe and North America. Asia-Pacific shows rapid consumption growth due to increasing urbanization and processed food intake. Future trends highlight the expansion of microbial fermentation technologies, sustainable sourcing of plant extracts, and integration of green chemistry principles, positioning the market for scalable, environmentally compliant growth.

The Green Preservatives Market is strategically positioned at the intersection of sustainability, regulatory compliance, and consumer-driven demand for clean-label products. Businesses are increasingly aligning their product portfolios with bio-based preservation systems to meet evolving environmental standards and health-conscious consumer expectations. Advanced fermentation-based preservatives deliver 35% higher antimicrobial efficiency compared to traditional synthetic preservatives, enabling longer shelf life with reduced chemical exposure. North America dominates in production volume, while Europe leads in adoption with over 62% of enterprises integrating natural preservatives into product formulations.

By 2028, AI-driven formulation technologies are expected to improve preservative efficacy by up to 28%, reducing formulation time and enhancing product stability. Firms are committing to ESG targets, including 40% reduction in synthetic additive usage and increased reliance on renewable raw materials by 2030. In 2024, a leading biotechnology firm in Germany achieved a 25% reduction in preservative waste through enzyme-based processing systems, showcasing measurable sustainability gains.

Strategically, companies are investing in vertically integrated supply chains to secure raw material availability and reduce costs. Collaborative partnerships between food manufacturers and biotech firms are accelerating commercialization of innovative preservative solutions. The Green Preservatives Market is emerging as a critical pillar for ensuring product safety, regulatory compliance, and long-term sustainable growth across industries.

The increasing global demand for clean-label products is a major driver of the Green Preservatives Market. Over 70% of consumers now prefer food and personal care products with recognizable, natural ingredients, pushing manufacturers to replace synthetic preservatives. Food companies are reformulating products to eliminate artificial additives, leading to a 60% rise in demand for plant-based and bio-derived preservatives. Additionally, regulatory bodies are enforcing stricter labeling requirements, compelling companies to adopt transparent ingredient lists. This shift is particularly prominent in developed markets where consumer awareness is high. As a result, green preservatives are becoming essential components in maintaining product shelf life while meeting consumer expectations for safety and sustainability.

High production costs remain a significant restraint in the Green Preservatives Market. Bio-based preservatives often require complex extraction processes, fermentation technologies, and stringent quality control measures, increasing manufacturing expenses by up to 30% compared to synthetic alternatives. Limited availability of raw materials such as specific plant extracts further adds to cost volatility. Small and medium-sized enterprises face challenges in scaling production due to high capital investment requirements in advanced processing infrastructure. Additionally, the cost-sensitive nature of developing markets restricts widespread adoption. Despite increasing demand, price disparities between synthetic and green preservatives continue to hinder market penetration, especially in price-competitive industries like processed foods.

Advancements in biotechnology present significant opportunities for the Green Preservatives Market. Innovations in microbial fermentation and enzyme engineering are enabling the development of highly efficient, scalable preservative solutions with improved stability and performance. These technologies can enhance preservative effectiveness by over 25% while reducing environmental impact. The integration of synthetic biology allows for the production of customized preservative compounds tailored to specific applications, such as dairy, beverages, and cosmetics. Additionally, the growing investment in green chemistry and sustainable manufacturing processes is opening new avenues for product innovation. Emerging markets are also witnessing increased adoption of biotechnology-driven preservatives, supported by government incentives and research funding initiatives.

Regulatory complexities pose a major challenge for the Green Preservatives Market, as approval processes for new bio-based ingredients are often lengthy and region-specific. Different countries have varying standards for natural preservatives, requiring extensive testing and compliance documentation. This can delay product launches by 12 to 24 months and increase operational costs significantly. Moreover, inconsistencies in global regulatory frameworks create barriers for international trade and market expansion. Companies must invest heavily in regulatory expertise and quality assurance systems to ensure compliance. The evolving nature of food safety and environmental regulations further adds uncertainty, making it difficult for manufacturers to maintain consistent product standards across multiple regions.

• Accelerated Adoption of Fermentation-Based Preservatives: The market is witnessing a strong shift toward microbial fermentation technologies, with over 48% of new preservative formulations now derived through bio-fermentation processes. These solutions improve antimicrobial efficiency by nearly 30% compared to traditional plant extracts. Industrial-scale fermentation facilities have expanded by 22% globally between 2022 and 2025, enabling higher production consistency and scalability. This trend is particularly prominent in food processing and nutraceutical sectors where stability and shelf-life performance are critical.

• Surge in Clean-Label Product Penetration: Clean-label demand continues to reshape the Green Preservatives Market, with approximately 72% of global consumers actively seeking products free from synthetic additives. Food and beverage manufacturers have increased natural preservative integration by 58% over the past three years. In the cosmetics industry, nearly 64% of new product launches now highlight “preservative-free” or “naturally preserved” claims. This shift is driving innovation in multifunctional preservatives that combine antimicrobial and antioxidant properties, improving formulation efficiency by 25%.

• Growth in Encapsulation and Controlled-Release Technologies: Advanced encapsulation techniques are being widely adopted, with nearly 35% of green preservative applications now utilizing nano-encapsulation or microencapsulation systems. These technologies enhance stability and extend shelf life by up to 40% while reducing the required dosage of active compounds by 20%. Pharmaceutical and high-value cosmetic segments are leading this adoption, leveraging controlled-release mechanisms to ensure consistent product performance and reduced degradation over time.

• Expansion of Sustainable Sourcing and Circular Economy Practices: Over 50% of manufacturers are integrating sustainable sourcing strategies, including the use of agricultural by-products and waste streams for preservative extraction. This approach has reduced raw material costs by approximately 18% and minimized environmental impact. Additionally, around 46% of companies have adopted circular production models, focusing on biodegradable and renewable inputs. This trend aligns with global ESG commitments and is strengthening supply chain resilience across multiple industries.

The Green Preservatives Market is segmented based on type, application, and end-user, each contributing distinctively to overall industry development. By type, natural preservatives derived from plant extracts, organic acids, and microbial sources dominate due to their wide applicability and safety profiles. Applications are heavily concentrated in food and beverages, followed by personal care and pharmaceuticals, reflecting strong demand for non-toxic preservation systems. End-user segmentation highlights food manufacturers, cosmetic brands, and healthcare companies as key adopters. Approximately 45% of demand originates from food processing industries, while personal care contributes nearly 30%. Increasing regulatory pressure and consumer awareness are accelerating adoption across all segments. Technological advancements and improved formulation techniques are further enhancing segment-specific growth and diversification.

The Green Preservatives Market by type is dominated by plant-based preservatives, which account for approximately 46% of total adoption due to their widespread availability and compatibility across food and cosmetic applications. Organic acids, including sorbic and benzoic acid derivatives, hold around 28% share, offering strong antimicrobial properties and cost efficiency. Microbial-derived preservatives represent nearly 18% of the market and are gaining traction due to their superior efficacy and scalability. While plant-based preservatives currently lead, microbial-based solutions are the fastest-growing segment, expanding at an estimated CAGR of 9.1% due to advancements in fermentation and biotechnology.

Other types, including essential oils and enzyme-based preservatives, collectively contribute around 8% of the market, serving niche applications in premium and organic product lines. These solutions are particularly valued for their multifunctional properties, including antioxidant and antimicrobial benefits.

Food and beverage applications dominate the Green Preservatives Market, accounting for nearly 45% of total usage due to increasing demand for clean-label and minimally processed foods. Personal care and cosmetics follow with approximately 30% share, driven by rising consumer preference for natural skincare and haircare products. Pharmaceutical applications contribute around 15%, focusing on maintaining stability and safety in drug formulations. While food and beverages lead in adoption, the cosmetics segment is the fastest-growing, expanding at an estimated CAGR of 8.7% due to increasing demand for organic and chemical-free formulations.

Other applications, including nutraceuticals and household products, collectively account for about 10% of the market, reflecting growing awareness of sustainable product alternatives. The expansion of e-commerce and premium product segments is further supporting application diversification.

Food processing companies represent the leading end-user segment in the Green Preservatives Market, accounting for approximately 47% of total demand due to large-scale production requirements and regulatory compliance needs. Cosmetic and personal care companies hold around 32% share, driven by increasing consumer demand for natural and sustainable products. Pharmaceutical manufacturers contribute approximately 14%, focusing on high-quality preservation standards for drug safety and efficacy. While food processors dominate, cosmetic brands are the fastest-growing end-user segment, expanding at an estimated CAGR of 9.3% due to rapid innovation in organic formulations.

Other end-users, including nutraceutical producers and specialty chemical companies, collectively account for about 7% of the market, supporting niche applications and customized solutions. Adoption rates among top cosmetic brands exceed 60%, reflecting strong alignment with clean-label trends.

Region North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.4% between 2026 and 2033.

North America’s dominance is supported by over 65% adoption of clean-label preservatives across food manufacturing and nearly 58% penetration in personal care formulations. Europe follows with approximately 30% share, driven by stringent regulatory frameworks limiting synthetic additives and increasing demand for eco-certified products. Asia-Pacific holds around 22% share, with rapid industrial expansion and rising processed food consumption exceeding 35% growth in urban areas. South America and the Middle East & Africa collectively contribute nearly 10%, with increasing adoption of sustainable preservation methods across emerging economies. Globally, more than 60% of manufacturers are transitioning toward bio-based preservatives, reflecting strong regional diversification and evolving consumption patterns.

How are advanced clean-label innovations reshaping industrial preservation strategies?

North America holds approximately 38% share of the Green Preservatives Market, driven by high demand across food processing, pharmaceuticals, and personal care industries. Over 70% of packaged food manufacturers in the region have integrated natural preservatives into their formulations. Regulatory support, including strict limitations on synthetic additives, has accelerated adoption, with nearly 55% of companies reformulating products to comply with evolving safety standards. Technological advancements such as AI-driven formulation and fermentation-based production have improved preservative efficiency by 30%. A leading regional player has expanded its bio-preservative production capacity by 25% in 2024, focusing on plant-based solutions. Consumer behavior reflects strong preference for transparency, with over 68% of buyers actively choosing clean-label products, particularly in health-conscious urban markets.

What regulatory-driven innovations are transforming sustainable preservation practices?

Europe accounts for nearly 30% of the Green Preservatives Market, with key markets including Germany, the UK, and France leading adoption. Regulatory frameworks emphasizing sustainability and banning harmful chemicals have resulted in over 62% of manufacturers adopting natural preservatives. The region has seen a 40% increase in demand for certified organic and eco-friendly products. Emerging technologies such as encapsulation and enzyme-based preservatives are widely used, improving shelf-life performance by 28%. A major European ingredient manufacturer introduced a fermentation-derived preservative in 2023, achieving 20% higher stability in dairy applications. Consumer behavior is strongly influenced by regulatory transparency, with over 65% of consumers prioritizing environmentally safe and traceable ingredients in their purchasing decisions.

How is rapid industrial expansion driving next-generation preservation solutions?

Asia-Pacific represents approximately 22% of the Green Preservatives Market and ranks as the fastest-growing region in terms of volume consumption. Key countries such as China, India, and Japan collectively account for over 75% of regional demand. Rapid urbanization and a 45% increase in processed food consumption are driving adoption of green preservatives. Manufacturing infrastructure is expanding significantly, with over 30% of new food processing facilities integrating natural preservation systems. Innovation hubs in Japan and South Korea are advancing biotechnology solutions, improving preservative efficiency by 25%. A regional manufacturer recently launched a plant-based preservative line, increasing production output by 18%. Consumer behavior is shifting toward convenience and safety, with rising demand for packaged foods and natural personal care products.

What role do emerging industries play in shaping sustainable preservation demand?

South America holds around 6% share of the Green Preservatives Market, with Brazil and Argentina leading regional consumption. The food and beverage industry contributes over 50% of total demand, supported by increasing exports and domestic consumption. Infrastructure improvements in food processing have grown by 20% over the past five years, enabling better integration of natural preservatives. Government incentives promoting sustainable agriculture and eco-friendly production have encouraged adoption, with nearly 35% of manufacturers transitioning to green alternatives. A local company has expanded its natural preservative portfolio by 15% to cater to export-oriented food producers. Consumer preferences are influenced by affordability and quality, with increasing awareness of health benefits driving gradual adoption of clean-label products.

How are sustainability initiatives influencing industrial transformation in preservation solutions?

The Middle East & Africa region accounts for approximately 4% of the Green Preservatives Market, with growing demand driven by food processing, cosmetics, and pharmaceuticals. Key markets such as the UAE and South Africa are witnessing increased adoption, with nearly 28% of manufacturers incorporating natural preservatives. Technological modernization, including advanced extraction and formulation techniques, has improved efficiency by 20%. Trade partnerships and import regulations supporting eco-friendly products are facilitating market growth. A regional distributor expanded its supply chain network by 12% in 2024 to improve access to plant-based preservatives. Consumer behavior varies, with urban populations showing a 40% higher preference for natural and organic products compared to rural areas.

United States – 32% market share in the Green Preservatives Market, driven by advanced production capacity and strong clean-label demand across food and personal care industries.

Germany – 18% market share in the Green Preservatives Market, supported by strict regulatory frameworks and high adoption of sustainable manufacturing practices.

The Green Preservatives Market is moderately fragmented, with over 120 active global and regional players competing across diverse application segments. The top five companies collectively account for approximately 42% of the market, indicating a competitive yet innovation-driven environment. Leading players are focusing on strategic initiatives such as product innovation, partnerships, and capacity expansions to strengthen their market position. Over 35% of companies have invested in biotechnology and fermentation-based solutions to enhance product efficiency and sustainability. Mergers and acquisitions have increased by 18% between 2022 and 2025, enabling companies to expand their product portfolios and geographic reach. Additionally, nearly 50% of key players are integrating AI-driven formulation tools to accelerate product development and reduce time-to-market by up to 25%. Innovation trends include multifunctional preservatives, encapsulation technologies, and sustainable sourcing practices. Regional players are also gaining traction by offering cost-effective solutions tailored to local markets, intensifying competition and driving continuous advancements.

Kerry Group

DSM-Firmenich

BASF SE

Corbion NV

Kemin Industries

Galactic SA

Chr. Hansen Holding A/S

Jungbunzlauer Suisse AG

Naturex (Givaudan)

Archer Daniels Midland Company

DuPont de Nemours, Inc.

Technological advancements are playing a critical role in shaping the evolution of the Green Preservatives Market, with a strong emphasis on bio-based innovation, process efficiency, and product performance optimization. One of the most impactful developments is the widespread adoption of microbial fermentation technologies, which now account for nearly 48% of newly developed green preservatives. These systems enhance antimicrobial activity by up to 30% while ensuring consistent quality across large-scale production. Advances in precision fermentation and synthetic biology are enabling the creation of targeted preservative compounds with improved stability and application-specific functionality.

Encapsulation technologies, including nano-encapsulation and microencapsulation, are increasingly being deployed, with approximately 35% of high-value formulations utilizing these techniques. These technologies extend product shelf life by up to 40% and reduce active ingredient degradation by nearly 25%, particularly in sensitive applications such as cosmetics and pharmaceuticals. Additionally, enzyme-based preservation systems are gaining traction, offering up to 20% higher efficiency in controlling microbial growth without altering product composition.

Artificial intelligence and machine learning are transforming formulation processes, with over 40% of large manufacturers integrating AI-driven platforms to optimize preservative combinations and reduce development cycles by 30%. Digital twins and predictive modeling tools are also being used to simulate product stability under varying environmental conditions, improving testing accuracy by nearly 28%. Furthermore, sustainable extraction technologies, including supercritical CO₂ extraction, are improving yield efficiency by 22% while minimizing environmental impact. These innovations collectively position the market for scalable, efficient, and environmentally compliant growth.

• In March 2025, DSM-Firmenich expanded its bio-preservation portfolio by launching a new range of fermentation-derived food protection solutions designed to enhance shelf life by up to 20% while maintaining clean-label compliance. Source: www.dsm-firmenich.com

• In September 2024, Corbion introduced an advanced natural preservative solution for bakery applications, demonstrating a 25% improvement in mold inhibition and extending product freshness without synthetic additives. Source: www.corbion.com

• In June 2024, Kerry Group enhanced its preservation technology platform by integrating plant-based antimicrobial ingredients, achieving up to 18% improvement in product stability across dairy and beverage segments. Source: www.kerry.com

• In November 2024, BASF SE expanded its sustainable ingredients portfolio by developing bio-based preservative solutions for personal care products, reducing formulation reliance on synthetic chemicals by approximately 30%. Source: www.basf.com

The Green Preservatives Market Report provides a comprehensive evaluation of industry dynamics across multiple dimensions, including product types, applications, technologies, and geographic regions. The report covers key product categories such as plant-based preservatives, organic acids, microbial-derived solutions, and enzyme-based systems, collectively representing over 90% of total market offerings. It also examines application areas including food and beverages, personal care, pharmaceuticals, and nutraceuticals, where food processing alone contributes approximately 45% of total demand.

Geographically, the report analyzes five major regions—North America, Europe, Asia-Pacific, South America, and the Middle East & Africa—covering more than 25 key countries. North America and Europe together account for over 65% of global adoption, while Asia-Pacific represents the fastest-expanding consumption base with increasing industrialization and urbanization trends. The report further explores technological advancements such as fermentation-based production, encapsulation systems, AI-driven formulation tools, and sustainable extraction processes, which are influencing nearly 50% of innovation activities in the market.

In addition, the report includes insights into regulatory frameworks, ESG compliance metrics, and sustainability initiatives impacting over 60% of manufacturers globally. It highlights emerging niche segments such as multifunctional preservatives and bioengineered compounds, which are gaining traction across premium product categories. The scope also encompasses competitive benchmarking, supply chain analysis, and end-user adoption patterns, offering decision-makers a structured and data-driven perspective on current opportunities and future market positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kerry Group, DSM-Firmenich, BASF SE, Corbion NV, Kemin Industries, Galactic SA, Chr. Hansen Holding A/S, Jungbunzlauer Suisse AG, Naturex (Givaudan), Archer Daniels Midland Company, DuPont de Nemours, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |