Reports

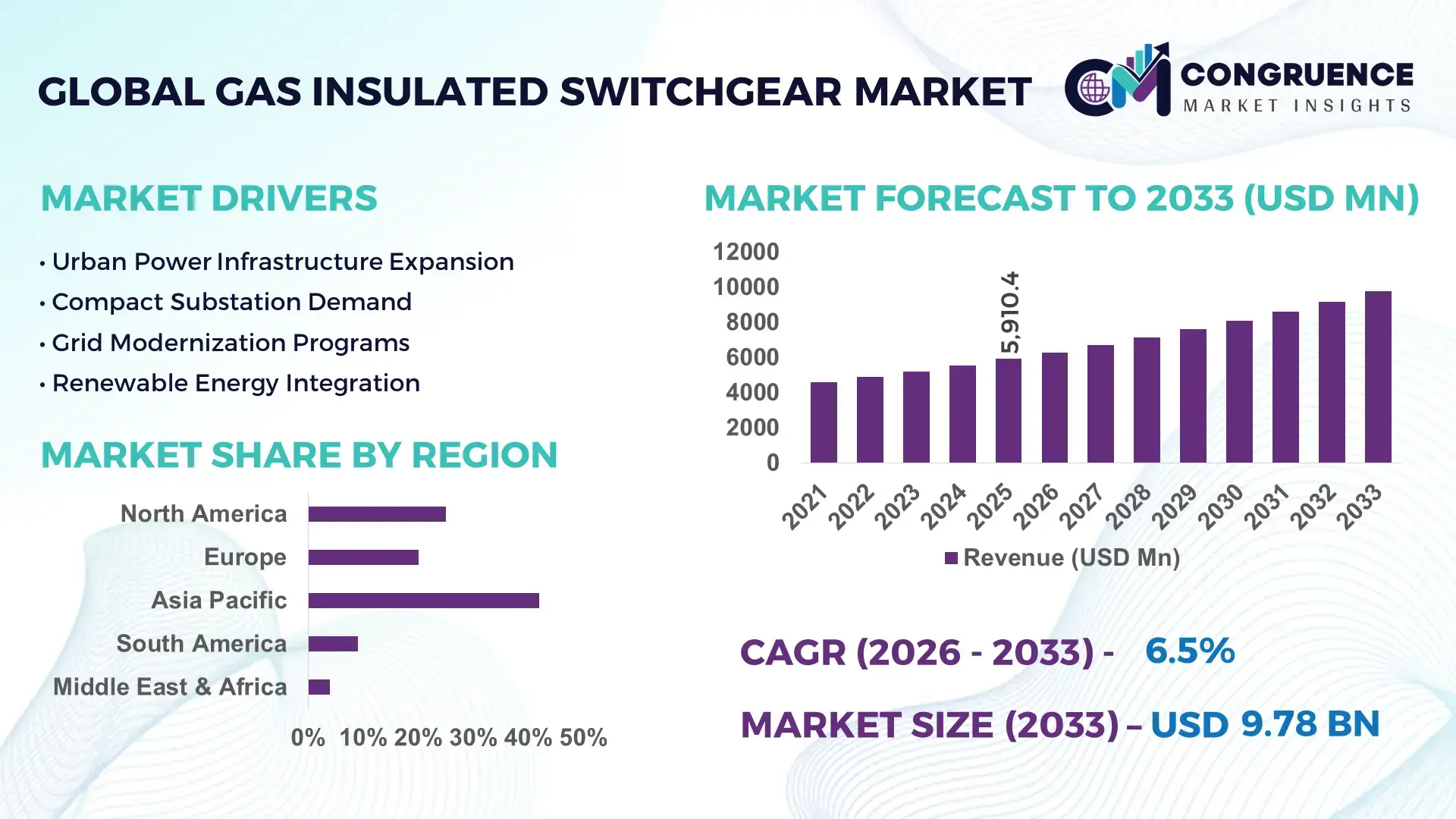

The Global Gas Insulated Switchgear Market was valued at USD 5910.44 Million in 2025 and is anticipated to reach a value of USD 9781.76 Million by 2033 expanding at a CAGR of 6.5% between 2026 and 2033. This growth is driven by rapid grid modernization, increasing renewable energy integration, and demand for compact, reliable power distribution systems.

China leads global Gas Insulated Switchgear deployment with extensive production capacity across high-voltage and medium-voltage units, backed by government grid expansion plans and renewable energy projects. China’s utilities deployed over 15,000 GIS units in recent years and manufacturers are advancing SF₆-free and compact GIS designs, with production investment rising annually to support urban substations and industrial power networks.

• Market Size & Growth: Market valued at ~USD 5.91 B in 2025, projected to ~USD 9.78 B by 2033 at a 6.5% CAGR, driven by infrastructure upgrades and renewable grid integration.

• Top Growth Drivers: Urbanization adoption ~48%, renewable integration ~35%, compact space efficiency ~30%.

• Short-Term Forecast: By 2028, GIS installations to achieve ~20% performance gain in network reliability metrics.

• Emerging Technologies: SF₆‑free insulation systems; IoT-enabled predictive monitoring; modular compact GIS solutions.

• Regional Leaders: Asia‑Pacific ~USD 4.5 B by 2033 with smart grid expansions; Europe ~USD 2.1 B with eco‑friendly GIS adoption; North America ~USD 1.8 B with retrofitting and HV infrastructure upgrades.

• Consumer/End‑User Trends: Utilities prioritize compact GIS for urban substations; industrial and commercial sectors adopt digital diagnostics for asset uptime.

• Pilot or Case Example: 2025 smart GIS deployments reduced outage downtime by ~15% in select metropolitan grids.

• Competitive Landscape: Market leader ABB ~11–12% share with global installations, followed by Siemens, Schneider Electric, Mitsubishi Electric, GE.

• Regulatory & ESG Impact: Stricter SF₆ regulations in EU and incentives for green grid technologies accelerate adoption of eco‑friendly GIS variants.

• Investment & Funding Patterns: Recent investments exceed USD 500 M in new manufacturing lines and digital GIS product R&D globally.

• Innovation & Future Outlook: Continued integration of digital monitoring, eco‑gas technologies, and hybrid GIS expected to shape next decade growth.

The Gas Insulated Switchgear Market continues evolving with strong contributions from transmission & distribution, infrastructure, and industrial sectors. High‑voltage GIS systems dominate deployments, supporting long‑distance power transfer and urban grid needs. Recent innovations include SF₆ alternatives and digital‑first switchgear products enhancing operational safety and reducing lifecycle costs. Regulatory emphasis on reducing greenhouse gas emissions and rising investments in smart grid and renewable integration further propel market expansion. Regional consumption patterns show Asia‑Pacific leading in unit installations and technology adoption, with Europe focusing on eco‑compliant solutions and North America on grid modernization. Future trends include wider adoption of predictive maintenance, compact substations, and GIS solutions tailored for renewable energy corridors.

The Gas Insulated Switchgear Market holds strategic importance as utilities and grid operators worldwide pursue enhanced reliability, compact infrastructure, and environmental compliance amid rapid electrification and renewable energy integration. Next‑generation clean‑air and vacuum‑insulated GIS delivers approximately 15–25% improvement in lifecycle environmental impact and operational safety compared to older SF₆‑based systems, accelerating adoption in regions with strict emission standards. Asia‑Pacific dominates in installation volume, while Europe leads in adoption with about 40% of utilities implementing next‑generation SF₆‑free or hybrid GIS technologies. By 2028, AI‑driven predictive maintenance and IoT‑enabled diagnostics are expected to improve substation uptime by over 20%, reducing unplanned outages and operational costs.

Firms are committing to ESG improvements such as a 30% reduction in SF₆ emissions and enhanced recyclability by 2030. In 2025, a major European utility achieved a 22% reduction in downtime through integration of digital sensor networks and advanced analytics within its GIS assets, setting a benchmark for performance gains. Strategic pathways include continued R&D investment in eco‑gas mixtures with global warming potential below 1, expanding digital integration for real‑time grid insights, and scaling manufacturing capacity in emerging economies. The Gas Insulated Switchgear Market will remain a pillar of resilience, compliance, and sustainable growth as grids evolve toward smarter, low‑carbon power systems.

Space efficiency and reliability are crucial drivers of Gas Insulated Switchgear demand, especially in highly urbanized and industrial regions. GIS offers up to 90% reduction in footprint compared to traditional air‑insulated alternatives, enabling utilities to install substations in space‑constrained metropolitan areas and industrial complexes. Utilities in major Asian cities have collectively deployed thousands of compact GIS units to optimize land use and improve system resilience. Furthermore, digital GIS with IoT sensors and predictive diagnostics enhance operational transparency, allowing operators to detect faults earlier and reduce unplanned outages. For example, smart GIS installations have been reported to cut outage durations by more than 20% in specific grid segments, reflecting how performance improvements directly influence procurement decisions and long‑term infrastructure planning.

High initial capital expenditure and complex installation requirements present significant restraints for Gas Insulated Switchgear adoption. GIS systems involve precision engineering, specialized materials, and detailed civil works that elevate costs relative to simpler alternatives. For many utilities and industrial operators, especially in budget‑constrained regions, these upfront expenses deter large‑scale deployment despite long‑term operational advantages. In addition, installation often requires highly trained technicians and extended project timelines, increasing labor costs and coordination complexity. Complex compliance and inspection protocols related to environmental regulations can further delay deployment. For cost‑sensitive infrastructure projects in developing economies, these financial and logistical hurdles continue to limit GIS uptake, even where long‑term benefits are acknowledged in strategic planning.

The rapid expansion of renewable energy capacity and smart grid modernization initiatives presents significant opportunities for the Gas Insulated Switchgear Market. Grid operators integrating variable solar and wind generation require flexible switchgear capable of handling dynamic power flows and maintaining grid stability. GIS solutions, particularly those with digital monitoring and control features, enable real‑time system responsiveness and predictive maintenance. A substantial portion of new renewable projects specify advanced GIS to support efficient power evacuation and distribution. Additionally, smart grid projects in multiple countries are incorporating GIS with IoT connectivity to enhance network visibility and enable automated control functions. These trends open opportunities for vendors to offer differentiated products that support decarbonization goals and improved grid asset management, extending GIS applicability across both new builds and retrofit programs.

Regulatory complexity and the lack of universal technical standards present ongoing challenges for the Gas Insulated Switchgear Market. While environmental regulations push stakeholders toward greener insulating technologies, inconsistent regional standards for SF₆ alternatives at high voltage levels create certification and interoperability hurdles. Utilities and manufacturers must navigate differing grid codes, testing protocols, and compliance frameworks, which prolong product development cycles and deployment timelines. Retrofitting existing installations with SF₆‑free or hybrid GIS solutions adds complexity, as older infrastructure may require civil modifications and planned downtime. Moreover, supply‑chain constraints for alternative insulating media and advanced components can lead to project delays and increased procurement risk. These challenges, combined with evolving regulatory expectations, demand strategic coordination among industry players to establish harmonized standards and streamline adoption pathways for next‑generation GIS technologies.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated GIS solutions is transforming infrastructure development. Approximately 55% of new high-voltage substation projects report cost reductions and 30% shorter installation times due to off-site prefabrication. Automated pre-bending and cutting of GIS components reduce labor requirements and minimize on-site errors. Europe and North America lead adoption, with over 40% of utilities integrating prefabricated GIS modules into urban substation projects.

• Expansion of Digital Monitoring and Predictive Maintenance: Utilities increasingly rely on digital sensors and predictive maintenance systems integrated into GIS units. In 2025, more than 35% of high-voltage installations globally utilized IoT-enabled monitoring to reduce unplanned downtime by 20% and extend equipment lifecycle by 15%. These smart systems facilitate early fault detection and remote diagnostics, enhancing operational reliability and cost-efficiency across transmission and distribution networks.

• Shift to Eco-Friendly Insulating Technologies: SF₆-free and low-global-warming-potential alternatives are gaining traction, with adoption reaching 25% of new GIS installations in Europe and Asia. These systems reduce greenhouse gas emissions by up to 70% per unit and align with regulatory mandates targeting sustainability. Manufacturers are developing hybrid designs combining traditional SF₆ and eco-gases to achieve measurable reductions while maintaining performance standards.

• Integration with Renewable Energy Grids: GIS solutions are increasingly deployed to support renewable energy integration. Over 40% of new wind and solar substations in Asia-Pacific now include GIS to manage variable power flows and maintain grid stability. High-voltage GIS enables faster switching, reduces fault propagation by 15%, and supports automated load balancing, providing critical infrastructure for growing renewable capacities.

The Gas Insulated Switchgear market is systematically segmented to reflect differentiated demand patterns across product types, applications, and end‑user categories. By type, the market ranges from high‑voltage systems designed for transmission networks to medium‑ and low‑voltage units tailored for urban distribution and commercial power systems, with hybrid configurations increasingly used for flexible infrastructure expansion. Application segmentation highlights GIS use in grid transmission and distribution, renewable energy integration, industrial power networks, and smart grid modernization. End‑user segmentation identifies utilities, industrial sectors, commercial infrastructure, and specialized installations like railways and data centers as distinct camps, each with unique reliability and performance requirements. This segmentation enables detailed analysis of how specific GIS technologies align with operational priorities, from space‑constrained urban substations to high‑capacity long‑distance transmission corridors, offering decision‑makers nuanced insights into deployment patterns and growth drivers across the power ecosystem.

High‑voltage GIS currently accounts for about 60% of global installations, reflecting its central role in voltage classes above 72.5 kV for transmission and substation projects. High‑voltage systems are preferred for long‑distance grid links and large utility networks due to their superior insulation performance and compact footprint compared to traditional alternatives, supporting consistent performance across harsh environments. Medium‑voltage GIS represents approximately 25–37% of deployments, widely used in urban distribution grids, commercial buildings, and industrial facilities; the installed base for medium‑voltage units exceeds 180,000 globally, with utilities comprising over 60% of end users. Low‑voltage GIS, though smaller (around 10%), serves niche applications in compact infrastructures such as hospitals, airports, and metro systems. Hybrid GIS solutions combining air‑insulated and gas‑insulated modules are emerging, with Europe recording hundreds of hybrid projects in rail electrification and flexible expansion sites.

Transmission applications dominate GIS usage with roughly 58% of unit share, as utilities prioritize reliable, high‑density switchgear for bulk power movement across regions. Within transmission, GIS supports extra‑high‑voltage corridors and interconnection links that demand robust dielectric performance and low physical footprint, especially in urban spines and cross‑border grids. Distribution networks account for a significant, though smaller, portion of GIS applications, where medium voltage systems address space constraints and enhanced safety protocols in city substations. Renewable energy integration is an increasingly visible application, with solar and wind farm substations relying on GIS to handle variable power inputs and maintain stability; in 2023, over 22% of new global GIS deployments were associated with renewable projects. Industrial applications, including manufacturing, mining, and petrochemical sectors, also contribute to GIS uptake, leveraging its resilience and low maintenance in demanding settings.

Utilities remain the leading end‑user segment, capturing approximately 45% of GIS unit installations, driven by grid modernization and the need for reliable transmission and distribution infrastructure. Utility demand spans both high‑voltage and medium‑voltage GIS systems, with a focus on reducing outages and accommodating renewable generation sources. Industrial sectors, including oil & gas, manufacturing, and heavy industries, follow utilities with over 30% contribution in high‑voltage GIS unit deployment, leveraging switchgear’s durability under harsh operational conditions. Commercial infrastructure, encompassing data centers, metros, and airports, constitute the remaining share with around 25% of installations, prioritizing uninterrupted power and compact solutions. Fast growth is seen in infrastructure applications where GIS enables power continuity in constrained environments.

Asia-Pacific accounted for the largest market share at 42% in 2025; however, Europe is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

In 2025, Asia-Pacific deployed over 15,500 GIS units across China, India, and Japan, supporting both transmission and distribution infrastructure. Europe recorded over 6,200 installations, driven by renewable integration and urban substation modernization. North America installed 5,400 units, with a focus on digitalized GIS for smart grids and industrial applications. South America contributed approximately 1,800 units, while Middle East & Africa accounted for 1,200 units in the same year. Asia-Pacific leads in high-voltage GIS adoption with over 55% of projects above 72.5 kV, while Europe emphasizes eco-friendly SF₆-free systems, achieving adoption by 40% of utilities. North America focuses on predictive maintenance with digital sensors in 35% of urban substations, and South America is integrating GIS in over 60% of new renewable energy projects.

How is advanced infrastructure shaping high-voltage distribution and adoption?

North America holds approximately 28% of the GIS market volume in 2025, driven by high adoption in utilities, industrial plants, and commercial facilities. Key industries include power transmission, healthcare, and finance, where uninterrupted energy is critical. Regulatory initiatives promoting grid modernization and incentives for low-emission technologies have increased GIS adoption. Digital transformation trends such as IoT-enabled monitoring and predictive maintenance are enhancing reliability across substations. Local players, such as ABB and Schneider Electric, are deploying advanced compact GIS units with remote monitoring for urban networks. North American consumers favor high-performance GIS in healthcare and finance sectors, with over 40% of urban substations integrating digital diagnostic systems.

What strategies are driving sustainable and regulatory-compliant GIS adoption?

Europe represents roughly 22% of GIS installations in 2025, led by Germany, the UK, and France. Regulatory bodies are driving demand for SF₆-free or low-GWP switchgear, with sustainability initiatives shaping product design and adoption. Emerging technologies, including hybrid GIS and IoT monitoring, are increasingly deployed, accounting for nearly 35% of new projects. Siemens and Schneider Electric are investing in digital GIS solutions for smart grids and urban retrofits. Regional consumer behavior emphasizes regulatory compliance, resulting in high demand for explainable, eco-friendly GIS solutions and proactive maintenance across utilities and industrial networks.

How are growing infrastructure projects boosting GIS deployment and innovation?

Asia-Pacific remains the largest GIS market, accounting for 42% of global installations in 2025. China, India, and Japan lead consumption, with China alone deploying over 8,500 high-voltage GIS units to expand ultra-high-voltage transmission. Rapid urbanization and industrialization drive demand for compact and digitalized GIS, while manufacturing hubs integrate automated assembly lines to improve production efficiency. Local players such as State Grid Corporation of China are investing in next-generation SF₆-free GIS systems. Regional consumers prioritize high-density urban substations and industrial power resilience, with over 50% of new installations in metropolitan areas adopting advanced digital monitoring.

How are energy initiatives and government policies shaping GIS adoption?

South America contributed approximately 1,800 GIS units in 2025, with Brazil and Argentina as key markets. Infrastructure expansion and energy sector modernization are primary drivers, supported by government incentives for renewable energy and international trade partnerships. Local players, including CPFL Energia, are adopting modular GIS solutions for urban substations. Regional consumers emphasize grid reliability and renewable integration, with over 60% of new projects including GIS for solar and wind farms. Industrial facilities are also increasingly leveraging compact GIS to improve operational uptime in space-constrained environments.

What factors are driving GIS growth in oil-rich and developing economies?

Middle East & Africa accounted for approximately 1,200 GIS units in 2025. Major growth countries include UAE, Saudi Arabia, and South Africa, driven by oil & gas, construction, and urban infrastructure projects. Technological modernization focuses on digital monitoring and remote-control GIS solutions, while local regulations encourage low-emission and sustainable installations. ABB and Siemens are deploying advanced GIS in new smart substations. Regional consumers prioritize reliability in energy-intensive sectors, with over 35% of industrial and commercial installations incorporating predictive maintenance features and eco-friendly insulating alternatives.

China: 25% market share – Strong production capacity and large-scale utility deployment support extensive GIS adoption.

Germany: 12% market share – High regulatory compliance and early adoption of SF₆-free technologies drive GIS installations.

The Gas Insulated Switchgear market is moderately consolidated, with approximately 35–40 active global competitors operating across high-voltage, medium-voltage, and hybrid GIS segments. The top five companies—ABB, Siemens, Schneider Electric, Mitsubishi Electric, and GE—collectively account for nearly 55–57% of total installations worldwide, reflecting strong brand presence and advanced technological capabilities. Competitive strategies include product innovation, strategic partnerships, and targeted mergers or acquisitions to expand regional footprints. In 2025, over 150 new product launches were reported globally, emphasizing SF₆-free solutions, compact designs, and digital monitoring integration. Partnerships between manufacturers and utilities are increasingly common, with more than 60 large-scale projects initiated in Asia-Pacific and Europe alone. Innovation trends shaping competition include IoT-enabled predictive maintenance, hybrid GIS configurations, and eco-friendly insulating technologies, which are becoming key differentiators. Smaller regional players focus on niche markets or retrofit projects, contributing to market fragmentation in localized areas. Overall, the competitive landscape balances dominance by global incumbents with agile, specialized players addressing regional demand and regulatory requirements.

Mitsubishi Electric

GE

Hitachi Energy

Toshiba

Hyosung Heavy Industries

CG Power and Industrial Solutions

Nari Group Corporation

The Gas Insulated Switchgear market is experiencing a technological transformation driven by the integration of digital systems, eco-friendly insulation, and modular designs. SF₆-free GIS technologies are gaining prominence, with approximately 25–30% of new installations in Europe and Asia-Pacific adopting alternative insulating gases that reduce greenhouse gas emissions by up to 70% per unit. Hybrid GIS, which combines air-insulated and gas-insulated modules, now represents nearly 12% of high-voltage projects, offering flexibility for retrofit and expansion in constrained urban substations. Digital monitoring and IoT-enabled sensors are increasingly standard in new GIS deployments. In 2025, over 35% of global high-voltage GIS installations incorporated real-time condition monitoring to detect faults, track temperature variations, and predict maintenance requirements, reducing unplanned downtime by 20–25%. Advanced diagnostic tools enable operators to schedule maintenance strategically, optimizing operational efficiency across transmission and distribution networks.

Automation and modular prefabrication are further reshaping GIS technology. Approximately 55% of recently completed substations in North America and Europe employed prefabricated GIS modules, significantly reducing on-site construction time and labor requirements. Smart GIS systems now integrate with grid management software to facilitate automated switching, load balancing, and renewable energy integration, particularly in solar and wind farms. Emerging innovations include vacuum and clean-air insulation alternatives for medium-voltage GIS, as well as AI-driven predictive analytics for enhanced grid reliability. These advancements are enhancing the lifespan, safety, and environmental performance of GIS units, positioning the market to meet future demands for compact, sustainable, and digitally connected power infrastructure.

• In May 2025, Hitachi Energy announced delivery of the world’s first SF₆‑free 550 kV gas‑insulated switchgear to the State Grid Corporation of China, marking a breakthrough in high‑voltage eco‑efficient infrastructure aimed at reducing greenhouse gas emissions while maintaining performance. (Hitachi Energy)

• In July 2025, Siemens Energy delivered the first SF₆‑free Gas Insulated Switchgear project in Saudi Arabia in collaboration with ELSEWEDY Electric PSP under contract with the Saudi Electricity Company, highlighting industry shifts to cleaner grid technology within the Middle East. (SaudiGulf Projects)

• In July 2025, ABB partnered with E.ON in Germany to supply next‑generation SF₆‑free GIS units, supporting the utility’s transition to sustainable grid operations and compliance with emerging environmental regulations focused on decarbonization. (ABB Group)

• In November 2025, Schneider Electric launched an SF₆‑free, compact, and natively digital primary gas‑insulated switchgear technology designed for high‑performance applications, eliminating the need for specialized gas handling and reducing total cost of ownership. (Schneider Electric)

The scope of the Gas Insulated Switchgear Market Report comprehensively covers segmentation, regional footprints, voltage class differentiation, technological innovation, and application domains across global power infrastructure. Market segmentation includes GIS by voltage levels—ranging from ≤ 38 kV medium‑voltage systems to ultra‑high‑voltage platforms above 550 kV—illustrating technical breadth and deployment contexts. It articulates distinctions between high‑, medium‑, and low‑voltage GIS across transmission substations, urban distribution networks, industrial power systems, and specialized installations such as renewable energy parks and metro rail infrastructure.

Geographic coverage spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with insights into regional consumption patterns, infrastructure development, regulatory dynamics, and grid modernization strategies. The report also outlines technology domains, including SF₆‑free insulation alternatives, digital monitoring and control systems, hybrid switchgear formats, and modular design innovations that address sustainability goals and operational resilience. Application focus areas emphasize the role of GIS in power transmission corridors, renewable injection points, commercial and industrial campuses, and smart grid initiatives—each segment supported with quantitative unit deployment statistics.

Additionally, the report explores industry challenges such as environmental compliance, supply chain constraints, and workforce skill requirements, along with opportunities arising from smart grid integration, predictive maintenance, and electrification trends. Emerging niches include eco‑efficient segregated phase bus technology, GIS for offshore substations, and digital twin integration for enhanced asset management, offering decision‑makers a strategic understanding of current capabilities and future expansion avenues within the GIS landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB, Siemens, Schneider Electric, Mitsubishi Electric, GE, Hitachi Energy, Toshiba, Hyosung Heavy Industries, CG Power and Industrial Solutions, Nari Group Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |