Reports

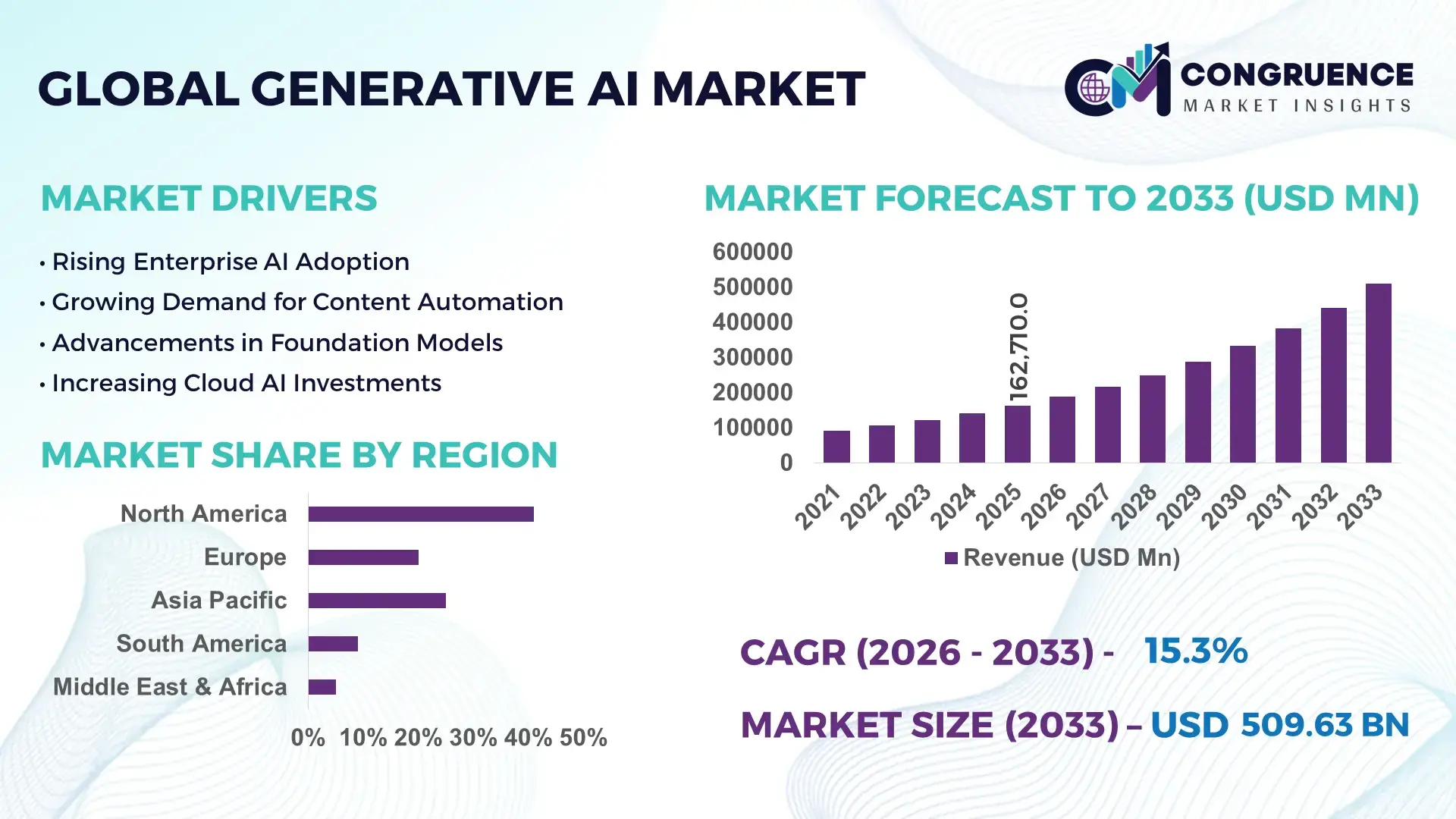

The Global Generative AI In Logistics Market was valued at USD 1086.29 Million in 2025 and is anticipated to reach a value of USD 10699.72 Million by 2033 expanding at a CAGR of 33.1% between 2026 and 2033. Growth is accelerating through AI-driven route orchestration, automated warehouse decision systems, and predictive shipment planning that reduce freight inefficiencies by over 28% across high-volume logistics networks.

The United States leads the global generative AI in logistics market with more than 34% share, supported by large-scale AI deployment across e-commerce, retail distribution, defense logistics, and third-party transportation networks. Over 62% of Tier-1 logistics operators in the country integrated generative AI models into fleet scheduling and warehouse automation systems by 2026, compared to less than 29% in 2023. Investments exceeding USD 4 billion in AI-enabled supply chain platforms strengthened deployment across ports, cold-chain logistics, and autonomous freight coordination. Compared with Europe, U.S. logistics firms process nearly 41% higher real-time shipment data volumes through generative AI-based control towers, improving warehouse throughput by 23% and reducing delivery exceptions by 19%.

Companies expanding AI-integrated logistics ecosystems and regional fulfillment intelligence platforms are positioned to secure stronger operational margins and faster cross-border supply chain execution.

Market Size & Growth: The market reached USD 1086.29 Million in 2025 and is projected to hit USD 10699.72 Million by 2033, driven by AI-led warehouse optimization and intelligent freight planning across global supply chains.

Top Growth Drivers: Automated route planning improves delivery efficiency by 31%, AI inventory forecasting cuts stock imbalance by 26%, and generative AI customer support reduces logistics response time by 38%.

Short-Term Forecast: By 2028, AI-enabled logistics platforms are expected to reduce operational costs by 22% while improving warehouse productivity by 27%.

Emerging Technologies: Generative AI, digital twins, and autonomous warehouse robotics are increasing shipment visibility accuracy by 35% and accelerating order processing cycles by 29%.

Regional Leaders: North America exceeds USD 3.8 Billion through advanced freight automation, Asia-Pacific crosses USD 3.1 Billion with rapid e-commerce expansion, and Europe surpasses USD 2.4 Billion through smart port digitization initiatives.

Consumer/End-User Trends: More than 58% of logistics enterprises adopted AI-assisted demand forecasting tools in 2026 to manage inventory volatility and faster fulfillment expectations.

Pilot/Case Example: In 2026, a multinational retail logistics operator deployed generative AI warehouse sequencing systems that lowered picking errors by 33% and improved dispatch speed by 24%.

Competitive Landscape: The top five providers control nearly 47% market share, with competition centered on AI scalability, cloud integration speed, and autonomous supply chain orchestration capabilities.

Regulatory & ESG Impact: AI-powered route optimization reduced fleet fuel consumption by 18% while supporting stricter emissions compliance and digital trade monitoring frameworks.

Investment & Funding: Global investments exceeded USD 5.6 Billion in 2026, led by cloud logistics partnerships, AI startup acquisitions, and intelligent warehouse infrastructure expansion.

Innovation & Future Outlook: Next-generation multimodal AI agents and real-time logistics copilots are transforming predictive supply chain management as companies prioritize resilient and decentralized freight ecosystems.

Generative AI in logistics is gaining rapid traction across retail, manufacturing, healthcare, and e-commerce sectors, which collectively contribute over 68% of enterprise deployments. Advanced AI copilots for warehouse orchestration, synthetic demand modeling, and autonomous shipment coordination improved fulfillment accuracy by nearly 32% in large distribution environments during 2026. North America continues leading high-value deployments, while Asia-Pacific records the fastest infrastructure expansion due to cross-border e-commerce growth and regional manufacturing diversification. Increasing customs digitization and supply chain security regulations are accelerating AI integration into freight documentation and risk monitoring systems. The market is steadily shifting toward self-learning logistics networks capable of adaptive decision-making across multimodal transportation ecosystems.

Generative AI in logistics is becoming strategically critical as freight operators, retailers, and industrial manufacturers shift from reactive supply-chain management to predictive and autonomous logistics ecosystems. The market is gaining importance through warehouse digitization, customs automation, and multimodal transportation optimization, particularly after global supply-chain restructuring increased pressure on delivery reliability and inventory accuracy. In 2026, more than 57% of large logistics enterprises integrated AI-assisted planning into transport management systems to reduce fulfillment delays and improve asset utilization across distributed networks.

Compared with conventional rule-based logistics software, generative AI platforms improve route recalibration speed by nearly 43% and reduce manual scheduling workloads by 35% through adaptive learning models. The United States and Germany are prioritizing AI-enabled warehouse intelligence and freight visibility systems, while India and Southeast Asia focus on scalable AI deployment across e-commerce fulfillment corridors and port-linked logistics parks. Over the next two to three years, automated shipment documentation and AI-generated demand forecasting are expected to expand across more than 48% of cross-border logistics operations.

Global logistics providers are accelerating partnerships with cloud infrastructure firms and robotics integrators to strengthen real-time orchestration capabilities. A major deployment trend involves AI copilots managing warehouse slotting, fuel optimization, and exception handling within unified logistics control towers. Companies securing scalable AI integration, interoperable data infrastructure, and faster deployment cycles are expected to achieve stronger operating resilience and higher network efficiency in increasingly decentralized supply chains.

Rapid expansion of AI-enabled logistics orchestration platforms is accelerating enterprise adoption across transportation, warehousing, and inventory management operations. In 2026, over 61% of large retail and manufacturing logistics operators deployed generative AI tools for demand forecasting and route optimization, reducing order processing delays by 27% and warehouse inefficiencies by 24%. The United States and China intensified investments in smart freight corridors and automated fulfillment hubs as same-day delivery expectations increased across e-commerce networks. This operational shift is pushing logistics providers to modernize legacy transportation management systems with AI-driven decision engines. Companies are responding through cloud logistics partnerships, acquisition of AI analytics firms, and expansion of autonomous warehouse infrastructure. Firms integrating predictive shipment intelligence with real-time fleet coordination are securing stronger delivery reliability and lower last-mile operational costs.

Integration complexity across fragmented logistics networks remains a major structural limitation for generative AI deployment. Nearly 46% of mid-sized logistics operators still rely on disconnected warehouse, freight, and inventory systems, creating interoperability bottlenecks and inconsistent data environments. In Germany and Japan, legacy enterprise resource planning infrastructure increased AI integration costs by approximately 31% compared with cloud-native logistics ecosystems. Data governance regulations and cross-border compliance requirements are also slowing deployment of AI-generated shipment documentation and automated customs workflows. These constraints directly affect scalability, operational visibility, and deployment consistency across multinational supply chains. Companies are mitigating risks through localized data centers, modular AI architecture, and long-term cloud migration strategies. Logistics providers prioritizing interoperable platforms and standardized operational datasets are achieving faster implementation timelines and lower integration overhead.

Next-generation autonomous logistics intelligence platforms are creating high-value opportunities across freight coordination, warehouse robotics, and predictive inventory allocation. In 2026, AI-assisted demand sensing improved inventory accuracy by 34% in large retail distribution networks, while predictive maintenance systems reduced fleet downtime by 22%. India and the United Arab Emirates are expanding smart logistics infrastructure linked to industrial corridors and automated port operations, accelerating deployment of AI-driven cargo management systems. Emerging adoption of multimodal AI agents capable of independently managing routing, scheduling, and exception handling is reshaping logistics operating models. Companies are increasing investments in digital twins, synthetic supply-chain simulations, and AI-powered fulfillment ecosystems to improve response speed during trade disruptions. Organizations building integrated AI logistics platforms with adaptive learning capabilities are positioned to capture higher-margin enterprise contracts and long-term infrastructure partnerships.

Long-term scalability of generative AI in logistics is constrained by cybersecurity risks, operational reliability concerns, and shortages of AI-skilled logistics personnel. In 2026, nearly 39% of logistics enterprises reported increased exposure to AI-related data vulnerabilities within connected transportation and warehouse systems. Large freight operators in the United States experienced higher compliance and infrastructure monitoring costs as AI-generated workflows expanded across customs processing and shipment tracking networks. Workforce adaptation also remains uneven, with less than 33% of warehouse employees trained to operate AI-assisted logistics platforms efficiently. These challenges affect deployment consistency, operational resilience, and trust in autonomous decision-making systems. Companies are responding through cybersecurity investments, workforce reskilling initiatives, and strategic partnerships with industrial automation providers. Logistics firms that secure resilient AI governance frameworks and scalable workforce integration models will maintain stronger competitive positioning in digitally connected supply-chain ecosystems.

AI-Controlled Warehouse Sequencing Automated warehouse sequencing systems are reducing order batching delays by 29% and improving picking efficiency by 24% across high-volume fulfillment centers in the United States and China. Rising labor shortages and same-day delivery pressure are accelerating deployment of AI-generated slotting and workflow orchestration tools. Logistics operators are restructuring warehouse layouts, integrating robotics fleets, and scaling AI-assisted inventory movement systems to increase throughput consistency during seasonal demand spikes.

Synthetic Demand Modeling Expansion Logistics providers are increasingly using synthetic demand modeling to improve inventory allocation accuracy and reduce forecasting errors by nearly 32%. In 2026, over 54% of large retail distribution networks integrated generative AI simulation tools into procurement and replenishment planning processes. Companies in Germany and India are expanding AI-driven digital twin capabilities to manage trade route disruptions and supplier variability. This shift is improving container utilization rates and reducing excess warehousing costs across multi-node supply chains.

Freight Documentation Automation Growth Automated freight documentation platforms are shortening customs processing time by 37% and reducing manual compliance workloads by 41% within cross-border logistics operations. Regulatory digitization initiatives and rising shipment complexity are accelerating adoption of AI-generated invoices, manifests, and trade compliance records. Transportation companies are partnering with cloud infrastructure firms to standardize multilingual documentation workflows and improve real-time shipment visibility across international freight corridors.

Logistics Copilot Integration Rising AI logistics copilots are becoming operational decision-support layers for fleet management, warehouse supervision, and delivery planning systems. More than 48% of enterprise logistics teams deployed conversational AI interfaces in 2026 to reduce dispatch coordination time and improve exception handling accuracy. Japanese and South Korean logistics firms are integrating multimodal AI copilots into transport control towers to optimize fuel consumption and rerouting decisions. Companies are prioritizing interoperable AI ecosystems that connect fleet telemetry, warehouse systems, and customer service operations through unified orchestration platforms.

Route Optimization Tools remain the leading segment due to their direct impact on fuel efficiency, delivery accuracy, and fleet utilization across large transportation networks. In 2026, nearly 44% of logistics enterprises prioritized AI-powered route orchestration systems to reduce delivery delays and improve last-mile coordination. These platforms outperform traditional dispatch systems by lowering fuel consumption by approximately 19% and improving shipment turnaround speed by 26%. Demand Forecasting Platforms represent the fastest-growing segment as retailers and manufacturers shift toward predictive inventory planning and dynamic replenishment strategies. Warehouse Automation Solutions are gaining traction in high-volume fulfillment hubs, particularly in the United States and China, where automated picking and slotting systems are being integrated with AI-generated workflow management. Predictive Analytics Solutions continue supporting operational intelligence and risk monitoring, while AI Chatbots are increasingly deployed for shipment tracking and customer query automation. Companies are expanding product ecosystems through cloud integrations, AI model customization, and partnerships with warehouse robotics providers to strengthen end-to-end logistics intelligence capabilities.

Supply Chain Optimization remains the dominant application segment as enterprises prioritize real-time logistics visibility, predictive shipment planning, and inventory synchronization across distributed networks. In 2026, more than 52% of large logistics operators integrated generative AI into supply-chain control towers to improve operational coordination and reduce fulfillment disruptions. Delivery Planning is emerging as the fastest-growing application due to increasing demand for dynamic routing, hyperlocal delivery management, and AI-assisted dispatch sequencing. Fleet Management applications continue evolving through predictive maintenance and fuel optimization systems that lower vehicle downtime by nearly 23%. Warehouse Operations are expanding rapidly within automated fulfillment environments, while Inventory Management platforms are increasingly integrated with demand sensing algorithms to reduce stock imbalances. Customer Service Automation is strengthening through conversational AI interfaces capable of resolving shipment inquiries and exception handling workflows. Logistics providers are scaling cloud-based orchestration systems and deploying AI-driven analytics layers to improve speed, cost efficiency, and shipment predictability across enterprise supply chains.

Logistics Providers account for the largest share of generative AI deployment due to their dependence on real-time fleet coordination, warehouse orchestration, and cross-border freight management infrastructure. In 2026, nearly 58% of large third-party logistics operators expanded AI integration across transportation planning and fulfillment operations to improve delivery precision and reduce manual coordination workloads. Retail and E-commerce represent the fastest-growing end-user segment as enterprises scale AI-driven inventory forecasting, hyperlocal delivery systems, and automated customer interaction platforms to support rising order volumes. Manufacturing companies are increasingly deploying predictive logistics intelligence to stabilize inbound material flow and reduce production downtime. Healthcare organizations are adopting AI-assisted cold-chain monitoring and compliance workflows, while Automotive and Transportation Companies are integrating generative AI into multimodal freight planning and connected fleet ecosystems. Vendors are responding through industry-specific platform customization, strategic cloud partnerships, and modular pricing models designed for enterprise-scale deployment and operational interoperability.

North America accounted for the largest market share at 36.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 35.8% between 2026 and 2033.

Enterprise AI Orchestration Driving Logistics Modernization

North America maintains leadership through large-scale deployment of AI-enabled transportation management systems, automated warehouse orchestration, and predictive freight intelligence platforms. The region accounts for over 36% of global deployment activity, supported by strong cloud infrastructure, advanced e-commerce fulfillment networks, and rapid enterprise AI integration across the United States and Canada. In 2026, more than 63% of Tier-1 logistics providers in the region implemented generative AI tools for dynamic routing and shipment exception management. Strategic partnerships between logistics operators and hyperscale cloud providers accelerated deployment of AI-powered control towers capable of processing real-time fleet and warehouse data streams. Growing labor optimization requirements and rising same-day delivery expectations continue pushing companies toward autonomous logistics coordination models.

United States Market Outlook: The United States remains the primary innovation hub for generative AI logistics deployment due to its concentration of large third-party logistics operators, advanced fulfillment infrastructure, and enterprise cloud adoption. More than 58% of warehouse automation projects initiated during 2026 integrated generative AI-assisted orchestration capabilities for inventory movement and dispatch planning. Strong investment activity across smart freight corridors, AI-enabled cold-chain logistics, and multimodal transportation networks continues strengthening operational scalability. Major logistics enterprises are prioritizing AI copilots and predictive shipment intelligence systems to reduce fuel inefficiencies and improve fulfillment precision across decentralized distribution ecosystems.

Regulatory Digitization Reshaping Freight Intelligence

Europe is strengthening its position through AI-enabled logistics compliance systems, smart port modernization, and sustainable transportation optimization initiatives. The region contributes nearly 27% of global enterprise deployment activity, with Germany, France, and the Netherlands leading adoption of AI-generated freight documentation and predictive warehouse management tools. In 2026, logistics firms implementing generative AI-assisted customs and compliance workflows reduced cross-border processing delays by approximately 29%. Increasing carbon-emission regulations and digital trade monitoring frameworks are accelerating adoption of AI-powered fleet optimization platforms. Companies are investing in interoperable logistics infrastructure and intelligent warehouse systems to improve operational transparency, multimodal freight coordination, and energy-efficient distribution management.

Germany Market Outlook: Germany remains the region’s strongest logistics technology market due to its industrial manufacturing scale, advanced transport infrastructure, and leadership in warehouse automation engineering. Over 46% of industrial logistics facilities in the country integrated AI-assisted predictive inventory systems by 2026 to support automotive, machinery, and export-oriented supply chains. German logistics operators are prioritizing AI-enabled route intelligence and digital twin simulation tools to improve freight synchronization across rail, road, and inland port networks. Strong enterprise investment in Industry 4.0 ecosystems continues reinforcing Germany’s strategic advantage in intelligent logistics deployment.

Large-Scale Fulfillment Automation Accelerating Adoption

Asia-Pacific is emerging as the fastest-expanding market due to rapid e-commerce growth, industrial manufacturing expansion, and accelerated smart logistics infrastructure development. The region accounts for nearly 31% of global deployment concentration, driven by China, India, Japan, and South Korea. In 2026, AI-enabled warehouse automation installations across Asia-Pacific increased by more than 34% as logistics providers expanded regional fulfillment capacity and cross-border shipment coordination. High shipment density, rising urban delivery volumes, and government-backed digital infrastructure investments are accelerating enterprise adoption of AI-powered transportation management systems. Companies are scaling autonomous fulfillment operations, AI-assisted inventory forecasting, and intelligent freight visibility platforms to improve operational agility and reduce delivery inefficiencies.

China Market Outlook: China dominates regional deployment activity through its extensive e-commerce logistics infrastructure, manufacturing supply-chain scale, and aggressive warehouse automation expansion. More than 61% of large distribution centers in eastern industrial provinces integrated AI-based dispatch optimization and warehouse sequencing tools during 2026. Domestic logistics providers are strengthening AI capabilities through robotics integration, cloud-based logistics orchestration, and predictive freight intelligence systems. Rapid expansion of smart ports and cross-border trade corridors continues positioning China as a central operational hub for AI-driven logistics modernization and fulfillment acceleration.

Digital Freight Coordination Gaining Momentum

South America is experiencing steady adoption of generative AI logistics systems through retail distribution modernization, fleet optimization initiatives, and expanding e-commerce fulfillment operations. Brazil and Chile account for the majority of enterprise AI logistics deployments, particularly across urban transportation and warehouse management networks. In 2026, logistics firms implementing AI-assisted delivery planning reduced route inefficiencies by nearly 18% within high-density metropolitan corridors. Infrastructure limitations and fragmented transportation networks continue affecting deployment consistency across several countries, yet growing investment in digital freight visibility and automated inventory management is improving operational coordination. Companies are focusing on cloud-based logistics platforms and strategic technology partnerships to strengthen scalability and reduce manual operational dependencies.

Brazil Market Outlook: Brazil leads regional adoption due to its large consumer distribution networks, expanding retail logistics ecosystem, and increasing investment in intelligent transportation management. More than 42% of large retail fulfillment operators in Brazil adopted AI-assisted route optimization systems in 2026 to improve last-mile delivery performance across congested urban centers. Logistics companies are prioritizing warehouse automation, predictive inventory planning, and AI-powered shipment monitoring platforms to address rising e-commerce order volumes. Ongoing modernization of port-linked logistics infrastructure continues supporting broader deployment of digital freight coordination technologies.

Smart Infrastructure Investments Supporting Expansion

The Middle East & Africa market is advancing through logistics corridor modernization, smart port investments, and AI-enabled trade facilitation initiatives. The United Arab Emirates and Saudi Arabia are leading deployment activity as governments accelerate digital transformation across transportation and supply-chain infrastructure. In 2026, AI-assisted cargo monitoring and customs automation systems improved shipment processing efficiency by nearly 26% across several Gulf logistics hubs. Rising investment in industrial free zones, multimodal freight connectivity, and cloud logistics ecosystems is strengthening adoption of intelligent warehouse and transportation management systems. Companies are entering regional partnerships focused on smart distribution networks, predictive cargo visibility, and automated freight documentation workflows.

United Arab Emirates Market Outlook: The United Arab Emirates remains the region’s most strategically advanced logistics technology market due to its integrated port infrastructure, free-zone ecosystem, and cross-border trade connectivity. More than 48% of large logistics facilities operating in Dubai and Abu Dhabi expanded AI-assisted freight coordination capabilities during 2026 to support rising international cargo movement. Enterprises are integrating generative AI into warehouse management, customs documentation, and multimodal transportation planning systems to improve shipment velocity and operational transparency. Continued investment in smart logistics corridors and automated trade infrastructure is reinforcing the country’s position as a leading AI-driven logistics gateway.

Global cloud technology leaders, logistics software specialists, and warehouse automation providers are competing aggressively across AI-driven supply-chain orchestration platforms. Microsoft, IBM, Oracle, SAP, and Blue Yonder compete against regional logistics intelligence firms and industrial automation vendors focused on lower-cost deployment models. The top five players collectively control nearly 49% of enterprise-scale implementations through integrated cloud ecosystems, transportation analytics, and warehouse automation capabilities. Competition increasingly centers on deployment speed, predictive accuracy, and interoperability, with AI-assisted route optimization improving delivery efficiency by 24% and automated warehouse sequencing reducing manual coordination workloads by 31%. Companies are strengthening market position through cloud partnerships, acquisition of AI startups, vertical integration with robotics platforms, and expansion of multimodal logistics intelligence networks. Technology disruption from generative AI copilots and autonomous decision engines is accelerating consolidation pressure. High integration complexity and enterprise data standardization remain major entry barriers. Winning requires scalable AI infrastructure, operational reliability, and seamless integration across fragmented logistics ecosystems.

Microsoft Corporation

IBM Corporation

Oracle Corporation

SAP SE

Blue Yonder

NVIDIA Corporation

Amazon Web Services

C.H. Robinson

Manhattan Associates

Kinaxis Inc.

Siemens AG

Samsung SDS

Project44

FourKites Inc.

Generative AI copilots, predictive orchestration engines, and AI-driven route optimization platforms are becoming core technologies across logistics operations. In 2026, nearly 59% of large logistics enterprises integrated generative AI into transportation management and warehouse sequencing systems to reduce dispatch delays and improve shipment visibility. Compared with legacy rule-based planning software, AI-enabled routing engines improve delivery recalibration speed by 43% and reduce fuel inefficiencies by 18%. Companies operating large fulfillment networks are combining generative AI with warehouse robotics and IoT telemetry to strengthen real-time operational coordination and lower manual planning workloads.

Emerging technologies between 2026 and 2028 include multimodal AI agents, digital twins, and autonomous logistics control towers capable of synchronizing freight, inventory, and warehouse decisions simultaneously. AI-generated demand simulations are improving inventory allocation accuracy by 31%, while synthetic supply-chain modeling reduces disruption response time by 27%. Japan and Germany are accelerating adoption of AI-assisted warehouse orchestration platforms integrated with edge computing infrastructure. Enterprises are responding through cloud partnerships, AI-specific infrastructure upgrades, and integration of natural-language operational interfaces for dispatch coordination and freight exception handling.

Disruptive innovation is shifting toward agentic AI systems capable of autonomous execution rather than predictive analysis alone. Logistics firms deploying AI-driven control towers reported nearly 35% faster exception resolution compared with conventional dashboard-based workflows. Technology leaders with scalable AI ecosystems, interoperable data architecture, and robotics integration capabilities are securing stronger competitive positioning as enterprises prioritize resilient, low-latency logistics intelligence networks through 2028.

May 2025 – SAP and Amazon Web Services launched an AI co-innovation program focused on generative AI supply-chain applications, improving logistics visibility and route optimization workflows by 30% across enterprise deployments, strengthening large-scale operational automation capabilities. Source: SAP News Center

January 2024 – IBM expanded its collaboration with SAP to develop generative AI solutions for retail and consumer supply-chain operations, accelerating direct-store delivery optimization and improving enterprise workflow efficiency through scalable AI integration frameworks. Source: IBM Newsroom

January 2025 – SAP introduced new agentic AI systems for supply-chain coordination during the Davos forum, enabling autonomous inventory and delivery synchronization while addressing infrastructure gaps affecting nearly 80% of enterprise customers. Source: Axios

October 2024 – IBM released Granite 3.0 enterprise AI models optimized for business operations and logistics intelligence, strengthening AI customization capabilities and accelerating deployment flexibility through integration with NVIDIA-powered enterprise infrastructure. Source: Reuters

The report provides comprehensive analysis of generative AI adoption across logistics planning, warehouse orchestration, transportation management, predictive fulfillment, and autonomous supply-chain coordination between 2026 and 2033. It evaluates deployment trends across Predictive Analytics Solutions, AI Chatbots, Route Optimization Tools, Warehouse Automation Solutions, and Demand Forecasting Platforms while assessing operational integration within Supply Chain Optimization, Fleet Management, Inventory Management, Warehouse Operations, Customer Service Automation, and Delivery Planning applications. More than 55% of enterprise deployments analyzed involve AI-assisted freight visibility and intelligent warehouse coordination systems.

The study covers key end-users including Logistics Providers, Retail and E-commerce, Manufacturing, Healthcare, Automotive, and Transportation Companies across North America, Europe, Asia-Pacific, South America, and Middle East & Africa. It examines enterprise AI deployment patterns, infrastructure modernization, cloud logistics ecosystems, and multimodal automation strategies shaping operational competitiveness. The report also delivers strategic insights into technology partnerships, autonomous logistics control towers, AI governance frameworks, and emerging agentic AI ecosystems supporting investment planning, market expansion, competitive positioning, and long-term supply-chain transformation priorities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1086.29 Million |

|

Market Revenue in 2033 |

USD 10699.72 Million |

|

CAGR (2026 - 2033) |

33.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, IBM Corporation, Oracle Corporation, SAP SE, Blue Yonder, NVIDIA Corporation, Amazon Web Services, C.H. Robinson, Manhattan Associates, Kinaxis Inc., Siemens AG, Samsung SDS, Project44, FourKites Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |