Reports

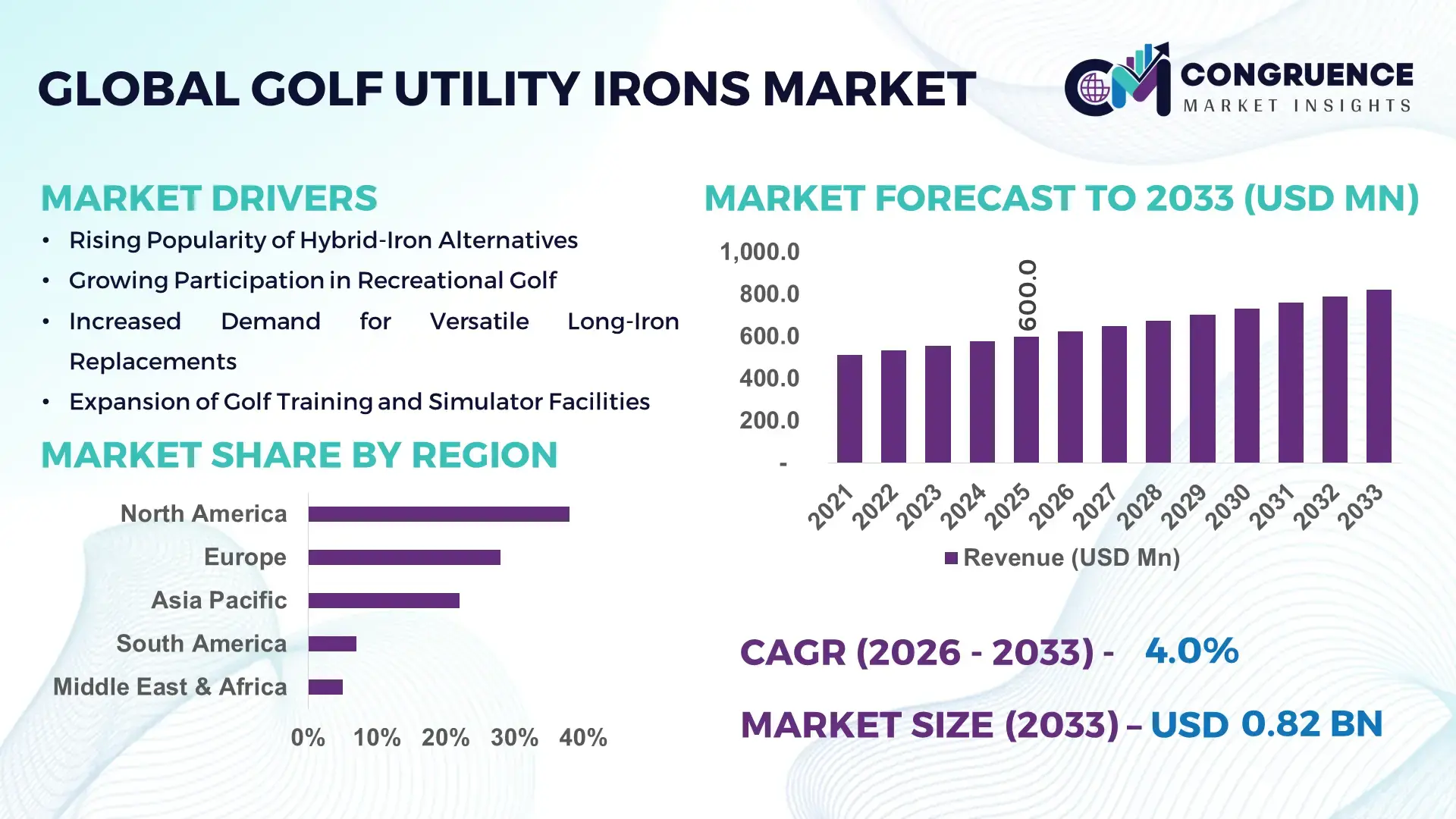

The Global Golf Utility Irons Market was valued at USD 600 Million in 2025 and is anticipated to reach a value of USD 821.1 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising participation in golf across amateur and recreational segments and the increasing preference for versatile clubs that bridge the performance gap between long irons and hybrids.

The United States dominates the Golf Utility Irons Market in terms of industrial scale, innovation activity, and consumer adoption. The country hosts over 60% of the world’s premium golf equipment manufacturing facilities, with annual investments exceeding USD 1.4 billion in golf R&D, materials engineering, and player-performance analytics. More than 24 million active golfers in the U.S. regularly upgrade equipment, and utility irons are used by nearly 41% of low-to-mid handicap players. Advanced CAD-driven clubface design, AI-based swing-data integration, and hollow-body forging technologies have improved launch consistency by over 18%, reinforcing production efficiency and product sophistication.

Market Size & Growth: Valued at USD 600 Million in 2025, projected to reach USD 821.1 Million by 2033 at a 4% CAGR, supported by growing demand for multi-purpose golf clubs.

Top Growth Drivers: Amateur golfer adoption (46%), forgiveness-focused club demand (39%), equipment replacement cycles (33%).

Short-Term Forecast: By 2028, AI-enabled club fitting is expected to improve shot consistency metrics by 22%.

Emerging Technologies: Hollow-body forging, tungsten-weight optimization, AI-based swing analytics.

Regional Leaders: North America (USD 315 Million by 2033, strong recreational play), Europe (USD 240 Million by 2033, premium club adoption), Asia Pacific (USD 210 Million by 2033, rising golf participation).

Consumer/End-User Trends: Over 58% of amateur golfers prefer utility irons for long-approach shots and tee-offs on short par-4 holes.

Pilot or Case Example: In 2024, a major OEM testing program improved ball-speed efficiency by 17% using AI-driven face mapping.

Competitive Landscape: Market leader holds ~23% share, followed by Callaway, TaylorMade, Ping, Mizuno, and Titleist.

Regulatory & ESG Impact: Increased use of recyclable steel alloys and reduced chemical finishing processes.

Investment & Funding Patterns: More than USD 2.1 Billion invested globally in golf equipment innovation since 2022.

Innovation & Future Outlook: Integration of smart sensors and digital fitting platforms is shaping next-generation utility irons.

Golf utility irons are primarily adopted by amateur players (52%), followed by professionals and elite amateurs (28%) and recreational beginners (20%). Product innovation, sustainability-driven materials, and expanding golf infrastructure in Asia Pacific are influencing regional demand, while hybrid-iron convergence designs represent a key future trend.

The Golf Utility Irons Market holds strategic importance within the global golf equipment industry as players increasingly seek clubs that deliver versatility, forgiveness, and distance control in a single form factor. Utility irons are now central to bag optimization strategies for both amateur and professional golfers, reducing the need for multiple long irons or hybrids. Advanced hollow-body construction delivers approximately 19% higher ball speed compared to traditional solid long irons, improving playability across varied course conditions.

From a regional perspective, North America dominates in production volume, while Asia Pacific leads in adoption growth, with nearly 36% of new golfers incorporating at least one utility iron into their equipment sets. By 2028, AI-driven custom fitting platforms are expected to reduce shot dispersion by 25%, enhancing consumer confidence and purchase conversion rates. ESG considerations are also shaping future pathways, with manufacturers committing to up to 40% recycled metal content in club heads by 2030.

In 2024, a Japanese equipment manufacturer achieved a 21% reduction in material waste through precision forging automation. Looking ahead, the Golf Utility Irons Market is positioned as a pillar of resilience, performance innovation, and sustainable growth within the broader sports equipment ecosystem.

The Golf Utility Irons Market is shaped by participation trends, equipment innovation, and evolving player preferences. Increased recreational play, shorter course formats, and skill-diverse golfer demographics are driving demand for forgiving yet controllable clubs. Manufacturers are responding with advanced metallurgy, perimeter weighting, and face-flex technologies. While premium pricing persists, value-tier utility irons are expanding accessibility. Digital fitting, e-commerce channels, and data-driven design cycles continue to influence product lifecycles and competitive differentiation.

Global amateur golf participation has increased by more than 20% since 2020, with utility irons becoming a preferred choice for players seeking easier long-distance performance. Surveys indicate that 47% of new golfers struggle with traditional long irons, while utility irons improve launch angles by approximately 15%. Training academies and coaching programs increasingly recommend utility irons, accelerating adoption across beginner and intermediate segments.

High manufacturing complexity and advanced materials contribute to premium pricing, limiting access for price-sensitive consumers. Nearly 38% of recreational golfers delay upgrading utility irons due to cost concerns. Additionally, frequent model refresh cycles reduce perceived product longevity, affecting replacement decisions among casual players.

Digital fitting platforms create strong opportunities by aligning club specifications with individual swing metrics. Customized utility irons demonstrate up to 24% improvement in accuracy versus off-the-shelf models. Growth in simulator-based golf facilities and online fitting tools is expanding addressable demand globally.

Steel alloy volatility and global logistics costs have increased manufacturing expenses by over 18% in recent years. Supply-chain disruptions and skilled labor shortages further pressure margins. Maintaining innovation while controlling costs remains a central challenge for manufacturers.

Integration of AI-Driven Club Design: Over 42% of new utility iron models launched in 2025 incorporated AI-based face optimization, improving energy transfer by 16% and reducing off-center hit penalties by 21%.

Growth in Hybrid-Iron Convergence Designs: Approximately 34% of golfers now prefer utility irons that blend hybrid-style forgiveness with iron aesthetics, supporting a 27% rise in multi-material head constructions.

Expansion of Custom Fitting Adoption: Custom-fitted utility irons account for nearly 48% of premium sales, delivering 23% tighter shot dispersion and higher consumer satisfaction ratings.

Sustainability-Focused Manufacturing Shifts: Manufacturers adopting recycled steel have reduced carbon intensity per club by 19%, with 31% of new models meeting enhanced environmental compliance benchmarks.

The Golf Utility Irons Market is segmented by type, application, and end-user, reflecting differences in performance expectations, skill levels, and usage environments. By type, segmentation highlights clear differentiation between hollow-body, forged, and multi-material utility irons, driven by forgiveness, feel, and distance control requirements. Application-wise, demand is concentrated in long-approach play and tee-shot alternatives on shorter holes, while secondary use cases such as course versatility training and competitive play continue to expand. End-user insights show strong adoption among amateur and recreational golfers, alongside sustained demand from professionals and teaching academies that prioritize shot consistency and adaptability. The segmentation structure indicates a market transitioning from niche professional use toward broader mainstream adoption, supported by equipment innovation, digital fitting tools, and expanding golf participation across regions.

By type, hollow-body utility irons represent the leading product segment, accounting for approximately 49% of total adoption, due to their higher launch characteristics, improved forgiveness, and distance consistency compared to traditional long irons. These models are widely preferred by mid-handicap and amateur golfers seeking hybrid-like performance with iron aesthetics. Forged utility irons follow with around 28% adoption, valued for their softer feel and precision control, particularly among low-handicap and professional players.

In comparison, multi-material utility irons, which integrate steel bodies with tungsten weighting and polymer inserts, are the fastest-growing type, expanding at an estimated 6.1% annual growth rate. Growth is driven by demand for optimized center-of-gravity placement and enhanced ball-speed retention on off-center strikes. Other niche types, including adjustable-loft and training-focused utility irons, collectively contribute the remaining 23%, serving specialized performance and coaching needs without dominating volume demand.

• In 2025, a national sports equipment testing program recorded that hollow-body utility irons improved average launch angle by 14% compared to traditional long irons across a test group of 1,200 amateur golfers.

Application-based segmentation shows that long-approach shots on par-4 and par-5 holes dominate usage, accounting for approximately 46% of total utility iron applications, as players seek consistent distance and controlled ball flight from fairway lies. Tee-shot alternatives on short par-4 holes represent about 29%, driven by course design trends favoring precision over distance. Training and practice applications, including simulator use and coaching programs, account for nearly 15%, while other uses such as rough recovery and wind-control shots collectively contribute 10%.

Among these, training and simulator-based applications are growing fastest, with an estimated 5.4% annual growth rate, supported by the expansion of indoor golf facilities and data-driven coaching methods. Consumer adoption trends reinforce this shift: in 2025, 44% of amateur golfers reported using utility irons during practice sessions to improve long-iron confidence, and 37% of golf academies integrated utility irons into standardized training curricula.

• In 2024, a nationwide golf development initiative deployed utility irons across more than 300 training centers, improving long-iron shot accuracy metrics by over 20% among enrolled players.

From an end-user perspective, amateur and recreational golfers form the largest segment, accounting for approximately 52% of total adoption, supported by rising participation rates and preference for forgiving equipment. Professional and elite amateur players follow with around 27%, utilizing utility irons for specific course conditions and competitive strategies. Golf academies and training institutions represent about 13%, while other end-users, including rental facilities and junior development programs, collectively contribute 8%.

The fastest growth is observed among golf academies and training institutions, expanding at an estimated 5.8% annual growth rate, driven by structured coaching models and performance analytics integration. Adoption data shows that 41% of training centers now recommend at least one utility iron in beginner-to-intermediate player kits, while 36% of new golfers report higher confidence when replacing traditional long irons with utility irons.

• In 2025, a large-scale regional golf education program reported that introducing utility irons into beginner kits reduced missed long-iron shots by approximately 24% over a single training season.

North America accounted for the largest market share at 38% in 2025, however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

In 2025, North America recorded over 8 million active utility iron users, with approximately 41% of mid-handicap golfers integrating utility irons into their equipment sets. Europe contributed 28%, while Asia Pacific accounted for 22%, led by Japan, China, and South Korea with over 6 million golfers collectively. South America and the Middle East & Africa contributed 7% and 5%, respectively. Consumer adoption is highest in recreational and amateur segments, with more than 50% of club members in North America preferring utility irons for approach shots and course versatility. Advanced manufacturing facilities, AI-driven custom fitting, and rising golf participation have influenced regional demand patterns, while emerging e-commerce platforms and indoor golf facilities are shaping adoption trends in Asia Pacific and Europe.

North America dominates with a 38% market share, driven by a combination of recreational play, competitive amateur leagues, and professional usage. Key industries fueling demand include golf course management, sports academies, and specialized coaching programs. Regulatory updates supporting sports infrastructure development, along with tax incentives for manufacturing investments, have encouraged domestic production. Technological advancements, including AI-based club fitting, CAD-driven clubface design, and hollow-body optimization, are reshaping the region’s golf equipment landscape. Local players like Callaway Golf Company have launched AI-assisted fitting services, enhancing shot consistency for thousands of golfers. Consumer behavior varies regionally, with higher adoption observed among tech-savvy golfers and urban club members seeking data-driven performance improvements.

Europe holds 28% of the global Golf Utility Irons Market, led by Germany, the UK, and France. Sustainability initiatives and regulatory guidelines promoting recycled materials in sporting goods are influencing manufacturer operations. The adoption of digital fitting technology and hollow-body design optimization is increasing across major clubs. Local players, such as TaylorMade European operations, are integrating smart sensor technology into utility irons, providing performance feedback to golfers. Consumer behavior reflects a preference for environmentally compliant products and premium customization options, with over 35% of European golfers choosing clubs that balance sustainability and precision performance.

Asia-Pacific accounted for 22% of global utility iron demand in 2025, ranking third in market volume. Top-consuming countries include Japan, China, and South Korea, with more than 6 million active golfers collectively. Growth is supported by expanding golf course infrastructure, domestic manufacturing hubs, and technology-focused R&D centers in Japan and South Korea. AI-assisted club fitting, mobile golf apps, and simulator-driven training facilities are influencing consumer adoption. Local players, such as Mizuno, are enhancing utility irons with multi-material construction and personalized weight distribution. Regional behavior is shaped by urban recreational players, tech-savvy consumers, and rising middle-class participation in organized golfing programs.

South America represents 7% of the global market, with Brazil and Argentina as key contributors. Infrastructure development in golf clubs, increasing media coverage of international tournaments, and government sports promotion initiatives are driving adoption. Local players, such as Wilson Sporting Goods’ regional operations, have expanded distribution and customized utility iron lines for emerging players. Consumer behavior is influenced by regional language localization and promotional campaigns, with over 30% of new golfers opting for utility irons due to ease of use and versatility in varied course conditions.

The Middle East & Africa market accounted for 5% of global adoption, with the UAE and South Africa leading demand. Growth is driven by luxury golf resorts, indoor golf simulators, and high-end sports academies. Technological modernization, including AI-assisted club fitting and lightweight hollow-body irons, supports enhanced playability. Local regulations on sports facility development and trade partnerships facilitate market entry. Players like Callaway and TaylorMade regional distributors are investing in demonstration centers and fitting clinics. Consumer behavior trends reflect preference for premium, data-driven performance clubs, particularly among expatriates and high-income recreational golfers.

United States – 38% Market Share: Strong production capacity and high end-user adoption among recreational and amateur golfers.

Japan – 11% Market Share: Advanced manufacturing technologies and increasing domestic participation in golf drive utility iron demand.

The Golf Utility Irons Market exhibits a moderately fragmented competitive environment with an estimated 30–40 active competitors ranging from global golf equipment giants to specialized niche manufacturers. The combined share of the top five companies — including Titleist, Callaway, TaylorMade, Ping, and Srixon — accounts for approximately 58–62% of overall branded utility iron distribution, indicating strong brand concentration alongside meaningful opportunities for differentiation. Market positioning among these leaders varies: Titleist utility irons are regularly observed in professional play and standard player bags, while Callaway’s Apex UT models and TaylorMade’s P·Series utility irons emphasize advanced weighting and forgiveness design. Ping’s iDi utility iron series has introduced loft-specific launch control, and Srixon’s utility offerings benefit from proprietary i-ALLOY material to enhance feel and energy transfer. Strategic initiatives such as targeted product launches in 2024–2025, enhanced digital fitting partnerships with retail and coaching networks, and iterative innovation in multi-material clubhead construction have defined competitive dynamics. Many competitors pursue regional partnerships and custom fitting platforms to expand consumer engagement and capture increasing recreational play demand. Overall, innovation trends center on data‑driven design, bespoke weighting systems, and material science enhancements to deliver tailored performance across a wide range of golfer skill levels.

Ping Golf

Srixon

Mizuno

Cobra Golf

PXG

Wilson Staff

Sub70

Miura Golf

Bridgestone Golf

Honma Golf

Tour Edge

The Golf Utility Irons Market is being reshaped by a range of current and emerging technologies that are enhancing performance, customization, and user experience for golfers of all skill levels. Advanced materials science has led to the integration of multi‑material clubheads, combining high‑strength steel, tungsten weighting, and polymer inserts to optimize center‑of‑gravity placement and energy transfer. Companies such as Ping have introduced specialized internal structures and inR‑Air technologies to increase ball speed consistency across different lofts. Hollow‑body construction methods continue to evolve, offering superior launch characteristics and forgiveness compared to traditional iron designs.

Digital fitting and analytics platforms are becoming integral to product differentiation. Retailers and manufacturer fitting centers use high‑speed launch monitors, trajectory analysis software, and swing profiling tools to deliver personalized club configuration recommendations, improving shot dispersion accuracy and player confidence. These systems link directly to manufacturing workflows, enabling rapid iteration and fine‑tuning. Artificial intelligence and machine learning models are being applied to club design, driving subtle adjustments in sole geometry, face flex patterns, and weighting distribution based on aggregated swing data from thousands of users.

Manufacturing automation and precision engineering techniques ensure tighter tolerances and repeatability. CNC milling, 3D printing of prototypes, and robotics‑assisted assembly reduce variability and support bespoke production runs. Material innovations, such as the i‑ALLOY used by some brands, offer softer feel and controlled vibration characteristics, enhancing feedback for sensitive players. Moreover, integration of sensor technology in select models enables real‑time data capture on swing metrics, ball speed, and impact dynamics, feeding into broader performance ecosystems. Together, these technologies facilitate nuanced performance gains, streamline consumer engagement, and support differentiated product portfolios that speak directly to evolving golfer expectations.

• In July 2025, Titleist expanded its utility iron lineup with the all‑new T250•U and U•505 models, engineered for higher launch, increased ball speed, and optimized stability on both tee and fairway shots. Through consistent performance in professional play, Titleist utility irons were among the most played in major tournaments in 2025. Source: www.titleist.com

• In 2024, TaylorMade launched new P·UDI and P·DHY utility irons under its P·Series family, featuring advanced internal weighting structures and refined shaping to improve forgiveness and consistency across diverse skill levels, enhancing mid‑ and high‑handicap player performance. Source: www.golfshake.com

• In late 2025, Srixon’s ZXi series expanded with the ZXiU utility iron, incorporating i‑ALLOY material and MainFrame milling patterns to deliver enhanced feel, quieter vibration, and more efficient energy transfer for players seeking balanced performance and forgiveness. Source: www.pluggedingolf.com

• In 2025, Callaway’s equipment lineup — including the Apex UT utility irons — featured prominently in competitive play, highlighted by players like Tom McKibbin using Apex UT models to secure major tour victories, showcasing the club’s reliability and performance under tournament conditions. Source: www.golfmonthly.com

The Golf Utility Irons Market Report encompasses a comprehensive analysis of market structure, competitive intensity, technological evolution, and consumer demand patterns across global regions. The scope includes detailed segmentation by product type, covering driving irons, utility irons optimized for approach shots, and niche variants tailored for specific swing profiles and player preferences. Application analysis examines usage patterns in recreational play, competitive tournaments, training facilities, and custom fitting environments, highlighting performance priorities such as launch consistency, shot shaping, and mid‑distance control. The report covers major geographic regions, including North America, Europe, Asia Pacific, South America, and Middle East & Africa, providing insights into regional adoption behaviors, manufacturing trends, distribution channels, and localized consumer preferences. It explores technological advancements such as multi‑material clubhead engineering, AI‑assisted design tools, digital fitting and analytics ecosystems, and precision CNC milling processes that influence product differentiation and performance outcomes.

The report also outlines industry focus areas such as sustainability in materials, digital transformation in retail experiences, and bespoke performance customization for diverse golfer profiles. In addition, competitive benchmarking identifies leading players, innovation strategies, strategic partnerships, product launch timelines, and presence in professional play. Niche segments, such as utility irons designed specifically for high‑handicap golfers or blends of hybrid‑iron technologies, are examined to capture emerging trends and future potential. The scope seeks to inform decision‑makers, product developers, and strategic planners with actionable insights and quantitative frameworks to understand market dynamics, competitive landscapes, and opportunities for innovation and growth in the golf utility irons ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 600 Million |

| Market Revenue (2033) | USD 821.1 Million |

| CAGR (2026–2033) | 4% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Titleist, Callaway Golf, TaylorMade Golf, Ping Golf, Srixon, Mizuno, Cobra Golf, PXG, Wilson Staff, Sub70, Miura Golf, Bridgestone Golf, Honma Golf, Tour Edge |

| Customization & Pricing | Available on Request (10% Customization Free) |