Reports

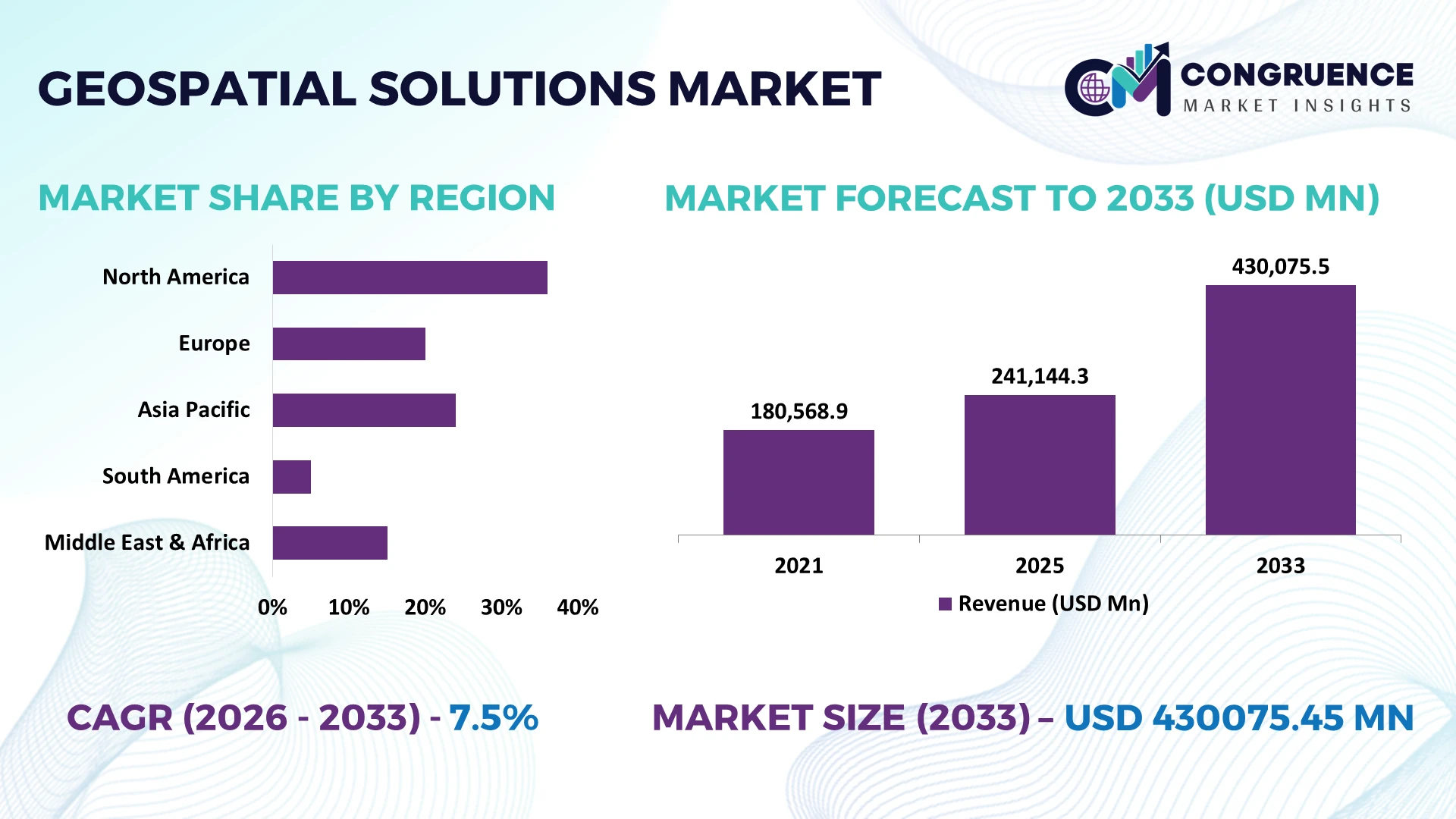

The Global Geospatial Solutions Market was valued at USD 241144.26 Million in 2025 and is anticipated to reach a value of USD 430075.45 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033. Growth is being driven by AI-enabled spatial analytics, expanding satellite constellations, digital infrastructure programs, and enterprise integration of real-time location intelligence across transportation, utilities, agriculture, and defense operations.

The United States leads the global geospatial solutions market with approximately 32% adoption across government, defense, logistics, and smart infrastructure, supported by multi-billion-dollar Earth observation and mapping investments. China follows with rapid deployment across smart cities and industrial monitoring, while the European Union accelerates geospatial modernization through cross-border digital infrastructure initiatives. Compared with China, the United States maintains broader enterprise deployment, while over 70% of large infrastructure projects increasingly integrate advanced geospatial analytics for planning and operational management amid evolving global security priorities.

Organizations investing in scalable geospatial intelligence platforms are strengthening operational resilience, accelerating infrastructure decisions, and improving long-term asset management capabilities.

Market Size & Growth: USD 241144.26 Million in 2025 to USD 430075.45 Million by 2033 at 7.5% CAGR, driven by AI-powered spatial intelligence and enterprise digital transformation.

Top Growth Drivers: AI mapping adoption exceeds 45%, satellite data utilization rises 38%, and smart infrastructure investments expand 30% globally.

Short-Term Forecast: By 2028, automated geospatial workflows improve planning efficiency by 28% while reducing field survey costs by 22%.

Emerging Technologies: AI analytics, digital twins, and cloud-native GIS platforms increase processing productivity by more than 35%.

Regional Leaders: North America surpasses USD 145000 Million, Asia-Pacific exceeds USD 128000 Million, and Europe crosses USD 98000 Million, supported by infrastructure modernization and regional digital expansion.

Consumer/End-User Trends: Over 62% of utilities, logistics, and public agencies deploy location intelligence for real-time operational decisions.

Pilot/Case Example: In 2026, an urban digital twin deployment improved infrastructure inspection efficiency by 34% and reduced maintenance response time by 26%.

Competitive Landscape: Top providers collectively control nearly 42% market share, with leading participation from Hexagon, Esri, Trimble, Autodesk, and Bentley Systems.

Regulatory & ESG Impact: Geospatial monitoring improves environmental compliance accuracy by 29% while supporting infrastructure resilience and land-use governance.

Investment & Funding: More than USD 12 Billion supports satellite analytics, cloud GIS, partnerships, and spatial AI expansion despite evolving global supply-chain realignment.

Innovation & Future Outlook: Edge-enabled geospatial intelligence and autonomous mapping increase decision speed by over 40%, reinforcing next-generation enterprise planning.

Rapid deployment of AI-powered spatial analytics, high-resolution Earth observation, and cloud-native mapping platforms is expanding demand across utilities, transportation, environmental monitoring, and precision agriculture. More than 55% of new enterprise geospatial deployments integrate automation for faster decision-making, while evolving infrastructure standards and resilient technology supply chains continue accelerating advanced location intelligence adoption, setting the foundation for the strategic market discussion.

Geospatial solutions have become a strategic capability for infrastructure planning, national security, logistics optimization, energy networks, and industrial asset management. Organizations increasingly rely on location intelligence to improve operational visibility as digital infrastructure modernization and resilient supply-chain restructuring reshape investment priorities. The integration of satellite imagery, IoT sensors, and AI-driven spatial analytics enables faster planning decisions while strengthening compliance with evolving land-use, environmental, and transportation regulations.

Modern AI-enabled geospatial platforms process spatial datasets nearly 45% faster than legacy desktop GIS environments while reducing manual mapping workflows by approximately 30%, improving enterprise productivity and decision accuracy. The United States continues to lead high-value commercial deployment through defense, utilities, and transportation programs, whereas India is expanding adoption across digital land records, smart mobility, and public infrastructure. Over the next two to three years, enterprise cloud-based geospatial deployments are expected to exceed 65% of new implementations as organizations prioritize scalable, real-time operational intelligence.

A practical example is the deployment of digital twin platforms for railway and utility corridor monitoring, where automated geospatial analytics reduce inspection cycles by more than 25% while improving maintenance planning. Leading technology providers are expanding AI capabilities, forming satellite-data partnerships, and investing in cloud-native mapping ecosystems to strengthen platform interoperability. Companies securing integrated geospatial intelligence capabilities today will achieve stronger operational resilience, faster infrastructure execution, and a durable competitive advantage.

AI-enabled geospatial analytics is transforming enterprise decision-making across transportation, utilities, mining, and defense by reducing manual spatial processing and improving operational visibility. More than 60% of large infrastructure programs now integrate advanced location intelligence, while automated mapping lowers field verification requirements by nearly 28% and improves planning accuracy by over 35%. India's national digital infrastructure initiatives and the United States' continued investment in geospatial modernization are accelerating deployment across public and private sectors. In response, leading companies are expanding cloud GIS portfolios, strengthening satellite data partnerships, and investing in AI-based spatial automation. The strategic outcome is faster infrastructure delivery, lower operational costs, and more resilient asset management across complex industrial environments.

Interoperability challenges remain a structural barrier as organizations combine satellite imagery, drone data, IoT networks, and legacy GIS platforms. Approximately 40% of enterprise spatial datasets require significant preprocessing before integration, while inconsistent data standards increase project implementation timelines by nearly 20%. Cross-border data governance requirements and national data sovereignty policies further complicate multinational deployments, particularly for organizations operating across the United States and Europe. To reduce operational risk, companies are investing in standardized cloud architectures, localized data hosting, and long-term software integration agreements. Organizations that successfully streamline data interoperability achieve faster deployment cycles and stronger returns from enterprise geospatial investments.

The convergence of digital twins, edge computing, and AI-powered remote sensing is creating new commercial opportunities beyond traditional mapping. More than 55% of industrial operators are evaluating continuous asset monitoring platforms, while predictive geospatial analytics can reduce maintenance costs by approximately 24% and improve operational uptime by over 20%. Japan's smart manufacturing initiatives and Australia's mining automation programs are accelerating adoption of intelligent spatial platforms. Technology providers are increasing R&D investment, developing interoperable software ecosystems, and expanding strategic partnerships with satellite and drone service providers. The greatest competitive advantage lies in delivering integrated, real-time geospatial intelligence rather than standalone mapping capabilities.

Expanding enterprise geospatial deployments requires secure cloud infrastructure, high-performance computing, and specialized workforce capabilities that remain uneven across industries. Nearly 37% of organizations report shortages of advanced geospatial and spatial AI professionals, while cyber risks affecting critical infrastructure continue to increase. Large-scale deployment also demands consistent integration with engineering, ERP, and operational technology systems, extending implementation complexity. Germany and the United States are increasing investment in secure digital infrastructure and workforce development to address these operational pressures. Companies that prioritize cybersecurity, standardized architectures, and continuous technical training will achieve more scalable, resilient, and competitive geospatial operations over the long term.

AI-Driven Mapping Automation Enterprise geospatial workflows increasingly integrate AI to automate feature extraction, reducing image interpretation time by nearly 45% and improving mapping accuracy by over 30%. Growing infrastructure modernization programs in the United States are accelerating deployment, while software providers expand cloud-native platforms and automation partnerships to shorten project delivery cycles and lower operational costs.

High-Resolution Earth Observation Expansion Commercial satellite constellations and advanced remote sensing services continue expanding, with revisit frequency improving by approximately 40% and image availability increasing more than 35%. Regulatory demand for environmental monitoring and infrastructure reporting is strengthening enterprise procurement, prompting companies to secure long-term satellite capacity agreements and diversify data acquisition strategies for uninterrupted operations.

Digital Twin Infrastructure Integration Utilities, transportation operators, and industrial asset owners are embedding geospatial data into digital twin environments, increasing predictive maintenance efficiency by around 28% while reducing field inspection requirements by nearly 25%. Germany and Japan are accelerating infrastructure digitization, encouraging technology vendors to integrate engineering software, IoT platforms, and real-time spatial analytics into unified operational ecosystems.

Cloud-Native Spatial Collaboration More than 65% of newly deployed enterprise geospatial platforms now support cloud-based collaboration, reducing project coordination time by about 32% across distributed engineering teams. Persistent skilled workforce shortages are encouraging companies to standardize workflows, expand managed geospatial services, and strengthen enterprise partnerships, creating scalable delivery models beyond traditional desktop GIS environments.

Geographic Information Systems (GIS) remain the leading segment with an estimated 36% market share, supported by enterprise-wide scalability, seamless integration with cloud platforms, and extensive deployment across government, utilities, and transportation. Organizations continue replacing fragmented mapping environments with centralized GIS ecosystems, improving operational coordination by approximately 30% while reducing manual spatial processing requirements. Spatial Analytics represents the fastest-growing segment as AI-enabled decision support expands across infrastructure planning and industrial operations. Companies are increasing investment in intelligent analytics engines, cloud deployment, and enterprise interoperability to strengthen competitive differentiation.

Remote Sensing continues expanding through high-frequency Earth observation and environmental monitoring, while Global Navigation Satellite Systems (GNSS) remain fundamental for positioning, fleet management, and autonomous operations. LiDAR Solutions are gaining momentum across digital twins, autonomous mobility, and precision infrastructure inspection, delivering survey productivity improvements exceeding 35% in complex environments. Vendors increasingly combine GIS, LiDAR, and spatial analytics into unified platforms, shifting investment toward integrated geospatial ecosystems rather than standalone mapping software.

Urban Planning remains the largest application, accounting for approximately 31% of total demand as governments modernize transportation networks, utilities, and smart city infrastructure. Integrated geospatial platforms improve planning efficiency by nearly 27% while enabling faster land-use assessment and infrastructure coordination. Disaster Management is the fastest-growing application as climate resilience initiatives and emergency response modernization increase investment in real-time spatial intelligence. Technology providers are expanding predictive analytics, cloud collaboration, and rapid-response mapping capabilities to support operational readiness.

Precision Agriculture continues gaining adoption through satellite monitoring and precision field management, helping optimize resource utilization by more than 20%. Asset Management remains a core enterprise application for utilities and industrial operators seeking predictive maintenance and lifecycle optimization, while Environmental Monitoring benefits from stronger compliance requirements and ecosystem assessment programs. Companies are broadening solution portfolios through AI integration and industry-specific deployment models that improve operational performance across multiple application environments.

Government remains the dominant end-user segment with an estimated 38% market share due to extensive deployment across land administration, infrastructure management, environmental monitoring, and public safety. Large-scale national mapping initiatives and digital governance programs continue driving procurement, while integrated geospatial platforms improve administrative efficiency by approximately 26%. Transportation & Logistics represents the fastest-growing end-user segment as real-time routing, fleet visibility, and supply-chain optimization become operational priorities. Solution providers are expanding cloud services and customized analytics platforms to address evolving enterprise requirements.

Defense continues investing in advanced geospatial intelligence for mission planning and situational awareness, while Utilities accelerate adoption for asset inspection, network resilience, and predictive maintenance. Agriculture increasingly deploys precision geospatial technologies to optimize irrigation, crop monitoring, and field productivity, with operational efficiency improving by nearly 22% in digitally managed farms. Companies are strengthening competitive positioning through sector-specific partnerships, modular software architectures, and integrated service ecosystems tailored to individual end-user requirements.

North America accounted for the largest market share at 35.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a 9.1% between 2026 and 2033.

Strategic Digital Infrastructure and Enterprise Mapping Leadership

North America maintains the highest deployment concentration through advanced geospatial integration across defense, utilities, transportation, energy, and smart infrastructure. The region represents approximately 35.8% of global demand, supported by mature cloud ecosystems, commercial satellite operators, and extensive enterprise GIS adoption. More than 68% of large infrastructure operators have integrated location intelligence into operational planning, while digital twin deployment continues expanding across critical infrastructure management. Enterprise software providers are strengthening interoperability between AI analytics, remote sensing, and engineering platforms through strategic technology partnerships. Continued modernization of transportation corridors, power grids, and environmental monitoring systems reinforces the region's leadership in high-value geospatial implementation and operational innovation.

United States Market Outlook: The United States remains the largest national market due to extensive federal infrastructure modernization, commercial satellite leadership, and enterprise digital transformation initiatives. More than 70% of major utility and transportation organizations utilize enterprise geospatial platforms for predictive asset management and network planning. Continuous investment in AI-enabled mapping, cloud-native GIS, and defense geospatial intelligence enables technology providers to expand integrated software ecosystems while supporting large-scale infrastructure modernization programs.

Regulatory Standardization Accelerating Intelligent Spatial Operations

Europe continues strengthening its position through standardized geospatial frameworks, sustainable infrastructure planning, and advanced environmental monitoring. The region contributes approximately 26% of global deployment activity, supported by integrated digital governance initiatives and cross-border spatial data interoperability. More than 60% of public infrastructure projects increasingly incorporate geospatial intelligence for planning, inspection, and compliance management. Engineering software providers are expanding partnerships to integrate digital twins, LiDAR, and cloud GIS into transportation and utility modernization programs. Strong regulatory alignment and continued investment in resilient infrastructure encourage consistent enterprise adoption while improving operational transparency across multiple industrial sectors.

Germany Market Outlook: Germany leads the regional market through advanced engineering capabilities, industrial digitalization, and intelligent infrastructure management. Large manufacturing enterprises increasingly integrate geospatial analytics into factory planning, logistics optimization, and utility management, with digital engineering adoption exceeding 55% across major industrial organizations. Technology companies continue expanding integrated software platforms that combine GIS, BIM, and digital twin capabilities to improve operational productivity and long-term infrastructure performance.

Large-Scale Infrastructure Digitization Driving Deployment

Asia-Pacific is experiencing the fastest operational expansion through smart city development, transportation modernization, industrial automation, and national digital infrastructure programs. The region represents approximately 28% of global deployment activity while recording the highest implementation momentum across emerging economies. More than 50% of newly launched metropolitan infrastructure initiatives incorporate advanced geospatial technologies for planning and monitoring. Governments and technology providers are expanding cloud GIS platforms, satellite applications, and AI-enabled spatial analytics to improve operational efficiency. Rapid urbanization, manufacturing expansion, and public infrastructure investment continue strengthening enterprise demand for integrated geospatial intelligence solutions.

China Market Outlook: China maintains a dominant position through extensive smart city deployment, satellite infrastructure, and industrial digitalization initiatives. Thousands of infrastructure projects integrate geospatial platforms for urban planning, transportation management, and environmental monitoring. National investment in high-resolution Earth observation and AI-powered mapping continues strengthening enterprise deployment capabilities while technology companies expand integrated spatial intelligence ecosystems supporting manufacturing, logistics, and public infrastructure management.

Resource Industries Expanding Spatial Intelligence Adoption

South America is steadily increasing geospatial deployment across mining, agriculture, transportation, and environmental monitoring. The region accounts for approximately 5.8% of global market activity, with mining operations and precision agriculture driving enterprise implementation. Geospatial monitoring has improved resource planning efficiency by nearly 24% across large industrial operations, while digital land management initiatives continue expanding. Companies increasingly establish partnerships with satellite analytics providers and cloud GIS vendors to improve operational visibility despite infrastructure disparities. Continued modernization of logistics corridors and natural resource management creates sustainable long-term deployment opportunities across industrial sectors.

Brazil Market Outlook: Brazil leads regional adoption through large-scale agriculture, mining operations, and infrastructure development. Precision farming technologies increasingly combine satellite imagery, GNSS, and spatial analytics to optimize field operations, with digital farm management adoption exceeding 40% among large commercial producers. Enterprise software providers continue strengthening localized platforms and industry partnerships to support operational efficiency across transportation, environmental management, and natural resource industries.

Infrastructure Transformation Supporting Advanced Spatial Platforms

The Middle East & Africa is strengthening geospatial adoption through smart infrastructure, energy diversification, urban development, and national digital transformation strategies. The region contributes approximately 4.4% of global deployment while accelerating implementation across utilities, transportation, and construction. More than 35% of newly planned metropolitan infrastructure developments incorporate digital mapping and spatial analytics from project initiation. Technology vendors continue expanding cloud deployment capabilities, AI-enabled monitoring platforms, and strategic implementation partnerships to support large-scale modernization programs. Infrastructure investment and digital governance reforms are steadily improving enterprise demand despite uneven deployment maturity across individual countries.

Saudi Arabia Market Outlook: Saudi Arabia represents the region's most strategically important market through extensive smart city initiatives, infrastructure expansion, and digital transformation programs. National development projects increasingly integrate geospatial intelligence for urban planning, transportation optimization, and environmental monitoring, while enterprise adoption continues accelerating across construction and utilities. Ongoing investment in advanced digital infrastructure and intelligent planning platforms strengthens long-term deployment opportunities for global and domestic geospatial technology providers.

Competition in the Geospatial Solutions Market is led by Esri, Hexagon AB, Trimble Inc., Bentley Systems, and Autodesk, while regional GIS providers and specialized spatial analytics firms compete through localized deployment and industry customization. The top five players collectively account for approximately 48% of the market, creating a moderately consolidated structure where technology leaders compete against cost-focused regional vendors. Competition centers on AI integration, cloud-native GIS, interoperability, and implementation speed, with automated workflows improving project efficiency by nearly 35% and cloud deployments reducing infrastructure costs by about 28%. Enterprise clients increasingly prioritize integrated ecosystems over standalone software, encouraging vendors to expand through strategic acquisitions, satellite-data partnerships, and vertical integration with digital twin and engineering platforms. The competitive shift favors intelligent spatial analytics rather than conventional mapping capabilities, accelerating consolidation around scalable cloud architectures. High implementation complexity, interoperability requirements, and enterprise switching costs remain significant entry barriers. Winning requires integrated AI-enabled platforms, strong enterprise partnerships, rapid deployment capability, and industry-specific operational expertise.

Esri

Hexagon AB

Trimble Inc.

Bentley Systems

Autodesk Inc.

Topcon Corporation

Leica Geosystems

FARO Technologies

Maxar Technologies

Planet Labs PBC

TomTom N.V.

SuperMap Software Co., Ltd.

Oracle Corporation

Google LLC

Artificial intelligence, cloud-native GIS, and high-resolution Earth observation are redefining enterprise geospatial operations by replacing isolated mapping workflows with integrated spatial intelligence platforms. More than 65% of new enterprise implementations now utilize cloud-based deployment, while AI-assisted feature extraction improves processing efficiency by approximately 40% and reduces manual interpretation by nearly 35%. Organizations increasingly integrate satellite imagery, drone data, IoT sensors, and engineering systems into unified operational environments, enabling faster planning and more accurate infrastructure management.

Modern AI-enabled geospatial platforms outperform legacy desktop GIS by processing large spatial datasets around 45% faster while lowering infrastructure maintenance costs by approximately 25%. LiDAR integrated with digital twins delivers significantly higher inspection precision than conventional field surveys, supporting utilities, transportation operators, and industrial asset owners. Technology leaders including Esri, Hexagon, and Trimble benefit from this transition by delivering interoperable platforms that combine analytics, visualization, automation, and enterprise-scale collaboration within a single operational ecosystem.

Between 2026 and 2028, edge computing, real-time satellite analytics, and autonomous spatial monitoring will become core enterprise capabilities rather than specialized applications. More than 70% of large infrastructure organizations are expected to prioritize intelligent geospatial automation for asset lifecycle management and predictive maintenance. Companies investing now in AI-enabled spatial analytics, cloud interoperability, and digital twin integration will strengthen operational resilience, shorten deployment cycles, improve infrastructure visibility, and establish a durable competitive advantage as enterprise geospatial ecosystems continue to mature.

July 2024 Trimble and Esri expanded their long-standing strategic partnership to integrate geospatial, BIM, and construction workflows, strengthening digital infrastructure project delivery while building on more than 25 years of collaboration across engineering and asset lifecycle management.

October 2025 Esri signed a Strategic Collaboration Agreement with Amazon Web Services to embed generative AI capabilities into ArcGIS, accelerating enterprise geospatial analytics and enabling scalable cloud-native spatial intelligence for public and commercial organizations. Source: https://esri.com

June 2026 Hexagon acquired ITRES Research Limited to strengthen its airborne mapping portfolio with hyperspectral and thermal imaging technologies. The acquired business is expected to contribute approximately EUR 13 million during 2026, expanding advanced multi-sensor geospatial capabilities. Source: https://hexagon.com

July 2025 ITRES and Leica Geosystems collaborated to combine hyperspectral imaging with single-photon LiDAR, delivering high-resolution remote sensing datasets that improve mapping efficiency and enable more accurate environmental and infrastructure analysis through integrated airborne surveying. Source: https://itres.com

The report provides a comprehensive assessment of the Geospatial Solutions Market across Geographic Information Systems (GIS), Remote Sensing, Global Navigation Satellite Systems (GNSS), LiDAR Solutions, and Spatial Analytics, covering the complete technology ecosystem and evolving enterprise deployment landscape. It evaluates applications including urban planning, precision agriculture, disaster management, asset management, and environmental monitoring, alongside demand across government, defense, agriculture, transportation & logistics, and utilities. The analysis spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, while tracking enterprise adoption, deployment intensity, and technology integration across more than 25 major country markets.

The study delivers strategic intelligence on competitive positioning, product innovation, AI-enabled spatial analytics, cloud-native GIS, digital twins, satellite intelligence, and LiDAR advancements. It assesses deployment patterns, regional investment priorities, supply-chain developments, regulatory influences, and industry partnerships to identify emerging business opportunities between 2026 and 2033. With coverage of 10+ leading companies and detailed segmentation across types, applications, end-users, and regions, the report supports investment planning, expansion strategy, competitive benchmarking, product development, and long-term decision-making for technology providers, infrastructure developers, enterprises, and institutional stakeholders.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 241144.26 Million |

Market Revenue in 2033 | USD 430075.45 Million |

CAGR (2026 - 2033) | 7.5% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Esri, Hexagon AB, Trimble Inc., Bentley Systems, Autodesk Inc., Topcon Corporation, Leica Geosystems, FARO Technologies, Maxar Technologies, Planet Labs PBC, TomTom N.V., SuperMap Software Co., Ltd., Oracle Corporation, Google LLC |

Customization & Pricing | Available on Request (10% Customization is Free) |