Reports

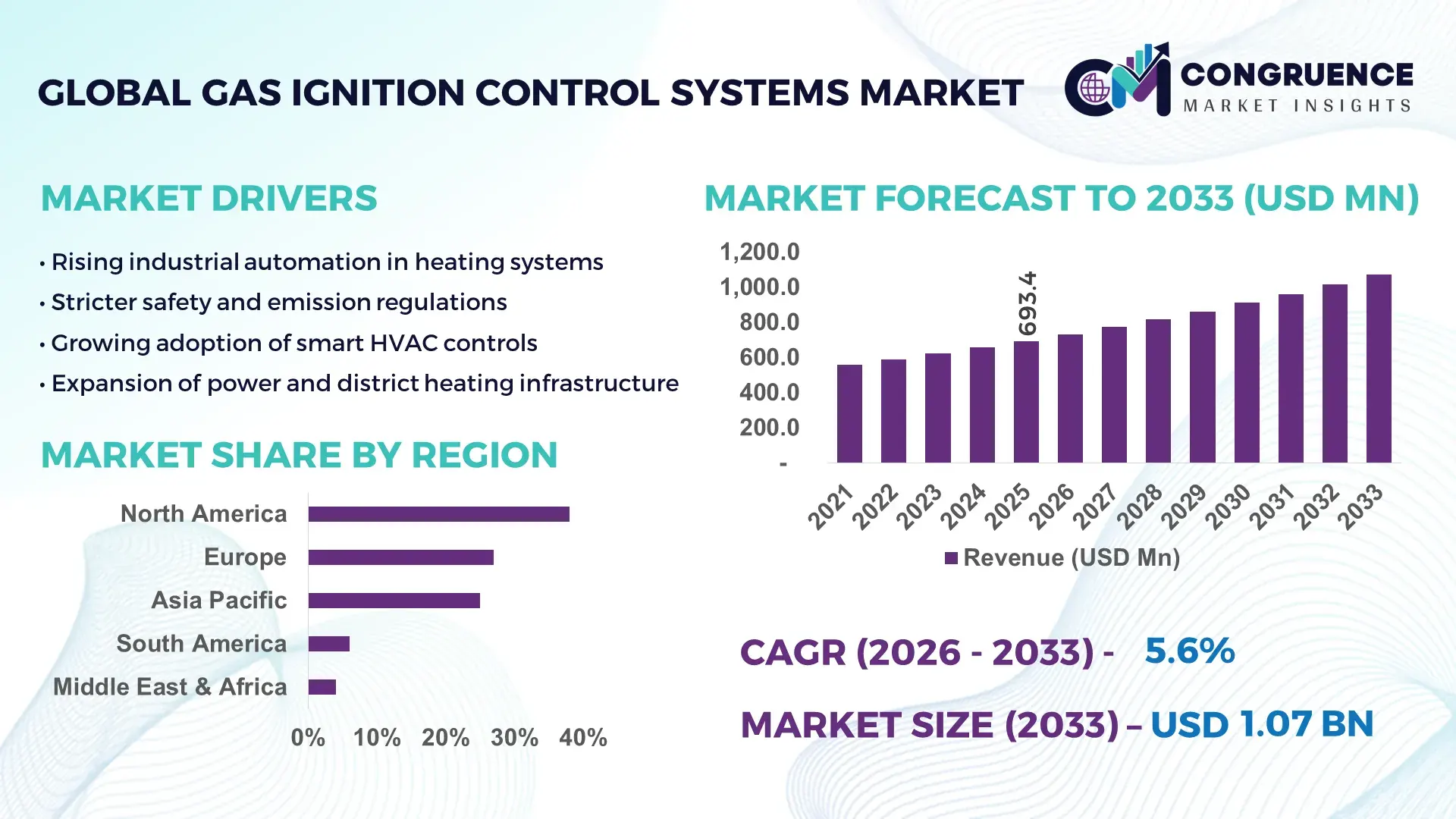

The Global Gas Ignition Control Systems Market was valued at USD 693.4 Million in 2025 and is anticipated to reach a value of USD 1,072.2 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. Rising deployment of energy-efficient heating and industrial combustion systems across manufacturing, power generation, and residential infrastructure is strengthening demand for advanced ignition control technologies.

The U.S. hosts one of the world’s largest installed bases of industrial furnaces, boilers, and gas-fired power plants, with more than 1,200 large-scale combustion facilities requiring high-reliability ignition systems. Annual domestic production of industrial burners and ignition controllers exceeds 2.5 million units, supported by sustained capital investments of roughly USD 1.8–2.2 billion per year in combustion upgrades, automation, and safety retrofits. The country leads in smart burner integration, with over 65% of new industrial installations incorporating digital ignition diagnostics, remote monitoring, and predictive maintenance platforms across petrochemicals, food processing, and commercial HVAC sectors.

Market Size & Growth: Market valued at USD 693.4 million in 2025, projected to reach USD 1,072.2 million by 2033, driven by tighter safety norms and automation in combustion processes.

Top Growth Drivers: Industrial boiler digitization (42%), efficiency gains from smart ignition (28%), adoption in clean-burning gas systems (31%).

Short-Term Forecast: By 2028, digital ignition diagnostics are expected to reduce unplanned burner downtime by 22%.

Emerging Technologies: AI-based flame monitoring, IoT-connected ignition modules, and hydrogen-ready ignition controls.

Regional Leaders: North America ~USD 410 million by 2033 (advanced retrofit cycle); Europe ~USD 290 million (decarbonization-linked upgrades); Asia-Pacific ~USD 320 million (rapid industrial expansion).

Consumer/End-User Trends: Strong pull from power generation, commercial HVAC, and food processing facilities prioritizing safety and energy efficiency.

Pilot/Case Example: In 2024, a U.S. refinery pilot using AI flame analytics cut burner trips by 27%.

Competitive Landscape: Honeywell (~28% share) leads, followed by Siemens, Schneider Electric, Johnson Controls, and Maxon.

Regulatory & ESG Impact: Stricter emission caps and NFPA combustion safety codes accelerating adoption of certified ignition controls.

Investment & Funding Patterns: Over USD 850 million invested since 2022 in smart combustion and burner automation startups.

Innovation & Future Outlook: Growth in hydrogen-compatible ignition systems and cloud-based fleet monitoring for burners.

The market is shaped by rising gas-fired power capacity, growing commercial building automation, and stricter safety standards for combustion equipment. Smart ignition modules with self-diagnostics and remote monitoring are replacing analog controls, reducing maintenance costs and improving reliability. Europe is witnessing faster replacement cycles due to decarbonization policies, while Asia-Pacific is driven by industrial expansion in chemicals, steel, and food processing. Future demand will increasingly favor hydrogen-ready and AI-enabled ignition platforms integrated with digital energy management systems.

The Gas Ignition Control Systems Market has become strategically critical as industries prioritize operational safety, energy efficiency, and emissions compliance in combustion-dependent applications. Modern ignition systems are no longer standalone components; they are integrated into digital industrial ecosystems that connect burners, boilers, and furnaces to centralized monitoring platforms. Compared with legacy relay-based ignition, AI-enabled flame analytics deliver 35% faster fault detection and 18% lower fuel wastage, materially improving plant reliability and energy performance.

Regionally, Asia-Pacific dominates in volume deployment, driven by rapid industrialization, while Europe leads in adoption with approximately 46% of large enterprises using smart, digitally monitored ignition systems due to stringent emissions and safety standards. North America sits between these two models, emphasizing retrofit upgrades in aging infrastructure and predictive maintenance.

In the short term, by 2028, the integration of AI-driven flame monitoring is expected to cut unplanned shutdowns in industrial burners by 20–25%, while improving start-up reliability and reducing manual inspections. This shift is accelerating the move toward condition-based maintenance rather than reactive repairs.

From a compliance and ESG perspective, firms are committing to measurable improvements such as a 25% reduction in methane leakage incidents by 2030 and broader adoption of low-NOx burner systems paired with advanced ignition controls. Many energy and manufacturing companies are also aligning investments with Scope 1 emissions reduction targets.

A micro-scenario illustrates this trajectory: In 2024, a German chemical plant deployed cloud-connected ignition controls and achieved a 23% reduction in burner-related downtime while cutting fuel consumption by 12% through optimized ignition timing.

Looking ahead, the Gas Ignition Control Systems Market is positioned as a foundational pillar for safer, cleaner, and more resilient energy and industrial operations—bridging traditional combustion infrastructure with next-generation digital and sustainable energy systems.

The Gas Ignition Control Systems Market is being reshaped by the convergence of industrial automation, safety regulations, and energy transition initiatives. Growing reliance on natural gas and emerging hydrogen blends is increasing demand for highly reliable, adaptive ignition solutions capable of handling variable fuel compositions. Digitalization of combustion assets—through IoT sensors, remote diagnostics, and predictive analytics—is reducing operational risks and maintenance costs while improving uptime. At the same time, stricter fire and explosion safety standards in manufacturing, power generation, and commercial buildings are accelerating replacement of legacy ignition systems. Supply chains are shifting toward modular, interoperable components, enabling faster installation and easier upgrades. However, high upfront costs and integration complexity continue to influence purchasing decisions, particularly in cost-sensitive industries.

Industrial automation is a major catalyst for demand as factories, refineries, and power plants increasingly integrate burners into digital control systems. More than 60% of new large-scale boilers installed since 2023 include programmable ignition controllers linked to distributed control systems (DCS). Automated flame monitoring reduces human error and enables real-time response to instability, which is critical in high-temperature processes such as steelmaking, glass production, and petrochemical cracking. Predictive maintenance platforms are now capable of analyzing ignition patterns to preempt failures, cutting emergency maintenance interventions by nearly one-third in advanced facilities. As Industry 4.0 adoption expands, operators prefer standardized, software-enabled ignition modules that can be remotely updated, calibrated, and audited—further embedding ignition controls into broader smart-plant architectures.

A significant portion of global combustion infrastructure is over 20 years old, particularly in emerging markets and heavy industries such as cement and metals. Retrofitting modern digital ignition controls into legacy burners often requires extensive mechanical and electrical upgrades, which can add 25–40% to project costs. Many older facilities lack compatible communication protocols, necessitating additional middleware or complete control system overhauls. Small and mid-sized plants also face budget constraints and limited technical expertise, slowing modernization efforts. Furthermore, downtime required for installation can disrupt production schedules, discouraging upgrades unless mandated by regulators or insurers. These structural barriers collectively restrain faster market penetration of next-generation ignition technologies.

The gradual introduction of hydrogen into natural gas networks is creating a new wave of demand for adaptive ignition systems capable of handling variable fuel mixtures. Hydrogen has different ignition characteristics, requiring faster response times and more precise flame detection. Several utilities in Europe and Japan are already piloting 20–30% hydrogen blends in industrial burners, necessitating upgraded controls. Manufacturers that develop hydrogen-ready ignition modules stand to benefit as gas networks transition toward lower-carbon fuels. Additionally, power-to-gas projects and green hydrogen hubs are investing in specialized combustion equipment, expanding addressable applications for advanced ignition control systems across utilities, chemicals, and heavy industry.

The market depends on high-precision sensors, flame rods, and microcontrollers, many of which are sourced from a limited number of global suppliers. Semiconductor shortages in recent years have extended lead times for smart ignition modules from 8–10 weeks to as long as 20–24 weeks in some cases. Price volatility for critical materials such as stainless steel and specialty alloys has also increased manufacturing costs. Smaller system integrators struggle to secure stable supply contracts, leading to project delays. Additionally, certification requirements for safety-critical components vary across regions, forcing manufacturers to maintain multiple product variants, which complicates production planning and increases inventory risks.

Rise in Modular and Prefabricated Construction: Modular construction is reshaping demand dynamics in the Gas Ignition Control Systems Market. Around 55% of recent commercial projects reported cost savings from prefabrication, as burner assemblies and control panels are built off-site using automated processes. Pre-bent piping and pre-wired ignition cabinets reduce on-site labor by nearly 30% and shorten installation timelines by 20–25%. Demand for high-precision, plug-and-play ignition modules is accelerating, particularly in Europe and North America where construction efficiency and standardization are critical.

Expansion of AI-Based Flame Analytics: Industrial plants are increasingly deploying AI-enabled flame monitoring that analyzes color, stability, and heat signatures in real time. Early adopters report up to 28% fewer burner trips and a 15% reduction in fuel wastage. More than 400 large facilities globally integrated camera-based flame analytics in 2024, signaling a shift from simple flame detection to intelligent combustion optimization.

Growth of Hydrogen-Ready Ignition Systems: With hydrogen blending trials reaching 30–40% in select gas networks, manufacturers are designing ignition controls with faster spark rates and adaptive flame sensors. Pilot projects in Germany and Japan have demonstrated stable combustion performance with less than 5% variance in flame quality, accelerating commercialization of hydrogen-compatible systems.

Cloud-Connected Remote Monitoring: Remote diagnostics platforms are becoming standard, allowing operators to monitor hundreds of burners from centralized control rooms. Facilities using cloud dashboards report 18–22% faster troubleshooting and a 12% reduction in maintenance costs, driving wider adoption across power generation and large commercial buildings.

The Gas Ignition Control Systems Market is structured around product types, applications, and end-user industries that reflect differing safety requirements, fuel characteristics, and levels of digitalization. Type segmentation is shaped by how ignition is initiated and monitored—ranging from traditional pilot-based solutions to fully electronic, sensor-driven systems. Application segmentation mirrors where combustion actually occurs, with heavy usage in industrial heating, power generation, and commercial HVAC alongside steady demand in residential appliances. End-user patterns vary by risk tolerance, regulatory exposure, and asset age: utilities and large manufacturers prioritize reliability and remote monitoring, while building owners emphasize energy efficiency and ease of maintenance. Across all segments, common themes include rising automation, tighter fire codes, greater use of IoT-enabled controls, and gradual preparation for hydrogen-blended fuels, which together are reshaping product design and procurement behavior.

Direct Spark Ignition (DSI) systems are the leading product type, accounting for roughly 38% of installations because they eliminate standing pilots, reduce fuel waste, and integrate easily with digital burner controls. They are increasingly paired with flame scanners and self-diagnostic modules that flag ignition anomalies before shutdowns occur. Hot Surface Ignition (HSI) holds about 27% of the market and is widely used in commercial HVAC and packaged boilers due to durability, lower maintenance needs, and consistent ignition performance in high-airflow environments.

Intermittent Pilot Ignition (IPI) represents around 18%, remaining popular in mid-scale industrial heaters and water boilers where operators prefer a hybrid approach combining a small pilot with electronic control. Continuous Pilot systems now account for about 10%, largely confined to legacy plants that value simplicity but face rising retrofit pressure. The remaining niche categories—multi-spark controllers, UV/IR flame scanners, and hybrid smart modules—together contribute roughly 7%, serving high-risk environments such as petrochemical crackers and glass furnaces.

The fastest-expanding type is next-generation smart DSI with AI-based flame analytics, growing at approximately 8% per year, driven by demand for remote diagnostics, reduced downtime, and compatibility with hydrogen blends.

Industrial heating is the leading application at about 34% of usage because steel, cement, glass, and chemical plants rely on high-temperature burners that require precise, fail-safe ignition. Commercial HVAC follows closely at 29%, supported by stricter building codes, large rooftop boiler fleets, and rising adoption of smart building management systems.

Power generation is the fastest-growing application, expanding by roughly 9% per year as gas-fired plants modernize ignition controls to improve start-up reliability, reduce emissions, and support flexible cycling with renewables. Residential heating accounts for around 16%, driven by replacements of aging furnaces and water heaters with electronically controlled systems. Petrochemicals, food processing, and other specialized uses together represent the remaining 21%, where high safety and process stability requirements dominate purchasing decisions.

In 2025, more than 40% of large industrial facilities reported piloting remote burner monitoring platforms linked to ignition controls. Separately, over 58% of new commercial buildings in North America specified digitally monitored ignition systems as part of smart HVAC packages.

Manufacturing and heavy industry is the leading end-user segment at about 36%, reflecting intensive use of furnaces, kilns, and process heaters that demand reliable ignition and continuous flame supervision. Utilities and power producers account for roughly 28%, prioritizing grid reliability, rapid start capability, and integration with plant-wide control systems.

Commercial building owners and facility managers are the fastest-growing end users, expanding at approximately 8% per year as energy codes tighten, building automation spreads, and property insurers require higher safety standards for boiler rooms. Residential appliance OEMs contribute about 14%, focusing on compact, cost-effective electronic ignition modules for mass-market products. Oil & gas, district heating, and other specialized sectors together make up the remaining 22%, where hazardous environments necessitate rugged, certified equipment.

In 2025, nearly 37% of large utilities reported deploying predictive maintenance tools tied to burner ignition data. Meanwhile, about 45% of Class A commercial buildings in major metro areas had begun using cloud-based boiler monitoring platforms linked to ignition systems.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America’s leadership reflects high replacement activity in aging boiler fleets, widespread industrial automation, and stringent fire-safety codes across the U.S. and Canada. Europe held approximately 27% share in 2025, supported by aggressive decarbonization programs, hydrogen-blending pilots, and large-scale retrofits in Germany, the UK, and France. Asia-Pacific represented about 25% of the market, driven by rapid industrial capacity additions in China, India, and Southeast Asia, alongside rising urban HVAC installations. South America contributed roughly 6%, centered on Brazil and Argentina’s expanding gas infrastructure and industrial modernization. The Middle East & Africa accounted for around 4%, with demand concentrated in oil & gas, petrochemicals, and large-scale district cooling projects. Across regions, digital ignition adoption rates ranged from ~45% in Europe to nearly 60% in North America, while Asia-Pacific led in volume-based installations due to new-build projects.

North America represents roughly 38% of global demand, led by the United States with dense installations across power plants, refineries, food processing, and commercial HVAC. Large industrial users are replacing legacy pilot systems with digital direct spark ignition tied to plant-wide control platforms, reducing unplanned shutdowns and improving operator safety. Stricter NFPA combustion codes, state-level emission rules in California and Texas, and utility incentive programs for high-efficiency boilers are accelerating upgrades. Cloud-connected burner monitoring is now common in large facilities, with remote diagnostics becoming a standard procurement requirement. Local integrators such as Maxon (a Honeywell brand) are expanding field-service fleets and offering retrofit kits tailored for aging industrial burners. Construction of data centers and advanced manufacturing plants is further lifting demand for high-precision ignition systems. Regionally, enterprises—especially in healthcare campuses and financial institutions—favor highly reliable, continuously monitored combustion systems to avoid service interruptions and insurance penalties.

Europe holds about 27% of the market, with Germany, the UK, France, Italy, and the Netherlands as core demand centers. Tight EU Ecodesign standards, national carbon taxes, and hydrogen-ready gas strategies are pushing rapid replacement of analog ignition systems. Utilities and chemical producers are heavily testing hydrogen blends (20–40%), creating strong pull for adaptive ignition controls. Manufacturers are prioritizing low-NOx burners paired with intelligent flame scanners and self-calibration features. German engineering firms are integrating ignition controls into digital twins for industrial furnaces, enabling virtual testing before deployment. Building retrofit programs in the UK and France are modernizing thousands of commercial boilers with smart ignition modules. Consumers and facility managers in Europe tend to favor certified, explainable, and auditable systems that provide transparent safety logs for regulators and insurers.

Asia-Pacific ranks first in installation volume growth, fueled by massive manufacturing expansion and urban infrastructure buildouts. China and India lead demand through steel, cement, glass, and chemical capacity additions, while Japan drives high-end adoption in precision industries. New gas pipelines, LNG terminals, and industrial parks are embedding modern ignition controls into greenfield projects rather than retrofitting legacy plants. Smart factory initiatives in China and South Korea are integrating burners with IoT platforms, while India’s push for cleaner fuels is replacing diesel boilers with gas-fired systems. Local players such as Weishaupt China and regional burner OEMs are scaling localized production to cut lead times. Rapid growth of commercial malls, hospitals, and data centers is lifting HVAC-related demand. Consumer behavior skews toward cost-efficient, mobile-monitored systems, with strong uptake of app-based remote diagnostics for facility managers.

South America accounts for roughly 6% of the market, concentrated in Brazil and Argentina. Expansion of natural gas pipelines, petrochemical complexes, and sugar-ethanol processing plants is increasing the need for reliable ignition controls. Brazil’s modernization of thermal power plants and fertilizer facilities is replacing outdated pilot systems with electronic alternatives. Argentina’s industrial revival and shale gas development in Vaca Muerta are stimulating demand for high-durability burners. Governments are encouraging domestic manufacturing of combustion equipment to reduce import dependence, while trade agreements are easing component flows. Local distributors are partnering with global OEMs to provide retrofit kits for aging boilers. Adoption is strongest in food processing and power generation, where downtime carries high financial risk. Regional users increasingly value bilingual (Spanish–Portuguese) monitoring interfaces and localized service support.

The Middle East & Africa region represents about 4% of the market, with demand anchored in oil & gas, petrochemicals, and large-scale construction. The UAE, Saudi Arabia, Qatar, and South Africa are key growth hubs. Gas processing plants and refineries are upgrading ignition systems to meet international safety standards and reduce flaring incidents. Mega district cooling and desalination projects are installing digitally monitored boilers and burners. Governments are promoting local content rules, encouraging regional assembly of ignition panels. Hydrogen and ammonia pilot projects in the Gulf are creating early demand for adaptive ignition technologies. Companies such as Emirates Industrial Gases are partnering with global suppliers to modernize plant combustion systems. Facility operators in the region favor rugged, heat-resistant equipment with strong remote monitoring due to harsh operating conditions and dispersed assets.

United States – 34% Market Share: High industrial automation, large gas-fired power fleet, and stringent NFPA safety codes drive sustained replacement demand for advanced ignition systems.

China – 22% Market Share: Massive manufacturing capacity, rapid gas infrastructure expansion, and smart-factory programs underpin large-scale installations across heavy industry and commercial buildings.

The Gas Ignition Control Systems Market exhibits a moderately consolidated competitive environment, with 60+ active global competitors offering diverse product portfolios and technological capabilities. The landscape includes both established automation and combustion control specialists as well as dedicated ignition module manufacturers. The top 5 companies combined account for approximately 42–48% of the total market, underscoring the presence of significant players alongside numerous niche and regional suppliers. Market leaders differentiate themselves through strategic initiatives such as integrated diagnostics, IoT connectivity, and digital retrofit offerings, which are increasingly sought by industrial and commercial end users to improve safety and operational uptime.

Strategic partnerships and co-development agreements are reshaping the competitive terrain. In early 2025, Schneider Electric entered a partnership with Mitsubishi Electric to co-develop integrated burner and energy optimization ignition solutions, strengthening combined capabilities in large industrial systems. Similarly, Bosch completed the acquisition of BurnerControl Technologies in September 2024, expanding its portfolio into commercial and industrial burner ignition solutions. Hammering the innovation trend, White-Rodgers (Emerson) introduced universal ignition modules with onboard diagnostics that have been installed in millions of units worldwide, while Resideo’s Wi-Fi connected modules bring remote lockout reset and smart home integration into mainstream HVAC deployments.

Emerging innovation includes next-generation smart ignition modules featuring microprocessor-based fault detection and adaptive controls, nimble handling of variable gas compositions, and enhanced safety features suitable for hydrogen blends. Competitive dynamics are also influenced by service offerings, global distribution reach, and compliance with regional safety standards. Overall, the combination of broad contestant participation and concentrated strength by top firms creates a dynamic market environment with sustained investment in technology and differentiation.

Honeywell International Inc. (Gas Ignition Control Solutions)

Schneider Electric SE

Johnson Controls International plc

Resideo Technologies, Inc.

Robertshaw Controls Company

Fenwal Controls (Kidde)

ICM CONTROLS

BASO Gas Products

Beckett Corporation

Capable Controls

Maxon Corporation

Flame Safeguard Technologies, Inc.

Teddington Controls Ltd.

The Gas Ignition Control Systems Market is being significantly shaped by the integration of advanced digital and smart technologies designed to boost safety, reliability, and operational intelligence. Traditional ignition controls—such as mechanical pilot systems or basic direct spark configurations—are increasingly supplemented or replaced by microprocessor-controlled modules that offer real-time diagnostics, fault logging, and remote monitoring capabilities. More than 17 million gas appliances in 2024 incorporated microprocessor-based ignition modules with self-diagnostic and lockout reset features, reflecting a shift toward embedded intelligence in both residential and commercial settings.

One major technological trend is the embedding of IoT connectivity in ignition control units. These connected modules enable facility managers to receive alerts, update firmware, and analyze ignition performance data remotely through cloud platforms. Adoption of such systems is especially strong in industrial boilers, commercial HVAC fleets, and distributed energy resources where uptime and safety are critical. Additionally, predictive diagnostics powered by embedded sensors are enabling operators to anticipate component wear or failure before it leads to unplanned downtime, enhancing maintenance planning and lowering lifecycle costs.

Materials innovation also plays a key role. Silicon carbide (SiC) igniters, introduced in 2024, demonstrate greater thermal tolerance and extended operating cycles—exceeding 56,000 ignition cycles without failure under test conditions—compared to traditional ceramic elements. Advanced solid-state relays are replacing mechanical contacts in heavy-cycle applications, improving durability by over 23% and reducing maintenance overhead.

Beyond hardware, advanced control algorithms are being incorporated into ignition systems to handle variable fuel compositions, including natural gas with higher hydrogen blends, which require adaptive spark timing and flame detection strategies. Some modern modules now incorporate multi-frequency flame sensing to differentiate stable combustion from anomalies more accurately. Digital-ready ignition platforms are also designed to integrate with broader industrial automation systems such as DCS (Distributed Control Systems) and BMS (Building Management Systems), further enhancing operational visibility and control.

Together, these technologies are transforming gas ignition controls from simple on/off devices into intelligent components within digital energy management and industrial automation ecosystems. Adoption of these innovations is accelerating across utilities, manufacturing, commercial infrastructure, and residential retrofit markets, underscoring the role of technology in driving both safety and efficiency.

• In July 30, 2025, Resideo Technologies announced its plan to spin off its ADI Global Distribution business into a separate public company, restructuring to sharpen focus on building products and controls (including connected HVAC and sensor systems) and unlocking operational and strategic flexibility for growth across residential and commercial controls portfolios. Source: www.resideo.com

• In August 5, 2025, Resideo Technologies reported record second quarter 2025 net revenue of $1.94 billion, up 22% year-over-year, driven by strong volume demand for connected controls and new product uptake across HVAC and distribution channels, highlighting expanding adoption of smart ignition-related control technologies in connected environments. Source: www.resideo.com

• In February 6, 2025, Honeywell announced a strategic portfolio realignment to separate its Automation and Aerospace businesses into dedicated public companies, positioning its automation segment (which includes advanced control and safety systems relevant to gas ignition controls) for focused investment, streamlined innovation, and tailored growth strategies. Source: www.honeywell.com

• In 2025, Siemens AG showcased a broad set of industrial AI and digital automation innovations at global tech events aimed at accelerating digital transformation, including enhanced software-defined automation and digital twin technologies designed to improve operational performance, integration, and reliability for critical industrial control systems. Source: www.press.siemens.com

The Gas Ignition Control Systems Market Report provides a comprehensive examination of technological, product, application, and regional dimensions of the global market. The technology scope spans conventional ignition types—Direct Spark (DSI), Hot Surface (HSI), Intermittent and Continuous Pilot systems—to advanced, microprocessor-based electronic modules with embedded diagnostics, IoT connectivity, and adaptive fuel handling. The report analyzes performance and deployment patterns in residential furnaces, commercial HVAC systems, industrial heaters, power plants, and specialized combustion applications, offering insights into reliability, safety integration, and retrofit dynamics. OEM and aftermarket channels are delineated, capturing volume and unit-level trends without revenue figures but with unit counts and adoption metrics.

Product segmentation includes ignition coils, control modules, flame sensors, and interface controllers, while application segmentation highlights industrial, commercial, and residential usage behaviors. End-user classification covers manufacturing facilities, utilities, commercial real estate, and housing markets, with data reflecting evolving end-user priorities such as remote monitoring, predictive maintenance, and compliance with safety codes. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, offering granular views of unit installations, regional regulatory environments, gas infrastructure trends, and technology adoption patterns.

Additionally, the report addresses cross-cutting themes such as digital transformation, energy-efficiency mandates, integration with automation systems (BMS/DCS), and emerging fuel compositions including hydrogen blends. Also captured are engineering trends such as enhanced flame detection methodologies, materials advancements like silicon carbide igniters, and modular control architectures that facilitate global standardization and faster deployment. This breadth equips decision-makers, investors, and technology strategists with actionable insights into both current market dynamics and future trajectories of the gas ignition control ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 693.4 Million |

| Market Revenue (2033) | USD 1,072.2 Million |

| CAGR (2026–2033) | 5.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Honeywell; Siemens; Emerson; Schneider Electric; Johnson Controls; Resideo; Robertshaw; Fenwal Controls; BASO Gas Products; Beckett Corporation; Capable Controls; Maxon; ICM Controls; Flame Safeguard Technologies; Teddington Controls |

| Customization & Pricing | Available on Request (10% Customization Free) |