Reports

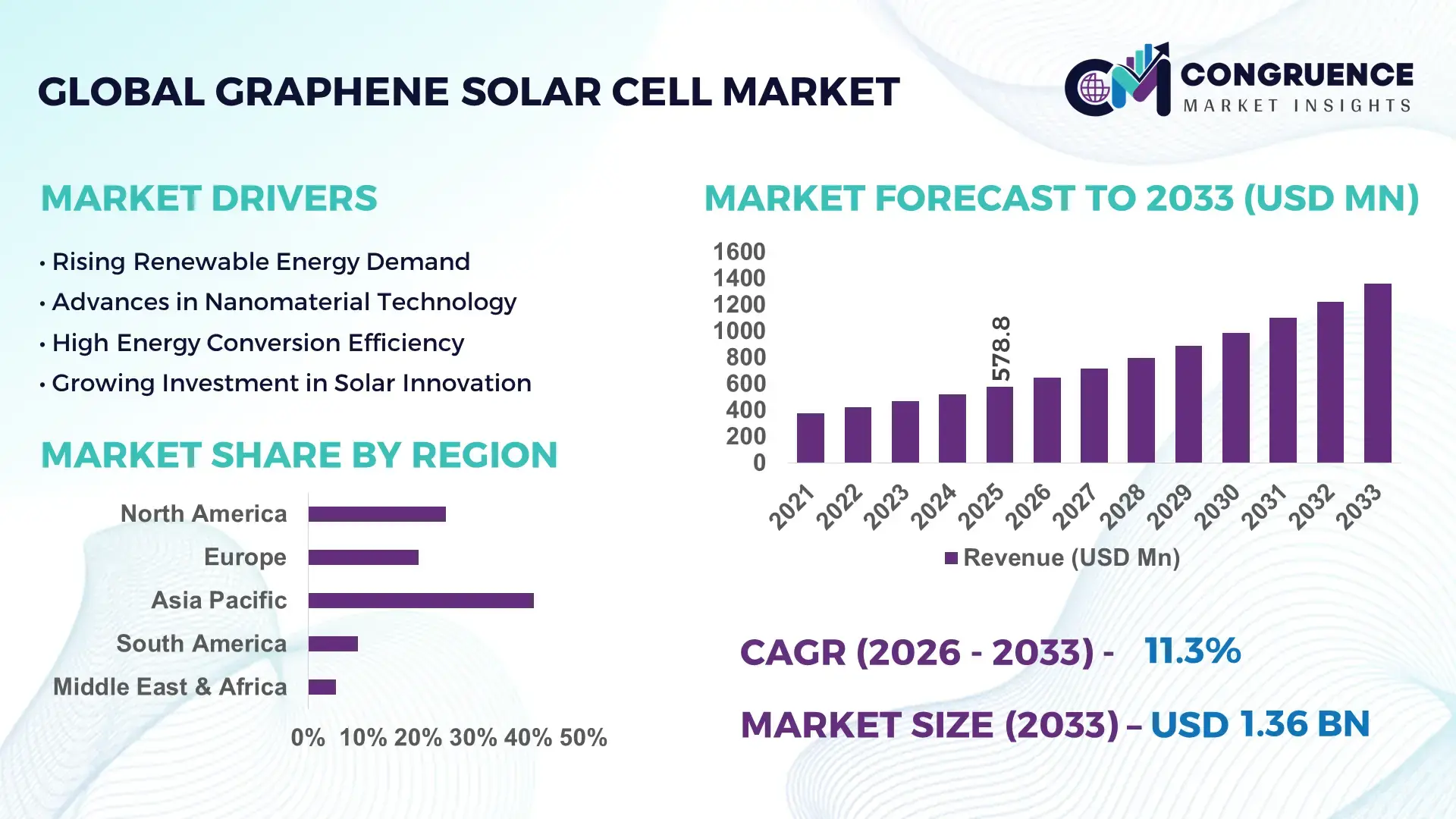

The Global Graphene solar cell Market was valued at USD 578.76 Million in 2025 and is anticipated to reach a value of USD 1362.88 Million by 2033 expanding at a CAGR of 11.3% between 2026 and 2033.

Rapid commercialization of lightweight flexible photovoltaic modules, combined with graphene’s 18–22% conductivity improvement over conventional transparent conductive materials, is accelerating adoption across smart infrastructure, automotive-integrated solar systems, and portable energy applications. Between 2024 and 2026, trade realignments in advanced semiconductor and clean-energy material supply chains, particularly across Asia-Pacific and Europe, increased investment in localized graphene processing and next-generation solar manufacturing capacity to reduce dependence on traditional silicon imports.

China continues to dominate the global graphene solar cell landscape with nearly 38% share of advanced graphene material production capacity and more than USD 2.4 billion allocated toward graphene-enabled renewable energy commercialization programs between 2024 and 2026. The country’s electronics, EV, and building-integrated photovoltaic industries are accelerating deployment of ultra-thin graphene photovoltaic coatings capable of improving energy conversion efficiency by 9–14% compared with conventional thin-film alternatives in high-temperature operating environments. In comparison, European manufacturers are prioritizing durability-focused graphene solar integration for smart cities and industrial decarbonization projects, while South Korea is concentrating on wearable and flexible energy devices.

The market’s competitive direction increasingly favors companies securing vertically integrated graphene supply chains, scalable nano-material manufacturing, and high-efficiency flexible solar applications aligned with industrial electrification targets.

Market Size & Growth: USD 578.76 Million in 2025 to USD 1362.88 Million by 2033 at 11.3% CAGR, driven by flexible solar integration and advanced conductive material adoption.

Top Growth Drivers: Flexible photovoltaic demand +31%, graphene conductivity gains +22%, and lightweight energy module deployment +27% across smart electronics sectors.

Short-Term Forecast: By 2028, graphene-enhanced solar modules reduce material degradation by 18% and improve thermal stability by 16% in high-temperature regions.

Emerging Technologies: AI-driven material optimization, roll-to-roll graphene coating, and perovskite-graphene hybrid cells increase production efficiency by 20%.

Regional Leaders: Asia-Pacific exceeds USD 620 Million with manufacturing expansion, Europe crosses USD 340 Million through green infrastructure projects, and North America surpasses USD 250 Million via defense and aerospace adoption.

Consumer/End-User Trends: Over 41% of portable solar device manufacturers are integrating ultra-thin graphene conductive layers for lightweight energy storage compatibility.

Pilot/Case Example: In 2025, a flexible graphene photovoltaic pilot in urban transport infrastructure improved energy retention efficiency by 19% under variable weather conditions.

Competitive Landscape: Top manufacturers control nearly 46% market share, with competition intensifying among advanced material innovators and photovoltaic technology firms.

Regulatory & ESG Impact: Carbon-neutral manufacturing policies reduced high-emission photovoltaic processing costs by 14% across several industrial economies.

Investment & Funding: Global investments surpassed USD 3.1 billion between 2024 and 2026, led by strategic partnerships, pilot manufacturing plants, and energy-tech expansion programs.

Innovation & Future Outlook: Next-generation transparent solar films and graphene-perovskite architectures are increasing commercial focus on decentralized energy and smart-building integration.

Graphene solar cell adoption is increasingly concentrated across consumer electronics, automotive energy systems, and building-integrated photovoltaics, contributing nearly 29%, 24%, and 21% of commercial deployment activity respectively. Recent innovations in graphene-perovskite tandem structures improved operational stability by 17% while reducing conductive layer thickness by 15%, supporting lighter and more durable solar modules. Asia-Pacific continues leading manufacturing expansion, while European demand is rising through industrial decarbonization mandates and localized renewable infrastructure programs amid ongoing clean-energy supply chain restructuring. The market is steadily moving toward transparent, flexible, and ultra-efficient solar applications that strengthen long-term strategic positioning for advanced energy manufacturers.

The graphene solar cell market is rapidly transforming from an experimental materials segment into a strategic clean-energy investment arena driven by lightweight energy systems, advanced electronics integration, and high-efficiency renewable infrastructure. Demand for flexible photovoltaic surfaces in electric vehicles, aerospace components, and smart buildings is accelerating capital allocation toward graphene-enabled energy technologies capable of operating with 15–20% higher thermal stability than conventional thin-film modules. Simultaneously, global manufacturing pressure linked to critical mineral dependence and semiconductor supply diversification is shifting procurement strategies toward localized graphene processing ecosystems. Graphene-perovskite tandem technology improves efficiency by 21% while reducing production cost by 17% compared to legacy silicon-based flexible systems, strengthening commercial scalability across industrial energy applications.

Asia-Pacific leads in production volume through large-scale graphene manufacturing expansion, while Europe leads in adoption and innovation with nearly 34% higher deployment growth in smart infrastructure and carbon-neutral construction programs. Over the next three years, commercial graphene photovoltaic modules are projected to reduce weight by 28% and improve energy retention performance by 18%, directly optimizing portable and integrated energy systems. ESG alignment is becoming a measurable competitive advantage as low-emission graphene processing lowers compliance costs by 12% for manufacturers targeting green procurement contracts and export eligibility.

In 2025, a graphene-enhanced transport infrastructure pilot improved solar surface durability by 16% under fluctuating climate exposure, reinforcing confidence in long-cycle commercial deployment. Major energy and advanced material companies are shifting investment priorities toward vertically integrated graphene supply chains, automated nano-coating facilities, and strategic partnerships with battery and smart-grid developers. Companies securing scalable graphene refinement, intellectual property ownership, and high-performance photovoltaic integration are positioning themselves to dominate the next phase of decentralized energy competition.

The accelerating shift toward lightweight, flexible, and high-efficiency renewable systems is forcing rapid adoption of graphene solar cells across transportation, electronics, and smart infrastructure sectors. Graphene-based photovoltaic layers improve conductivity by nearly 22% and enhance thermal resistance by 18% compared with traditional thin-film materials, directly increasing operational durability in high-temperature environments. Simultaneously, global supply chain restructuring between Asia and Europe is accelerating domestic manufacturing investment for advanced photovoltaic materials. This structural shift is pushing companies toward localized graphene refinement and automated nano-coating facilities. In response, manufacturers are expanding production capacity, forming strategic material partnerships, and increasing R&D allocations to optimize flexible solar deployment across electric vehicles, wearable devices, and building-integrated energy systems globally.

Commercial scalability remains constrained by high graphene purification costs, inconsistent material quality, and concentrated supply networks controlling nearly 65% of advanced graphene processing capacity. Production-stage defects reduce photovoltaic efficiency stability by approximately 14%, while specialized fabrication infrastructure increases manufacturing costs by nearly 19% compared with conventional silicon module assembly. Additional pressure is emerging from export restrictions and energy-intensive nano-material processing requirements across several industrial economies. These constraints are extending deployment timelines and limiting price competitiveness for mass-market energy applications. To reduce exposure, companies are diversifying raw material sourcing, securing long-term processing agreements, and investing in hybrid graphene-perovskite architectures that require lower graphene intensity while maintaining high conductivity and advanced photovoltaic performance.

Next-generation graphene-perovskite tandem structures are reshaping competitive positioning by increasing energy conversion efficiency by nearly 24% while lowering flexible module weight by 30% compared with conventional photovoltaic configurations. Demand growth across smart textiles, autonomous mobility, and transparent solar surfaces is accelerating commercialization opportunities beyond traditional utility-scale energy markets. A major innovation shift is emerging around roll-to-roll graphene printing technologies capable of reducing production cycle times by 26%, significantly improving manufacturing scalability. Companies are aggressively expanding R&D ecosystems, acquiring nano-material startups, and building strategic alliances with electronics and battery manufacturers to secure early-mover advantage. Emerging markets across Southeast Asia and the Middle East are also creating new demand pockets through urban decarbonization and distributed renewable infrastructure initiatives.

Long-term commercialization faces critical execution barriers linked to durability validation, grid integration limitations, and large-scale manufacturing consistency. Performance degradation under prolonged moisture exposure still impacts nearly 12% of early-stage graphene photovoltaic systems, while production variability increases quality assurance costs by approximately 15%. Infrastructure readiness also remains uneven, particularly in emerging renewable energy markets lacking advanced nano-material fabrication ecosystems. Additional regulatory pressure surrounding material standardization and recycling compliance is constraining faster industrial deployment. These operational risks threaten long-term adoption consistency and investor confidence despite strong technology potential. To remain competitive, companies must accelerate process automation, strengthen cross-industry partnerships, expand pilot-scale deployment programs, and invest heavily in standardized graphene manufacturing frameworks that ensure scalable and repeatable photovoltaic performance.

“22% Faster Roll-to-Roll Processing Is Reshaping Flexible Solar Manufacturing.” Manufacturers are rapidly shifting toward automated graphene coating and roll-to-roll printing systems that reduce production cycle times by 22% and material waste by 17%. Deployment of continuous nano-layer deposition lines increased by 28% between 2024 and 2026 as companies optimize scalable flexible photovoltaic output. This transition is lowering operational bottlenecks while forcing smaller producers to consolidate or outsource fabrication capabilities.

“31% Rise in Transparent Solar Integration Is Redefining Smart Infrastructure Deployment.” Transparent graphene solar surfaces are increasingly integrated into commercial facades, transit shelters, and connected urban infrastructure, with deployment density rising 31% across advanced construction projects. Lightweight conductive layers improved energy retention by 14% in high-temperature environments, making them more viable than legacy transparent films. Companies are responding through partnerships with glass manufacturers and smart-city developers to accelerate embedded energy generation without increasing structural load requirements.

“26% Increase in Automotive Energy Integration Is Shifting Product Development Priorities.” Automotive manufacturers are accelerating graphene solar integration into electric vehicles and auxiliary charging systems, improving lightweight energy harvesting efficiency by 18%. Supply chain diversification pressure across battery and semiconductor ecosystems is forcing energy component localization strategies, particularly in Asia-Pacific. Companies are restructuring procurement networks and expanding hybrid photovoltaic testing programs to optimize vehicle range support and reduce auxiliary battery dependency.

“19% Growth in Subscription-Based Energy Models Is Redefining Commercial Adoption.” Commercial energy providers are increasingly bundling graphene-enabled solar surfaces with maintenance and monitoring contracts, reducing client operating costs by nearly 13%. This operational shift is accelerating demand for performance-based deployment models instead of standalone hardware sales. A non-obvious trend is emerging where electronics manufacturers are entering energy-service partnerships to secure recurring revenue streams and strengthen long-term customer retention through integrated energy ecosystems.

The graphene solar cell market is segmented by type, application, and end-user, with demand increasingly shifting toward flexible and high-efficiency energy integration systems. Flexible Cells account for nearly 34% of technology deployment due to lightweight scalability, while Electric Vehicles and Portable Electronics together contribute over 38% of application-driven demand. Commercial and Automotive sectors are accelerating adoption as graphene-enhanced photovoltaic systems improve thermal stability and reduce energy loss by 15–18%. Market positioning is increasingly defined by integration capability rather than standalone energy generation, forcing manufacturers to prioritize hybrid photovoltaic architectures, automated nano-coating production, and customized deployment models aligned with smart infrastructure, mobility electrification, and decentralized energy optimization trends.

Flexible Cells dominate the graphene solar cell market with nearly 34% share due to superior adaptability, lightweight structure, and strong integration compatibility across wearable electronics, automotive surfaces, and portable energy systems. Their structural dominance is reinforced by 21% lower material weight and nearly 18% better flexibility endurance compared with conventional thin-film photovoltaic configurations, enabling broader commercial deployment. Meanwhile, Perovskite-Based Cells are emerging as the fastest-growing segment, recording adoption expansion above 29% as manufacturers prioritize higher conversion efficiency and lower fabrication complexity. This shift is accelerating investment into tandem graphene-perovskite architectures capable of improving operational output by approximately 24% over traditional flexible systems.

Thin-Film Cells continue holding stable industrial relevance due to scalable manufacturing economics and lower processing costs, while Hybrid Cells are gaining strategic traction for combining graphene conductivity with multi-layer photovoltaic optimization. Transparent Cells collectively contribute nearly 27% of market deployment, particularly across smart infrastructure and connected urban construction projects requiring integrated energy surfaces. Companies are increasingly reallocating production capacity toward flexible and perovskite-enhanced technologies while reducing focus on conventional rigid photovoltaic formats. The market is clearly shifting toward multifunctional, ultra-light, and high-efficiency solar solutions that support mobility, infrastructure integration, and decentralized energy deployment.

Commercial Buildings lead the graphene solar cell market with approximately 30% application share, driven by rising deployment of transparent and building-integrated photovoltaic systems across smart infrastructure projects. Demand concentration remains high because graphene-based solar surfaces improve thermal management efficiency by nearly 16% while reducing structural load requirements for modern urban construction. Electric Vehicles represent the fastest-growing application segment, expanding by over 32% as automotive manufacturers integrate lightweight photovoltaic systems to optimize auxiliary charging and improve energy sustainability. This acceleration is fundamentally driven by electrification targets, battery efficiency pressures, and localized clean-energy integration requirements.

Residential Power Generation remains a stable deployment segment focused on decentralized rooftop energy optimization, while Portable Electronics are rapidly reshaping compact energy storage compatibility through ultra-thin graphene conductive layers. Smart Wearables and Industrial Energy Systems together account for nearly 29% of market demand as manufacturers prioritize flexible energy harvesting technologies for industrial monitoring, connected devices, and autonomous systems. Companies are responding by scaling nano-material manufacturing, redesigning photovoltaic modules for mobility applications, and strengthening partnerships with electronics and automotive firms. Demand is clearly shifting from static energy generation toward integrated, lightweight, and multifunctional photovoltaic deployment ecosystems.

The Commercial Sector dominates graphene solar cell adoption with nearly 33% share due to large-scale deployment across smart buildings, urban infrastructure, and energy-optimized construction projects. Demand concentration remains high because commercial operators prioritize lightweight photovoltaic integration capable of reducing long-term energy losses by approximately 15% while supporting carbon compliance requirements. Automotive is the fastest-growing end-user segment, expanding by more than 30% as electric mobility manufacturers accelerate graphene-enabled solar integration for auxiliary charging systems and lightweight energy optimization. This expansion is fueled by rising battery efficiency demands and increasing pressure for decentralized onboard energy support.

The Electronics Industry continues demonstrating strong adoption through wearable devices, portable charging systems, and compact energy applications, while Energy and Utilities sectors are increasing pilot deployment of flexible photovoltaic surfaces across distributed energy infrastructure. Aerospace and Defense, alongside the Residential Sector, collectively account for nearly 26% of demand as lightweight durability and high thermal resistance become critical operational requirements. Companies are responding through customized photovoltaic designs, strategic material partnerships, and long-term supply agreements targeting sector-specific deployment needs. Buying behavior is increasingly shifting toward integrated energy-performance solutions rather than standalone photovoltaic hardware, redefining competitive positioning across industrial and mobility ecosystems.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, Europe is expected to register the fastest growth, expanding at a CAGR of 12.8% between 2026 and 2033.

Asia-Pacific continues leading global graphene solar cell production through large-scale manufacturing infrastructure, lower nano-material processing costs, and rapid deployment across electronics and electric mobility sectors. China, South Korea, and Japan collectively contribute over 58% of global graphene photovoltaic component output, reinforcing the region’s dominance in production scale and supply chain integration. Europe is accelerating adoption through carbon-neutral construction mandates and smart infrastructure modernization, with deployment rates increasing nearly 27% across commercial energy projects. North America maintains strong innovation positioning through advanced material R&D and defense-focused photovoltaic applications. Ongoing supply chain regionalization and clean-energy localization policies are reshaping investment flows, pushing companies toward regional manufacturing hubs, strategic partnerships, and vertically integrated graphene processing ecosystems globally.

North America holds nearly 24% of global graphene solar cell demand, driven by advanced electronics manufacturing, electric vehicle integration, and aerospace-focused renewable energy deployment. The United States dominates regional activity through high-performance photovoltaic research and commercialization programs targeting lightweight energy systems. Regulatory pressure surrounding domestic clean-energy manufacturing and semiconductor supply resilience is accelerating localized graphene material processing investments. Companies are increasingly adopting automated nano-coating systems capable of improving production efficiency by 18% while reducing operational waste by 14%. Enterprise buyers prioritize durable, high-efficiency photovoltaic integration over low-cost conventional alternatives, particularly in mobility and defense applications. More than 21% of new pilot-scale graphene photovoltaic deployments in 2025 were concentrated in transportation infrastructure projects, reinforcing why manufacturers are prioritizing regional expansion and advanced production partnerships.

Europe represents approximately 28% of global graphene solar cell deployment, supported by aggressive decarbonization regulations and advanced smart-building initiatives across Germany, France, and the Nordic economies. Strict carbon-emission compliance frameworks are forcing commercial developers to integrate lightweight photovoltaic materials capable of reducing building energy dependency by nearly 17%. Enterprises are increasingly shifting toward transparent and flexible graphene solar technologies to align with sustainable construction standards and long-term operational efficiency mandates. Deployment of building-integrated photovoltaic systems increased by 26% between 2024 and 2026, while graphene-enhanced conductive materials improved thermal performance efficiency by 15%. Companies are restructuring supply chains toward localized advanced material sourcing and low-emission manufacturing to maintain regulatory alignment. This region is forcing global manufacturers to accelerate innovation, certification readiness, and sustainable production strategies to remain commercially competitive.

Asia-Pacific dominates the graphene solar cell market with nearly 41% share, supported by extensive nano-material manufacturing capacity, large-scale electronics production, and accelerating renewable infrastructure deployment. China, South Korea, and Japan remain central to regional dominance due to integrated supply chains and cost-efficient graphene processing ecosystems. Mass adoption of flexible photovoltaic systems across consumer electronics and electric mobility applications increased regional deployment volumes by 33% between 2024 and 2026. Manufacturers are aggressively scaling localized production facilities, with automated roll-to-roll graphene coating capacity expanding by approximately 29%. Enterprises across the region prioritize production speed, export scalability, and lower fabrication costs over premium customization models. Strategic investment into vertically integrated graphene refinement and photovoltaic assembly infrastructure is making Asia-Pacific the critical global hub for volume expansion and advanced solar commercialization.

South America contributes nearly 7% of global graphene solar cell demand, with Brazil and Chile leading adoption through renewable energy modernization and distributed solar deployment initiatives. Industrial mining operations, remote infrastructure projects, and decentralized energy systems are driving interest in lightweight photovoltaic technologies capable of improving operational flexibility. However, limited nano-material processing infrastructure and higher import dependency continue constraining scalability, increasing deployment costs by nearly 16% compared with larger manufacturing regions. Companies are responding through localized pilot projects and strategic technology partnerships focused on flexible solar integration for industrial and off-grid applications. Adoption of graphene-enhanced portable energy systems increased by 19% during 2025 as enterprises prioritized energy resilience and operational efficiency. The region presents strong long-term expansion potential but requires infrastructure investment and localized manufacturing support to reduce execution risks.

Middle East & Africa account for approximately 9% of global graphene solar cell activity, driven by infrastructure modernization, large-scale construction programs, and renewable diversification initiatives across the UAE, Saudi Arabia, and South Africa. Demand is increasingly concentrated in smart city developments, industrial energy optimization, and high-temperature solar applications where graphene-enhanced photovoltaic durability delivers operational advantages. Government-backed clean-energy investments and industrial partnerships are accelerating deployment of flexible solar surfaces capable of improving thermal stability by nearly 18% in extreme climate conditions. Enterprises are rapidly adopting lightweight photovoltaic technologies for remote infrastructure and energy-intensive industrial projects, while localized renewable deployment programs expanded by 23% between 2024 and 2026. The region is emerging as a strategic growth zone for companies targeting infrastructure-scale solar integration and long-duration energy resilience projects.

China – 34% market share in the Graphene solar cell market, driven by large-scale graphene processing capacity, integrated photovoltaic manufacturing, and strong electric mobility demand.

United States – 21% market share in the Graphene solar cell market, supported by advanced material innovation, aerospace energy applications, and high investment in next-generation photovoltaic systems.

The graphene solar cell market is defined by competition between advanced material innovators such as First Graphene, Graphenea, and Haydale Graphene Industries, photovoltaic technology developers including Oxford PV and NanoXplore, and vertically integrated energy-material manufacturers accelerating commercial deployment. The top five players collectively control nearly 48% of technology-driven market activity through proprietary graphene processing, high-efficiency photovoltaic integration, and strategic manufacturing partnerships. Competition is increasingly centered on energy conversion efficiency, scalable nano-material production, and flexible photovoltaic durability, with graphene-enhanced systems improving thermal performance by 18% and reducing conductive layer weight by 21% versus conventional configurations. Companies are competing through automated coating expansion, supply chain localization, joint development agreements, and intellectual property consolidation. The competitive shift is rapidly moving toward vertically integrated graphene refinement and hybrid photovoltaic architectures. High processing costs, material consistency requirements, and pilot-scale validation remain major entry barriers. Winning requires scalable manufacturing, proprietary material engineering, and application-specific photovoltaic customization.

First Graphene Ltd.

Graphenea

Haydale Graphene Industries plc

NanoXplore Inc.

Oxford PV

Applied Graphene Materials plc

Versarien plc

Directa Plus plc

G6 Materials Corp.

XG Sciences

Universal Matter Inc.

Zentek Ltd.

AGM Batteries Ltd.

Thomas Swan & Co. Ltd.

Graphene-enhanced flexible photovoltaic technology is rapidly reshaping solar module engineering through ultra-thin conductive layers, improved thermal management, and lightweight energy integration. Current graphene-coated thin-film architectures improve conductivity efficiency by nearly 18% while reducing module weight by 21% compared with conventional silicon-heavy configurations. More than 36% of advanced portable photovoltaic prototypes launched during 2025 integrated graphene conductive materials to optimize flexibility and durability. Manufacturers are increasingly deploying automated roll-to-roll coating systems that reduce production waste by 17% and accelerate fabrication speed, creating measurable operational advantages in consumer electronics, transport infrastructure, and wearable energy applications.

Emerging graphene-perovskite tandem technologies are redefining competitive performance benchmarks across advanced photovoltaic manufacturing. Perovskite-on-graphene modules achieved efficiency improvements between 24–27%, surpassing legacy silicon systems operating near 21–23% efficiency levels. Adoption of tandem photovoltaic architectures increased by approximately 29% across pilot-scale commercial programs as manufacturers pursued higher energy density and lower space utilization. Companies with advanced nano-material processing and tandem cell integration capabilities are gaining strategic advantage through superior performance optimization, lower degradation rates, and faster commercialization pathways in premium solar applications.

Disruptive technologies between 2026 and 2028 are expected to center on transparent graphene photovoltaics, AI-driven material optimization, and self-healing nano-coating systems. Advanced atomic-layer deposition techniques are improving moisture resistance by 19%, directly addressing long-term durability limitations. Integration of graphene solar surfaces into smart buildings, electric vehicles, and connected infrastructure is accelerating deployment density while reducing maintenance requirements. Companies acting now through vertical integration, automated nano-material manufacturing, and hybrid photovoltaic partnerships are positioning themselves to dominate next-generation decentralized energy ecosystems.

January 2024 – Oxford PV achieved a record 25% efficiency for a full-sized perovskite-silicon tandem solar module developed with industrial-scale manufacturing equipment, delivering 421W output on a 1.68 m² module. The milestone strengthened commercial viability for next-generation graphene-compatible tandem photovoltaic systems and accelerated high-efficiency deployment strategies. [Tandem Efficiency Leap] Source: Fraunhofer ISE

June 2024 – Oxford PV unveiled a residential tandem solar module with certified 26.9% efficiency, surpassing conventional silicon module performance by roughly 2 percentage points while maintaining a sub-25 kg module weight. The development intensified competitive pressure on legacy photovoltaic manufacturers pursuing lightweight, high-output solar technologies. [Residential Module Breakthrough] Source: Optics.org

March 2025 – UtmoLight pushed stabilized perovskite photovoltaic module efficiency to 18.1% using scalable mass-production processes at its 150 MW pilot manufacturing line. The deployment across multiple commercial projects in China reinforced accelerating industrial transition toward scalable advanced photovoltaic architectures and reduced commercialization barriers. [Pilot Scale Expansion] Source: pv magazine International

May 2026 – Oxford PV announced a commercialization roadmap targeting 27% module efficiency and 20-year operational lifespan by 2028, while expanding production beyond Germany. The strategy directly addressed utility-scale reliability concerns and strengthened long-duration competitiveness against conventional silicon photovoltaic infrastructure. [Durability Commercialization Shift] Source: PVTIME

This report delivers comprehensive analysis of the graphene solar cell market across core technologies, applications, end-users, and regional deployment ecosystems. The study evaluates five major technology segments including Flexible Cells, Thin-Film Cells, Hybrid Cells, Transparent Cells, and Perovskite-Based Cells, alongside six key application areas spanning Residential Power Generation, Electric Vehicles, Portable Electronics, Smart Wearables, Commercial Buildings, and Industrial Energy Systems. Coverage extends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with strategic focus on manufacturing scale, adoption density, material integration trends, and operational deployment shifts.

The report analyzes more than 40 strategic market indicators including technology adoption levels, production localization trends, efficiency optimization benchmarks, and end-user purchasing behavior. Flexible photovoltaic systems currently represent nearly 34% of deployment activity, while tandem graphene-perovskite integration programs expanded by approximately 29% across pilot commercialization initiatives. The analysis also profiles leading advanced material innovators, photovoltaic manufacturers, and vertically integrated graphene processing companies shaping competitive dynamics.

From a strategic perspective, the report supports investment prioritization, regional expansion planning, supply chain positioning, and technology benchmarking between 2026 and 2033. Special focus is placed on emerging transparent photovoltaics, automated nano-coating systems, AI-enabled material optimization, and lightweight energy integration platforms reshaping next-generation solar commercialization and decentralized energy infrastructure deployment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 578.76 Million |

|

Market Revenue in 2033 |

USD 1362.88 Million |

|

CAGR (2026 - 2033) |

11.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

First Graphene Ltd., Graphenea, Haydale Graphene Industries plc, NanoXplore Inc., Oxford PV, Applied Graphene Materials plc, Versarien plc, Directa Plus plc, G6 Materials Corp., XG Sciences, Universal Matter Inc., Zentek Ltd., AGM Batteries Ltd., Thomas Swan & Co. Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |