Reports

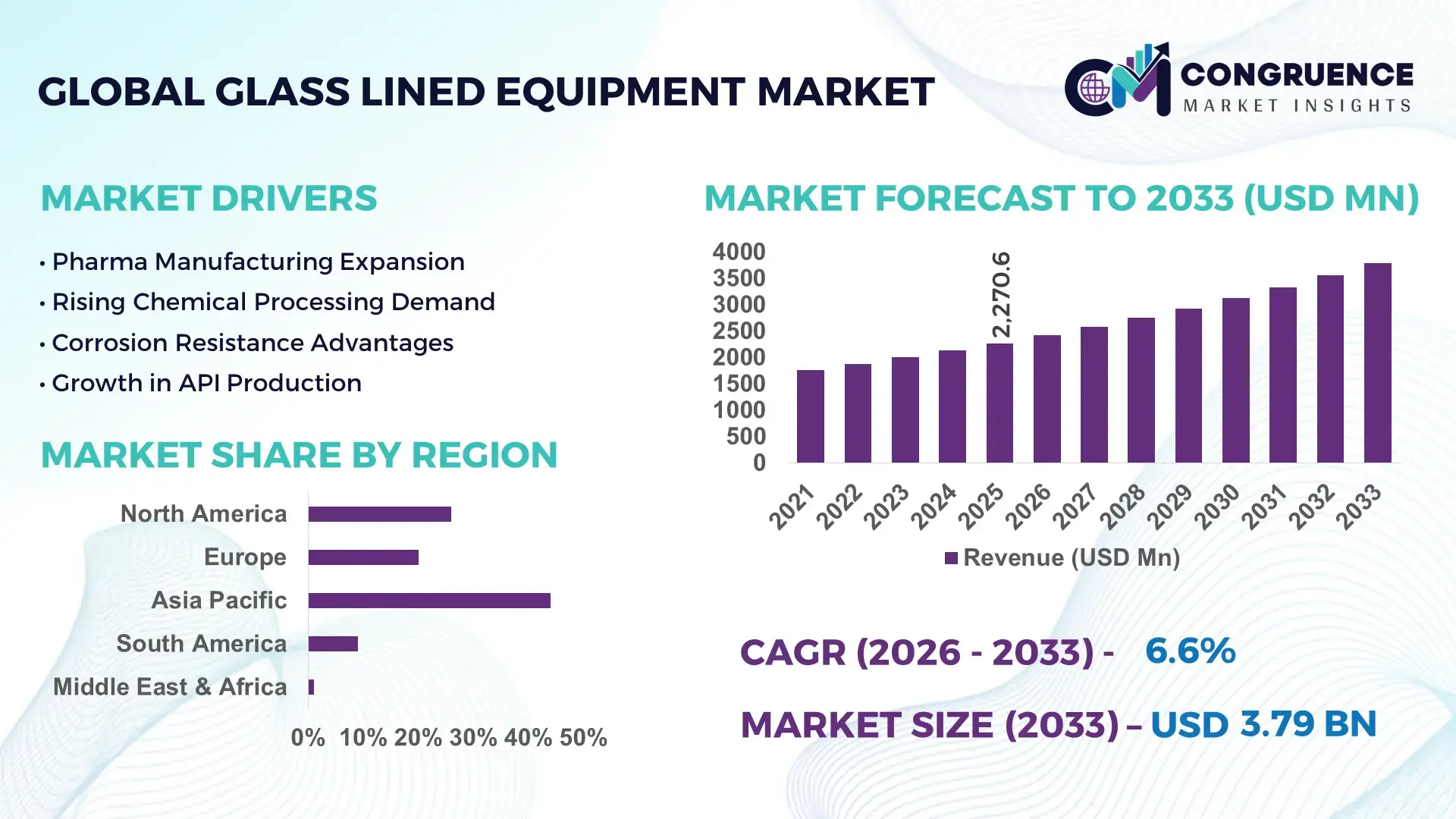

The Global Glass Lined Equipment Market was valued at USD 2270.58 Million in 2025 and is anticipated to reach a value of USD 3786.12 Million by 2033 expanding at a CAGR of 6.6% between 2026 and 2033. Rising investments in high-purity pharmaceutical processing, corrosion-resistant chemical manufacturing, and automated reactor systems accelerated adoption of advanced glass lined reactors and storage vessels, with production efficiency improvements exceeding 18% compared to conventional alloy-based systems.

China maintained the dominant position in the global glass lined equipment industry with more than 34% manufacturing share in 2026, supported by large-scale chemical processing clusters, pharmaceutical API expansion, and government-backed industrial modernization programs exceeding USD 4 billion. India strengthened its position through rapid specialty chemical capacity additions and over 15% annual expansion in pharmaceutical reactor installations, while Germany led premium engineering adoption with high-automation glass lining technologies improving equipment lifecycle performance by nearly 20% versus conventional systems. Compared with stainless steel processing units, advanced glass lined systems delivered superior corrosion resistance and lower contamination rates in high-acid applications.

Market Size & Growth: USD 2270.58 million in 2025 reaching USD 3786.12 million by 2033, driven by pharmaceutical reactor expansion and corrosion-resistant process modernization at 6.6% CAGR.

Top Growth Drivers: Specialty chemicals contributed 31% demand growth, pharmaceutical APIs 28%, and automated processing upgrades improved equipment utilization by 19%.

Short-Term Forecast: By 2027, smart monitoring integration reduces unplanned maintenance costs by 14% while operational efficiency improves by 17%.

Emerging Technologies: AI-enabled predictive maintenance, robotic glass coating systems, and hybrid enamel technologies improve durability by 22% and inspection accuracy by 30%.

Regional Leaders: Asia-Pacific surpasses USD 1.7 billion led by chemical capacity expansion, Europe exceeds USD 920 million through ESG-driven retrofits, and North America crosses USD 640 million with biotech processing adoption.

Consumer/End-User Trends: Over 61% of pharmaceutical manufacturers prioritize contamination-free glass lined reactors for high-purity batch production environments.

Pilot/Case Example: In 2025, a large specialty chemical facility upgraded automated glass lined reactors, reducing corrosion-related shutdowns by 26% and process losses by 11%.

Competitive Landscape: Top manufacturers collectively control nearly 42% market share, with leading competition centered on advanced reactor engineering and export-focused expansion.

Regulatory & ESG Impact: Industrial emission compliance programs lowered hazardous waste exposure risks by 16% while energy-efficient coating processes reduced thermal losses by 13%.

Investment & Funding: More than USD 1.2 billion in industrial expansion investments targeted localized production hubs amid global supply chain restructuring between 2024 and 2026.

Innovation & Future Outlook: Next-generation nano-coated glass lining and digital twin-enabled maintenance systems accelerate lifecycle optimization and strengthen high-growth industrial automation strategies.

Pharmaceutical manufacturing accounted for nearly 38% of total industry demand, followed by specialty chemicals at 33% and food-grade processing applications exceeding 11%. Advanced enamel coating technologies improved corrosion durability by over 20%, while automated inspection systems reduced maintenance intervals by 15%. Asia-Pacific remained the strongest demand center due to rapid chemical infrastructure expansion, whereas Europe accelerated replacement demand under stricter industrial compliance standards. Growing adoption of digital monitoring platforms and localized manufacturing strategies signals a transition toward smarter, lower-risk processing ecosystems through 2030.

Glass lined equipment is transforming from a niche industrial asset into a strategic infrastructure category for pharmaceutical, specialty chemical, and high-purity processing industries. Accelerating demand for contamination-free production, combined with stricter industrial compliance standards, is forcing manufacturers to replace conventional alloy-based systems with advanced corrosion-resistant reactors and storage solutions. Between 2024 and 2026, supply chain regionalization and export-control pressures reshaped procurement strategies, pushing over 32% of global chemical processors toward localized equipment sourcing and automated production ecosystems. AI-enabled predictive maintenance platforms are optimizing equipment lifecycle performance while reducing unscheduled shutdown frequency across high-volume process industries.

Advanced robotic glass-lining technology improves coating precision by 27% while reducing operational costs by 18% compared to legacy manual enamel systems. Asia-Pacific leads in production volume with more than 46% manufacturing concentration, while Europe leads in innovation adoption with nearly 39% penetration of digitally monitored reactor systems focused on ESG-driven operational compliance. Over the next three years, smart reactor integration is projected to increase maintenance efficiency by 21% and reduce inspection cycles by 16%. Manufacturers implementing energy-efficient furnace systems are also lowering thermal energy consumption by 14%, creating a measurable compliance and cost advantage in emission-regulated industries.

In 2025, a major pharmaceutical processing facility upgraded automated glass lined reactors and improved batch consistency by 24% while cutting contamination incidents by 19%. Global manufacturers are accelerating capital allocation toward regional production hubs, digital inspection platforms, and nano-coated lining technologies to strengthen delivery resilience and margin stability. The competitive advantage is rapidly shifting toward companies capable of integrating automation, material science innovation, and localized manufacturing agility into scalable industrial process solutions.

Rapid expansion in pharmaceutical APIs, specialty chemicals, and agrochemical processing is accelerating demand for corrosion-resistant glass lined reactors and storage systems. More than 41% of new pharmaceutical production lines commissioned in 2025 integrated automated glass lined equipment to reduce contamination risks and improve process consistency. Simultaneously, global chemical producers reported nearly 18% lower maintenance frequency after replacing legacy alloy reactors with advanced enamel-coated systems. Supply chain restructuring across Asia and Europe, intensified by geopolitical trade disruptions, forced manufacturers to localize critical equipment sourcing and expand production capacity closer to industrial clusters. In response, equipment suppliers are accelerating strategic partnerships, expanding furnace automation investments, and scaling digitally monitored reactor manufacturing to secure long-term contracts in regulated, high-value processing sectors.

Volatility in borosilicate glass compounds, nickel-based alloys, and industrial energy costs is constraining production scalability across the global glass lined equipment industry. Between 2024 and 2026, specialized coating material prices increased by nearly 22%, while furnace-related operating expenses rose over 17% due to energy market instability. Manufacturing concentration in limited industrial regions created extended lead times exceeding 20 weeks for high-capacity reactors, disrupting pharmaceutical and chemical expansion timelines. These constraints directly increased procurement costs and delayed facility commissioning schedules across emerging markets. To reduce exposure, manufacturers are diversifying supplier networks, securing long-term raw material agreements, and investing in modular reactor production systems. Several companies are also accelerating hybrid coating research to reduce dependency on high-cost imported material inputs.

Digital manufacturing integration and next-generation coating technologies are reshaping future growth pathways in the glass lined equipment market. Smart reactor systems equipped with AI-driven monitoring platforms improved predictive maintenance accuracy by 29% and reduced equipment downtime by nearly 18% across pharmaceutical processing facilities. Emerging markets in Southeast Asia and the Middle East are expanding specialty chemical infrastructure at over 14% annually, creating new demand pockets for localized reactor manufacturing. A major innovation shift toward nano-engineered glass coatings is extending equipment lifecycle performance by nearly 25% compared to traditional enamel technologies. Manufacturers are positioning for future dominance through dedicated R&D centers, regional expansion strategies, and integrated service ecosystems combining digital diagnostics, automation support, and long-term process optimization contracts for industrial clients.

Scaling advanced glass lined equipment production while maintaining coating precision, delivery speed, and regulatory compliance remains a major execution challenge. Nearly 16% of industrial reactor failures reported in 2025 were linked to coating inconsistencies or thermal stress defects during high-volume processing operations. At the same time, skilled labor shortages across industrial engineering sectors reduced specialized glass lining workforce availability by over 13%, slowing installation and inspection cycles. Rising industrial decarbonization mandates are also forcing manufacturers to modernize furnace infrastructure, increasing near-term capital expenditure pressure. These operational barriers are constraining production consistency and limiting expansion efficiency in fast-growing chemical markets. To remain competitive, companies must accelerate automation investment, strengthen technical training ecosystems, and establish regional engineering partnerships capable of supporting scalable, high-precision manufacturing execution.

AI-driven monitoring adoption increased 31% across industrial reactor systems in 2025, reshaping maintenance execution. Manufacturers are deploying predictive diagnostics and sensor-enabled inspection platforms to reduce unplanned shutdowns by 18% and shorten maintenance cycles by 14%. Pharmaceutical processors accelerated digital reactor monitoring after stricter contamination compliance audits in Europe and Asia. Equipment suppliers are responding through software partnerships, integrated service contracts, and centralized monitoring hubs that optimize asset utilization across multi-site operations.

Localized manufacturing expansion rose 27% as supply chain disruptions forced regional production restructuring. Chemical and pharmaceutical companies shifted procurement toward domestic and nearshore suppliers to reduce delivery delays by nearly 22% and logistics costs by 11%. India and Southeast Asia recorded faster deployment of modular glass lined systems due to shorter installation timelines and lower import dependency. Manufacturers are expanding regional fabrication facilities and restructuring supplier networks to secure faster industrial delivery commitments.

Automated glass-lining processes improved coating precision by 24%, redefining operational consistency standards. Robotic enamel application systems reduced coating defects by 16% while improving batch-level production speed by 19% compared to manual processing methods. Labor shortages in specialized industrial engineering accelerated automation deployment across high-volume manufacturing facilities. Companies are scaling furnace automation and digital quality inspection systems to improve consistency in corrosion-sensitive applications.

Service-based equipment contracts expanded 21%, shifting the market beyond one-time equipment sales. Industrial buyers increasingly prefer lifecycle-based agreements covering predictive maintenance, digital inspections, and performance optimization services. This transition reduced emergency repair costs by 13% and improved equipment uptime by 17% across continuous processing environments. A non-obvious shift emerged as mid-sized manufacturers adopted subscription-style technical support models to compete with larger engineering firms while preserving long-term customer retention.

The glass lined equipment market is segmented by type, application, and end-user, with reactors dominating demand due to widespread deployment in pharmaceutical and chemical processing operations. Chemical processing accounted for nearly 35% of application demand, while pharmaceutical manufacturing contributed over 29% driven by contamination-control requirements and high-purity production standards. Demand is shifting toward automated reactors, advanced agitators, and digitally monitored systems as manufacturers prioritize efficiency and maintenance optimization. Among end-users, the chemical industry maintained the largest share, while water treatment and food processing sectors recorded faster adoption of corrosion-resistant systems due to tightening environmental compliance and operational reliability requirements.

Reactors dominated the glass lined equipment market with nearly 44% share due to their critical role in high-pressure chemical synthesis, pharmaceutical batch processing, and contamination-sensitive industrial applications. Their structural dominance is driven by superior corrosion resistance, scalable production compatibility, and integration with automated monitoring systems that improved process consistency by 21% across large-scale facilities. Storage tanks remained the second-largest segment because of growing demand for secure handling of aggressive chemicals and intermediates, particularly in export-oriented manufacturing hubs. However, heat exchangers emerged as the fastest-growing type with deployment expansion exceeding 16% as industries intensified focus on thermal efficiency optimization and energy reduction initiatives. Compared with traditional storage-focused systems, advanced heat exchangers reduced process energy losses by nearly 14% in continuous manufacturing environments.

Columns, agitators, and auxiliary glass lined systems collectively accounted for approximately 29% market share, serving niche but strategically important functions in material separation, reaction uniformity, and high-viscosity processing operations. Companies are increasingly prioritizing modular reactor production, automated agitator systems, and integrated thermal management technologies to capture higher-margin industrial contracts. Investment focus is rapidly shifting toward digitally enabled reactors and energy-efficient heat exchange infrastructure, while conventional standalone vessel demand is stabilizing in mature industrial markets.

Chemical processing remained the leading application segment with nearly 35% share, supported by intensive use of corrosion-resistant reactors, storage systems, and thermal processing equipment across specialty chemicals, industrial intermediates, and agrochemical manufacturing. Usage concentration exists because glass lined systems significantly reduce contamination risks and maintenance frequency in highly acidic production environments. Pharmaceutical manufacturing emerged as the fastest-growing application, expanding by more than 18% due to stricter purity regulations, biologics production growth, and increasing deployment of automated batch processing systems. Compared with mature chemical processing operations, pharmaceutical facilities are adopting digitally monitored reactors at a faster pace to improve traceability and reduce validation downtime by approximately 16%.

Food processing, corrosive material handling, industrial mixing, and waste treatment collectively represented nearly 41% of market demand, with waste treatment gaining stronger traction due to industrial discharge compliance reforms and rising hazardous material handling requirements. Companies are repositioning product portfolios toward high-purity pharmaceutical systems, modular chemical reactors, and energy-efficient mixing technologies to capture evolving operational demand. Industrial buyers increasingly prioritize low-maintenance equipment with integrated monitoring capabilities, reshaping deployment strategies across contamination-sensitive applications.

The chemical industry led the glass lined equipment market with approximately 38% demand share due to continuous reliance on corrosion-resistant processing systems for acids, solvents, and high-reactivity compounds. Demand concentration remains high because chemical manufacturers operate large-scale batch and continuous processing facilities requiring durable reactor infrastructure and low contamination risk. The pharmaceutical industry represented the fastest-growing end-user segment with adoption growth exceeding 17%, fueled by biologics expansion, sterile manufacturing requirements, and regulatory pressure for high-purity production systems. Compared with the established chemical sector, pharmaceutical buyers increasingly prioritize digitally integrated and validation-ready reactor systems to improve process traceability and reduce operational interruptions by nearly 15%.

Food and beverage, petrochemical industry, water treatment, and industrial manufacturing collectively contributed around 43% of overall demand, with water treatment facilities recording stronger adoption of glass lined storage systems under tightening environmental discharge regulations. Procurement behavior is shifting toward customized reactor configurations, predictive maintenance support, and long-term technical service agreements. Manufacturers are targeting these end-users through regional partnerships, application-specific engineering solutions, and lifecycle-based pricing models designed to strengthen customer retention and operational reliability across industrial processing environments.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Asia-Pacific dominated global production and industrial deployment due to large-scale pharmaceutical and specialty chemical manufacturing expansion across China and India, with over 52% of newly installed reactors concentrated in the region. Europe captured nearly 24% share through high adoption of automated and ESG-compliant processing systems, leading in digital reactor monitoring and energy-efficient glass lining technologies. North America contributed approximately 21% demand share, driven by contamination-control upgrades and advanced pharmaceutical processing infrastructure. Meanwhile, Middle East & Africa accelerated infrastructure-led demand as industrial diversification and refinery modernization projects increased corrosion-resistant equipment deployment. Supply chain regionalization and stricter industrial compliance standards are forcing manufacturers to prioritize localized production, automation investment, and regional engineering partnerships globally.

North America accounted for nearly 21% of global glass lined equipment demand in 2025, supported by strong pharmaceutical processing, specialty chemical manufacturing, and industrial modernization initiatives. The United States dominated regional deployment as over 58% of pharmaceutical production facilities accelerated replacement of aging alloy-based reactors with contamination-resistant glass lined systems. Stricter FDA compliance requirements and rising maintenance costs are forcing manufacturers toward digitally monitored equipment platforms that reduced operational downtime by approximately 15%. Companies are increasingly investing in predictive maintenance integration and automated inspection technologies, while regional suppliers expanded localized fabrication capacity by over 12% to improve delivery speed. Enterprise buyers prioritize lifecycle efficiency, regulatory reliability, and rapid technical support, making North America a strategic region for premium engineered equipment expansion.

Europe represented approximately 24% of the global glass lined equipment market, led by Germany, France, and Italy through advanced pharmaceutical and specialty chemical manufacturing ecosystems. Tightening industrial emission standards and ESG-focused production mandates are reshaping procurement priorities, with nearly 37% of newly installed systems incorporating energy-efficient furnace technologies and automated monitoring platforms. Regional manufacturers reduced process-related thermal losses by around 13% through advanced enamel engineering and digitally optimized reactor operations. Compliance-driven enterprises increasingly favor high-durability, low-maintenance equipment capable of supporting long-cycle industrial operations under strict environmental regulations. Strategic investment is shifting toward smart reactor systems, localized engineering support, and sustainable coating technologies, forcing suppliers to innovate rapidly to maintain competitiveness across Europe’s quality-first industrial landscape.

Asia-Pacific led the global glass lined equipment market with nearly 46% share in 2025, supported by aggressive pharmaceutical, agrochemical, and specialty chemical manufacturing expansion across China and India. More than 55% of newly commissioned glass lined reactors in 2025 were installed within regional industrial clusters focused on export-oriented production. Strong supply chain integration, lower fabrication costs, and faster delivery cycles improved regional manufacturing competitiveness by approximately 19% compared to Western markets. Companies accelerated localized production strategies, while digital inspection systems and automated enamel technologies gained rapid deployment across high-volume manufacturing facilities. Industrial buyers prioritize scale, operational speed, and cost efficiency, prompting suppliers to expand modular reactor manufacturing capacity and strengthen regional engineering partnerships to capture accelerating industrial infrastructure demand.

South America accounted for nearly 6% of global glass lined equipment demand, with Brazil and Argentina leading adoption across chemical processing and industrial manufacturing sectors. Expansion in agrochemical production and industrial waste treatment infrastructure increased deployment of corrosion-resistant reactor systems by approximately 11% during 2025. However, import dependency and fluctuating industrial investment cycles continue constraining large-scale equipment procurement and extending delivery timelines. Regional enterprises increasingly shifted toward modular and lower-maintenance glass lined systems to optimize operational costs and reduce maintenance interruptions by nearly 9%. Suppliers are responding through localized distributor partnerships and application-specific engineering solutions tailored to mid-sized industrial operators. The region presents strong long-term industrial modernization potential, although infrastructure limitations and cost sensitivity continue shaping purchasing decisions and expansion speed.

Middle East & Africa contributed approximately 3% of global glass lined equipment demand, led by Saudi Arabia, the UAE, and South Africa through refinery modernization and chemical infrastructure expansion programs. Industrial diversification strategies and downstream petrochemical investments increased deployment of corrosion-resistant processing systems by nearly 14% in 2025. Governments and private operators accelerated partnerships for specialty chemical manufacturing and industrial water treatment projects, while automated reactor monitoring adoption improved maintenance efficiency by approximately 12%. Enterprises increasingly prioritize long-lifecycle equipment capable of operating under high-temperature and corrosive processing conditions with reduced operational risk. Suppliers are expanding regional service capabilities and technical support networks, positioning the region as an emerging strategic market for infrastructure-driven industrial transformation and long-term process manufacturing growth.

China – 34% market share: China dominates the Glass Lined Equipment market through massive specialty chemical production capacity, integrated manufacturing ecosystems, and rapid industrial infrastructure expansion.

United States – 18% market share: The United States leads high-value Glass Lined Equipment demand due to advanced pharmaceutical manufacturing, strict contamination-control standards, and strong adoption of automated processing systems.

The glass lined equipment market is dominated by global engineering leaders including De Dietrich Process Systems, Pfaudler, THALETEC, HLE Glascoat, and GMM Pfaudler, competing directly against regional fabricators and cost-focused Asian manufacturers. The top five players collectively controlled nearly 48% market share in 2025, with competition centered on coating durability, delivery speed, automation integration, and lifecycle maintenance capability. Premium suppliers improved reactor efficiency by 20% through advanced enamel engineering, while low-cost regional manufacturers reduced procurement costs by nearly 15% through localized sourcing and modular production. Companies are aggressively expanding regional fabrication hubs, forming technical service partnerships, and integrating predictive maintenance platforms to strengthen industrial retention rates. Market competition is shifting toward digitally enabled process systems and vertically integrated manufacturing control as supply chain volatility intensifies. High furnace investment requirements, specialized labor dependency, and compliance certification barriers continue limiting new entrants. Winning requires precision engineering, scalable regional operations, and integrated digital service ecosystems.

De Dietrich Process Systems

GMM Pfaudler

THALETEC GmbH

HLE Glascoat Limited

Buchiglas

Zibo Taiji Industrial Enamel Co., Ltd.

Standard Glass Lining Technology Limited

DINEX Ecotech

Sigma Scientific Glass Pvt. Ltd.

Glasscoat International

Yoshitake Inc.

Swiss Glascoat Equipments Limited

3V Tech

Advanced glass lining technologies integrated with AI-enabled monitoring platforms are reshaping industrial reactor performance across pharmaceutical and specialty chemical processing. More than 42% of newly installed glass lined reactors in 2026 incorporated predictive maintenance sensors that reduced unplanned downtime by 18% and improved maintenance scheduling accuracy by 24%. Automated inspection systems using thermal imaging and digital diagnostics are also optimizing coating integrity verification, lowering defect-related maintenance costs by nearly 15%. Companies deploying these systems are strengthening operational reliability while securing faster compliance validation in contamination-sensitive production environments.

Emerging technologies such as robotic enamel coating and nano-engineered glass surfaces are accelerating manufacturing precision and lifecycle durability. Robotic glass-lining systems improved coating consistency by 27% while reducing processing waste by 13% compared to legacy manual enamel application methods. Nearly 36% of premium reactor manufacturers adopted digitally controlled furnace technologies to improve thermal efficiency and shorten production cycles. Suppliers focusing on high-purity pharmaceutical and biotech applications are gaining competitive advantage through advanced cleanability, lower corrosion rates, and faster reactor turnaround capabilities.

Disruptive hybrid technologies combining silicon carbide heat transfer systems with smart glass-lined reactors are redefining industrial process optimization between 2026 and 2028. New-generation heat exchange systems improved thermal conductivity efficiency by 25% compared to conventional glass-lined configurations while reducing energy consumption by approximately 14%. Integrated digital twin platforms are also accelerating remote diagnostics and lifecycle analytics across multi-site manufacturing operations. Companies investing early in intelligent reactor ecosystems, automation-led coating infrastructure, and modular process integration are positioning themselves to capture high-value industrial contracts as operational efficiency increasingly defines competitive leadership.

March 2026 – GMM Pfaudler expanded advanced glass-lined manufacturing operations through enhanced automation integration across multiple production facilities, increasing fabrication throughput by nearly 18% and improving delivery efficiency for pharmaceutical and specialty chemical clients. The move strengthened regional supply resilience and accelerated export-oriented production scalability. [Automation Scale-Up] Source: GMM Pfaudler

October 2025 – De Dietrich Process Systems strengthened deployment of OptiMix reactor technology featuring integrated wall-baffle systems that improved heat transfer performance by up to 25% compared to conventional reactor configurations. The innovation accelerated adoption in high-purity chemical processing and optimized operational cleanability for regulated pharmaceutical environments. [Thermal Efficiency Shift] Source: De Dietrich Process Systems

July 2025 – THALETEC advanced deployment of abrasion-resistant glass lining solutions across corrosive industrial applications, supporting extended reactor lifecycle performance and reducing maintenance intervention frequency by approximately 20%. The technology upgrade improved operational continuity for heavy chemical processing operators facing rising durability and compliance requirements. [Durability Enhancement Drive] Source: LPP Group THALETEC Solutions

May 2024 – Pfaudler accelerated adoption of silicon carbide-enabled heat exchanger systems within glass-lined processing infrastructure, improving thermal transfer efficiency and reducing process energy consumption by nearly 14%. The deployment strengthened competitive positioning in energy-intensive chemical manufacturing and reinforced demand for hybrid corrosion-resistant process technologies. [Hybrid Process Integration] Source: Pfaudler Technologies

The Glass Lined Equipment Market report delivers comprehensive analysis across key product categories including reactors, storage tanks, heat exchangers, columns, and agitators, while evaluating major applications such as chemical processing, pharmaceutical manufacturing, industrial mixing, waste treatment, and corrosive material handling. The study covers six core end-user industries and assesses regional performance across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. More than 45% of evaluated installations were concentrated in pharmaceutical and specialty chemical operations, reflecting the increasing importance of contamination-resistant processing systems and automated reactor technologies.

The report analyzes over 12 major industry participants and tracks operational shifts including AI-enabled maintenance adoption, robotic glass-lining deployment, nano-engineered coating innovation, and silicon carbide heat transfer integration. Nearly 38% of manufacturers assessed are transitioning toward digitally monitored reactor infrastructure, while advanced automated coating systems improved production precision by over 20% across high-volume manufacturing facilities. The report also evaluates future-facing trends between 2026 and 2033, including modular reactor ecosystems, localized manufacturing strategies, and lifecycle-based service models. Strategic insights support investment prioritization, regional expansion planning, supplier benchmarking, technology positioning, and competitive differentiation for decision-makers operating within high-purity industrial processing markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 2270.58 Million |

|

Market Revenue in 2033 |

USD 3786.12 Million |

|

CAGR (2026 - 2033) |

6.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

De Dietrich Process Systems, GMM Pfaudler, THALETEC GmbH, HLE Glascoat Limited, Buchiglas, Zibo Taiji Industrial Enamel Co., Ltd., Standard Glass Lining Technology Limited, DINEX Ecotech, Sigma Scientific Glass Pvt. Ltd., Glasscoat International, Yoshitake Inc., Swiss Glascoat Equipments Limited, 3V Tech |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |