Reports

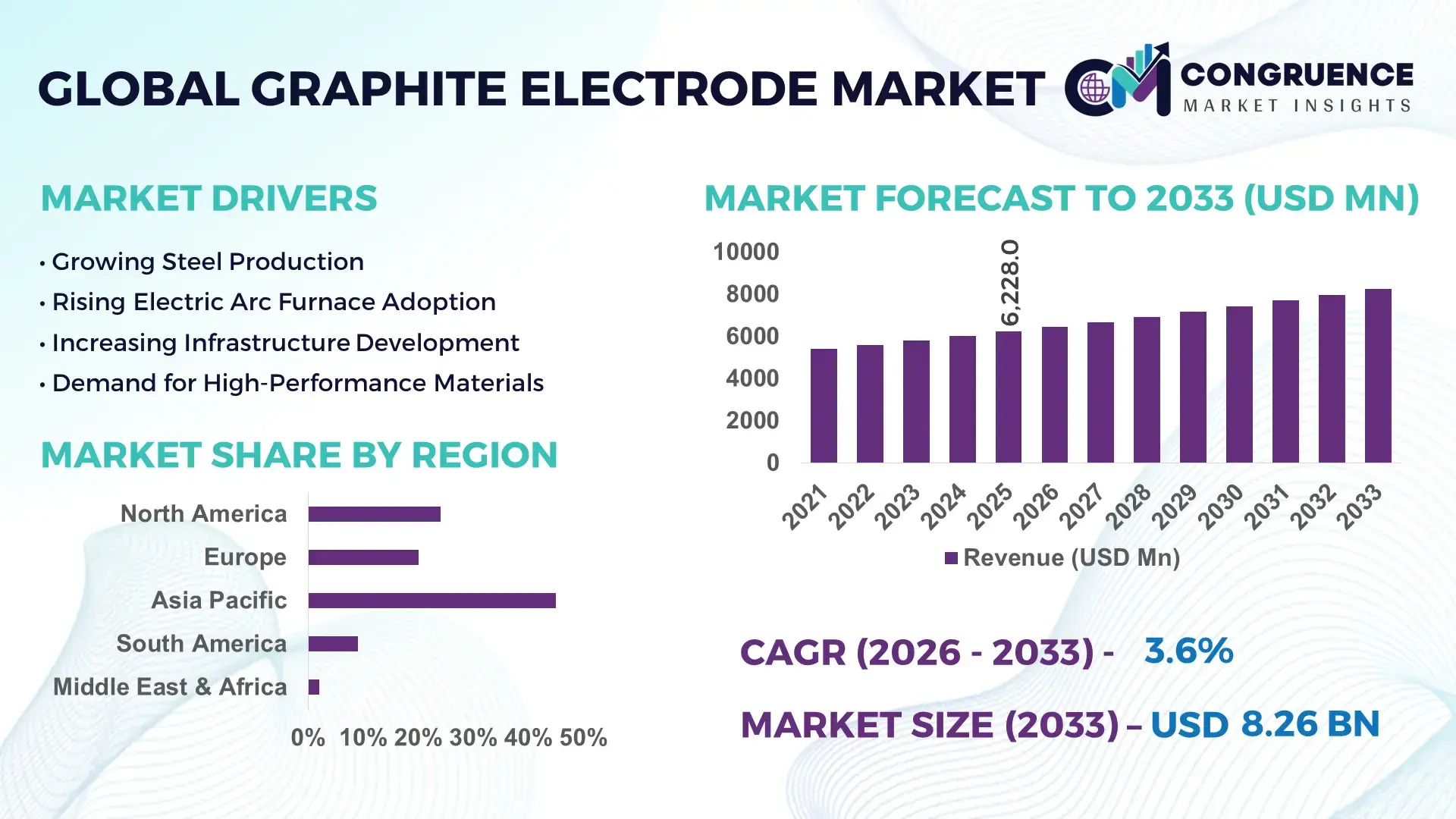

The Global Graphite Electrode Market was valued at USD 6228 Million in 2025 and is anticipated to reach a value of USD 8264.69 Million by 2033 expanding at a CAGR of 3.6% between 2026 and 2033. Growth is being accelerated by electric arc furnace steel production expansion, needle coke capacity integration, and rising ultra-high-power graphite electrode deployment across low-emission steelmaking facilities.

China retained over 52% of global graphite electrode production capacity in 2026, supported by integrated needle coke supply chains and large-scale electric arc furnace steel output exceeding 140 million tons annually. India expanded capacity investments by nearly 11% through new furnace-grade electrode projects linked to infrastructure and automotive steel demand, while Europe increased recycled steel utilization above 46% under carbon reduction mandates following continued Russia-Ukraine energy and raw material disruptions.

Strategic investments in vertically integrated raw material sourcing and high-performance electrode technology are becoming critical for maintaining pricing stability and long-term steel sector competitiveness.

Market Size & Growth: USD 6228 Million in 2025 is projected to reach USD 8264.69 Million by 2033, driven by 38% higher electric arc furnace steel adoption and advanced ultra-high-power electrode demand.

Top Growth Drivers: Electric arc furnace utilization increased 34%, low-emission steel investments rose 29%, and needle coke integration capacity expanded 18% globally.

Short-Term Forecast: By 2028, electrode consumption efficiency improves 12% while operational furnace downtime declines nearly 9% through automated electrode monitoring systems.

Emerging Technologies: AI-based furnace optimization, automated electrode regulation, and advanced impregnation materials improve conductivity performance by 15% in high-output steel plants.

Regional Leaders: Asia Pacific surpasses USD 4.3 Billion with integrated steel expansion, Europe exceeds USD 1.5 Billion through green steel adoption, and North America crosses USD 1.2 Billion from reshoring-driven EAF investments.

Consumer/End-User Trends: More than 61% of secondary steel producers shifted toward ultra-high-power graphite electrodes for faster melting cycles and lower energy intensity.

Pilot/Case Example: In 2026, a large Asian steelmaker reduced electrode consumption by 8% after deploying AI-enabled furnace balancing and predictive thermal monitoring systems.

Competitive Landscape: The top five manufacturers control nearly 47% market share, with capacity expansion focused on premium-grade electrodes and captive needle coke integration.

Regulatory & ESG Impact: European low-carbon steel policies accelerated recycled steel utilization by 14%, increasing demand for advanced graphite electrode solutions amid global supply chain realignment.

Investment & Funding: More than USD 1.1 Billion entered furnace modernization, electrode expansion, and raw material integration projects between 2025 and 2026.

Innovation & Future Outlook: Next-generation oxidation-resistant electrodes and digital furnace analytics are strengthening high-growth steel manufacturing efficiency and long-term supply resilience.

Advanced graphite electrode demand is strengthening across electric arc furnace steelmaking, specialty alloys, and recycled steel production facilities. Manufacturers are integrating oxidation-resistant coatings, AI-enabled furnace analytics, and high-density ultra-high-power electrode designs to improve thermal conductivity and reduce consumption rates by nearly 10%. Asia-based supply diversification and tighter carbon-emission compliance standards are accelerating localized production strategies, creating a stronger foundation for long-term operational and procurement planning across the global graphite electrode market.

Graphite electrodes are becoming strategically critical as steelmakers accelerate electric arc furnace modernization to reduce energy intensity and comply with tightening industrial emission targets. More than 57% of new secondary steel capacity announced in 2026 is linked to electric arc furnace infrastructure, increasing pressure on premium ultra-high-power electrode supply. Simultaneously, supply-chain restructuring after prolonged raw material disruptions has pushed manufacturers in India, China, and the Gulf region to secure captive needle coke sourcing and localized processing capacity.

Advanced ultra-high-power graphite electrodes now deliver nearly 14% longer furnace operating cycles and reduce electrode consumption rates by approximately 9% compared with conventional furnace-grade products. Japan and South Korea continue leading in high-density electrode innovation and automated furnace integration, while India is expanding deployment scale through low-cost steel production clusters. In 2026, a major steel producer in Gujarat integrated AI-based electrode regulation systems that improved furnace stability by 11% and reduced unplanned shutdown frequency during continuous casting operations.

Over the next two to three years, companies are prioritizing oxidation-resistant materials, strategic raw material agreements, and furnace digitalization partnerships to strengthen operational resilience. Competitive advantage will increasingly depend on integrated supply security, electrode performance consistency, and the ability to support low-emission steel production at industrial scale.

Electric arc furnace steel production exceeded 35% of total global steelmaking activity in 2026, directly increasing demand for ultra-high-power graphite electrodes with higher thermal resistance and conductivity. India expanded secondary steelmaking capacity by nearly 12% through infrastructure-linked industrial projects, while China accelerated replacement of older blast furnace assets under industrial decarbonization mandates. This structural transition increased premium electrode consumption intensity by approximately 8% across large-scale steel facilities. In response, manufacturers are expanding captive needle coke integration, long-term supply agreements, and automated production lines to stabilize margins and improve delivery reliability. A notable operational shift involves steel producers prioritizing higher-grade electrodes to reduce furnace interruption frequency, creating stronger supplier preference for technically integrated manufacturers with advanced graphitization capabilities.

The graphite electrode market remains highly exposed to needle coke availability, with more than 65% of premium electrode production dependent on petroleum-based feedstock supply concentration. China and Japan continue controlling a major portion of high-grade needle coke processing, creating procurement pressure for independent electrode manufacturers. During 2026, industrial electricity tariffs in several steel-producing economies increased between 9% and 14%, significantly affecting graphitization and baking operations that require energy-intensive processing cycles. This cost volatility directly impacts pricing stability, production scheduling, and export competitiveness. To reduce operational risk, companies are diversifying raw material sourcing, increasing localized storage capacity, and securing fixed-volume contracts with refinery operators. Some producers are also evaluating synthetic blending technologies to partially offset premium feedstock dependency and improve long-term procurement flexibility.

Rising recycled steel production is creating high-value opportunities for advanced graphite electrode manufacturers capable of supporting continuous high-temperature furnace operations. Europe increased recycled steel utilization above 46% in 2026, while India expanded electric arc furnace installations by nearly 10% across automotive and construction steel hubs. Next-generation oxidation-resistant coatings and AI-enabled electrode monitoring systems are improving electrode lifecycle efficiency by approximately 13%, reducing operational waste and furnace instability. Companies are responding through R&D investments focused on ultra-high-density materials, automated quality analytics, and furnace optimization partnerships. A notable strategic opportunity is emerging in integrated digital service models where electrode suppliers provide predictive maintenance and consumption optimization platforms alongside physical products, strengthening long-term customer retention and operational integration.

Maintaining uniform quality across ultra-high-power graphite electrode production remains a significant execution challenge due to complex graphitization cycles, precision machining requirements, and fluctuating raw material characteristics. Premium electrode rejection rates in some mid-scale facilities still exceed 6%, increasing production losses and delivery delays for steel customers operating continuous melting systems. In Germany and South Korea, stricter industrial emission standards are also forcing upgrades to thermal processing infrastructure and filtration systems, increasing compliance-related capital expenditure by nearly 15%. At the same time, skilled workforce shortages in advanced carbon processing operations are limiting production scalability. Companies must strengthen automation, digital quality inspection, and process control integration while investing in technical training partnerships to maintain long-term competitiveness and consistent electrode performance across global steel manufacturing networks.

AI-Based Furnace Optimization Rising Steel producers in China and India increased deployment of AI-assisted electrode regulation systems by nearly 21% during 2026 to stabilize arc performance and reduce unplanned furnace interruptions. Automated thermal balancing improved electrode consumption efficiency by approximately 8% while shortening melting cycles by 6%. Companies are integrating predictive analytics with furnace control software to offset rising labor costs and improve high-volume secondary steel production consistency.

Localized Needle Coke Integration Expanding Supply-chain disruptions and shipping volatility pushed several electrode manufacturers to restructure raw material sourcing through captive needle coke agreements and domestic storage expansion. Japan and India increased localized procurement contracts by over 17% in 2026, reducing exposure to imported feedstock fluctuations. This operational shift lowered lead-time variability by nearly 11% and strengthened pricing stability for long-duration steel supply contracts.

Oxidation-Resistant Materials Accelerating Advanced oxidation-resistant coatings gained traction across ultra-high-power electrode production, extending furnace operating cycles by approximately 13% compared with standard graphite formulations. South Korean and German manufacturers are scaling high-density electrode engineering to improve conductivity under continuous high-temperature operations. A less visible trend involves automotive-grade steel producers prioritizing premium electrodes to reduce contamination risks during specialty alloy manufacturing.

Digital Quality Inspection Scaling Automated inspection systems using machine vision and real-time graphitization analytics expanded across mid-scale production facilities, reducing electrode defect rates by nearly 9% in 2026. Manufacturers are replacing manual density verification workflows with digital process monitoring to improve machining precision and export-grade consistency. Tightening industrial emission compliance standards are also accelerating investment in energy-efficient baking and purification infrastructure upgrades.

Ultra High Power graphite electrodes remained the dominant segment in 2026, accounting for more than 48% of industrial demand due to their superior conductivity, thermal shock resistance, and compatibility with high-capacity electric arc furnaces. Large steel producers in China, India, and Turkey increasingly prioritized UHP electrodes to support continuous melting operations and lower electrode consumption intensity by nearly 9%. Manufacturers are expanding graphitization capacity, upgrading machining precision, and securing premium needle coke supply agreements to maintain operational consistency for high-output steel facilities.

Synthetic Graphite emerged as the fastest-growing type as steelmakers and specialty alloy producers accelerated demand for higher-purity electrode materials with stable performance under elevated furnace temperatures. Adoption of Synthetic Graphite increased by approximately 14% during 2026, particularly in automotive and engineered steel applications. High Power and Regular Power electrodes continue serving cost-sensitive foundries and mid-scale smelting operations, while Natural Graphite maintains strategic relevance in blended formulations and energy-efficient production processes. Companies are increasingly differentiating portfolios through oxidation-resistant coatings and digitally monitored quality control systems.

Electric Arc Furnaces represented the leading application segment, contributing over 54% of graphite electrode utilization in 2026 due to accelerating recycled steel production and industrial decarbonization initiatives. Secondary steelmakers in India and the United States expanded electric arc furnace deployment by nearly 16%, increasing demand for ultra-high-power electrodes capable of supporting high-current melting environments. Manufacturers are responding through automated electrode management systems, long-term steel producer partnerships, and capacity expansion focused on continuous furnace operations with lower energy intensity.

Steel Production remained the most operationally intensive use case, while Smelting Operations and Non-Ferrous Metal Production recorded faster technology-driven adoption in specialty metals and copper processing facilities. Foundries continue relying on Regular Power and High Power electrodes for medium-scale thermal applications, although process automation is improving consumption efficiency by approximately 7%. Companies are strengthening integration between electrode engineering and furnace analytics platforms to improve melt consistency, reduce downtime, and optimize raw material utilization across industrial processing environments.

The Steel Industry remained the dominant end-user segment in 2026, accounting for nearly 68% of graphite electrode consumption due to the rapid expansion of electric arc furnace steelmaking and recycled steel processing infrastructure. Large integrated steel producers in China, India, and the Gulf region increased procurement of premium-grade electrodes by approximately 15% to support continuous high-temperature operations and lower furnace interruption rates. Manufacturers are responding with customized ultra-high-power product lines, captive raw material integration, and long-term supply partnerships designed to stabilize operational performance across high-volume steel plants.

The Automotive Industry emerged as the fastest-growing end-user group as advanced steel and lightweight alloy manufacturing intensified demand for high-purity graphite electrode solutions. Metal Processing Industry facilities are also increasing adoption of oxidation-resistant electrodes for precision smelting and specialty alloy production. Meanwhile, the Energy Sector and Chemical Industry are creating niche demand for graphitized carbon materials in thermal processing applications. Companies are strengthening competitive positioning through application-specific engineering, predictive maintenance integration, and flexible pricing agreements tailored to industrial consumption intensity and operational reliability requirements.

Asia-Pacific accounted for the largest market share at 54% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 4.8% between 2026 and 2033.

Electric Arc Furnace Modernization Accelerating Domestic Demand

North America maintained a strong position in the graphite electrode market due to high electric arc furnace penetration and expanding recycled steel production capacity. The United States contributed more than 72% of regional graphite electrode consumption in 2026, supported by infrastructure modernization and automotive-grade steel demand. Steelmakers increased deployment of ultra-high-power electrodes to improve furnace productivity and reduce energy intensity during continuous melting operations. Automated electrode regulation systems improved process stability by nearly 9% across large-scale steel facilities. Companies are strengthening regional supply resilience through long-term procurement agreements, localized warehousing, and operational partnerships linked to low-emission steel manufacturing.

United States Market Outlook: The United States remains the region’s most strategically significant market due to its large secondary steel industry, advanced electric arc furnace network, and industrial reshoring activity. More than 70% of domestic steel production capacity is connected to electric arc furnace operations, increasing demand for premium graphite electrode grades. Producers are investing in AI-enabled furnace monitoring and integrated raw material sourcing to improve operational efficiency and reduce supply volatility across infrastructure and automotive steel manufacturing.

Decarbonized Steel Production Reshaping Electrode Procurement

Europe is strengthening graphite electrode demand through industrial decarbonization initiatives and recycled steel expansion strategies. Germany, Italy, and Turkey collectively represented over 58% of regional graphite electrode utilization in 2026 due to concentrated electric arc furnace steel production and specialty alloy manufacturing. Carbon-emission compliance measures accelerated adoption of ultra-high-power electrodes with improved thermal conductivity and lower consumption intensity. European manufacturers increased investment in energy-efficient graphitization systems and automated quality inspection infrastructure, reducing production defects by approximately 8%. Companies are restructuring procurement through localized sourcing partnerships and long-duration supply contracts to stabilize operations amid energy market volatility.

Germany Market Outlook: Germany remains the region’s operational leader due to its advanced specialty steel sector, precision manufacturing ecosystem, and industrial automation capabilities. Steel producers are integrating digitally controlled furnace systems and premium graphite electrode technologies to support low-emission manufacturing targets. In 2026, several German steel facilities upgraded thermal processing infrastructure, improving furnace energy efficiency by nearly 10% across automotive and engineered steel production lines.

Manufacturing Scale and Export Strength Dominating Production

Asia-Pacific leads the global graphite electrode market through integrated manufacturing capacity, large-scale steel production, and strong raw material accessibility. China, India, and Japan accounted for more than 67% of global graphite electrode production output in 2026, supported by vertically integrated needle coke processing and expanding electric arc furnace infrastructure. China continues dominating export-oriented supply chains, while India is rapidly scaling domestic production through industrial corridor investments and secondary steel expansion. Regional manufacturers increased automation deployment across graphitization and machining operations by nearly 15%, improving production consistency and export competitiveness. Companies are strengthening strategic partnerships with steel producers to secure long-term supply stability during fluctuating raw material cycles.

China Market Outlook: China remains the largest operational hub for graphite electrode manufacturing due to its integrated steel ecosystem, large graphitization infrastructure base, and extensive needle coke processing capabilities. The country accounted for more than half of global ultra-high-power graphite electrode production capacity in 2026. Chinese manufacturers are expanding high-density electrode lines, increasing automated machining adoption, and strengthening export logistics networks to maintain supply leadership across global steelmaking and specialty alloy production industries.

Infrastructure Steel Demand Supporting Industrial Expansion

South America is experiencing steady graphite electrode demand growth through infrastructure-linked steel production and mining sector expansion. Brazil contributed nearly 48% of regional graphite electrode utilization in 2026 due to its established electric arc furnace steel industry and industrial metal processing activity. Regional steel producers are increasingly adopting higher-grade electrodes to improve melting efficiency and reduce operational downtime in continuous casting applications. However, energy cost fluctuations and limited domestic needle coke processing infrastructure continue constraining production scalability. Companies are responding through import diversification, localized storage expansion, and operational partnerships supporting construction-grade and industrial steel manufacturing.

Brazil Market Outlook: Brazil remains the region’s strongest market due to its integrated steel production capacity, industrial mining activity, and expanding infrastructure development projects. Domestic steelmakers are modernizing electric arc furnace operations and increasing adoption of premium graphite electrodes to improve productivity during high-volume steel processing cycles. In 2026, multiple industrial facilities expanded furnace automation systems to reduce electrode consumption variability and strengthen production reliability across construction and heavy-equipment steel applications.

Industrial Diversification and Steel Investments Accelerating Adoption

Middle East & Africa is emerging as a high-priority graphite electrode market due to industrial diversification programs, expanding steel infrastructure, and rising investment in low-emission manufacturing assets. Gulf countries increased electric arc furnace-linked steelmaking capacity by approximately 13% during 2026, strengthening demand for ultra-high-power graphite electrodes across construction and industrial projects. Saudi Arabia and the UAE are leading modernization efforts through integrated steel complexes and automated furnace deployment initiatives. Regional manufacturers and steel operators are forming long-term supply partnerships to improve procurement stability and reduce import dependency. Infrastructure limitations and limited localized raw material processing still affect scalability, although industrial policy support is accelerating investment momentum.

Saudi Arabia Market Outlook: Saudi Arabia is becoming the region’s most strategically important market due to large-scale industrial diversification initiatives, expanding steel infrastructure, and advanced manufacturing investments linked to national development programs. Electric arc furnace steel production capacity increased significantly across industrial clusters supporting construction, energy, and transportation sectors. Producers are prioritizing premium graphite electrode procurement, furnace automation integration, and long-term raw material agreements to strengthen operational continuity and improve production efficiency across modernized steel manufacturing facilities.

The graphite electrode market is dominated by integrated global manufacturers including GrafTech International, Showa Denko, Fangda Carbon, HEG Limited, Tokai Carbon, and Graphite India, competing aggressively against regional low-cost suppliers and specialty carbon producers. The top five players collectively control nearly 47% of global supply capacity, with competition centered on ultra-high-power electrode performance, captive needle coke integration, delivery reliability, and furnace optimization support. Premium electrode producers achieved approximately 8% lower consumption rates and 10% higher operational stability in advanced electric arc furnace applications compared with standard-grade suppliers. Companies are strengthening market positions through vertical integration, automated graphitization infrastructure, export expansion, and long-term steel producer partnerships. A major competitive shift involves raw material control, as needle coke access increasingly determines pricing power and supply resilience. High energy intensity, advanced machining requirements, and qualification timelines remain critical entry barriers. Winning requires integrated supply security, technical consistency, and operational alignment with low-emission steel production systems.

GrafTech International

Fangda Carbon New Material Co., Ltd.

HEG Limited

Graphite India Limited

Tokai Carbon Co., Ltd.

Resonac Holdings Corporation

Nippon Carbon Co., Ltd.

SEC Carbon Limited

Kaifeng Carbon Co., Ltd.

Dan Carbon Co., Ltd.

Yangzi Carbon Co., Ltd.

Showa Denko Materials Co., Ltd.

Jilin Carbon Co., Ltd.

Nantong Yangzi Carbon Co., Ltd.

Graphite electrode manufacturing in 2026 is increasingly centered on ultra-high-power electrode engineering, AI-enabled furnace analytics, and automated graphitization systems. More than 44% of large electric arc furnace facilities now use digital electrode monitoring platforms to reduce thermal instability and optimize consumption cycles. Advanced graphitization technologies improved conductivity efficiency by approximately 11% while lowering defect rates by 8% compared with conventional batch-processing systems. Manufacturers in China and Japan are integrating automated machining and density inspection systems to improve export-grade consistency and reduce production variability across high-volume steelmaking operations.

Emerging technologies between 2026 and 2028 include oxidation-resistant coatings, predictive thermal balancing software, and high-density synthetic graphite formulations designed for continuous casting environments. New-generation ultra-high-power electrodes deliver nearly 13% longer operating cycles than traditional furnace-grade products while reducing interruption frequency during high-temperature melting operations. Steel producers benefit through lower maintenance downtime and higher furnace throughput, strengthening operational competitiveness in infrastructure and automotive steel manufacturing.

Disruptive integration trends are shifting toward vertically integrated needle coke sourcing and AI-driven production control systems. Companies investing early in automated graphitization and premium raw material integration are securing stronger pricing resilience, operational stability, and long-term supply advantages across advanced electric arc furnace ecosystems.

February 2026 – GrafTech International reported 6% annual sales volume growth reaching 109.2 thousand metric tons while strengthening U.S.-focused supply allocation strategies amid global pricing pressure. The move reinforced regional supply resilience and improved operational positioning in electric arc furnace steelmaking markets. Source: graftech.com

July 2025 – GrafTech International accelerated cost optimization and production balancing initiatives, targeting approximately 10% year-over-year sales volume expansion while maintaining integrated needle coke sourcing advantages. The strategy improved manufacturing flexibility and strengthened competitiveness during prolonged graphite electrode pricing volatility.

May 2025 – GrafTech International reduced first-quarter cash production costs per metric ton by 21% year-over-year through operational efficiency measures and production optimization programs. The improvement enhanced margin stability and reinforced the company’s ability to support large-scale electric arc furnace steelmakers during uncertain trade conditions.

October 2025 – GrafTech International operated at 63% production capacity utilization during planned European maintenance cycles while increasing quarterly graphite electrode sales volume by 9% year-over-year. The operational balancing strategy improved inventory discipline and strengthened supply continuity across key industrial steel manufacturing customers.

The report provides detailed analysis of the graphite electrode market across Ultra High Power, High Power, Regular Power, Natural Graphite, and Synthetic Graphite segments, with operational assessment across electric arc furnaces, steel production, foundries, non-ferrous metal processing, and smelting applications. It evaluates adoption trends across the steel industry, automotive manufacturing, energy sector, chemical processing, and industrial metal operations. More than 60% of current market deployment remains concentrated in electric arc furnace-linked steelmaking infrastructure, while premium ultra-high-power electrode utilization continues expanding in automated continuous casting facilities.

The study delivers regional intelligence across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, covering manufacturing concentration, export positioning, infrastructure investments, and raw material integration strategies between 2026 and 2033. The report also analyzes AI-enabled furnace monitoring, oxidation-resistant electrode technologies, graphitization automation, and vertically integrated needle coke sourcing trends. Strategic insights support procurement planning, expansion prioritization, supplier benchmarking, operational optimization, and long-term competitive positioning across evolving low-emission steel production ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 6228 Million |

|

Market Revenue in 2033 |

USD 8264.69 Million |

|

CAGR (2026 - 2033) |

3.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

GrafTech International, Fangda Carbon New Material Co., Ltd., HEG Limited, Graphite India Limited, Tokai Carbon Co., Ltd., Resonac Holdings Corporation, Nippon Carbon Co., Ltd., SEC Carbon Limited, Kaifeng Carbon Co., Ltd., Dan Carbon Co., Ltd., Yangzi Carbon Co., Ltd., Showa Denko Materials Co., Ltd., Jilin Carbon Co., Ltd., Nantong Yangzi Carbon Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |