Reports

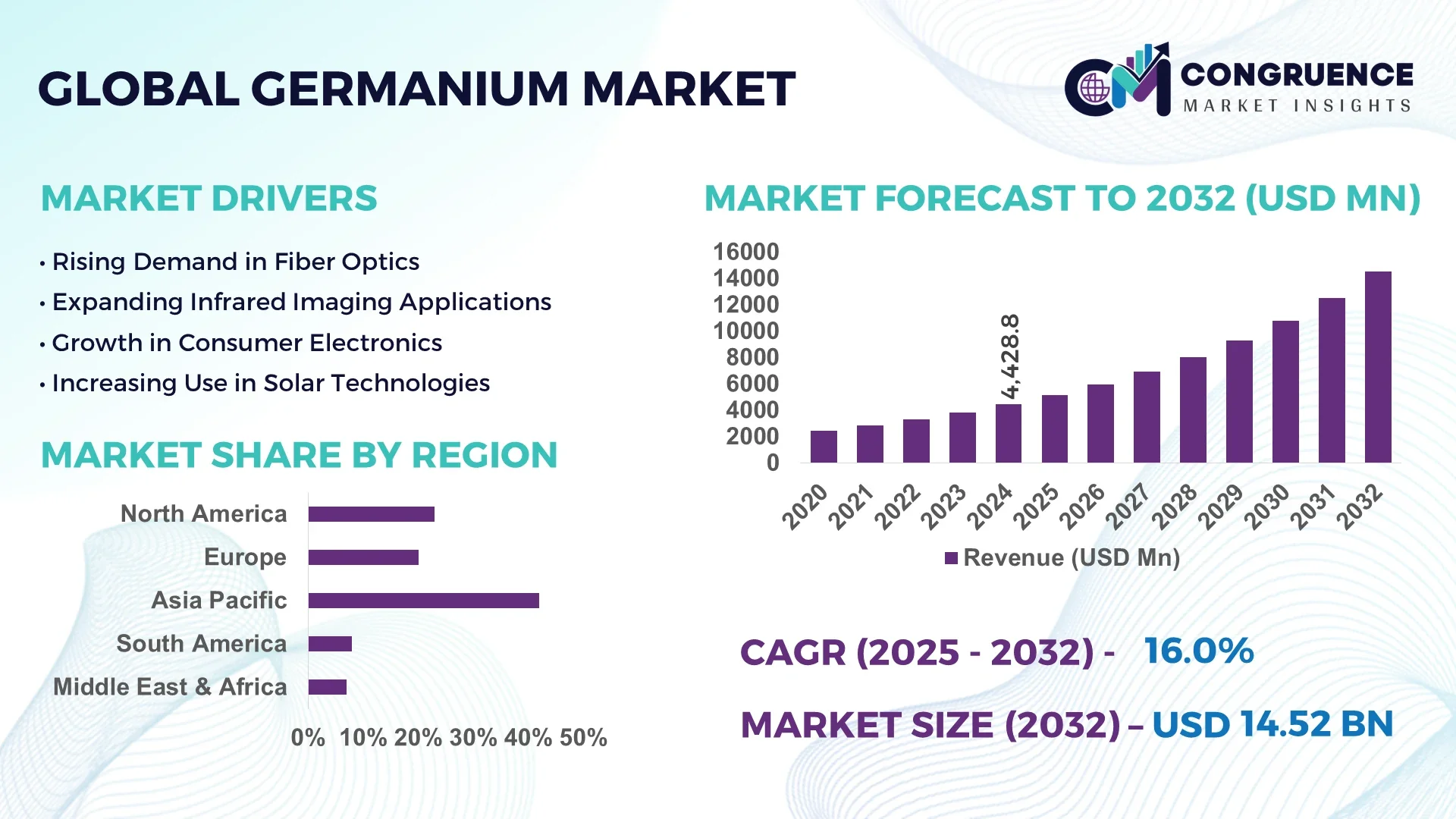

The Global Germanium Market was valued at USD 4428.75 Million in 2024 and is anticipated to reach a value of USD 14519.28 Million by 2032 expanding at a CAGR of 16% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

China leads the global Germanium market with significant production capacity driven by substantial investments in refining technologies and advanced extraction processes. The country has rapidly expanded its Germanium production facilities, focusing heavily on semiconductor applications and fiber optics manufacturing, supported by ongoing government incentives and industry collaborations.

The Germanium market is crucial across multiple high-tech sectors including electronics, telecommunications, and solar energy, where its unique semiconductor properties enable superior performance. Recent innovations in purification techniques and crystal growth have enhanced product quality, enabling new applications in infrared optics and 5G technology infrastructure. Regulatory emphasis on sustainable mining and environmentally friendly processing methods is influencing market dynamics, encouraging companies to adopt green technologies. Regional consumption trends indicate increasing demand in Asia-Pacific due to expanding electronics manufacturing hubs, while North America and Europe focus on research-driven applications. Emerging trends such as integration with quantum computing and advanced photonics point to a robust future outlook, highlighting Germanium’s pivotal role in next-generation technologies.

Artificial Intelligence (AI) is revolutionizing the Germanium Market by significantly enhancing operational efficiency and precision in both extraction and processing stages. AI-powered predictive analytics are being utilized to optimize mining operations, improving yield and reducing waste by accurately forecasting ore quality and extraction rates. Automation integrated with AI enables real-time monitoring of refining processes, ensuring consistency and higher purity levels of Germanium products. The Germanium Market benefits from AI-enabled supply chain management systems that improve inventory control, reduce downtime, and streamline logistics, leading to cost reductions and faster delivery timelines.

Furthermore, AI-driven material science simulations accelerate the development of novel Germanium-based compounds with enhanced optical and electronic properties. This technological advancement supports the Germanium Market’s expansion into cutting-edge applications like high-speed fiber optics and infrared sensors. Machine learning algorithms analyze vast datasets from manufacturing processes to identify defects early, improving product reliability and reducing rework costs. AI is also instrumental in regulatory compliance by automating environmental impact assessments and ensuring adherence to evolving standards. Overall, AI integration is driving the Germanium Market towards more intelligent, sustainable, and innovative practices, positioning industry players to meet rising global demand with improved quality and efficiency.

“In 2024, a major semiconductor manufacturer deployed an AI-driven process optimization platform in its Germanium refining operations, resulting in a 12% increase in product purity and a 15% reduction in energy consumption within six months.”

The Germanium Market benefits substantially from growing demand in telecommunications and electronics industries, where Germanium’s superior optical and semiconductor properties are critical. The widespread adoption of 5G networks fuels the need for high-performance fiber optic components, increasing Germanium usage in optical fibers and infrared optics. Additionally, the electronics sector’s reliance on Germanium for manufacturing high-speed transistors and photodetectors supports market expansion. Investment in advanced Germanium-based devices by technology firms highlights this driver’s importance, as industries seek to enhance device efficiency and miniaturization. The increasing rollout of smart technologies globally reinforces this trend, creating sustained demand growth across diverse applications.

A key restraint in the Germanium Market is the scarcity of naturally occurring, high-purity Germanium ore, which limits raw material supply. Germanium is often produced as a byproduct during zinc ore processing, causing dependency on fluctuating zinc mining activities. This supply constraint leads to price volatility and challenges in meeting growing industrial demand. Additionally, the complex and costly refining processes required to obtain pure Germanium increase production expenses, further restricting market expansion. Environmental regulations surrounding mining activities add operational burdens and compliance costs, contributing to supply-side limitations. These factors collectively impose constraints on the Germanium Market’s scalability and long-term supply security.

The Germanium Market holds significant opportunity through expanding use in renewable energy and quantum computing technologies. Germanium-based photovoltaic cells exhibit higher efficiency in solar panels, attracting interest from clean energy initiatives worldwide. As governments and industries prioritize sustainability, demand for Germanium in solar technology is expected to rise, opening new avenues for market growth. Moreover, the material’s exceptional electronic properties position it as a critical component in quantum computing hardware development. Investment in research and development for quantum devices enhances Germanium’s role beyond traditional sectors, signaling untapped potential. These opportunities encourage innovation and strategic partnerships within the Germanium Market landscape.

The Germanium Market faces significant challenges from elevated production costs and complex regulatory compliance requirements. Extracting and refining Germanium demand sophisticated technology and energy-intensive processes, increasing operational expenses. These high costs limit price competitiveness, particularly against alternative semiconductor materials. Additionally, stringent environmental regulations governing mining and chemical processing impose rigorous compliance obligations, increasing administrative and operational overheads. Variations in regional regulatory frameworks further complicate market entry and expansion for manufacturers. These challenges require companies to invest heavily in sustainable technologies and risk management strategies, posing barriers to rapid market scaling and innovation within the Germanium Market.

• Growth in High-Purity Germanium Applications: The Germanium market is witnessing increased demand for high-purity Germanium, particularly in semiconductor and fiber optic sectors. Advanced refining techniques now enable purities exceeding 99.999%, essential for next-generation electronic devices and infrared optics. This trend is driving investments in purification technologies and quality control systems across key production hubs in Asia and North America.

• Expansion of Germanium Use in Solar Energy Technologies: The integration of Germanium in multi-junction solar cells is gaining momentum due to its superior ability to convert sunlight into electricity efficiently. Several large-scale solar projects in Europe and the Asia-Pacific region have incorporated Germanium substrates, boosting the material’s adoption in renewable energy. This shift reflects growing emphasis on sustainable energy solutions and advances in photovoltaic cell design.

• Advancements in Automated Manufacturing Processes: Automation and robotics are increasingly incorporated into Germanium processing and component manufacturing. Automated crystal growth and wafer slicing technologies enhance production precision and reduce defects, particularly in East Asia’s semiconductor manufacturing centers. These innovations lead to higher throughput and improved product consistency, positioning the Germanium market for enhanced competitiveness.

• Increased Focus on Environmentally Sustainable Practices: Environmental regulations and corporate sustainability goals are shaping Germanium mining and refining operations. Companies are adopting greener extraction methods, reducing waste generation, and implementing energy-efficient technologies. This trend is especially pronounced in Europe and North America, where regulatory frameworks incentivize cleaner production processes, fostering long-term market viability.

The Germanium Market is segmented based on product types, applications, and end-user industries, offering a comprehensive understanding of demand drivers and growth areas. Product types include high-purity Germanium, Germanium dioxide, and Germanium tetrachloride, each serving distinct industrial purposes. Applications span electronics, optics, solar energy, and infrared technologies, reflecting Germanium’s versatile role in advanced technological sectors. End-users primarily involve telecommunications, semiconductor manufacturing, and renewable energy industries, with emerging interest from quantum computing and defense sectors. This segmentation enables decision-makers to pinpoint critical market segments and tailor strategies according to evolving technological and industrial trends.

High-purity Germanium dominates the Germanium Market due to its critical role in semiconductor devices and fiber optic systems requiring exceptional electrical and optical performance. This product type’s superior purity levels support advanced applications in infrared detectors and photonics. The fastest-growing type is Germanium dioxide, driven by its expanding use in the production of optical fibers and photovoltaic cells, where it enhances light transmission and energy conversion efficiency. Germanium tetrachloride, while smaller in market share, remains important for chemical synthesis and manufacturing of specialty glass. Each type contributes uniquely to the market, with high-purity Germanium accounting for the bulk of industrial consumption, Germanium dioxide fueling growth in renewable energy, and Germanium tetrachloride serving niche chemical applications.

Electronics is the leading application in the Germanium Market, attributed to the material’s use in high-speed transistors, diodes, and photodetectors essential for modern communication and computing devices. The precision and reliability of Germanium-based components make electronics the largest demand driver. Solar energy applications are the fastest-growing segment, as Germanium substrates are integral to multi-junction solar cells used in concentrated photovoltaic systems, which provide enhanced solar efficiency. Infrared optics and fiber optics remain important applications, supporting defense, aerospace, and telecommunication industries with high-performance materials for sensors and communication networks. Other applications such as LED technology and medical imaging contribute to the overall diversified use of Germanium.

The telecommunications industry leads as the primary end-user of Germanium, driven by the critical need for high-quality fiber optics and optical components in expanding 5G infrastructure and data networks worldwide. Semiconductor manufacturing is the fastest-growing end-user segment, propelled by the increasing demand for advanced computing devices and quantum technology development that rely on Germanium’s superior electronic properties. Other significant end-users include renewable energy firms, focusing on Germanium-based photovoltaic technologies, and defense sectors utilizing Germanium in infrared sensors and surveillance equipment. These end-user segments collectively influence market dynamics by demanding specialized Germanium products tailored to their evolving technological needs.

Asia-Pacific accounted for the largest market share at 42% in 2024; however, Africa is expected to register the fastest growth, expanding at a CAGR of 16% between 2025 and 2032.

To Learn More About This Report, Request A Free Sample Copy

Asia-Pacific’s dominance is driven by extensive manufacturing infrastructure, high consumption in electronics and solar sectors, and continuous technological innovation. Africa’s rapid growth is fueled by increasing investments in mining operations, infrastructure development, and expanding energy projects. The region’s regulatory reforms and favorable trade agreements also support emerging Germanium applications. Overall, regional consumption patterns reflect diverse industrial demands, regulatory environments, and technological adoption, shaping the global Germanium market landscape for the coming decade.

Emerging High-Tech Applications Boost Demand in Key Industries

North America holds approximately 25% of the global Germanium market volume, driven largely by its advanced electronics, aerospace, and defense industries. The region benefits from strong government support for semiconductor innovation and renewable energy projects, with recent regulatory updates encouraging sustainable material sourcing and efficient manufacturing. Technological advances such as AI-enabled manufacturing and automation enhance production precision and operational efficiency. The digital transformation of supply chains and growing investments in 5G infrastructure further elevate Germanium demand. North America continues to lead in research and development activities, integrating Germanium into cutting-edge applications across multiple high-tech sectors.

Focus on Sustainability and Innovation in Leading Industrial Hubs

Europe accounts for nearly 20% of the Germanium market volume, with Germany, the UK, and France serving as the main contributors. The region emphasizes strict environmental regulations and sustainability initiatives that influence Germanium extraction and processing practices. European regulatory bodies actively promote greener manufacturing processes, driving innovation in recycling and waste reduction. Adoption of emerging technologies such as advanced photonics and high-efficiency solar cells is widespread. Investment in research institutions and clean energy projects further enhances demand. Europe’s commitment to circular economy principles and renewable energy integration creates a progressive environment for Germanium market growth.

Manufacturing Powerhouse with Expanding High-Tech Ecosystem

Asia-Pacific commands the largest volume share of the Germanium market, with China, India, and Japan as leading consumers. The region’s robust manufacturing sector, including semiconductor fabrication and solar panel production, underpins high Germanium consumption. Infrastructure expansion and rapid urbanization fuel demand in electronics and energy industries. Technology hubs in China and Japan pioneer innovations in Germanium-based photonics and infrared applications. Government incentives for renewable energy projects and advanced materials research accelerate market development. Asia-Pacific’s blend of production capacity, technological innovation, and growing domestic consumption secures its dominant position in the global Germanium market.

Energy Sector Development and Industrial Growth Drive Demand

South America contributes around 7% to the Germanium market, with Brazil and Argentina as primary participants. The region’s growing energy infrastructure projects and expanding telecommunications networks increase demand for Germanium components. Trade policies promoting mineral exports and government incentives for renewable energy accelerate market activity. Industrial sectors are gradually adopting high-purity Germanium in electronics and solar applications. Investment in manufacturing facilities and partnerships with international firms further support market expansion. South America’s strategic focus on energy diversification and infrastructure modernization creates promising prospects for Germanium usage.

Technological Modernization and Resource Development Spur Growth

Middle East & Africa represent roughly 6% of the global Germanium market volume, with significant demand in UAE and South Africa. The region’s oil & gas sector drives specialized Germanium applications in sensors and monitoring equipment. Rapid urban development and construction projects increase material consumption. Technological modernization initiatives focus on integrating Germanium in renewable energy and advanced electronics. Local regulations promoting sustainable mining and trade partnerships with global suppliers enhance market accessibility. Investment in research and infrastructure supports long-term growth. This region’s expanding industrial base and strategic resource management contribute to its rising Germanium market profile.

China: Holds 38% market share due to vast production capacity and strong domestic electronics and solar energy demand.

United States: Accounts for 24% market share, driven by advanced semiconductor manufacturing and significant government support for innovation in high-tech applications.

The Germanium market is characterized by a highly competitive environment with over 30 active global players involved in mining, refining, and application-specific production. Market leaders have strategically positioned themselves through innovation in material processing and integration into advanced technology sectors such as semiconductors, fiber optics, and solar energy. Partnerships and joint ventures are increasingly common, aimed at expanding production capabilities and enhancing research and development efforts. Recent product launches focus on higher purity Germanium and novel applications in photonics and infrared technologies, providing differentiation in a crowded marketplace. Mergers and acquisitions continue to reshape the competitive landscape, allowing companies to consolidate resources and optimize supply chains. Additionally, companies are investing heavily in sustainable sourcing and green manufacturing practices, responding to growing regulatory pressure and customer demand for environmentally responsible products. Innovation trends, including automation and digitalization in production, are further intensifying competition by improving efficiency and reducing costs. Overall, the Germanium market’s competitive dynamics are driven by technological advancement, strategic collaborations, and a focus on sustainability.

Umicore

Teck Resources Limited

American Elements

Nippon Light Metal Co., Ltd.

ASMC (Advanced Semiconductor Materials Co.)

5N Plus Inc.

AXT, Inc.

Anglo American plc

Vital Materials Co., Ltd.

Metallo-Chimique NV

The Germanium market is undergoing significant technological advancements that are shaping production processes and expanding application potential. High-purity germanium (HPGe) production technologies continue to evolve, enabling ultra-refined material essential for semiconductor and infrared optics industries. Techniques such as zone refining and chemical vapor deposition have improved purity levels exceeding 99.9999%, which is critical for high-performance electronic devices. Additionally, innovations in germanium alloying and thin-film deposition are facilitating enhanced performance in fiber optic systems and photovoltaic cells. The integration of nanotechnology has also introduced opportunities for germanium-based nano-devices used in advanced computing and sensing applications.

Emerging technologies in recycling and recovery of germanium from industrial byproducts are gaining traction, reducing dependence on primary mining and contributing to sustainable resource management. Furthermore, automation and digitalization in germanium refining plants improve operational efficiency, consistency, and yield while reducing costs and environmental impact. Research into germanium-based materials for next-generation photonics and quantum computing is progressing, positioning germanium as a vital component in future technology ecosystems. The continued focus on enhancing material properties through advanced manufacturing techniques ensures that the Germanium market remains dynamic and innovative, providing substantial value across diverse industrial sectors.

In June 2024, LAPP introduced the ETHERLINE® FD bioP Cat.5e, its first bio-based Ethernet cable produced in series. This sustainable variant features a bio-based outer sheath composed of 43% renewable raw materials, reducing the carbon footprint by 24% compared to traditional fossil-based TPU sheaths.

In November 2023, 5N Plus announced the expansion of its germanium refining facility, increasing production capacity by 15% to meet rising demand from the semiconductor and solar industries, incorporating advanced purification technology for improved material quality.

In March 2024, Nippon Light Metal Co. launched a new line of germanium-based infrared optical components, leveraging enhanced thin-film coating techniques to improve transmission efficiency by over 10%, targeting aerospace and defense applications.

In August 2023, American Elements developed a patented germanium nanowire synthesis process, enabling scalable production of nanowires with controlled dimensions and enhanced electrical properties, facilitating their use in next-generation electronics and sensor technologies.

The Germanium Market Report provides an extensive analysis covering a wide array of market segments, including product types, applications, and end-user industries. Key product segments include high-purity germanium, germanium dioxide, and germanium wafers, each catering to distinct industrial needs. The report examines applications spanning electronics, fiber optics, solar energy, and infrared optics, highlighting usage trends and technology integration within these sectors. Additionally, it covers emerging segments such as germanium nanomaterials and quantum computing components, reflecting the market’s innovation trajectory.

Geographically, the report encompasses comprehensive regional coverage, focusing on major markets in North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It offers insights into regional consumption patterns, infrastructure development, and regulatory frameworks influencing germanium demand and supply dynamics. Industry focus areas include semiconductor manufacturing, telecommunications, renewable energy, aerospace, and defense, providing a holistic view of market drivers and constraints.

The report also explores technological advancements, including refining techniques, recycling methods, and material engineering innovations shaping market evolution. Strategic insights into competitive landscapes, supply chain considerations, and investment opportunities are incorporated to support informed decision-making. Overall, the report equips business leaders and industry professionals with critical data and analysis required to navigate the Germanium market’s complex and rapidly evolving environment effectively.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 4428.75 Million |

|

Market Revenue in 2032 |

USD 14519.28 Million |

|

CAGR (2025 - 2032) |

16% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Umicore, Teck Resources Limited, American Elements, Nippon Light Metal Co., Ltd., ASMC (Advanced Semiconductor Materials Co.), 5N Plus Inc., AXT, Inc., Anglo American plc, Vital Materials Co., Ltd., Metallo-Chimique NV |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |