Reports

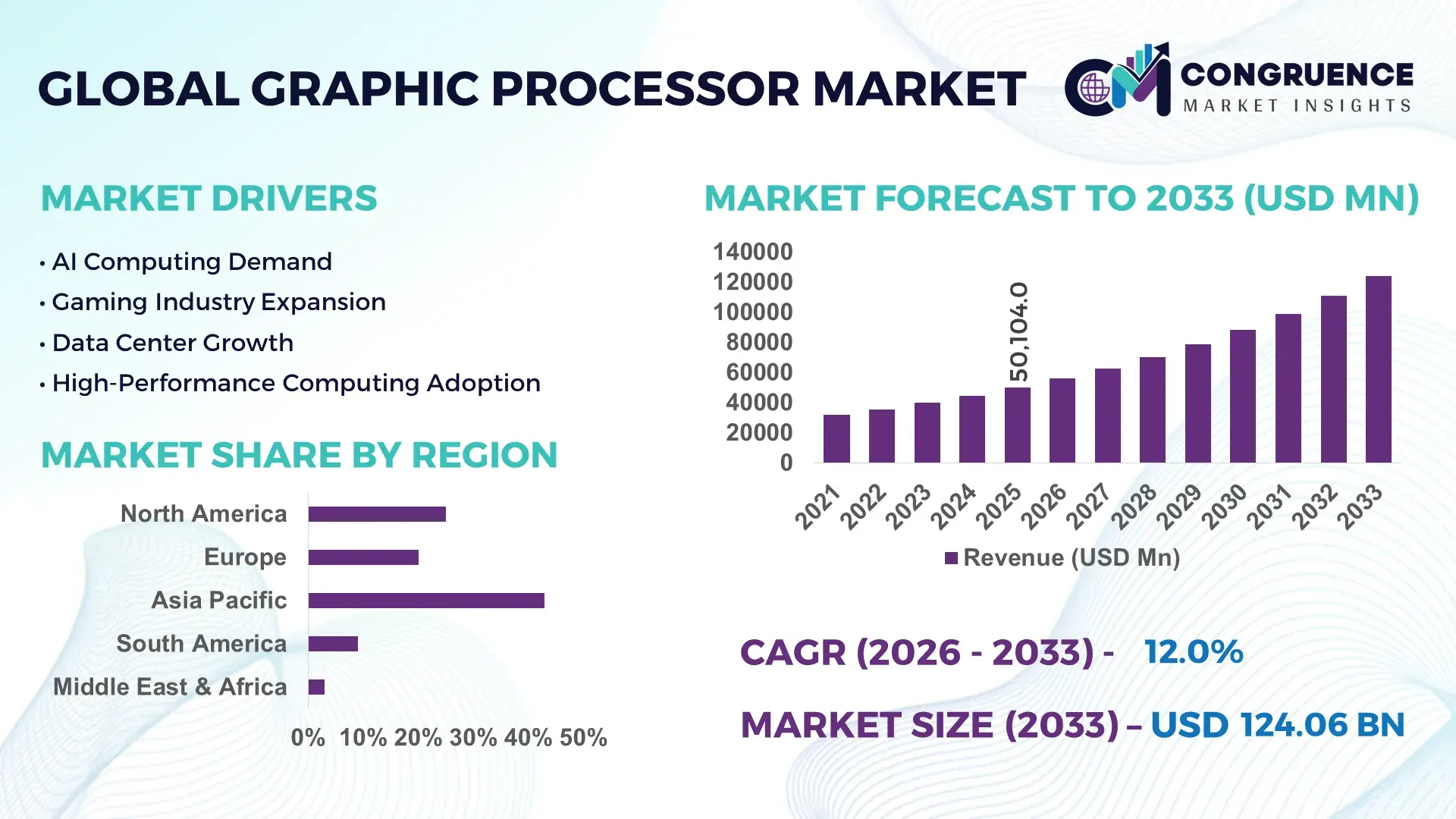

The Global Graphic Processor Market was valued at USD 50104 Million in 2025 and is anticipated to reach a value of USD 124055.65 Million by 2033 expanding at a CAGR of 12% between 2026 and 2033. Rising AI workstation deployments, advanced gaming ecosystems, sovereign semiconductor investments, and accelerated GPU integration across automotive simulation, cloud rendering, and industrial digital twins are driving high-performance graphic processor adoption globally in 2026.

China maintains the dominant position in the global graphic processor market with nearly 32% manufacturing-linked supply participation and aggressive semiconductor localization investments exceeding USD 40 billion across advanced packaging and AI accelerator infrastructure. The United States leads in premium GPU architecture innovation, hyperscale AI server deployment, and enterprise visualization software adoption, controlling over 45% of high-end AI graphic processing demand across cloud and defense-linked computing environments. Taiwan continues to anchor advanced chip fabrication capacity with sub-5nm production leadership supporting next-generation graphic processors, while South Korea strengthens memory integration efficiency for high-bandwidth GPU applications. Export-control tensions between the United States and China accelerated regional supply-chain diversification by over 18% during 2025–2026, pushing manufacturers toward India, Vietnam, and Malaysia for assembly expansion and logistics resilience. Automotive design simulation, generative AI model training, and edge-based industrial analytics remain the fastest-growing deployment sectors globally.

Strategic competition now centers on securing advanced fabrication access, AI compute scalability, and regional supply-chain resilience to sustain long-term graphic processor market leadership.

Market Size & Growth: USD 50104 Million in 2025 reaching USD 124055.65 Million by 2033 at 12% growth, supported by AI infrastructure expansion and high-performance computing demand.

Top Growth Drivers: AI server deployment surged 38%, cloud gaming traffic increased 27%, and automotive visualization workloads expanded 22% globally.

Short-Term Forecast: By 2027, advanced GPU clusters improve rendering efficiency by 35% while reducing enterprise processing latency by 28%.

Emerging Technologies: AI-integrated GPUs, chiplet architectures, and high-bandwidth memory solutions improved processing throughput by over 40% in advanced workloads.

Regional Leaders: North America exceeds USD 41 billion through hyperscale AI adoption, Asia-Pacific crosses USD 48 billion through semiconductor manufacturing strength, and Europe surpasses USD 18 billion via automotive simulation investments.

Consumer/End-User Trends: Over 64% of enterprise AI workloads now rely on GPU acceleration, while premium gaming GPU upgrades increased 31% globally.

Pilot/Case Example: In 2026, an industrial digital twin deployment reduced simulation processing time by 42% using AI-optimized graphic processors.

Competitive Landscape: One leading GPU vendor controls nearly 70% of AI accelerator shipments, alongside strong competition from AMD, Intel, Qualcomm, and emerging regional chipmakers.

Regulatory & ESG Impact: Energy-efficient GPU architectures lowered data-center power consumption by 19% amid stricter global sustainability compliance standards.

Investment & Funding: Semiconductor and AI infrastructure investments exceeded USD 95 billion globally, driven by sovereign manufacturing incentives and strategic partnerships.

Innovation & Future Outlook: Advanced edge AI graphics, photonic interconnects, and sovereign chip ecosystems are reshaping long-term competitive positioning amid ongoing supply-chain regionalization.

Graphic processor demand remains concentrated in AI data centers, immersive gaming platforms, automotive simulation, and industrial visualization systems. Advanced chiplet GPU designs improved computational efficiency by 30% while reducing thermal load across enterprise deployments. Supply-chain regionalization and export-control policies are accelerating localized semiconductor manufacturing strategies, positioning AI-optimized graphic processors as a core infrastructure priority entering the next phase of strategic market competition.

Graphic processors have become a strategic infrastructure asset across AI computing, autonomous systems, defense simulation, cloud rendering, and industrial digitalization. Enterprises are prioritizing GPU-centric architectures to secure competitive advantages in automation speed, real-time analytics, and high-density computing performance. In 2026, export-control restrictions and semiconductor supply-chain restructuring accelerated localized chip manufacturing investments across India, Vietnam, and the United States, while hyperscale operators increased GPU server deployments by over 34% to support generative AI and advanced workload orchestration.

AI-optimized graphic processors now deliver nearly 45% lower processing latency and 30% higher energy efficiency compared with legacy accelerator configurations in enterprise-scale training environments. The United States leads in advanced GPU software ecosystems and AI infrastructure deployment, while China maintains stronger scale advantages in hardware assembly and electronics manufacturing integration. Japan and South Korea are strengthening high-bandwidth memory capabilities to improve rendering throughput and thermal optimization for industrial and automotive applications. Over the next three years, enterprise edge-AI GPU deployments are projected to expand by more than 28% as factories modernize real-time operational analytics.

Automotive manufacturers, cloud service providers, and semiconductor firms are expanding strategic partnerships to secure advanced packaging, AI accelerator access, and localized production resilience. Companies deploying liquid-cooled GPU clusters reduced data-center power utilization by nearly 18% in large-scale AI operations. Competitive positioning increasingly depends on GPU supply security, software optimization capability, and scalable compute infrastructure supporting long-term digital transformation priorities.

Rapid enterprise AI deployment and accelerated computing modernization continue to reshape graphic processor demand across cloud infrastructure, industrial automation, and autonomous mobility systems. Hyperscale data-center operators increased GPU cluster investments by over 36% during 2025–2026, while AI-driven enterprise workloads expanded nearly 41% across manufacturing, financial analytics, and healthcare imaging applications. The United States and Taiwan strengthened advanced semiconductor packaging capacity to reduce lead-time pressure caused by export restrictions and AI server demand concentration. Automotive companies integrating AI-enabled simulation platforms reported approximately 27% faster design validation cycles using advanced graphic processors. In response, chipmakers are expanding high-bandwidth memory partnerships, localized assembly operations, and AI accelerator ecosystems to secure long-term enterprise contracts. The market increasingly rewards vendors capable of combining compute density, thermal efficiency, and scalable software optimization within integrated AI infrastructure environments.

The graphic processor market continues to face structural pressure from concentrated semiconductor fabrication dependency and advanced packaging bottlenecks. More than 70% of high-end GPU fabrication remains linked to limited sub-5nm foundry capacity, exposing manufacturers to procurement delays and pricing instability. During 2026, advanced memory component costs increased nearly 18% due to AI server demand surges and constrained supply availability across South Korea and Taiwan. Export-control regulations affecting high-performance chips also disrupted cross-border deployment consistency for enterprise AI infrastructure projects. These constraints directly impacted hardware scalability, inventory planning, and operating margins for cloud providers and system integrators. In response, companies are diversifying sourcing networks, securing multi-year wafer agreements, and expanding regional assembly operations in India and Southeast Asia. Strategic localization is becoming essential to reduce supply-chain exposure and maintain enterprise delivery reliability under volatile semiconductor market conditions.

Edge-based AI computing and sovereign semiconductor initiatives are creating high-value expansion opportunities for graphic processor manufacturers. Industrial edge deployments using AI-enabled GPUs improved real-time operational analytics efficiency by nearly 33% across logistics hubs, manufacturing facilities, and smart transportation networks. India, Saudi Arabia, and the United Arab Emirates accelerated national AI infrastructure programs in 2026, increasing demand for localized GPU-enabled cloud platforms and advanced data-processing capability. AI-integrated automotive systems and robotics platforms are also driving demand for compact, power-efficient graphic processors with enhanced thermal management. Companies investing in chiplet architecture research achieved approximately 22% lower production costs through modular design flexibility and improved yield efficiency. Semiconductor vendors are expanding regional R&D centers, forming software ecosystem alliances, and developing industry-specific accelerator platforms to capture emerging enterprise workloads beyond traditional gaming and consumer electronics applications.

Long-term market expansion faces growing challenges linked to power density management, integration complexity, and advanced workforce requirements. Large AI training clusters now consume nearly 25% more cooling capacity than conventional enterprise server environments, increasing infrastructure modernization pressure across data centers in the United States, Germany, and Singapore. Integration inconsistency between GPU hardware, AI frameworks, and legacy enterprise systems continues to delay deployment timelines by approximately 20% in industrial-scale environments. Cybersecurity exposure within GPU-accelerated cloud workloads has also intensified as enterprises process larger volumes of real-time operational data. Companies must simultaneously address thermal efficiency, interoperability standards, and software optimization while maintaining deployment scalability. Industry leaders are responding through liquid-cooling innovation, specialized AI engineering partnerships, and vertically integrated hardware-software ecosystems designed to improve long-term operational stability and compute reliability across high-density digital infrastructure environments.

AI-Centric GPU Infrastructure Scaling enterprise AI deployments are reshaping graphic processor procurement priorities as hyperscale operators increased GPU server installations by nearly 39% during 2025–2026. Companies are restructuring procurement contracts around high-bandwidth memory availability and liquid-cooling compatibility to manage power-intensive AI workloads. In the United States, AI-focused data-center rack density increased over 26%, reducing processing latency while improving compute utilization efficiency. Semiconductor vendors are expanding software optimization partnerships and vertically integrated accelerator ecosystems to secure long-term enterprise contracts.

Localized Semiconductor Supply Expansion supply-chain fragmentation and export-control restrictions accelerated regional manufacturing diversification across India, Vietnam, and Malaysia. Advanced GPU assembly capacity outside China expanded approximately 21% in 2026 as enterprises sought logistics resilience and tariff exposure reduction. Japanese and South Korean manufacturers increased advanced packaging automation by nearly 18% to stabilize delivery cycles. Companies are prioritizing localized testing facilities, multi-country sourcing agreements, and modular production workflows to improve operational continuity during semiconductor shortages and geopolitical disruptions.

Energy-Efficient GPU Deployment Models data-center operators are aggressively adopting power-optimized graphic processors as AI training clusters increase electricity consumption intensity. Liquid-cooled GPU infrastructure improved thermal efficiency by approximately 24% while reducing operational cooling costs by nearly 16% across large enterprise environments. European cloud operators accelerated deployment of energy-aware scheduling systems following stricter sustainability reporting requirements. GPU manufacturers are redesigning chip architectures around performance-per-watt metrics, creating competitive advantages in long-duration AI and simulation workloads.

Automotive Simulation Workload Growth automotive OEMs and mobility software firms expanded GPU-driven digital twin and autonomous driving simulation programs by more than 31% in 2026. Real-time rendering integration reduced vehicle prototype testing cycles by nearly 28%, accelerating software validation and safety modeling workflows. German automotive suppliers increasingly shifted from CPU-based simulation systems toward AI-enabled graphic processors for sensor fusion testing. Hardware vendors are responding through automotive-grade GPU platforms, embedded AI accelerator partnerships, and dedicated software stacks supporting autonomous mobility infrastructure.

Data Center GPU remains the dominant segment due to large-scale AI model training, cloud acceleration demand, and enterprise compute consolidation requirements. More than 46% of advanced GPU deployments in 2026 were linked to hyperscale and enterprise AI infrastructure, supported by increasing rack-density optimization and GPU virtualization adoption. Data Center GPUs deliver superior parallel processing capability and workload scalability compared with conventional compute architectures, making them essential for generative AI, industrial simulation, and cloud orchestration environments. Mobile GPU is emerging as the fastest-growing segment as AI-enabled smartphones, handheld gaming devices, and edge-computing systems accelerate demand for power-efficient graphics processing solutions. Integrated GPU continues maintaining relevance in cost-sensitive enterprise laptops and consumer systems due to lower thermal requirements and integrated efficiency advantages, while Discrete GPU demand remains concentrated in premium gaming, engineering visualization, and creator workflows. Manufacturers are increasing investments in chiplet architectures, memory bandwidth optimization, and software ecosystems to strengthen workload specialization and deployment flexibility across segments. Enterprise buyers are increasingly prioritizing performance-per-watt efficiency and scalable deployment compatibility over standalone hardware capability.

Gaming continues to represent the leading application segment due to its massive installed user base, premium hardware upgrade cycles, and sustained demand for high-frame-rate rendering environments. Nearly 58% of discrete GPU shipments in 2026 remained linked to gaming-oriented systems, particularly across China, South Korea, and the United States. However, AI & Machine Learning is the fastest-growing application segment as enterprises expand generative AI deployment, predictive analytics, and industrial automation infrastructure. AI-focused GPU utilization increased over 42% across enterprise data centers during 2025–2026, driven by large language model training and real-time inference processing. Cloud Computing is also strengthening operational relevance through GPU-as-a-service deployment models supporting scalable compute access, while Professional Visualization demand continues expanding in architecture, defense simulation, and digital twin applications. Automotive Systems are becoming strategically important as autonomous driving validation and sensor-processing workloads intensify. GPU vendors are expanding AI software frameworks, cloud optimization partnerships, and industry-specific accelerator platforms to capture evolving deployment patterns beyond traditional graphics-intensive applications.

IT & Telecom remains the dominant end-user segment due to hyperscale data-center expansion, cloud orchestration requirements, and enterprise AI infrastructure modernization. Nearly 49% of enterprise-grade graphic processor deployments in 2026 were concentrated within cloud computing, telecom edge infrastructure, and AI-enabled networking environments. Companies are scaling GPU-intensive compute clusters to support generative AI, cybersecurity analytics, and real-time data-processing operations. Automotive represents the fastest-growing end-user segment as autonomous mobility systems, digital twin simulation, and advanced driver-assistance platforms expand rapidly across Germany, Japan, and the United States. Consumer Electronics continues generating stable demand through gaming systems, AI-enabled smartphones, and creator-focused devices, while Media & Entertainment is accelerating GPU adoption for virtual production, high-resolution rendering, and immersive content workflows. Healthcare adoption is strengthening through AI-assisted diagnostics and medical imaging acceleration. Vendors are responding through sector-specific GPU customization, cloud-based deployment partnerships, and pricing models optimized for enterprise-scale compute utilization. Competitive differentiation increasingly depends on software integration capability, workload optimization, and energy-efficient deployment architecture.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2026 and 2033.

AI Infrastructure and Enterprise GPU Consolidation

North America remains the most advanced deployment hub for high-performance graphic processors due to hyperscale AI infrastructure, cloud orchestration demand, and enterprise compute modernization. The region represented nearly 31% of global GPU-intensive AI deployments in 2025, supported by aggressive expansion of liquid-cooled data centers and AI-native cloud environments. Large technology firms increased GPU cluster density by over 28% to support generative AI processing, cybersecurity analytics, and industrial simulation workloads. Semiconductor partnerships between cloud operators and chip manufacturers accelerated localized packaging and advanced memory integration initiatives across the United States and Canada. Enterprise demand increasingly prioritizes software ecosystem compatibility, thermal optimization, and low-latency processing efficiency for scalable AI operations.

United States Market Outlook: The United States dominates the North American graphic processor market through advanced AI infrastructure, semiconductor design leadership, and enterprise-scale cloud deployment capability. More than 65% of the region’s AI accelerator installations were concentrated in U.S.-based hyperscale facilities during 2026. Federal semiconductor manufacturing incentives strengthened localized chip packaging and advanced fabrication investments, while defense, healthcare, and automotive industries accelerated GPU deployment for simulation and real-time analytics applications. Major enterprises are prioritizing vertically integrated hardware-software ecosystems to secure compute scalability and operational resilience.

Sustainable Compute Modernization Accelerating Adoption

Europe is strengthening its graphic processor ecosystem through energy-efficient compute infrastructure, automotive simulation demand, and industrial AI modernization programs. The region accounted for approximately 22% of enterprise GPU-enabled industrial deployments in 2025, particularly across Germany, France, and the Netherlands. Data-center operators expanded liquid-cooling adoption by nearly 19% to align with stricter sustainability and energy-efficiency regulations. Automotive manufacturers increasingly integrated GPU-based digital twins and AI-assisted engineering workflows to improve product validation efficiency and reduce testing cycles. Semiconductor and cloud infrastructure collaborations are also increasing across the European Union to reduce dependence on external advanced computing supply chains and improve sovereign digital infrastructure capability.

Germany Market Outlook: Germany leads the European graphic processor market through advanced automotive engineering, industrial automation strength, and AI-driven manufacturing infrastructure. Industrial enterprises expanded GPU-enabled simulation deployments by approximately 26% during 2025–2026 to support robotics, factory optimization, and autonomous mobility development. German automotive OEMs are accelerating partnerships with semiconductor firms and AI software providers to strengthen digital twin integration and sensor-processing capability. The country’s emphasis on sustainable industrial modernization is also driving adoption of energy-efficient GPU architectures across enterprise and research computing facilities.

Manufacturing Scale and Electronics Integration Leadership

Asia-Pacific remains the largest graphic processor production and deployment hub due to semiconductor manufacturing concentration, electronics assembly strength, and large-scale gaming and AI adoption. The region contributed nearly 43% of global GPU manufacturing activity in 2025, with Taiwan, China, South Korea, and Japan anchoring advanced chip fabrication and memory integration ecosystems. AI-enabled electronics production and gaming hardware demand increased over 32% across major industrial clusters during 2025–2026. Export-control disruptions accelerated manufacturing diversification into India, Vietnam, and Malaysia, improving supply-chain flexibility and assembly resilience. Regional enterprises are increasingly investing in advanced packaging, AI accelerators, and localized semiconductor ecosystems to secure long-term competitiveness in high-density compute infrastructure markets.

China Market Outlook: China maintains a strategically dominant position through large-scale electronics manufacturing, AI infrastructure expansion, and domestic semiconductor ecosystem development. More than 48% of regional gaming GPU shipments were linked to Chinese consumer and enterprise markets in 2026. Domestic firms are increasing investments in AI accelerators, localized fabrication capability, and sovereign cloud infrastructure following tightening international semiconductor restrictions. Industrial AI deployment across manufacturing, logistics, and smart-city platforms continues expanding rapidly, strengthening long-term demand for scalable and cost-optimized graphic processor technologies.

Cloud Expansion and Gaming Demand Momentum

South America is witnessing increasing graphic processor adoption through cloud modernization, gaming ecosystem expansion, and enterprise digital transformation initiatives. The region represented nearly 7% of emerging-market GPU deployment activity in 2025, with Brazil and Argentina driving most enterprise infrastructure investments. Cloud operators expanded GPU-enabled processing capacity by approximately 18% to support financial analytics, e-commerce scaling, and AI-assisted enterprise applications. However, infrastructure limitations, semiconductor import dependency, and power-cost volatility continue affecting deployment consistency and procurement timelines. Companies are responding through regional data-center partnerships, localized distribution agreements, and cloud-based GPU access models designed to reduce upfront infrastructure costs and improve compute accessibility for mid-sized enterprises.

Brazil Market Outlook: Brazil leads the South American graphic processor market through expanding cloud infrastructure, strong gaming demand, and enterprise digitalization programs. Enterprise GPU deployment within financial services and telecommunications increased nearly 21% during 2025–2026 as organizations modernized analytics and cybersecurity operations. Domestic cloud operators are increasing partnerships with international semiconductor and AI platform providers to strengthen compute availability and reduce latency constraints. Growth in esports, content creation, and AI-assisted retail analytics is also supporting broader adoption of advanced graphic processing technologies across commercial sectors.

AI Infrastructure Investment Reshaping Demand

The Middle East & Africa graphic processor market is evolving through sovereign AI infrastructure investments, smart-city modernization, and cloud computing expansion. The region accounted for approximately 5% of global enterprise AI infrastructure deployment activity in 2025, with Gulf countries leading advanced compute investments. Data-center operators in the United Arab Emirates and Saudi Arabia increased GPU-enabled AI processing capacity by over 24% to support smart mobility, energy optimization, and digital government platforms. Industrial diversification programs are accelerating enterprise demand for high-performance computing infrastructure across logistics, healthcare, and financial services sectors. Companies are strengthening regional partnerships and edge-computing ecosystems to improve operational scalability and localized AI processing capability.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the most strategically significant market within the region due to aggressive AI infrastructure expansion and national digital transformation initiatives. Government-backed smart-city and industrial modernization programs accelerated GPU-intensive cloud deployment by approximately 27% during 2026. Enterprises across energy, logistics, and public-sector operations are integrating AI-enabled analytics platforms requiring scalable graphic processor capability. Strategic investments in hyperscale facilities, sovereign cloud infrastructure, and advanced connectivity networks are positioning the country as a regional hub for AI-driven compute and digital industrialization.

NVIDIA, AMD, Intel, Qualcomm, and Apple dominate the graphic processor market, competing across AI accelerators, gaming GPUs, mobile graphics, and integrated compute platforms. Global leaders are challenging regional semiconductor firms focused on cost-optimized AI chips and localized supply resilience, while OEM-integrated developers compete against discrete GPU specialists through vertically optimized ecosystems. The top five players collectively control nearly 78% of high-performance GPU shipments. Competition increasingly centers on memory bandwidth, AI processing efficiency, software compatibility, and supply-chain control rather than raw hardware pricing alone. AI-focused GPU architectures improved enterprise workload efficiency by over 40%, while advanced liquid-cooling integration reduced operating costs by nearly 18% in hyperscale deployments. Companies are expanding fabrication partnerships, securing long-term wafer agreements, and integrating proprietary AI software stacks to strengthen deployment lock-in. Export restrictions and advanced packaging shortages intensified competitive pressure. Winning requires scalable manufacturing access, AI software optimization capability, and resilient infrastructure partnerships across global enterprise ecosystems.

NVIDIA Corporation

Advanced Micro Devices (AMD)

Intel Corporation

Qualcomm Technologies

Apple Inc.

Samsung Electronics

Imagination Technologies

Arm Holdings

MediaTek Inc.

Broadcom Inc.

IBM Corporation

Huawei Technologies

ASUSTeK Computer Inc.

Micro-Star International (MSI)

Advanced AI-centric GPU architectures are redefining compute efficiency across hyperscale data centers, automotive simulation, and industrial analytics environments. Fifth-generation tensor cores and high-bandwidth memory integration improved AI training throughput by nearly 42% while reducing inference latency by approximately 30% compared with previous accelerator generations. More than 58% of enterprise AI workloads in 2026 now operate on GPU-accelerated infrastructure, driven by cloud-native orchestration and large language model deployment. Companies integrating liquid-cooled GPU clusters reduced power-management overhead by nearly 18%, strengthening operational scalability for high-density compute environments.

Emerging technologies such as chiplet-based GPU designs, unified memory architectures, and photonic interconnects are accelerating deployment flexibility and reducing manufacturing complexity. Unified memory GPU platforms lowered data-transfer overhead by nearly 25% compared with conventional discrete accelerator environments, improving engineering simulation and real-time analytics performance. Semiconductor firms across the United States, Taiwan, and South Korea are increasing advanced packaging partnerships to stabilize supply-chain efficiency and accelerate AI server deployment cycles. Automotive and industrial robotics companies are also integrating edge-AI graphic processors to improve autonomous decision-making capability and low-latency processing efficiency.

Between 2026 and 2028, disruptive GPU technologies including AI-native orchestration engines, optical networking integration, and energy-aware compute scheduling will intensify competitive differentiation. Enterprises deploying software-optimized AI accelerators are achieving nearly 35% faster workload scaling than legacy CPU-dependent infrastructure. Cloud providers, automotive OEMs, and industrial automation leaders benefit most from early adoption due to stronger compute utilization, lower operational bottlenecks, and improved deployment resilience under expanding AI infrastructure demand.

March 2024 – NVIDIA launched the Blackwell GPU platform featuring next-generation tensor cores and NVLink integration, reducing LLM inference cost and energy consumption by up to 25x compared with earlier architectures. The rollout strengthened hyperscale AI infrastructure competitiveness and accelerated enterprise GPU modernization globally. Source: nvidianews.nvidia.com

November 2024 – AMD powered the El Capitan supercomputer using Instinct MI300A accelerators, achieving 1.742 exaflops and securing the top position on the Top500 list. The deployment strengthened AMD’s high-performance computing credibility and expanded competitive pressure within enterprise AI and scientific computing environments. Source: ir.amd.com

October 2024 – NVIDIA resolved a production-related Blackwell chip design flaw with manufacturing partner TSMC after yield constraints delayed shipments to hyperscale cloud customers. The correction stabilized supply continuity for advanced AI infrastructure deployments and reduced enterprise concerns around next-generation GPU delivery consistency. Source: reuters.com

May 2026 – OpenAI and NVIDIA deployed GPT-5.5 Codex across Blackwell GB200 NVL72 systems for over 10,000 employees, delivering 50x higher token efficiency per megawatt and reducing inference costs by 35x. The deployment validated enterprise-scale AI agent viability and accelerated GPU-driven workflow automation adoption. Source: techradar.com

The Graphic Processor Market report delivers comprehensive analysis across Integrated GPU, Discrete GPU, Mobile GPU, and Data Center GPU segments, covering deployment trends across gaming, AI & machine learning, cloud computing, automotive systems, and professional visualization environments. The study evaluates operational adoption patterns across Consumer Electronics, Automotive, IT & Telecom, Healthcare, and Media & Entertainment sectors, where enterprise GPU acceleration usage surpassed 55% within AI-driven infrastructure environments during 2026. Regional coverage includes North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with focused assessment of semiconductor manufacturing hubs, hyperscale infrastructure clusters, and emerging sovereign AI ecosystems.

The report examines advanced technologies including chiplet architectures, high-bandwidth memory integration, liquid-cooled GPU systems, and AI-native accelerator platforms shaping competitive differentiation between 2026 and 2033. It provides strategic insight into supply-chain restructuring, enterprise compute modernization, cloud deployment expansion, and edge-AI integration trends. Business stakeholders can leverage the analysis for infrastructure investment planning, regional expansion prioritization, technology benchmarking, partnership evaluation, and long-term competitive positioning within evolving high-performance computing ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 50104 Million |

|

Market Revenue in 2033 |

USD 124055.65 Million |

|

CAGR (2026 - 2033) |

12% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

NVIDIA Corporation, Advanced Micro Devices (AMD), Intel Corporation, Qualcomm Technologies, Apple Inc., Samsung Electronics, Imagination Technologies, Arm Holdings, MediaTek Inc., Broadcom Inc., IBM Corporation, Huawei Technologies, ASUSTeK Computer Inc., Micro-Star International (MSI) |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |