Reports

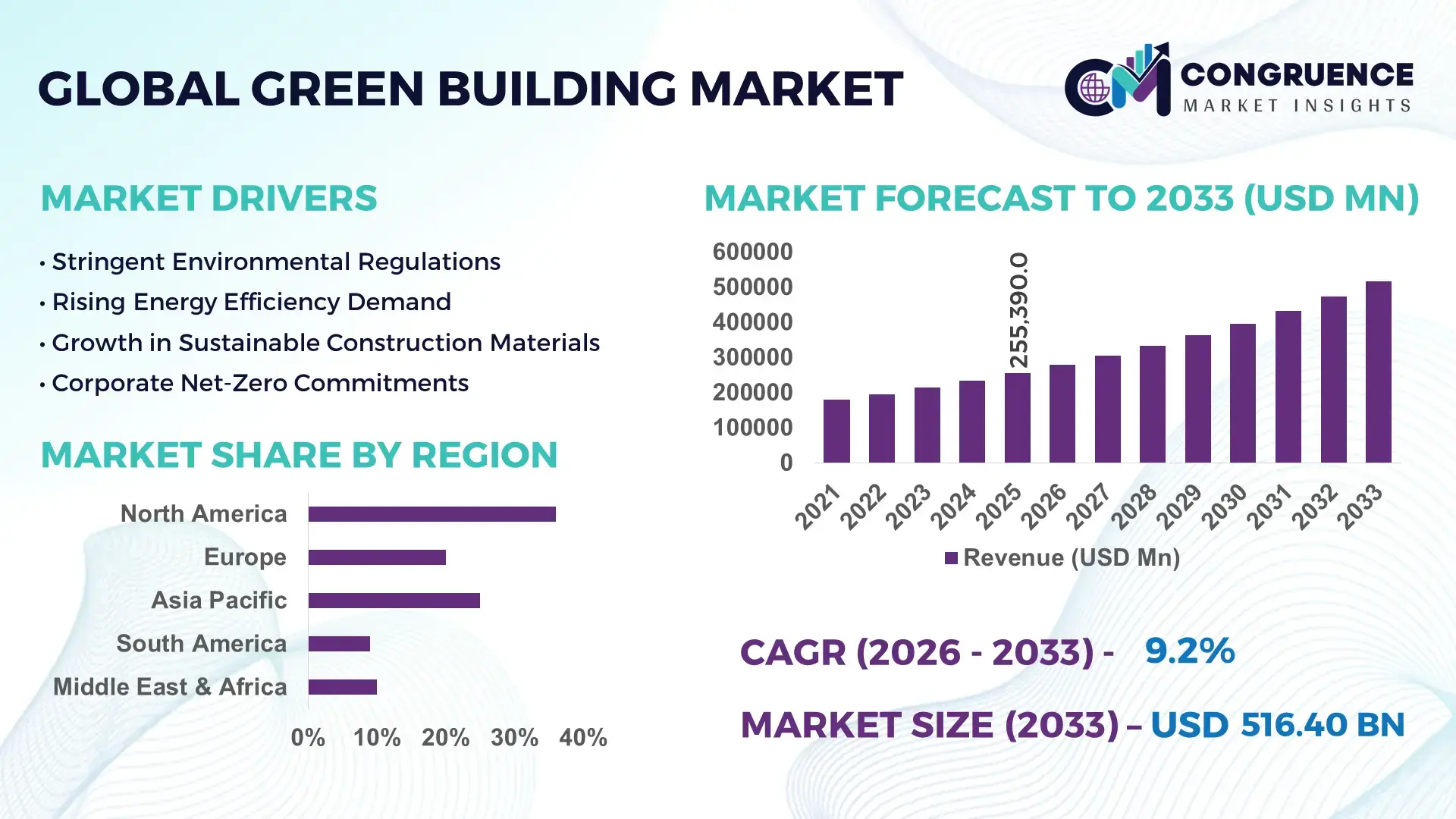

The Global Green Building Market was valued at USD 255390 Million in 2025 and is anticipated to reach a value of USD 516398.52 Million by 2033 expanding at a CAGR of 9.2% between 2026 and 2033. This growth is driven by increasing adoption of sustainable construction practices and energy-efficient infrastructure across residential and commercial sectors.

The United States demonstrates strong dominance in the Green Building Market with extensive large-scale infrastructure investments and advanced sustainable construction capabilities. The country has over 100,000 certified green buildings, with commercial structures accounting for nearly 65% of certified developments. Annual investments in energy-efficient construction and retrofitting exceed USD 30 billion, supporting the integration of renewable energy systems and smart building technologies. More than 40% of new urban developments incorporate green design standards, while IoT-enabled building systems have improved operational energy efficiency by up to 25%. Key sectors such as healthcare, education, and corporate real estate continue to drive adoption, supported by high penetration of automated energy management solutions and low-carbon construction materials.

Market Size & Growth: Valued at USD 255390 Million in 2025 and projected to reach USD 516398.52 Million by 2033 at a CAGR of 9.2%, driven by rapid adoption of eco-friendly construction and energy-efficient building solutions.

Top Growth Drivers: 45% increase in sustainable material adoption, 38% improvement in building energy efficiency targets, 32% rise in green certification compliance.

Short-Term Forecast: By 2028, advanced smart building integration is expected to enhance operational efficiency by 28% and reduce lifecycle energy costs by 20%.

Emerging Technologies: AI-driven building management systems, IoT-enabled energy monitoring platforms, and high-performance insulation materials.

Regional Leaders: North America projected at USD 180000 Million by 2033 with strong retrofit demand; Europe at USD 140000 Million driven by strict environmental regulations; Asia-Pacific at USD 150000 Million supported by rapid urbanization.

Consumer/End-User Trends: Commercial and institutional sectors contribute over 60% of adoption, with increasing demand in residential smart housing developments.

Pilot or Case Example: In 2024, a smart commercial complex project achieved 30% energy savings through AI-based energy optimization systems.

Competitive Landscape: Leading player holds approximately 18% share, followed by major construction, engineering, and sustainable material providers.

Regulatory & ESG Impact: Stringent carbon reduction targets and green building certification frameworks are accelerating market adoption globally.

Investment & Funding Patterns: Over USD 120 billion invested annually in sustainable infrastructure, driven by public-private partnerships and green financing models.

Innovation & Future Outlook: Integration of net-zero building designs, carbon-neutral materials, and digital twin technologies is shaping future market expansion.

The Green Building Market encompasses key sectors including commercial real estate contributing approximately 45% of total demand, followed by residential construction at around 35% and industrial infrastructure accounting for nearly 20%. Technological innovations such as prefabricated sustainable materials, energy-efficient glazing systems, and advanced HVAC solutions are transforming construction practices. Regulatory frameworks promoting net-zero emissions, combined with rising environmental awareness and urbanization trends in Asia-Pacific and Europe, are accelerating adoption. Increasing deployment of renewable energy systems within buildings and digital energy optimization tools further supports long-term market growth and operational efficiency improvements.

The Green Building Market holds significant strategic relevance as global economies transition toward low-carbon infrastructure and sustainable urban development. Advanced technologies such as AI-enabled energy management systems deliver 30% improvement in energy optimization compared to conventional building control systems, enabling substantial reductions in operational costs. North America dominates in construction volume, while Europe leads in adoption with over 55% of new commercial developments integrating certified green building standards.

By 2028, AI-driven predictive maintenance and smart energy analytics are expected to improve building performance efficiency by 35%, reducing maintenance costs and energy waste across large-scale facilities. Firms are committing to ESG targets such as 40% reduction in carbon emissions and 50% recycling of construction waste by 2030, aligning with global sustainability mandates. In 2024, Germany achieved a 25% reduction in building energy consumption through the implementation of smart grid-integrated building technologies and automated energy systems.

Strategically, the integration of digital twin technology, renewable energy systems, and advanced materials is redefining infrastructure resilience. The Green Building Market is increasingly positioned as a critical enabler of sustainable economic growth, regulatory compliance, and long-term environmental performance, supporting global climate objectives and efficient resource utilization.

The growing demand for energy-efficient infrastructure is a major driver of the Green Building Market, supported by measurable improvements in building performance and operational cost savings. Buildings account for nearly 40% of global energy consumption, prompting governments and organizations to adopt advanced energy-saving solutions. The implementation of high-performance insulation, energy-efficient lighting systems, and smart HVAC technologies has resulted in energy savings of up to 30% in commercial buildings. Additionally, green-certified buildings have demonstrated up to 20% lower operating costs compared to traditional structures. The adoption of renewable energy systems, including solar panels and geothermal solutions, is further enhancing energy efficiency and reducing dependence on fossil fuels. Corporate sustainability commitments and increasing investor focus on ESG performance are accelerating the transition toward green construction practices across multiple industry sectors.

High upfront investment costs and complex certification requirements present significant restraints for the Green Building Market, particularly for small and medium-scale developers. The cost of sustainable construction materials and advanced building technologies can be 10% to 20% higher than conventional alternatives, creating financial barriers for widespread adoption. Additionally, green building certification processes often involve stringent compliance standards, extensive documentation, and prolonged approval timelines, which can delay project execution. Limited availability of skilled professionals and technical expertise in sustainable construction further adds to implementation challenges. In developing regions, lack of awareness and insufficient financial incentives also hinder market penetration. These constraints collectively impact the pace of adoption despite the long-term economic and environmental benefits associated with green building practices.

Rapid urbanization and the integration of smart technologies are creating significant growth opportunities in the Green Building Market. Smart city initiatives across Asia-Pacific and Europe are driving the demand for intelligent, energy-efficient infrastructure capable of supporting large urban populations. The deployment of IoT-based building management systems enables real-time monitoring and optimization of energy consumption, improving efficiency by up to 35%. Additionally, the increasing adoption of prefabricated and modular construction techniques is reducing construction time by nearly 25% while enhancing sustainability. Opportunities are also emerging in retrofitting existing buildings with energy-efficient solutions, as older infrastructure accounts for a substantial portion of energy consumption. Government incentives, tax benefits, and green financing programs are further encouraging investments in sustainable construction projects, creating a favorable environment for market expansion.

The Green Building Market faces challenges related to regulatory complexities and supply chain constraints for sustainable materials. Variations in building codes and environmental standards across regions create compliance challenges for developers operating in multiple markets. Additionally, the supply of eco-friendly construction materials, such as recycled steel, low-carbon cement, and high-performance insulation, is often limited, leading to cost fluctuations and project delays. Transportation and logistics issues further impact the availability of specialized materials, particularly in emerging economies. The need for continuous innovation and adaptation to evolving regulatory frameworks also increases operational complexity for industry stakeholders. These challenges require strategic planning, investment in local supply chains, and collaboration across the construction ecosystem to ensure consistent growth and market stability.

Rapid Adoption of Smart Energy Management Systems: The integration of intelligent energy management solutions has increased by over 48% across commercial green buildings, significantly enhancing operational efficiency. These systems leverage AI and IoT technologies to optimize energy consumption, resulting in up to 30% reduction in electricity usage and 22% improvement in building performance. More than 60% of newly constructed green commercial spaces now incorporate real-time energy monitoring platforms, particularly in North America and Europe, where energy optimization is a regulatory priority.

Expansion of Net-Zero and Carbon-Neutral Buildings: The development of net-zero energy buildings has grown by approximately 42% globally, with over 35% of new urban infrastructure projects targeting carbon neutrality. Advanced building materials such as low-carbon concrete and energy-efficient glazing systems have reduced carbon emissions by up to 25% per structure. Governments and private developers are increasingly committing to zero-emission construction, with nearly 50% of large-scale commercial projects integrating renewable energy systems like solar photovoltaics and energy storage solutions.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Green Building market, with around 55% of new projects reporting cost efficiencies through prefabricated practices. Off-site manufacturing of pre-engineered components has reduced construction timelines by nearly 30% and labor requirements by 20%. High-precision automated fabrication technologies are gaining traction, especially in Europe and North America, where demand for faster, cost-effective, and sustainable construction solutions continues to rise.

Increased Use of Sustainable and Recycled Materials: The utilization of eco-friendly construction materials has expanded by 40%, driven by stringent environmental regulations and growing awareness of sustainable practices. Materials such as recycled steel, bamboo composites, and bio-based insulation are now used in over 45% of green building projects, contributing to a 20% reduction in overall construction waste. This trend is further supported by innovations in material science, enabling improved durability, thermal performance, and lifecycle sustainability.

The Green Building Market segmentation is defined by diverse product types, applications, and end-user categories that collectively shape industry demand patterns. In terms of types, energy-efficient materials, smart building systems, and sustainable construction methods dominate adoption, reflecting a strong shift toward integrated infrastructure solutions. Applications are primarily driven by commercial and institutional construction, which account for a substantial portion of green building adoption due to regulatory compliance and operational cost benefits. Residential applications are steadily increasing, supported by rising consumer awareness and urban housing demand. From an end-user perspective, real estate developers, government agencies, and corporate enterprises are key contributors, with increasing investments in sustainable infrastructure projects. The segmentation reflects a balanced mix of innovation-driven adoption and policy-driven growth across global markets.

The Green Building Market by type includes energy-efficient materials, green building software and smart systems, renewable energy integration solutions, and sustainable construction techniques. Energy-efficient materials lead the segment, accounting for approximately 38% of total adoption due to their widespread use in insulation, glazing, and structural components that enhance building performance. In comparison, smart building systems hold around 27%, while renewable energy integration accounts for nearly 20%. However, smart building systems represent the fastest-growing segment, expanding at an estimated CAGR of 11.5%, driven by increasing demand for automated energy optimization and real-time monitoring.

Other types, including water-efficient technologies and eco-friendly construction methods, collectively contribute around 15% of the market, offering niche but critical sustainability benefits. Technological advancements such as AI-enabled building automation and high-performance insulation materials are further accelerating adoption across all segments.

The application segment of the Green Building Market is dominated by commercial construction, which accounts for approximately 45% of total adoption due to high demand for energy-efficient office spaces, retail complexes, and institutional buildings. Residential applications follow with around 35%, while industrial applications represent nearly 20%. However, residential construction is emerging as the fastest-growing application segment, expanding at an estimated CAGR of 10.8%, supported by increasing consumer demand for sustainable housing and government incentives for eco-friendly homes.

Other applications, including public infrastructure and mixed-use developments, collectively contribute about 15% of the market, driven by urbanization and smart city initiatives. The adoption of green building practices in commercial applications has led to operational cost reductions of up to 25%, making it a preferred choice for large enterprises.

End-user segmentation in the Green Building Market highlights real estate developers as the leading segment, accounting for approximately 40% of total adoption due to their active involvement in large-scale construction projects. Government and public sector entities follow with around 30%, while corporate enterprises contribute nearly 20%. However, corporate enterprises are the fastest-growing end-user segment, expanding at an estimated CAGR of 12.2%, driven by ESG commitments and the need for sustainable office environments.

Other end-users, including educational institutions and healthcare organizations, collectively account for about 10% of the market, with increasing adoption of green building standards to improve energy efficiency and occupant well-being. Industry adoption rates indicate that over 50% of large corporations are investing in green-certified office spaces to meet sustainability targets.

Region North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

North America continues to lead due to over 65% of commercial buildings incorporating energy-efficient systems and more than 100,000 certified green structures. Europe follows with approximately 30% share, driven by strict carbon neutrality targets and over 50% of new developments adhering to green certification standards. Asia-Pacific holds nearly 25% of the market, supported by rapid urbanization and infrastructure investments exceeding USD 1 trillion annually across China and India. South America contributes around 5%, with Brazil accounting for over 60% of regional green construction projects. The Middle East & Africa region captures close to 4%, with UAE and South Africa leading adoption through smart city initiatives and sustainable infrastructure projects. Regional growth is further supported by increasing investments in renewable integration, energy-efficient retrofitting, and digital building technologies improving operational efficiency by up to 30%.

North America holds approximately 36% of the Green Building Market, supported by strong demand from commercial real estate, healthcare, and institutional infrastructure sectors. Over 65% of new office developments incorporate energy-efficient HVAC systems and smart energy management solutions. Government initiatives such as tax credits and green building certification programs have accelerated adoption, with more than 70% of large-scale projects complying with sustainability standards. Digital transformation is evident through widespread deployment of AI-based building automation systems, improving energy efficiency by up to 28%. A leading regional construction firm has implemented smart building platforms across over 200 projects, reducing energy consumption by 25% and maintenance costs by 18%. Consumer behavior in this region reflects higher enterprise adoption, particularly in healthcare and financial sectors, where sustainable infrastructure is prioritized for long-term operational savings and ESG compliance.

Europe accounts for nearly 30% of the Green Building Market, with key countries such as Germany, the United Kingdom, and France leading adoption. Over 55% of new commercial buildings in these countries meet stringent environmental standards, driven by regulatory frameworks focused on carbon neutrality and energy efficiency. The region has implemented policies targeting a 40% reduction in building emissions by 2030, significantly influencing construction practices. Emerging technologies such as smart energy grids and advanced insulation systems are widely adopted, improving building performance by up to 30%. A major European construction company has developed low-carbon building materials used in over 500 projects, reducing construction-related emissions by 20%. Consumer behavior reflects strong regulatory influence, with demand for compliant and energy-efficient buildings increasing across both commercial and residential sectors.

Asia-Pacific ranks as the fastest-growing region in the Green Building Market, contributing nearly 25% of global demand. China, India, and Japan are the top consuming countries, with China alone accounting for over 50% of regional green construction projects. Infrastructure investments exceeding USD 1 trillion annually are driving large-scale adoption of sustainable building practices. The region is witnessing rapid expansion in smart city projects, with over 40% of new urban developments integrating energy-efficient systems. Technological innovation hubs in Japan and South Korea are advancing smart building solutions, improving energy efficiency by up to 35%. A leading regional developer has implemented modular green construction techniques across multiple residential projects, reducing construction time by 30%. Consumer behavior is influenced by urbanization and population growth, with increasing demand for affordable, energy-efficient housing solutions.

South America holds approximately 5% of the Green Building Market, with Brazil and Argentina as key contributors. Brazil accounts for over 60% of regional green construction activities, supported by growing investments in energy-efficient infrastructure and renewable energy integration. Government incentives promoting sustainable construction have increased adoption of green materials by nearly 35% across commercial projects. Infrastructure development in urban areas has led to a 25% rise in demand for energy-efficient buildings. A regional construction firm has implemented sustainable design practices in over 100 projects, achieving a 20% reduction in energy consumption. Consumer behavior in this region is influenced by cost efficiency and environmental awareness, with increasing adoption of green building solutions in commercial and residential sectors.

The Middle East & Africa region accounts for nearly 4% of the Green Building Market, with the UAE and South Africa leading development. The UAE has implemented over 1,000 sustainable building projects as part of its smart city initiatives, while South Africa is focusing on energy-efficient infrastructure to address power challenges. The region is witnessing increased adoption of advanced construction technologies, including smart energy systems and water-efficient solutions, improving building efficiency by up to 25%. Government regulations promoting energy conservation and sustainable urban planning are driving adoption, particularly in commercial and hospitality sectors. A leading regional developer has integrated renewable energy systems into large-scale projects, reducing operational energy consumption by 22%. Consumer behavior reflects growing demand for modern, sustainable infrastructure aligned with economic diversification and environmental goals.

United States Green Building Market – 34% share: Strong infrastructure investment and high adoption of energy-efficient commercial buildings drive market leadership.

China Green Building Market – 22% share: Large-scale urban development and government-backed sustainable construction initiatives support rapid expansion.

The Green Building Market is characterized by a moderately fragmented competitive landscape with over 150 active global and regional players operating across construction, materials, and technology segments. The top five companies collectively account for approximately 28% of the market, indicating a competitive yet diversified ecosystem. Major players are focusing on strategic partnerships, mergers, and product innovation to strengthen their market position. Over 40% of companies have invested in digital transformation initiatives, including AI-driven building management systems and smart construction technologies.

Innovation remains a key competitive factor, with more than 35% of firms introducing advanced sustainable materials such as low-carbon concrete and energy-efficient glazing solutions. Strategic collaborations between construction firms and technology providers have increased by 30%, enabling integrated green building solutions. Additionally, companies are expanding their portfolios through acquisitions of specialized sustainability solution providers, enhancing their capabilities in renewable energy integration and smart infrastructure development. The competitive environment is further shaped by increasing demand for ESG-compliant solutions, prompting firms to align their strategies with global sustainability standards and regulatory requirements.

Siemens AG

Schneider Electric SE

Johnson Controls International plc

Honeywell International Inc.

Daikin Industries Ltd.

Saint-Gobain S.A.

Kingspan Group plc

Skanska AB

Turner Construction Company

Lendlease Group

LafargeHolcim Ltd.

Mitsubishi Electric Corporation

The Green Building Market is increasingly driven by advanced digital and material technologies that enhance energy efficiency, reduce carbon emissions, and improve lifecycle performance. Smart building management systems powered by artificial intelligence and IoT sensors are now deployed in over 60% of new commercial green buildings, enabling real-time monitoring and optimization of energy usage. These systems can reduce energy consumption by up to 30% while improving operational efficiency by nearly 25%. Digital twin technology is gaining traction, allowing developers to simulate building performance and predict maintenance needs, reducing downtime by approximately 20%.

Advanced construction materials are also transforming the market, with low-carbon concrete reducing embodied carbon emissions by up to 40% and high-performance insulation improving thermal efficiency by 35%. Energy-efficient glazing systems now reduce heat loss by nearly 50%, significantly lowering heating and cooling requirements. Renewable energy integration is another key technological trend, with over 45% of green buildings incorporating solar photovoltaic systems and energy storage solutions to achieve partial or full energy independence.

Automation and robotics in construction processes are reducing labor requirements by 20% and shortening project timelines by up to 30%, particularly in modular and prefabricated construction. Additionally, water-efficient technologies such as smart water management systems and greywater recycling are reducing water consumption by up to 25% in large-scale buildings. These technological advancements collectively support sustainable infrastructure development and are becoming essential for compliance with evolving environmental regulations and performance standards.

• In March 2025, Schneider Electric launched an advanced EcoStruxure Building platform upgrade that integrates AI-driven analytics to optimize energy consumption, achieving up to 30% improvement in building efficiency and enabling predictive maintenance capabilities across large commercial infrastructures. Source: www.se.com

• In September 2024, Siemens AG expanded its smart infrastructure portfolio by introducing a next-generation building automation system designed to reduce energy usage by 25% and improve occupant comfort through real-time environmental monitoring and control systems. Source: www.siemens.com

• In November 2024, Saint-Gobain introduced a new range of low-carbon glass solutions that reduce embodied carbon emissions by up to 40% while maintaining high thermal insulation performance for sustainable building applications. Source: www.saint-gobain.com

• In January 2025, Johnson Controls International implemented a large-scale smart building project integrating AI-based HVAC optimization systems, resulting in a 28% reduction in energy consumption and enhanced indoor air quality across multiple commercial facilities. Source: www.johnsoncontrols.com

The scope of the Green Building Market Report encompasses a comprehensive evaluation of sustainable construction practices, advanced building technologies, and energy-efficient infrastructure across multiple segments and geographies. The report covers key product categories including energy-efficient materials, smart building systems, renewable energy integration solutions, and sustainable construction techniques, which collectively account for over 80% of market adoption. It also examines applications across commercial, residential, and industrial sectors, with commercial construction representing the largest share due to high demand for energy optimization and regulatory compliance.

Geographically, the report provides detailed insights into North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional consumption patterns, infrastructure investments, and policy frameworks. Asia-Pacific is highlighted for rapid urban expansion, with over 40% of new infrastructure projects integrating green building practices, while Europe focuses on stringent emission reduction targets and regulatory compliance.

The report further explores emerging technologies such as AI-driven energy management, digital twin simulations, and advanced sustainable materials, which are improving building performance by up to 35%. It includes analysis of niche segments such as net-zero buildings, modular construction, and retrofitting of existing infrastructure, which are gaining traction due to increasing environmental awareness and policy incentives. Additionally, the report evaluates end-user industries including real estate developers, government agencies, and corporate enterprises, offering a holistic view of market dynamics, innovation trends, and strategic growth opportunities within the global Green Building Market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

9.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, Schneider Electric SE, Johnson Controls International plc, Honeywell International Inc., Daikin Industries Ltd., Saint-Gobain S.A., Kingspan Group plc, Skanska AB, Turner Construction Company, Lendlease Group, LafargeHolcim Ltd., Mitsubishi Electric Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |