Reports

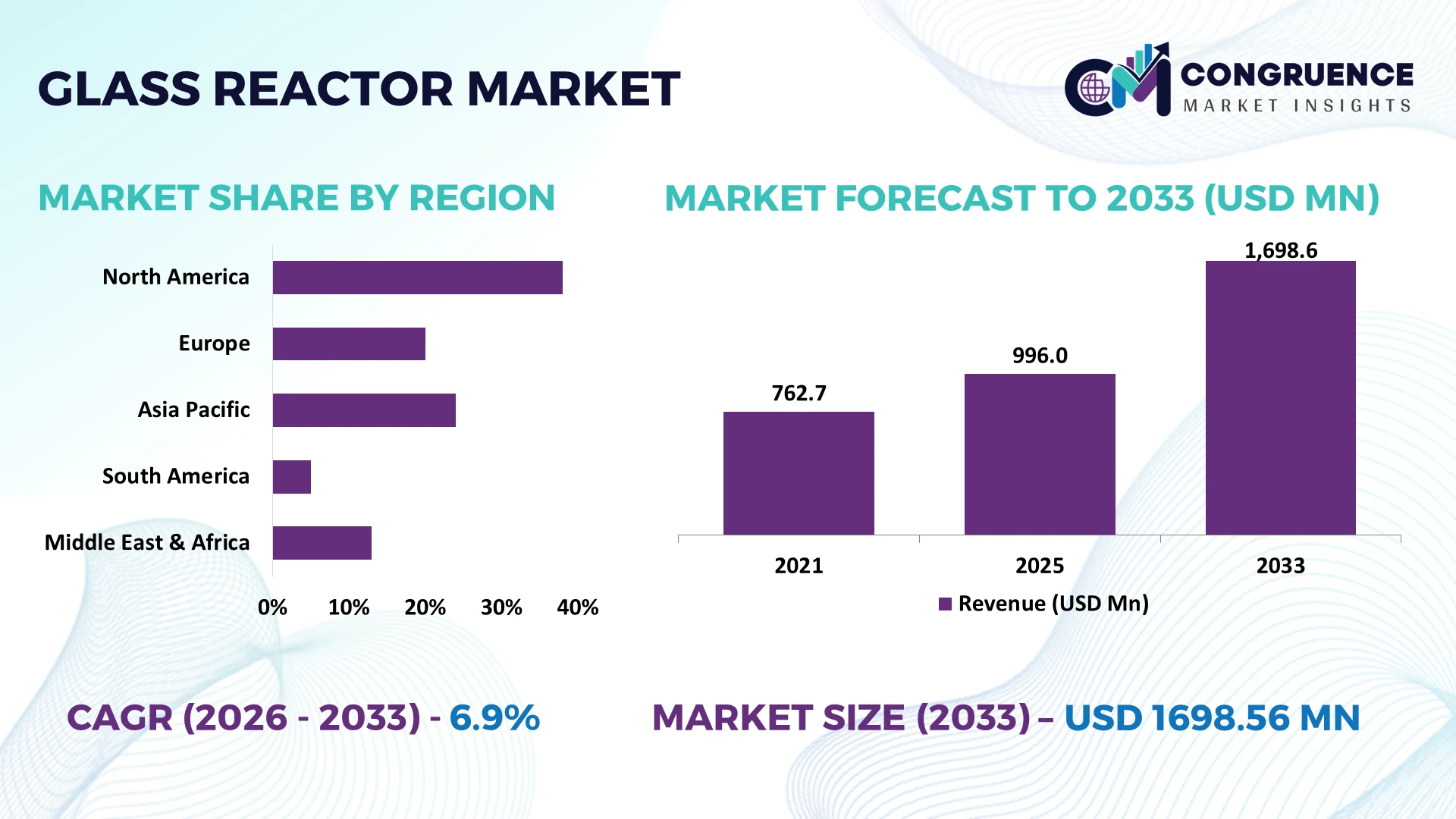

The Global Glass Reactor Market was valued at USD 996 Million in 2025 and is anticipated to reach a value of USD 1698.56 Million by 2033 expanding at a CAGR of 6.9% between 2026 and 2033. Growth is supported by expanding pharmaceutical process development, specialty chemical manufacturing, and higher adoption of corrosion-resistant laboratory and pilot-scale reaction systems with advanced digital process monitoring.

China remains the dominant manufacturing hub, accounting for approximately 38% of global glass reactor production capacity, supported by sustained investments in pharmaceutical ingredients, specialty chemicals, and laboratory equipment. Germany follows with strong engineering capabilities and higher automation adoption exceeding 70% across advanced processing facilities, while ongoing global supply-chain diversification after Red Sea shipping disruptions has accelerated regional procurement strategies and localized production investments.

Manufacturers strengthening regional production networks, automation integration, and high-performance reactor portfolios are positioned to secure long-term industrial contracts and improve operational resilience.

Market Size & Growth: USD 996 Million in 2025, reaching USD 1698.56 Million by 2033 at 6.9% CAGR, supported by advanced pharmaceutical process expansion and specialty chemical manufacturing.

Top Growth Drivers: Pharmaceutical manufacturing (+18%), specialty chemicals (+15%), and laboratory automation (+12%) continue accelerating global equipment deployment.

Short-Term Forecast: By 2028, automated reactor operations improve batch efficiency by 20% while reducing process downtime by approximately 15%.

Emerging Technologies: AI-enabled process control, automated reactor platforms, and smart sensor integration increase process consistency by nearly 25%.

Regional Leaders: Asia-Pacific exceeds USD 720 Million, Europe approaches USD 470 Million, and North America surpasses USD 360 Million through advanced manufacturing expansion and regional supply-chain localization.

Consumer/End-User Trends: More than 62% of pharmaceutical and research facilities prioritize digitally monitored glass reactor systems for improved process validation.

Pilot/Case Example: A 2026 pharmaceutical process modernization project improved reaction yield by 16% through automated temperature and pressure control integration.

Competitive Landscape: Leading manufacturers collectively control about 42% of global market activity, supported by established engineering expertise, customized systems, and strong international distribution networks.

Regulatory & ESG Impact: Energy-efficient reactor designs lower utility consumption by nearly 14%, aligning with stricter industrial sustainability and operational compliance targets.

Investment & Funding: More than USD 420 Million supports manufacturing expansion, strategic partnerships, and advanced laboratory infrastructure across high-growth industrial regions.

Innovation & Future Outlook: Digital twins, modular reactor platforms, and predictive maintenance strengthen production flexibility while supporting resilient global manufacturing expansion.

Glass reactor systems are increasingly deployed across biopharmaceutical research, specialty chemical synthesis, and pilot-scale production where precision process control is essential. Automated temperature regulation, digital monitoring, and modular vessel configurations improve operational consistency by nearly 20%. Rising localization of laboratory equipment manufacturing and stricter quality compliance standards continue reshaping procurement priorities, setting the foundation for the strategic market discussion.

Glass reactor systems have become strategically important as pharmaceutical, specialty chemical, and biotechnology manufacturers prioritize flexible batch production, faster process validation, and higher operational precision. Supply-chain restructuring following recent logistics disruptions has encouraged localized equipment manufacturing and dual-source procurement strategies, while stricter process quality requirements are accelerating investment in digitally monitored reaction systems. These shifts strengthen competitive positioning by reducing operational downtime and improving manufacturing resilience across regulated industries.

Modern automated glass reactors equipped with intelligent temperature, pressure, and data acquisition systems improve batch consistency by nearly 22% while lowering manual intervention by approximately 30% compared with conventional manually controlled reactors. Germany leads in engineering sophistication through highly automated laboratory infrastructure, whereas China maintains larger-scale production capacity supported by integrated chemical manufacturing clusters. Over the next two to three years, digital monitoring adoption across pilot and laboratory-scale reactors is expected to exceed 65%, supported by increasing process standardization and industrial automation initiatives.

A practical example is pharmaceutical process development, where modular jacketed glass reactors enable rapid formulation changes without major production interruptions, reducing changeover time by nearly 18%. Manufacturers are expanding localized assembly facilities, strengthening technology partnerships, and investing in automation-ready product portfolios to meet evolving customer requirements. Companies that integrate digital process control, engineering customization, and resilient manufacturing networks will establish stronger competitive differentiation while improving long-term operational performance.

The increasing transition toward precision pharmaceutical manufacturing and specialty chemical synthesis is reinforcing demand for advanced glass reactor systems capable of controlled batch processing. More than 60% of pilot-scale pharmaceutical development now relies on automated reaction monitoring, while digitally controlled reactors improve process reproducibility by approximately 24% and reduce batch deviations by nearly 16%. India continues expanding active pharmaceutical ingredient manufacturing capacity, increasing demand for corrosion-resistant laboratory equipment. In response, equipment manufacturers are investing in modular reactor platforms, localized engineering centers, and automation partnerships that shorten delivery timelines and strengthen customization capabilities. This structural transition enables suppliers to differentiate through application-specific engineering rather than equipment volume alone.

Volatility in borosilicate glass availability, precision instrumentation, and specialized sealing components continues affecting production planning and procurement efficiency. Lead times for selected high-performance components have remained 20–25% above historical averages, while imported instrumentation costs have increased by approximately 12% in several manufacturing markets. Germany and Japan remain critical suppliers of precision reactor components, creating dependency for many equipment manufacturers. Companies are reducing operational exposure through supplier diversification, localized component sourcing, and long-term procurement agreements. Organizations achieving higher local content are improving production continuity while protecting project margins against external supply-chain disruptions.

The integration of intelligent automation with modular glass reactor platforms creates significant opportunities beyond traditional laboratory applications. AI-assisted process optimization and predictive maintenance reduce unplanned equipment downtime by approximately 20%, while digital batch documentation improves quality compliance efficiency by nearly 28%. China continues investing in smart laboratory infrastructure, supporting wider deployment of connected process equipment across pharmaceutical and chemical facilities. Manufacturers are expanding R&D partnerships with automation specialists and software providers to develop integrated reactor ecosystems. The strongest competitive advantage increasingly comes from combining hardware performance with digital process intelligence rather than competing solely on reactor specifications.

Deploying advanced glass reactor systems across multiple manufacturing sites requires seamless integration with laboratory information systems, manufacturing execution platforms, and enterprise quality management software. Around 35% of industrial facilities continue operating mixed legacy and digital infrastructure, while workforce shortages in process automation delay implementation by nearly 18% in several developed manufacturing economies. The United States faces growing pressure to modernize laboratory infrastructure while maintaining strict regulatory compliance and cybersecurity standards. Companies must invest in workforce training, interoperable automation architecture, and standardized digital validation frameworks to ensure consistent deployment quality and sustain long-term operational competitiveness.

Smart Process Control Expansion Automated control platforms are becoming standard across pharmaceutical and specialty chemical facilities, with digital reactor monitoring adoption increasing by nearly 27% and batch documentation time declining by approximately 21%. Stricter quality compliance requirements are accelerating deployment, while manufacturers are integrating remote diagnostics and predictive maintenance into new product portfolios through technology partnerships and software-enabled equipment upgrades.

Localized Manufacturing Networks Supply-chain restructuring has encouraged companies to regionalize production, reducing average equipment delivery cycles by around 18% while increasing local component sourcing by nearly 25%. China and India continue expanding engineering capacity to support domestic demand, enabling manufacturers to improve inventory resilience, shorten customization timelines, and strengthen long-term customer contracts despite ongoing logistics volatility.

Modular Laboratory Infrastructure Pharmaceutical and biotechnology facilities are increasingly replacing fixed process equipment with modular glass reactor platforms that reduce installation time by approximately 20% and improve laboratory utilization by nearly 17%. Companies are standardizing interchangeable reactor configurations and expanding engineering collaborations to accelerate validation cycles while supporting multi-product research environments with greater operational flexibility.

Energy-Efficient Reactor Engineering Improved jacket designs, optimized heat-transfer systems, and intelligent thermal management lower process energy consumption by nearly 15% while reducing maintenance interventions by approximately 12%. Industrial sustainability initiatives and modernization programs are encouraging equipment redesign, prompting manufacturers to scale high-efficiency product lines and strengthen collaborations with automation providers to deliver lower operating costs without compromising process precision.

Jacketed glass reactors remain the leading segment, accounting for approximately 41% of overall deployment due to superior thermal control, scalable batch processing, and compatibility with pharmaceutical and specialty chemical applications. Their ability to maintain consistent reaction temperatures improves process stability while supporting automated production workflows. Pressure Rated reactors represent the fastest-growing segment as advanced chemical processing increasingly requires higher operating pressure and enhanced safety performance. Adoption of Pressure Rated systems has expanded by nearly 19% across industrial pilot facilities seeking broader process flexibility.

Single Wall reactors continue serving cost-sensitive laboratory environments where basic reaction processes dominate, while Double Wall systems provide balanced thermal efficiency for research laboratories and pilot operations. Triple Wall reactors are gaining attention in high-precision applications requiring enhanced insulation and tighter thermal consistency. Manufacturers are expanding modular product portfolios, strengthening engineering partnerships, and investing in customizable reactor platforms that address evolving industrial requirements while improving production efficiency and equipment lifecycle performance.

Pharmaceutical Research represents the largest application segment with approximately 37% of total demand, supported by continuous drug development, formulation optimization, and process validation activities. Precision temperature control, contamination resistance, and digital monitoring capabilities make glass reactors indispensable throughout laboratory and pilot-scale pharmaceutical workflows. Biotechnology Processing is the fastest-growing application, with deployment increasing by nearly 22% as biologics manufacturing, cell culture optimization, and fermentation research expand globally.

Chemical Synthesis remains a mature application supporting specialty chemicals and fine chemicals production, while Laboratory Testing continues benefiting from increasing analytical validation requirements. Material Development is strengthening as advanced materials research requires flexible reactor configurations for controlled experimentation. Equipment suppliers are responding through automation integration, modular system expansion, and customized reactor configurations that improve productivity while supporting increasingly complex research environments across industrial and institutional facilities.

The Pharmaceutical Industry remains the dominant end-user, representing approximately 39% of overall equipment demand because of intensive laboratory development, pilot production, and regulated manufacturing activities. Continuous investment in process optimization and quality assurance sustains high replacement and expansion rates. Biotechnology Companies represent the fastest-growing buyer group, with equipment deployment increasing by nearly 21% as biologics development and advanced therapeutic research continue expanding across specialized production facilities.

The Chemical Industry maintains consistent purchasing through specialty chemical manufacturing and process development, while Research Laboratories increasingly prioritize automation-ready systems to improve workflow efficiency. Academic Institutions continue modernizing laboratory infrastructure to support collaborative industrial research and advanced scientific training. Manufacturers are strengthening customer engagement through customized reactor designs, flexible service agreements, application-specific engineering support, and strategic partnerships that enhance long-term customer retention across multiple end-user segments.

Asia-Pacific accounted for the largest market share at 43% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.8% between 2026 and 2033.

Advanced Pharmaceutical Modernization Driving Equipment Upgrades

North America represents approximately 24% of the global Glass Reactor Market, supported by mature pharmaceutical manufacturing, biotechnology expansion, and advanced laboratory infrastructure. The region continues replacing conventional laboratory systems with digitally integrated glass reactors that improve process traceability and operational consistency. More than 58% of newly commissioned pharmaceutical pilot facilities now incorporate automated reaction platforms. Investment in domestic pharmaceutical manufacturing and laboratory modernization is strengthening demand for modular reactor systems with advanced temperature control and process monitoring. Equipment suppliers are expanding engineering support, application-specific customization, and lifecycle service offerings to reinforce long-term enterprise partnerships while improving deployment efficiency across regulated manufacturing environments.

United States Market Outlook: The United States remains the regional leader due to its extensive pharmaceutical R&D ecosystem, advanced biotechnology sector, and large concentration of pilot-scale manufacturing facilities. More than 65% of regional laboratory equipment investments are directed toward automation-enabled research infrastructure. Manufacturers continue strengthening local engineering capabilities, software integration, and customized reactor solutions to support increasingly complex process development and regulated production workflows.

Engineering Precision and Sustainable Manufacturing Leadership

Europe accounts for nearly 22% of global market activity through its highly specialized chemical processing, pharmaceutical engineering, and precision equipment manufacturing capabilities. Regulatory emphasis on process quality, operational safety, and energy efficiency continues encouraging replacement of legacy laboratory systems. Nearly 52% of advanced research laboratories have accelerated digital equipment modernization programs to improve experimental consistency and compliance. Equipment manufacturers are expanding modular product lines and automation integration while strengthening technical collaborations with pharmaceutical producers. Industrial modernization programs and high engineering standards continue supporting stable deployment across both commercial manufacturing and research environments.

Germany Market Outlook: Germany serves as Europe's primary engineering hub for high-performance laboratory and process equipment, supported by strong pharmaceutical, specialty chemical, and industrial automation sectors. Automated laboratory systems are deployed across more than 70% of large industrial research facilities. Domestic manufacturers continue investing in precision engineering, intelligent process control, and export-oriented production strategies that reinforce Germany's leadership in advanced reactor technologies.

Manufacturing Scale and Industrial Expansion

Asia-Pacific leads the global Glass Reactor Market with approximately 43% market share, supported by extensive pharmaceutical production, specialty chemical manufacturing, and rapidly expanding laboratory infrastructure. China and India continue increasing manufacturing capacity while improving automation across industrial research facilities. More than 38% of global glass reactor production capacity is concentrated within China, supported by integrated supply networks and engineering capabilities. Companies are expanding localized manufacturing, increasing production automation, and strengthening regional distribution networks to improve delivery performance and equipment customization for diverse industrial applications.

China Market Outlook: China remains the largest individual market due to its dominant laboratory equipment manufacturing ecosystem and extensive pharmaceutical ingredient production base. Approximately 38% of worldwide glass reactor manufacturing capacity operates within the country. Domestic producers continue expanding intelligent manufacturing facilities, investing in automated production technologies, and strengthening export competitiveness through standardized quality systems and application-focused engineering innovation.

Pharmaceutical Capacity Supporting Industrial Demand

South America represents an emerging market where pharmaceutical manufacturing, university research, and specialty chemical production continue driving equipment deployment. Brazil and neighboring countries are increasing investments in laboratory modernization to improve domestic manufacturing capability and reduce dependence on imported technologies. Automated laboratory equipment adoption has increased by approximately 17% among larger pharmaceutical facilities, while localized engineering partnerships are shortening equipment installation timelines. Although infrastructure limitations remain in selected markets, manufacturers are responding through regional service centers, technical training, and distributor expansion to improve operational reliability and customer support.

Brazil Market Outlook: Brazil leads regional demand through its expanding pharmaceutical manufacturing sector, established research institutions, and growing specialty chemical industry. Nearly 45% of South America's advanced laboratory infrastructure is concentrated within the country. Equipment suppliers are strengthening local technical support, engineering partnerships, and maintenance capabilities to improve deployment efficiency while supporting regulatory compliance across pharmaceutical and industrial applications.

Industrial Diversification and Laboratory Modernization

The Middle East & Africa market is expanding as governments diversify industrial production beyond traditional sectors while strengthening pharmaceutical manufacturing and scientific research infrastructure. Investment in laboratory modernization, industrial biotechnology, and chemical processing facilities continues increasing equipment deployment across key economies. More than 20% of newly established pharmaceutical laboratories within Gulf industrial development programs incorporate digitally monitored process equipment. International manufacturers are expanding regional partnerships, localized technical services, and engineering support to improve project execution while addressing increasing demand for high-performance laboratory systems.

Saudi Arabia Market Outlook: Saudi Arabia remains the region's most strategically significant market due to large-scale industrial diversification initiatives, pharmaceutical manufacturing investments, and expanding research infrastructure. Advanced laboratory deployment has accelerated across industrial development projects, with automation integration increasing by approximately 19% in newly commissioned facilities. Equipment suppliers continue establishing regional partnerships, technical service capabilities, and localized engineering support to strengthen long-term competitiveness and improve operational responsiveness.

The competitive landscape is led by De Dietrich Process Systems, Asahi Glassplant, Buchiglas, Chemglass Life Sciences, and Ace Glass, collectively controlling approximately 44% of global market activity. These global engineering specialists compete directly with regional manufacturers in China and India that emphasize lower production costs and faster delivery. Competition is defined by reactor customization, automation capability, thermal performance, and after-sales engineering rather than standard pricing alone. Automated reactor platforms improve laboratory productivity by nearly 22%, while modular configurations reduce installation time by approximately 18% and localized manufacturing shortens delivery cycles by almost 20%. Leading suppliers are expanding regional assembly facilities, strengthening automation partnerships, introducing digitally monitored reactor systems, and integrating component manufacturing to improve supply security. The competitive shift favors intelligent, application-specific equipment over standardized laboratory vessels as customers prioritize operational flexibility. High engineering expertise, regulatory compliance, and precision manufacturing remain major entry barriers. Sustainable success depends on combining advanced automation, customization speed, dependable supply networks, and lifecycle technical support.

De Dietrich Process Systems

Asahi Glassplant Inc.

Buchiglas AG

Chemglass Life Sciences LLC

Ace Glass Incorporated

HEL Group

Syrris Ltd.

Radleys Ltd.

Labfirst Scientific Instruments

Ablaze Glass Works

Sigma Scientific Glass

Borosil Glass Works Ltd.

Advanced automation is redefining glass reactor performance through intelligent temperature control, real-time pressure monitoring, and integrated data acquisition. More than 62% of newly installed pharmaceutical laboratory reactors now incorporate digital control platforms, improving batch consistency by approximately 23% while reducing manual intervention by nearly 28%. Remote diagnostics and automated safety interlocks enable continuous process supervision, allowing manufacturers to minimize operational interruptions and strengthen regulatory compliance across high-value research environments.

Emerging technologies include AI-assisted process optimization, predictive maintenance, digital twin simulation, and Industrial Internet of Things connectivity. Compared with conventional manually operated reactors, intelligent systems shorten process optimization cycles by approximately 20% and improve energy efficiency by nearly 15%. Pharmaceutical innovators, specialty chemical manufacturers, and contract research organizations gain the greatest competitive advantage because integrated automation accelerates validation, enhances reproducibility, and supports multi-product laboratory operations without increasing engineering complexity.

Between 2026 and 2028, modular reactor architecture combined with cloud-enabled analytics and smart sensor networks will become the preferred deployment model for advanced laboratories. Deployment of connected reactor platforms is expected to exceed 70% among newly commissioned research facilities. Companies investing early in interoperable automation ecosystems, cybersecurity-ready control systems, and software-driven process intelligence will achieve stronger operational flexibility, faster product development, and superior competitive differentiation in precision manufacturing.

June 2024 Buchiglas AG introduced the Buchi Filter Reactor system, combining reaction and filtration processes in a single vessel for pharmaceutical and chemical applications. The system supports working volumes from 10 L to 50 L, improving process efficiency by reducing transfer steps and contamination risks. Source: https://www.buchiglas.com

March 2025 De Dietrich Process Systems expanded its engineered glass-lined and glass reactor solutions for pharmaceutical manufacturing, strengthening modular process equipment capabilities. The company supports reactor configurations from laboratory scale to industrial applications, enabling faster customization and improving production flexibility for regulated industries. Source: https://www.dedietrich.com

October 2024 Chemglass Life Sciences expanded its laboratory and pilot-scale reactor portfolio with advanced jacketed glass reactor systems designed for chemical synthesis and process development. The product range supports reactor capacities up to 150 L, helping research organizations improve scalability from laboratory experimentation to pilot production. Source: https://www.chemglass.com

February 2026 HEL Group strengthened its automated reactor technology portfolio with advanced process control solutions integrating real-time monitoring and reaction optimization features. The systems improve experimental efficiency by approximately 25% through automated control workflows, supporting pharmaceutical and chemical companies seeking faster development cycles. Source: https://helgroup.com

This report provides a comprehensive analysis of the Glass Reactor Market covering product types, applications, end-users, regional trends, technology adoption, and competitive strategies. The study includes Single Wall, Double Wall, Triple Wall, Jacketed, and Pressure Rated reactors used across chemical synthesis, pharmaceutical research, laboratory testing, biotechnology processing, and material development. It evaluates demand patterns among chemical manufacturers, pharmaceutical companies, biotechnology organizations, research laboratories, and academic institutions.

The report examines automation integration, digital monitoring, modular reactor designs, advanced material engineering, and supply-chain developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. Strategic insights support investment planning, product innovation, expansion strategies, partnership decisions, and competitive positioning while identifying emerging opportunities influencing market direction between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 996 Million |

Market Revenue in 2033 | USD 1698.56 Million |

CAGR (2026 - 2033) | 6.9% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | De Dietrich Process Systems, Asahi Glassplant Inc., Buchiglas AG, Chemglass Life Sciences LLC, Ace Glass Incorporated, HEL Group, Syrris Ltd., Radleys Ltd., Labfirst Scientific Instruments, Ablaze Glass Works, Sigma Scientific Glass, Borosil Glass Works Ltd. |

Customization & Pricing | Available on Request (10% Customization is Free) |