Reports

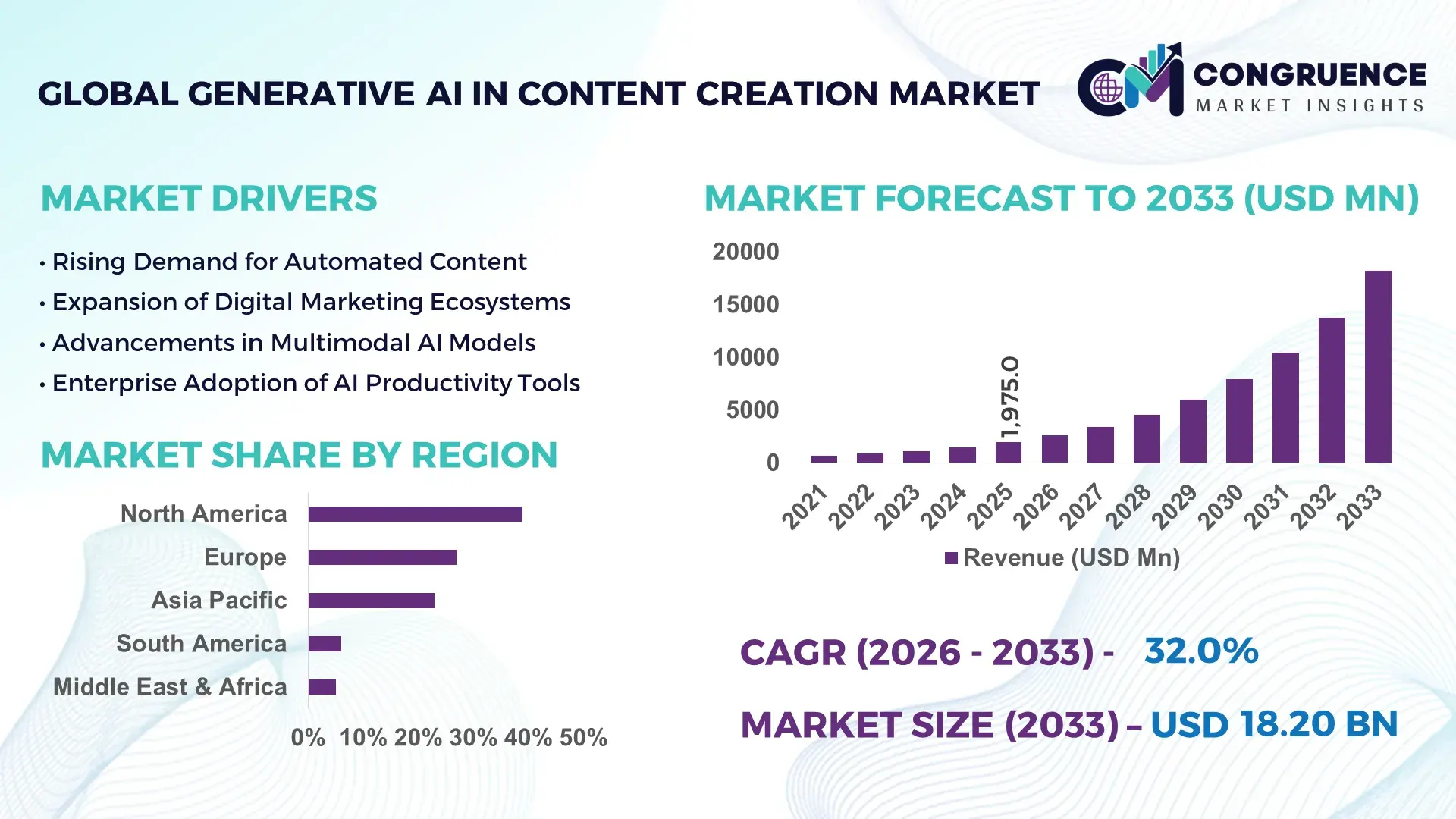

The Global Generative AI in Content Creation Market was valued at USD 1,975.0 Million in 2025 and is anticipated to reach a value of USD 18,203.7 Million by 2033 expanding at a CAGR of 32% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is expanding rapidly due to the accelerating adoption of AI-powered automation across marketing, media, entertainment, and enterprise communication workflows.

The United States represents the dominant country in the Generative AI in Content Creation Market, supported by strong production capacity, large-scale cloud infrastructure, and significant venture capital investments. In 2024 alone, U.S.-based generative AI startups secured over USD 23 billion in funding, accounting for more than 60% of global AI venture investment. Over 70% of Fortune 500 enterprises have integrated generative AI tools into marketing and content operations. The country hosts more than 35% of the world’s AI data centers, enabling high computational throughput for model training and deployment. Media, advertising, gaming, and e-commerce sectors collectively account for over 55% of enterprise generative AI deployments, with consumer adoption exceeding 65% among digital marketing professionals.

Market Size & Growth: Valued at USD 1,975.0 Million in 2025, projected to reach USD 18,203.7 Million by 2033 at a CAGR of 32%, driven by enterprise automation and scalable AI content workflows.

Top Growth Drivers: 68% enterprise AI adoption rate, 45% content production efficiency improvement, 40% reduction in creative turnaround time.

Short-Term Forecast: By 2028, AI-assisted content workflows are expected to reduce production costs by 35% and improve campaign performance metrics by 28%.

Emerging Technologies: Multimodal large language models, real-time AI video generation, and generative AI copilots integrated into SaaS platforms.

Regional Leaders: North America projected at USD 7,850.0 Million by 2033 with enterprise-scale deployment; Asia-Pacific at USD 5,420.0 Million driven by digital commerce growth; Europe at USD 3,960.0 Million supported by regulated AI frameworks.

Consumer/End-User Trends: Over 60% of marketing teams use AI for copywriting, while 48% of media firms deploy AI-driven video and design tools.

Pilot or Case Example: In 2024, a global e-commerce firm achieved 30% higher click-through rates using AI-generated personalized content.

Competitive Landscape: Market leader holds approximately 18% share, followed by major players including OpenAI, Google, Adobe, Microsoft, and Meta.

Regulatory & ESG Impact: AI governance frameworks mandate 100% transparency labeling in certain regions, accelerating responsible AI adoption.

Investment & Funding Patterns: Over USD 30 Billion invested globally in generative AI platforms during 2023–2025, with strong venture and strategic corporate funding.

Innovation & Future Outlook: Rapid integration of generative AI into CRM, ERP, and marketing automation systems is shaping scalable enterprise content ecosystems.

Generative AI in Content Creation Market applications are led by marketing & advertising (38%), media & entertainment (26%), and e-commerce (18%). Recent advancements in multimodal AI and synthetic video engines are reshaping digital campaigns. Regulatory focus on AI transparency and data protection is influencing deployment strategies. North America and Asia-Pacific drive consumption, while Europe emphasizes compliance-centric innovation. Enterprise integration and personalized content engines define the forward outlook.

The Generative AI in Content Creation Market holds strategic relevance as enterprises transition from manual creative processes to AI-augmented digital ecosystems. Organizations are embedding generative AI into marketing automation, customer engagement platforms, and internal knowledge management systems to enhance scalability and reduce operational latency. Multimodal generative AI delivers 45% faster content turnaround compared to traditional manual content production models, enabling real-time personalization at scale.

North America dominates in deployment volume, while Asia-Pacific leads in adoption velocity, with over 52% of digital-native enterprises actively piloting generative AI tools. By 2028, AI-driven personalization engines are expected to improve customer engagement rates by 30% and reduce campaign production costs by 35%. Firms are committing to ESG-aligned digital transformation goals, including 25% reduction in resource-intensive production processes by 2030 through AI-enabled digital workflows.

In 2024, a leading U.S.-based e-commerce enterprise achieved a 32% increase in content-driven conversion rates after implementing generative AI personalization engines. Comparatively, AI-powered creative optimization platforms deliver 40% performance improvement compared to conventional A/B testing frameworks.

Strategically, enterprises are building proprietary AI models trained on first-party data to enhance differentiation and compliance. As regulatory oversight increases, explainable AI and responsible content generation frameworks are becoming integral. The Generative AI in Content Creation Market is positioning itself as a pillar of operational resilience, regulatory alignment, and sustainable digital growth across industries.

The Generative AI in Content Creation Market is characterized by rapid technological innovation, enterprise-scale experimentation, and increasing integration into digital value chains. Organizations across media, retail, education, and corporate communications are adopting AI-generated text, video, audio, and design solutions to improve scalability and reduce manual intervention. The proliferation of cloud computing infrastructure and high-performance GPUs has enabled faster model training cycles, while API-based deployments allow seamless integration into SaaS platforms. Demand is particularly strong in digital advertising, where personalization and real-time engagement drive competitive advantage. Simultaneously, regulatory scrutiny around AI-generated misinformation and data privacy is shaping governance frameworks. Vendor competition is intensifying, with firms differentiating through proprietary datasets, multimodal capabilities, and enterprise-grade compliance features.

Enterprise automation is a primary driver reshaping the Generative AI in Content Creation Market. Over 68% of global enterprises are investing in AI-based workflow automation to streamline marketing, product documentation, and customer communication. AI-generated copy and design tools can reduce manual content development time by up to 45%, enabling marketing teams to execute multi-channel campaigns simultaneously. In digital advertising, AI-personalized content improves click-through rates by 25–35%, directly influencing performance metrics. Additionally, AI-powered chatbots and dynamic content engines are handling over 50% of initial customer engagement interactions in large enterprises. The integration of generative AI within CRM and marketing automation platforms further accelerates deployment, reducing operational bottlenecks and increasing campaign scalability across geographies.

Data privacy regulations and intellectual property (IP) complexities present notable restraints. Over 60% of enterprises cite compliance risks as a barrier to full-scale AI deployment. Strict data protection laws require transparent data sourcing and user consent management, increasing compliance costs. Additionally, lawsuits and disputes regarding AI-trained copyrighted content have created uncertainty in creative industries. Around 42% of media firms report hesitation in deploying AI-generated materials due to IP ambiguity. The need for secure, explainable AI systems also raises infrastructure expenses, particularly for enterprises handling sensitive customer or financial data. These regulatory and legal complexities slow enterprise-wide implementation despite technological readiness.

Hyper-personalization represents a significant growth avenue. Approximately 72% of consumers prefer personalized digital experiences, and AI-driven content engines can tailor messaging in real time across web, mobile, and social platforms. Retailers deploying generative AI for product descriptions and recommendations report up to 30% higher engagement rates. Video-based AI personalization tools are expanding rapidly, enabling localized marketing in multiple languages simultaneously. Emerging economies in Asia-Pacific are witnessing over 50% annual increases in AI-driven marketing pilots. Furthermore, generative AI in education and corporate training—producing adaptive learning modules—opens untapped enterprise verticals beyond marketing and entertainment.

Generative AI systems require high computational power, advanced GPUs, and scalable cloud infrastructure. Training large language models can consume thousands of megawatt-hours of electricity annually, increasing operational expenditure. Around 48% of mid-sized enterprises report budget constraints related to AI infrastructure upgrades. Additionally, latency issues in real-time content generation affect deployment in regions with limited cloud infrastructure. The shortage of skilled AI engineers further compounds operational complexity, with demand for AI talent increasing by over 35% year-over-year. These technical and financial challenges limit rapid scalability for smaller organizations despite strong market demand.

Multimodal AI Integration Across Text, Video, and Audio (65% Enterprise Adoption): Over 65% of large enterprises are piloting multimodal generative AI systems capable of producing synchronized text, video, and voice outputs. AI-generated video content production time has decreased by 40%, while automated voice synthesis accuracy exceeds 90%, enabling scalable multimedia campaigns across global markets.

AI-Powered Real-Time Personalization Improving Engagement by 30%: Advanced generative AI engines now analyze behavioral data within milliseconds, increasing campaign engagement rates by 28–32%. Approximately 58% of e-commerce platforms have integrated AI-driven personalization tools into customer journeys, enhancing retention and repeat purchase rates.

Expansion of AI Copilots in SaaS Platforms (50% Workflow Automation): AI copilots embedded in productivity and marketing software now automate up to 50% of content drafting tasks. Adoption among digital marketing agencies has surpassed 62%, with workflow cycle times reduced by nearly 35% compared to traditional editing processes.

Responsible AI and Content Authenticity Frameworks (100% Labeling in Regulated Markets): Regulatory mandates in several developed markets require 100% labeling of AI-generated political and advertising content. Over 55% of enterprises have implemented AI governance dashboards to monitor bias, transparency, and ethical compliance metrics, ensuring sustainable and compliant AI-driven content ecosystems.

The Generative AI in Content Creation Market is segmented by type, application, and end-user, reflecting the technology’s expanding role across digital ecosystems. By type, solutions include text generation models, vision-language models, audio-text systems, video-language models, and multimodal foundation models. Enterprises increasingly demand multimodal capabilities that combine text, image, and video outputs within unified architectures. By application, marketing and advertising lead deployments, followed by media & entertainment, e-commerce, gaming, education, and corporate communications. AI-generated copy, automated video editing, synthetic voiceovers, and dynamic personalization engines are core functionalities across these verticals. End-user segmentation highlights strong adoption among large enterprises, digital-native firms, media houses, and retail platforms, while SMEs are rapidly scaling pilot projects. Adoption intensity varies regionally, with North America emphasizing enterprise-grade integrations and Asia-Pacific focusing on high-volume digital commerce deployments.

The Generative AI in Content Creation Market by type includes text generation models, vision-language models, audio-text systems, video-language models, and multimodal foundation models. Text generation models currently account for approximately 38% of total adoption due to their extensive use in automated copywriting, chatbots, documentation, and SEO content production. Vision-language models represent around 27%, widely adopted in advertising design and social media automation. Audio-text systems hold nearly 18%, primarily deployed in podcast transcription and AI voice synthesis. However, video-language models are the fastest-growing segment, expanding at an estimated CAGR of 36%, driven by demand for automated video summaries, digital avatars, and AI-generated promotional media. Adoption in video-language systems is expected to surpass 30% by 2033 as enterprises prioritize short-form video marketing. Multimodal foundation models collectively contribute about 17%, gaining traction in enterprises seeking integrated content pipelines combining text, image, and video outputs within single AI frameworks.

In 2025, a leading global streaming platform implemented video-language generative AI to auto-generate multilingual captions and scene summaries for over 12 million users, significantly enhancing accessibility and engagement.

By application, marketing and advertising dominate with nearly 41% share, as enterprises leverage AI to automate campaign copy, ad creatives, and customer personalization workflows. Media & entertainment account for approximately 24%, deploying AI for script drafting, post-production editing, and digital character creation. E-commerce contributes around 16%, driven by automated product descriptions and dynamic recommendations. Gaming and interactive media hold 9%, while education and corporate training collectively account for 10%. While marketing leads in adoption, media & entertainment represents the fastest-growing application segment, expanding at an estimated CAGR of 34%, fueled by AI-assisted video production and virtual influencer ecosystems. Over 62% of digital marketing agencies report daily reliance on generative AI tools for campaign execution. In 2025, more than 44% of enterprises globally reported piloting generative AI systems for customer engagement platforms. Additionally, over 58% of Gen Z consumers indicate higher brand engagement when AI-driven personalized content is integrated.

In 2025, a national public broadcasting network deployed generative AI to automate subtitle generation across 18 regional channels, improving processing efficiency by 40% and expanding multilingual reach to over 8 million viewers.

Large enterprises represent the leading end-user segment, accounting for approximately 46% of total adoption, supported by advanced IT infrastructure and proprietary AI model customization. Technology companies and digital marketing agencies are the primary contributors within this group. SMEs account for nearly 28%, increasingly adopting subscription-based AI platforms for scalable content production. Media & entertainment companies represent 15%, while retail and e-commerce enterprises contribute about 11%. Although large enterprises lead overall adoption, SMEs are the fastest-growing end-user segment, expanding at an estimated CAGR of 35%, driven by cloud-based AI services and lower entry barriers. In 2025, over 52% of mid-sized enterprises reported integrating AI-driven content tools into customer communication workflows. Furthermore, 61% of digitally native startups rely on AI-assisted branding and campaign management solutions.

In 2025, a national digital innovation agency reported that AI adoption among small and mid-sized retail enterprises increased by 24%, enabling over 600 businesses to enhance customer analytics and automate promotional content workflows.

North America accounted for the largest market share at 39% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 34% between 2026 and 2033.

North America’s leadership is supported by over 70% enterprise-level AI deployment across marketing and digital communication platforms, with more than 65% of Fortune 500 companies integrating generative AI tools into daily workflows. Europe holds approximately 27% share, driven by strong regulatory alignment and over 55% of enterprises adopting AI governance frameworks. Asia-Pacific represents nearly 23% of global adoption, with digital commerce penetration exceeding 68% in major economies such as China and India. South America accounts for around 6%, supported by increasing digital advertising expenditure growth of over 18% annually. The Middle East & Africa contribute close to 5%, with government-backed AI modernization initiatives increasing enterprise AI investments by more than 20% year-over-year in key innovation hubs.

North America holds approximately 39% of the global Generative AI in Content Creation Market share, making it the largest regional contributor. The region benefits from strong demand across marketing, media & entertainment, healthcare communications, and financial services. Over 72% of large enterprises in the U.S. and Canada report integrating AI-driven content tools into marketing automation systems. Regulatory frameworks promoting transparent AI labeling and data governance are shaping responsible adoption. Government-backed AI research funding programs exceeding USD 2 billion annually further strengthen innovation pipelines. Technological advancements such as multimodal AI, real-time personalization engines, and AI copilots embedded in SaaS platforms are accelerating enterprise deployment. A prominent regional player, OpenAI, continues to expand enterprise-grade generative AI APIs, supporting over 2 million developers globally. Consumer behavior reflects high trust in AI-assisted services, with 64% of digital users engaging with AI-powered chat or content tools weekly. Adoption is particularly strong in healthcare and finance, where automated documentation reduces processing time by nearly 30%.

Europe accounts for roughly 27% of the Generative AI in Content Creation Market. Key markets include Germany, the United Kingdom, and France, which collectively represent over 60% of regional AI deployments. Regulatory oversight through structured AI governance frameworks has led to 58% of enterprises implementing explainable AI mechanisms in digital content workflows. Sustainability initiatives promote energy-efficient data centers, reducing AI training energy consumption by up to 20% in advanced facilities. Emerging technologies such as AI-based translation engines and multilingual content automation tools are widely adopted, especially in cross-border digital commerce. A regional technology provider, SAP, integrates generative AI copilots within enterprise resource planning platforms, enabling automated report generation and workflow optimization. Consumer behavior reflects heightened sensitivity to privacy and transparency, with 62% of users favoring platforms that clearly label AI-generated content. This compliance-driven ecosystem enhances long-term market stability.

Asia-Pacific represents nearly 23% of global market volume and ranks as the fastest-expanding regional ecosystem. China, India, and Japan are the top consuming countries, collectively contributing over 75% of regional AI deployments. The region hosts more than 50 major AI innovation hubs and technology parks focused on large language model research and digital media applications. E-commerce penetration exceeds 68% in leading economies, driving strong demand for AI-generated product descriptions, localized marketing content, and live-stream commerce automation. Cloud infrastructure expansion across Asia-Pacific has increased AI data center capacity by over 25% in the past two years. A leading regional technology company, Baidu, is deploying generative AI models for enterprise marketing and search optimization tools. Consumer behavior trends show that over 70% of mobile-first users engage with AI-powered recommendation systems daily, reflecting strong adoption in mobile commerce and social platforms.

South America holds approximately 6% of the Generative AI in Content Creation Market share, with Brazil and Argentina serving as primary contributors. Brazil accounts for nearly 55% of the regional adoption due to its expanding digital advertising sector, which has grown by over 18% annually. Infrastructure modernization initiatives and improved cloud connectivity are supporting scalable AI deployment. Governments are introducing digital transformation incentives to enhance technology adoption in SMEs. Local media houses increasingly deploy AI-powered translation and subtitle generation systems to support multilingual audiences across Spanish and Portuguese markets. Regional consumer behavior indicates that 59% of online users engage with AI-curated content recommendations weekly. Demand is closely tied to media production, digital marketing, and localized e-commerce campaigns, where AI reduces content production timelines by up to 35%.

The Middle East & Africa contribute nearly 5% to the global Generative AI in Content Creation Market. The UAE and South Africa are leading growth countries, supported by national AI strategies and digital economy initiatives. Government-led AI programs have increased enterprise technology investments by over 20% annually in the Gulf region. Demand is particularly strong in sectors such as oil & gas communications, tourism marketing, and public sector digital engagement. Technological modernization trends include smart city platforms integrating AI-generated public communication systems and automated multilingual content engines. A UAE-based technology incubator recently supported over 150 AI startups focused on digital content and language models. Consumer adoption varies, with 54% of urban digital users interacting with AI-generated customer service tools, reflecting gradual but steady uptake across enterprise and public-facing services.

United States – 34% Market Share: It leads due to high enterprise adoption, advanced AI infrastructure, and strong venture capital investment exceeding global averages.

China – 21% Market Share: It is driven by large-scale digital commerce ecosystems, strong government-backed AI development programs, and extensive mobile-first consumer engagement.

The Generative AI in Content Creation Market is moderately consolidated, with over 120 active technology vendors competing across model development, API services, and verticalized AI content platforms. The top five companies collectively account for approximately 58% of total market share, reflecting strong brand positioning, proprietary model capabilities, and enterprise-scale infrastructure advantages. Market leaders differentiate through multimodal model architectures, enterprise-grade compliance tools, and scalable cloud integrations.

Strategic partnerships between AI model developers and cloud hyperscalers have intensified, with more than 65% of leading vendors integrating directly into CRM, ERP, and marketing automation ecosystems. Over 40 major product launches were recorded between 2024 and 2025, focusing on real-time video generation, synthetic voice cloning, and AI copilots embedded into productivity suites. Mergers and acquisitions activity has increased by 22% year-over-year, as firms seek proprietary datasets and specialized AI research teams to enhance model training quality.

Innovation trends emphasize multimodal large language models, retrieval-augmented generation (RAG) systems, and domain-specific fine-tuned models for healthcare, finance, and legal documentation. Competitive intensity is further shaped by AI governance compliance, with over 55% of vendors introducing explainability dashboards and watermarking features. The market environment remains dynamic, driven by rapid iteration cycles, enterprise customization requirements, and global AI infrastructure expansion.

Microsoft

Meta Platforms

Amazon Web Services (AWS)

NVIDIA

Anthropic

Stability AI

IBM

Salesforce

Baidu

Alibaba Cloud

Canva

Jasper AI

Runway AI

The Generative AI in Content Creation Market is driven by rapid advancements in multimodal foundation models, high-performance GPU acceleration, and scalable cloud-native architectures. Modern large language models (LLMs) now exceed hundreds of billions of parameters, enabling contextual accuracy improvements of over 35% compared to earlier transformer-based systems. Multimodal systems integrating text, image, audio, and video processing have achieved latency reductions of up to 40%, enabling near real-time content generation for enterprise workflows.

GPU clusters equipped with advanced AI accelerators now process training datasets exceeding 5 petabytes, significantly improving model fine-tuning efficiency. Retrieval-Augmented Generation (RAG) architectures enhance factual grounding by integrating enterprise databases, reducing hallucination rates by nearly 25%. Synthetic voice models now achieve over 95% phonetic accuracy, while AI-generated video engines reduce editing time by up to 50%.

Edge AI deployment is emerging as a strategic differentiator, allowing localized content generation with latency under 200 milliseconds in mobile environments. Furthermore, AI watermarking and content authentication technologies are gaining traction, with 60% of enterprise vendors implementing traceability features to comply with transparency regulations.

Low-code and no-code AI platforms are also accelerating SME adoption, enabling over 45% faster deployment cycles. As enterprise ecosystems demand interoperability, API-based AI orchestration frameworks are enabling seamless integration across marketing, design, analytics, and workflow automation systems. These technology advancements collectively position generative AI as a core digital transformation enabler.

• In March 2025, Adobe expanded its GenStudio content supply chain platform with new AI-driven workflow optimization, unified data interfaces, content production agents, and advanced APIs for video and 3D workflows, enabling marketing teams to scale personalized content creation across channels with AI agents integrated into Adobe Experience and Creative Clouds. Source: www.adobe.com

• At Adobe MAX 2025 in October 2025, Adobe unveiled AI assistants and multimodal models across Creative Cloud, including Firefly Image Model 5, AI Assistants in Photoshop and Express, and integrations with partner models from Google, OpenAI, Runway, ElevenLabs, and Topaz Labs, aimed at empowering creative professionals with conversational, prompt-based generative content workflows. Source: www.adobe.com

• In December 2025, OpenAI released its GPT-5.2 model, the company’s most capable generative AI yet, offering enhanced long-context comprehension, multimodal capabilities, and professional productivity improvements for tasks in content creation, coding, presentations, and business workflows. This model supports improved enterprise adoption. Source: www.barrons.com

• Throughout 2025, OpenAI’s official product updates included enhanced ChatGPT image generation and task automation features, introducing an upgraded ChatGPT Images experience on web and mobile with improved precision and usability for creative content generation and automated tasks such as scheduled prompts and Pulsed task automation. Source: www.help.openai.com

The Generative AI in Content Creation Market Report provides comprehensive coverage of technological, application-based, and regional dimensions shaping industry development. The scope includes segmentation by type, covering text generation models, vision-language systems, audio-text engines, video-language architectures, and multimodal foundation models. Application coverage spans marketing & advertising, media & entertainment, e-commerce, gaming, education, and enterprise communications, collectively representing over 90% of AI-driven content deployment use cases globally.

Geographically, the report evaluates five major regions—North America, Europe, Asia-Pacific, South America, and Middle East & Africa—representing 100% of global adoption patterns, with country-level insights for more than 15 key markets. The analysis includes enterprise adoption rates exceeding 70% in developed economies and rapid SME integration trends across emerging markets.

The report further explores infrastructure readiness indicators such as AI data center expansion exceeding 25% annually in high-growth regions and GPU deployment density across enterprise clusters. It also addresses regulatory compliance frameworks, AI transparency mandates, and ESG-aligned digital transformation strategies influencing purchasing decisions.

Emerging segments such as AI-generated virtual influencers, synthetic media authentication tools, and industry-specific fine-tuned language models are included to provide forward-looking visibility. The scope equips decision-makers with structured insights into competitive positioning, innovation trends, deployment models, and enterprise integration strategies shaping the Generative AI in Content Creation Market landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,975.0 Million |

| Market Revenue (2033) | USD 18,203.7 Million |

| CAGR (2026–2033) | 32% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | OpenAI; Google; Adobe; Microsoft; Meta Platforms; Amazon Web Services (AWS); NVIDIA; Anthropic; Stability AI; IBM; Salesforce; Baidu; Alibaba Cloud; Canva; Jasper AI; Runway AI |

| Customization & Pricing | Available on Request (10% Customization Free) |