Reports

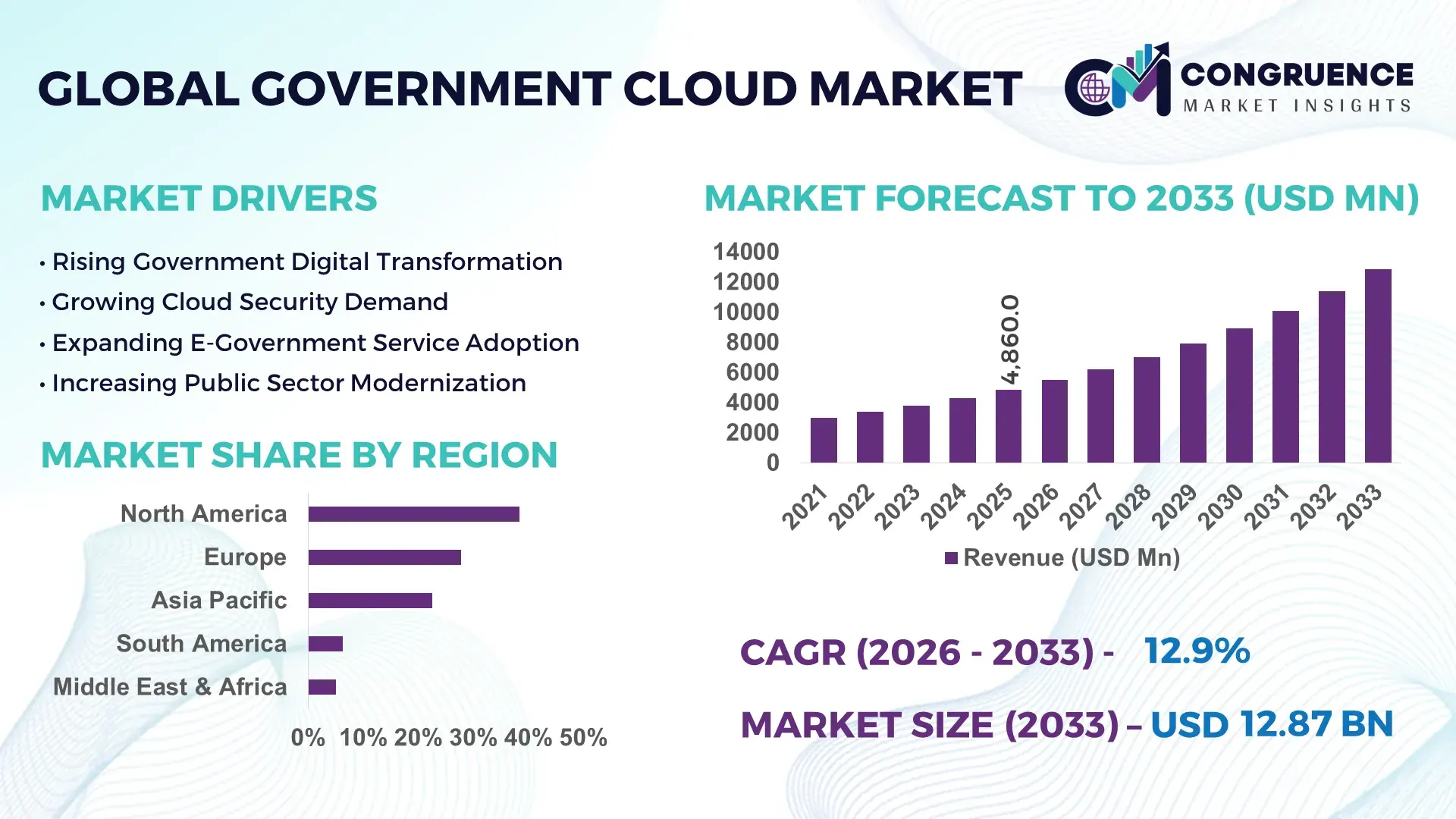

The Global Government Cloud Market was valued at USD 4,860.0 Million in 2025 and is anticipated to reach a value of USD 12,865.2 Million by 2033 expanding at a CAGR of 12.94% between 2026 and 2033. Growth is being accelerated by sovereign cloud mandates, public-sector AI deployment programs, and modernization of legacy government IT infrastructure across defense, healthcare, taxation, and citizen-service platforms.

The United States dominates the global government cloud landscape, accounting for nearly 38% of total public-sector cloud deployments, supported by federal cloud modernization budgets exceeding USD 12 billion and FedRAMP-authorized environments surpassing 350 cloud services. In comparison, the United Kingdom has digitized over 85% of central government services, while the U.S. maintains broader multi-agency cloud integration across defense and civilian departments. Rising cybersecurity requirements following heightened geopolitical tensions have further strengthened adoption of secure government cloud architectures.

For technology providers and infrastructure partners, prioritizing sovereign-cloud capabilities, compliance-ready platforms, and AI-enabled government workloads remains essential for long-term contract competitiveness.

Market Size & Growth: USD 4,860.0 Million in 2025, projected to reach USD 12,865.2 Million by 2033, supported by a 12.94% CAGR and accelerated government digital modernization programs.

Top Growth Drivers: Sovereign cloud adoption (+42%), public-sector cybersecurity spending (+18%), and AI-enabled government services deployment (+31%) are driving market expansion.

Short-Term Forecast: By 2028, cloud-based government operations are expected to reduce infrastructure maintenance costs by nearly 25% while improving service delivery efficiency by 30%.

Emerging Technologies: Generative AI, confidential computing, and zero-trust architecture are being integrated into over 40% of newly deployed government cloud environments.

Regional Leaders: North America (~USD 4.8 Billion by 2030), Europe (~USD 3.6 Billion), and Asia-Pacific (~USD 3.1 Billion) lead adoption through digital governance and sovereign-cloud initiatives.

Consumer/End-User Trends: More than 68% of public agencies are prioritizing cloud-native applications to improve citizen engagement and digital service accessibility.

Pilot/Case Example: In 2024, a national digital government project reduced application-processing times by 45% through cloud-based workflow automation.

Competitive Landscape: Microsoft holds approximately 23% market influence, with Amazon Web Services, Google Cloud, Oracle, and IBM remaining key strategic competitors.

Regulatory & ESG Impact: Government cloud deployments have lowered public-sector data-center energy consumption by up to 28% while strengthening compliance frameworks.

Investment & Funding: More than USD 15 billion has been allocated globally toward government cloud modernization, emphasizing sovereign infrastructure and cybersecurity resilience.

Innovation & Future Outlook: AI-driven governance platforms, digital identity ecosystems, and secure multi-cloud frameworks are reshaping next-generation public-sector operations.

Government Cloud Market demand is increasingly concentrated in digital citizen services, defense modernization, smart governance, and public healthcare platforms. Recent innovations include AI-assisted case management, confidential computing, and sovereign cloud environments designed for sensitive workloads. Nearly 40% of newly procured government digital platforms now require cloud-native architecture. Growing data-localization mandates and cyber-resilience requirements are encouraging agencies to prioritize secure, interoperable cloud ecosystems, setting the stage for broader strategic transformation.

Government cloud infrastructure has evolved into a strategic foundation for public-sector modernization, national cybersecurity resilience, and digital governance competitiveness. Governments are replacing fragmented legacy systems with integrated cloud environments capable of supporting real-time analytics, digital identity platforms, and AI-powered public services. Regulatory shifts emphasizing data sovereignty and secure digital infrastructure are accelerating procurement of sovereign and hybrid cloud architectures across critical government functions.

Cloud-native government environments deliver measurable operational advantages over traditional on-premise systems. Agencies adopting automated cloud management platforms report infrastructure provisioning times that are up to 70% faster and operational costs approximately 25–30% lower than legacy deployments. The United States leads large-scale multi-agency integration initiatives, while Singapore and the United Kingdom demonstrate higher deployment efficiency through centralized digital-government frameworks and cloud-first policies.

Over the next two to three years, public-sector cloud workloads are expected to represent a significantly larger share of government IT operations as agencies expand AI-enabled service delivery and cybersecurity modernization programs. Recent deployments integrating cloud-based citizen-service portals have reduced processing delays by over 40%. Technology providers are responding through sovereign-cloud partnerships, compliance-focused investments, and regional infrastructure expansion. Organizations that establish trusted, secure, and interoperable government cloud ecosystems will secure stronger competitive positioning and long-term relevance in public-sector digital transformation.

National governments are accelerating cloud adoption through sovereign digital infrastructure initiatives designed to improve cybersecurity, operational efficiency, and citizen-service delivery. More than 70% of advanced economies now maintain formal cloud-first or cloud-smart government strategies, while public-sector cybersecurity investments have increased by approximately 18% in the past three years. The expansion of AI-enabled administrative services has further increased demand for secure cloud environments capable of processing sensitive data. Following heightened geopolitical cyber threats, governments in the United States, Germany, and Australia have strengthened requirements for domestic data hosting and secure cloud operations. In response, cloud providers are expanding sovereign-cloud offerings, forming compliance partnerships, and investing in dedicated government regions. The strategic outcome is stronger public-sector resilience alongside greater vendor differentiation through security, compliance, and localized infrastructure capabilities.

Government cloud deployment continues to face structural limitations due to fragmented regulatory requirements and deep integration with legacy systems. Nearly 60% of government agencies still operate critical applications on infrastructure over a decade old, creating interoperability constraints during cloud migration. Compliance obligations can increase deployment timelines by 20–35%, particularly for defense, taxation, and public-safety workloads. Cross-border data transfer restrictions and data-localization mandates further complicate multi-cloud deployment strategies. Public-sector organizations in countries with decentralized administrative structures often encounter inconsistent procurement standards and certification requirements. To mitigate these challenges, technology providers are investing in localized data centers, compliance automation tools, and migration frameworks that reduce integration complexity. Successfully addressing regulatory and interoperability barriers remains essential for achieving scalable cloud transformation across government ecosystems.

The next phase of market expansion is being shaped by AI-enabled governance platforms, digital identity systems, and advanced citizen-service automation. More than 65% of government digital transformation initiatives now include AI, automation, or advanced analytics components. National digital identity adoption has exceeded 80% in several digitally advanced countries, creating opportunities for secure cloud-hosted public services. Governments are increasingly seeking platforms capable of supporting predictive service delivery, automated case management, and intelligent fraud detection. Emerging technologies such as confidential computing and privacy-enhancing technologies are improving trust in cloud-based processing of sensitive citizen data. Leading providers are expanding research partnerships, developing sector-specific government clouds, and integrating AI governance capabilities. A particularly attractive opportunity lies in modernizing medium-sized municipal agencies that remain underpenetrated despite rising digital-service expectations.

Long-term market expansion depends on solving increasingly complex cybersecurity and operational execution challenges. Government organizations experienced a rise of more than 25% in sophisticated cyber incidents targeting critical digital infrastructure over recent years, increasing pressure on cloud security architectures. At the same time, cybersecurity workforce shortages continue to affect nearly 40% of public-sector technology departments. Multi-cloud environments introduce additional complexity in identity management, monitoring, and compliance auditing across diverse platforms. Countries expanding large-scale digital-government initiatives face challenges maintaining consistent security standards across national and local agencies. Providers are responding through zero-trust security frameworks, managed security services, and workforce training partnerships. Organizations that successfully combine advanced security controls, cloud governance expertise, and scalable operational models will maintain stronger deployment consistency and sustainable competitive advantage.

Sovereign Cloud Deployment Expansion Government agencies are accelerating sovereign cloud adoption as data-localization requirements tighten across critical sectors. More than 45% of newly procured government cloud environments now include sovereign hosting requirements, while secure domestic data processing mandates have increased by nearly 30% over the past three years. Following heightened cybersecurity concerns and geopolitical data-governance pressures, providers are expanding localized infrastructure and compliance-ready environments, reducing procurement complexity and improving workload control for sensitive public-sector operations.

AI-Enabled Service Automation Growth Artificial intelligence is becoming embedded within government cloud workflows, with over 40% of newly modernized digital-service platforms incorporating AI-assisted automation. Automated document processing has reduced administrative handling times by approximately 35%, while AI-driven citizen support systems have improved response efficiency by nearly 25%. Technology vendors are scaling government-specific AI platforms and forming ecosystem partnerships to support secure deployment, operational transparency, and regulatory compliance.

Multi-Cloud Governance Adoption Public agencies are increasingly adopting multi-cloud architectures to improve resilience and vendor flexibility. Nearly 55% of large government organizations now operate workloads across multiple cloud environments, reducing dependency risks and improving service continuity. Advanced orchestration tools have lowered infrastructure provisioning times by almost 30%. In response, cloud providers are strengthening interoperability capabilities and expanding centralized governance frameworks to simplify operational management.

Zero-Trust Security Integration Zero-trust architecture is rapidly becoming a standard component of government cloud modernization programs. More than 60% of cybersecurity-focused cloud projects now incorporate continuous identity verification and adaptive access controls. Security teams report reductions of approximately 20% in unauthorized access incidents following implementation. Providers are investing heavily in automated threat detection, identity governance, and security analytics as agencies prioritize resilient digital infrastructure amid increasingly sophisticated cyber threats.

Hybrid Cloud represents the leading segment of the Government Cloud Market, accounting for approximately 46% of deployments due to its ability to balance security, scalability, and regulatory compliance. Government agencies increasingly rely on hybrid architectures to maintain sensitive workloads within controlled environments while leveraging public cloud resources for analytics, collaboration, and citizen-facing services. This model supports interoperability with legacy systems and reduces migration risks, making it particularly attractive for defense, taxation, and public administration functions. Private Cloud continues to maintain strong adoption in highly regulated environments, particularly where data sovereignty and mission-critical workloads require dedicated infrastructure and stricter access controls. Public Cloud is emerging as the fastest-growing segment, supported by expanding digital-service initiatives and cloud-native government applications. More than 35% of newly launched public-sector digital projects now utilize public cloud environments for faster deployment and lower infrastructure overhead. Cloud providers are responding by expanding sovereign-cloud offerings, compliance certifications, and government-focused service portfolios. Investment priorities are shifting toward flexible architectures that support workload portability, AI integration, and secure data exchange, positioning Hybrid Cloud and Public Cloud as central components of future government modernization strategies.

Security and Compliance remains the dominant application segment, representing nearly 30% of government cloud utilization as agencies prioritize cyber resilience, identity management, and regulatory adherence. Increasing cyber threats and data-protection requirements have accelerated investments in secure cloud frameworks, encryption technologies, and zero-trust architectures. Government organizations are integrating compliance automation and continuous monitoring capabilities to improve operational visibility while reducing administrative burdens. Disaster Recovery and Data Backup also maintain significant demand as public institutions seek greater service continuity and resilience against operational disruptions. Analytics is the fastest-growing application segment as governments expand data-driven policymaking and AI-enabled public services. More than 40% of new digital-government programs now include advanced analytics capabilities to improve resource allocation, fraud detection, and citizen-service performance. Server and Storage applications continue to underpin large-scale modernization efforts, while Content Management platforms are gaining traction through digitization of public records and document-intensive workflows. Technology providers are expanding automation capabilities and integrating AI-powered analytics to strengthen decision-making, accelerate service delivery, and improve operational efficiency across government environments.

Federal and Central Government agencies constitute the largest end-user segment, contributing approximately 50% of overall demand due to their extensive digital infrastructure, cybersecurity responsibilities, and large-scale modernization initiatives. National-level departments manage significant volumes of citizen, defense, taxation, and administrative data, creating sustained demand for secure and scalable cloud environments. Large procurement budgets and centralized cloud strategies further reinforce adoption. Defense and Military agencies also represent a substantial segment as intelligence operations, secure communications, and mission-critical systems increasingly transition toward cloud-enabled architectures with enhanced security controls. State and Local Government organizations are emerging as the fastest-growing end-user category as regional administrations accelerate digital-service modernization and citizen engagement initiatives. Nearly 38% of local government technology projects launched during recent modernization programs have incorporated cloud-first deployment strategies. Vendors are responding through customized service packages, managed-security offerings, and public-sector partnerships tailored to regional agencies with limited in-house IT resources. Demand is increasingly shifting toward solutions that simplify compliance, improve operational efficiency, and support scalable service delivery, creating new competitive opportunities across subnational government institutions.

North America accounted for the largest market share at 38.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 14.8% between 2026 and 2033.

North America remains the largest Government Cloud Market, supported by extensive public-sector digital transformation programs, advanced cybersecurity infrastructure, and mature cloud procurement frameworks. The region contributes approximately 38.4% of global market demand, with federal agencies accounting for a substantial share of cloud spending and deployment activity. Government organizations are increasingly transitioning mission-critical workloads to hybrid and sovereign cloud environments to improve operational resilience and data security. Recent federal modernization programs have accelerated cloud-native application deployment, while multi-cloud adoption across major agencies has surpassed 50%. Technology vendors continue expanding compliance-certified cloud environments and strategic public-sector partnerships, strengthening the region’s leadership in secure government cloud implementation and digital governance innovation.

United States Market Outlook: The United States dominates regional demand through large-scale federal cloud modernization initiatives, extensive cybersecurity investments, and advanced regulatory frameworks supporting cloud adoption. More than 350 government-authorized cloud services operate under stringent compliance standards, while a growing share of federal agencies are implementing AI-enabled digital service platforms. Strong collaboration between government departments and leading cloud providers continues to accelerate infrastructure modernization, secure workload migration, and digital citizen-service expansion, reinforcing the country's position as the most influential government cloud market globally.

Europe represents a significant government cloud market driven by digital sovereignty initiatives, cybersecurity regulations, and public-sector modernization programs. The region accounts for approximately 27.8% of global demand, with governments prioritizing secure cloud infrastructures aligned with national data governance requirements. Sovereign cloud deployments are expanding rapidly as agencies seek greater control over sensitive public data and critical digital services. Several European governments are integrating cloud-first procurement frameworks and centralized digital governance models to improve efficiency. Public-sector organizations are also adopting cloud-based analytics and citizen-service platforms, while technology providers continue investing in regionally compliant cloud infrastructure and security-focused partnerships.

Germany Market Outlook: Germany serves as a leading government cloud market due to its strong industrial base, advanced digital infrastructure, and emphasis on data protection. Federal and state-level administrations are expanding secure cloud adoption across taxation, public administration, and healthcare services. Government-backed digital modernization initiatives have accelerated migration from legacy systems, while increasing investment in sovereign-cloud frameworks strengthens national cybersecurity capabilities. Germany’s focus on regulatory compliance and digital resilience continues to position it as a strategic center for government cloud innovation.

Asia-Pacific is emerging as the fastest-expanding government cloud market, supported by aggressive digital-government initiatives, smart governance programs, and expanding public-sector IT investments. The region contributes approximately 22.5% of global market activity and is witnessing rapid deployment of cloud-enabled citizen-service platforms. Governments are increasingly adopting cloud-native infrastructure to support digital identity systems, healthcare modernization, and administrative automation. Large-scale investments in digital infrastructure and cybersecurity are strengthening deployment capacity, while local cloud ecosystems continue expanding through public-private collaboration. Growing demand for scalable and cost-efficient government technology platforms is further accelerating adoption across developing and advanced economies.

China Market Outlook: China leads regional deployment activity through extensive government digitization programs and large-scale investments in domestic cloud infrastructure. Public-sector agencies continue expanding cloud adoption across smart-city administration, public security, and digital governance applications. Government-supported infrastructure projects have strengthened domestic cloud capabilities, while increasing emphasis on data localization and cybersecurity has accelerated deployment of compliant cloud environments. The country’s substantial public-sector technology investments and operational scale position it as a major driver of government cloud adoption throughout Asia-Pacific.

South America is experiencing steady government cloud adoption as public institutions modernize administrative systems and expand digital service delivery. The region accounts for approximately 6.3% of global market demand, supported by increasing investments in e-government platforms, cybersecurity frameworks, and public-sector digitalization programs. Governments are prioritizing cloud deployment to improve operational efficiency, citizen engagement, and service accessibility. However, infrastructure disparities and budget constraints continue to influence deployment speed across several countries. Technology providers are addressing these limitations through managed-service partnerships, localized cloud offerings, and phased modernization strategies designed to improve implementation outcomes and reduce operational complexity.

Brazil Market Outlook: Brazil represents the largest government cloud market in South America due to its sizeable public-sector infrastructure and expanding digital transformation agenda. Federal agencies are increasing cloud utilization across taxation, public administration, and citizen-service platforms to improve service delivery efficiency. Government-backed digital modernization programs continue to encourage migration toward secure cloud environments, while growing cybersecurity investments strengthen cloud adoption across critical government functions. Brazil’s large administrative scale and evolving regulatory framework support continued cloud deployment activity throughout the public sector.

The Middle East & Africa government cloud market is expanding through national digital transformation programs, smart-government initiatives, and increasing investment in secure digital infrastructure. The region contributes approximately 5.0% of global demand, with governments prioritizing cloud deployment to improve public-service efficiency, data management, and cybersecurity readiness. Significant investment in digital infrastructure and government technology modernization is creating new deployment opportunities across public institutions. Strategic partnerships between technology vendors and government agencies are strengthening cloud adoption capabilities, while increasing demand for sovereign-cloud environments supports compliance and data governance objectives across critical sectors.

Saudi Arabia Market Outlook: Saudi Arabia is the most strategically significant government cloud market within the region, supported by extensive digital transformation objectives and strong public-sector technology investments. Government agencies are expanding cloud deployment across smart-government platforms, healthcare administration, and digital citizen services. National initiatives focused on economic diversification and public-sector modernization continue driving infrastructure development and cloud adoption. The country's growing investment in data centers, cybersecurity frameworks, and cloud partnerships is strengthening deployment capacity while positioning Saudi Arabia as a leading digital-government hub within the Middle East and Africa region.

The Government Cloud Market is led by global hyperscalers including Microsoft, Amazon Web Services, Google Cloud, Oracle, and IBM, which collectively control approximately 68–72% of market activity. Competition primarily occurs between global cloud leaders offering broad sovereign-cloud portfolios and regional providers focused on data residency, compliance, and localized infrastructure. Technology capability, security certification, and deployment speed outweigh price competition in most government procurements. Agencies increasingly prioritize sovereign-cloud functionality, with over 45% of new government cloud projects requiring enhanced data-control capabilities. AI-enabled cloud platforms have improved operational efficiency by nearly 30%, while automated compliance tools reduce deployment timelines by approximately 20%. Vendors are expanding through sovereign-cloud partnerships, regional infrastructure investments, defense-sector collaborations, and AI integration. Competitive dynamics are shifting toward sovereignty-focused ecosystems and secure AI deployment. High certification requirements, regulatory approvals, and cybersecurity obligations remain significant entry barriers. Success depends on combining trusted compliance, sovereign infrastructure, advanced AI capabilities, and proven public-sector execution.

Amazon Web Services (AWS)

Google Cloud LLC

Oracle Corporation

IBM Corporation

Salesforce Inc.

SAP SE

VMware LLC

Dell Technologies Inc.

Alibaba Cloud

Rackspace Technology

Fujitsu Limited

NTT DATA Group

Thales Group

Government cloud technology is rapidly evolving beyond traditional infrastructure hosting toward intelligent, sovereign, and security-centric environments. Hybrid cloud architectures remain the dominant deployment model, supporting approximately 46% of government implementations due to their ability to combine regulatory control with scalable computing resources. Zero-trust security frameworks are now integrated into more than 60% of cybersecurity-focused government cloud projects, reducing unauthorized access risks while improving compliance visibility. Automated governance tools are helping agencies shorten policy enforcement cycles by nearly 25%.

Artificial intelligence, confidential computing, and sovereign-cloud platforms are emerging as the most influential technologies shaping government cloud deployments. AI-enabled workflow automation has reduced administrative processing times by approximately 35%, while advanced analytics platforms improve operational decision-making speed by over 30%. Compared with legacy on-premise infrastructure, cloud-native government environments can reduce provisioning times by nearly 70% and lower operational overhead by approximately 25%. Hyperscale providers and specialized sovereign-cloud operators benefit most from this transition because they possess the infrastructure scale and regulatory expertise required for public-sector workloads.

Between 2026 and 2028, adoption of sovereign AI environments, disconnected cloud operations, and privacy-enhancing technologies is expected to accelerate. Governments are increasingly prioritizing secure AI processing, localized data governance, and interoperable cloud ecosystems. Organizations investing early in compliance-ready AI platforms and sovereign-cloud architectures will secure stronger operational resilience, procurement competitiveness, and long-term public-sector engagement opportunities.

July 2025 – Google Cloud secured a USD 200 million ceiling contract from the U.S. Department of Defense Chief Digital and Artificial Intelligence Office (CDAO) to accelerate AI and cloud deployment using Google’s cloud infrastructure and TPUs. The agreement strengthens defense-sector cloud modernization and AI readiness. Source: www.cloud.google.com

December 2025 – Microsoft announced expanded Microsoft 365 Government capabilities, adding AI-powered security and management functions across government cloud offerings. The enhancements support wider public-sector deployment while strengthening compliance and cyber resilience for government agencies operating in increasingly complex threat environments.

February 2026 – Microsoft expanded Microsoft Sovereign Cloud with disconnected operations, enabling organizations to run mission-critical infrastructure and large AI models without cloud connectivity. The platform supports fully disconnected sovereign environments and extends support for government, defense, and classified workloads requiring maximum operational control.

June 2026 – Microsoft and the Australian Government signed a strategic Memorandum of Understanding focused on secure cloud infrastructure, cybersecurity, AI systems, and critical infrastructure protection. The partnership establishes a national framework for digital resilience and strengthens government cloud deployment across security-sensitive environments.

The report provides comprehensive coverage of the Government Cloud Market across deployment models, applications, end-user groups, competitive dynamics, technology evolution, and regional demand patterns. Analysis includes Public Cloud, Private Cloud, and Hybrid Cloud environments; applications such as security and compliance, analytics, disaster recovery, server and storage infrastructure, and content management; and key end-user segments including federal, state, local, defense, and intelligence agencies. More than 60% of current deployment activity is concentrated in security-sensitive and mission-critical government workloads.

The study evaluates market developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting adoption trends, sovereign-cloud initiatives, AI integration, cybersecurity modernization, and digital-government transformation. It also examines strategic positioning of leading cloud providers, technology deployment patterns, partnership activity, and evolving procurement priorities. The report supports investment evaluation, market-entry planning, infrastructure expansion, competitive benchmarking, and long-term strategic decision-making across the 2026–2033 planning horizon.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 4,860.0 Million |

| Market Revenue (2033) | USD 12,865.2 Million |

| CAGR (2026–2033) | 12.94% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Microsoft Corporation; Amazon Web Services (AWS); Google Cloud LLC; Oracle Corporation; IBM Corporation; Salesforce Inc.; SAP SE; VMware LLC; Dell Technologies Inc.; Alibaba Cloud; Rackspace Technology; Fujitsu Limited; NTT DATA Group; Thales Group |

| Customization & Pricing | Available on Request (10% Customization Free) |