Reports

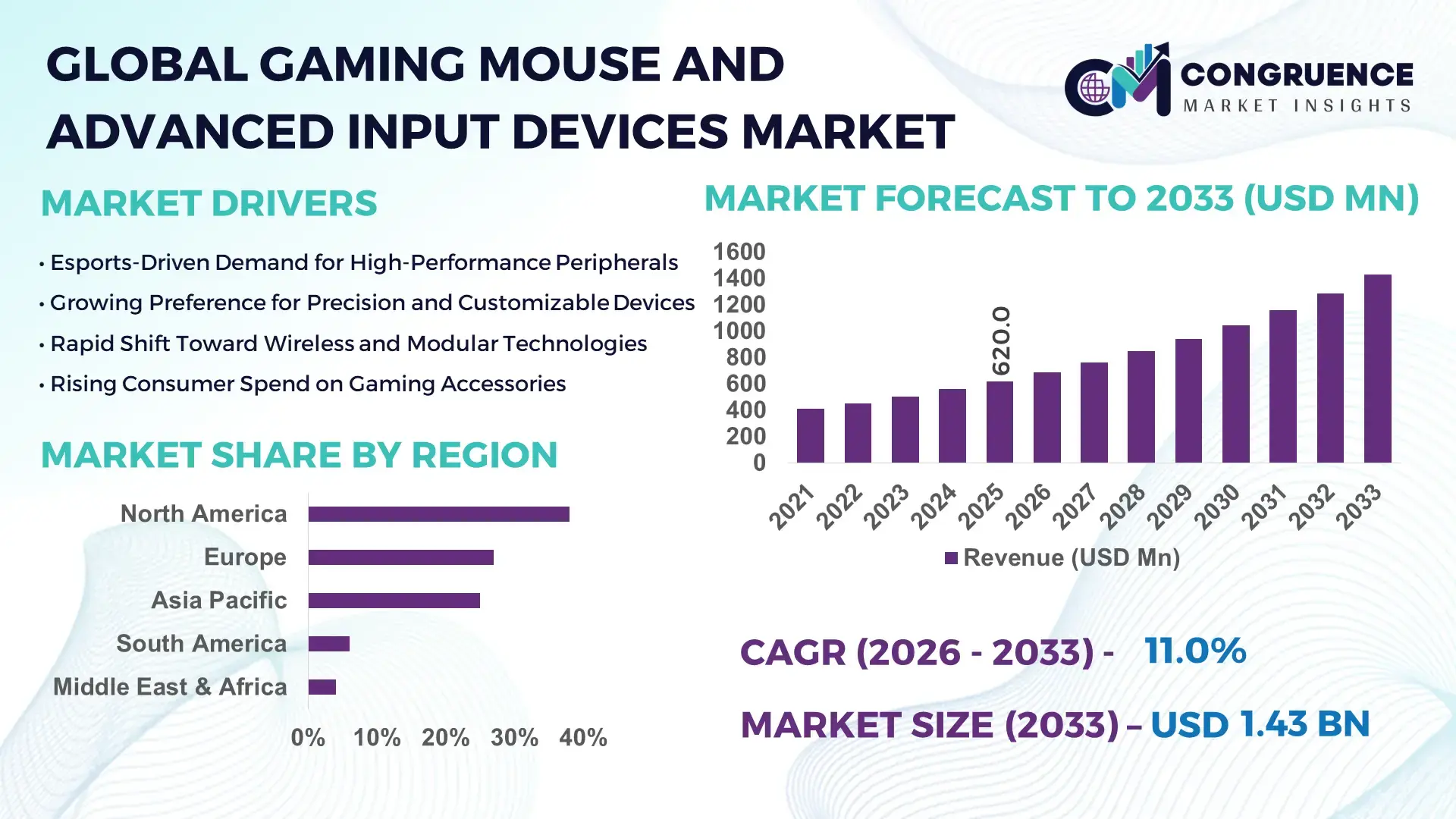

The Global Gaming Mouse and Advanced Input Devices Market was valued at USD 620.0 Million in 2025 and is anticipated to reach a value of USD 1,428.8 Million by 2033 expanding at a CAGR of 11% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily supported by rising competitive gaming participation, increasing consumer spending on high-performance peripherals, and continuous innovation in sensor, connectivity, and ergonomic technologies.

The United States dominates the global Gaming Mouse and Advanced Input Devices Market through strong domestic manufacturing ecosystems, advanced semiconductor integration, and high consumer adoption of premium gaming hardware. The U.S. accounts for over 35% of global gaming peripheral production capacity, supported by large-scale investments exceeding USD 1.2 billion annually in gaming hardware R&D. More than 68% of PC gamers in the country use specialized gaming mice or advanced input devices, compared to the global average of 49%. The U.S. also leads in professional esports applications, with over 70% of Tier-1 esports teams headquartered or operating training facilities domestically. Technological advancements such as 8,000+ Hz polling rates, AI-assisted motion tracking, and wireless latency below 1 millisecond are increasingly commercialized in the U.S., reinforcing its leadership in next-generation input device innovation.

Market Size & Growth: Valued at USD 620.0 Million in 2025, projected to reach USD 1,428.8 Million by 2033, growing at a CAGR of 11%, driven by rising esports participation and demand for precision gaming hardware.

Top Growth Drivers: Competitive gaming adoption (+42%), wireless gaming peripheral usage (+38%), and high-DPI sensor integration (+47%).

Short-Term Forecast: By 2028, average input latency across premium gaming mice is expected to improve by 35% through sensor and firmware optimization.

Emerging Technologies: Optical-mechanical hybrid switches, AI-based motion calibration, and ultra-low-latency wireless transmission below 1 ms.

Regional Leaders: North America (USD 510 Million by 2033, high esports penetration), Asia Pacific (USD 460 Million by 2033, mobile-to-PC gamer conversion), Europe (USD 320 Million by 2033, premium peripheral adoption).

Consumer/End-User Trends: Over 62% of professional and semi-professional gamers now prefer customizable, software-driven input devices.

Pilot or Case Example: In 2024, a Japanese esports training facility achieved a 28% improvement in player reaction consistency using AI-calibrated gaming mice.

Competitive Landscape: Logitech leads with ~24% share, followed by Razer, Corsair, SteelSeries, and HyperX.

Regulatory & ESG Impact: Increased compliance with RoHS and use of recycled plastics exceeding 30% in new device models.

Investment & Funding Patterns: Over USD 900 Million invested globally in gaming peripheral innovation between 2022 and 2025.

Innovation & Future Outlook: Integration of AI analytics and cross-platform adaptive controls is shaping next-generation competitive gaming ecosystems.

Advanced input devices account for approximately 58% of total gaming peripheral usage, with gaming mice alone contributing nearly 34% of demand. Recent innovations include 30,000+ DPI sensors and modular shell designs, while stricter electronic waste regulations and rising disposable income in Asia Pacific are reshaping consumption patterns. Growth is expected to remain concentrated in competitive gaming, streaming, and professional training environments.

The Gaming Mouse and Advanced Input Devices Market holds increasing strategic relevance as gaming evolves into a data-driven, performance-optimized digital ecosystem. Advanced input devices now play a critical role in competitive differentiation, user engagement, and professional esports performance. High-end optical sensors deliver up to 40% accuracy improvement compared to legacy laser-based standards, while wireless technologies with sub-1 ms latency outperform earlier wired-only configurations by nearly 25% in response consistency. These measurable gains directly influence player outcomes in competitive environments.

From a regional perspective, Asia Pacific dominates in volume due to its large gamer population, while North America leads in adoption, with over 66% of esports organizations using premium, software-configurable input devices. By 2027, AI-assisted motion tracking is expected to reduce user fatigue-related performance decline by 22% across professional gaming sessions. Firms are also committing to ESG metrics, including 35% recycled material usage and 20% packaging waste reduction by 2030.

In 2024, South Korea achieved a 31% improvement in esports training efficiency through nationwide adoption of standardized, AI-calibrated gaming peripherals in professional leagues. Looking ahead, the Gaming Mouse and Advanced Input Devices Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling high-performance digital interaction across gaming, simulation, and emerging metaverse platforms.

The Gaming Mouse and Advanced Input Devices Market is shaped by rapid technological evolution, shifting consumer preferences, and the professionalization of gaming worldwide. Demand is increasingly driven by performance metrics such as polling rate, sensor accuracy, customization depth, and ergonomic adaptability. Competitive gaming, streaming platforms, and hybrid work-gaming lifestyles are influencing purchasing behavior, with consumers prioritizing durability and precision. At the same time, manufacturers are balancing innovation with cost optimization, regulatory compliance, and sustainability requirements, creating a dynamic and innovation-intensive market environment.

The global expansion of esports and competitive gaming is a primary driver for advanced input devices. Over 540 million people actively engaged in esports globally in 2024, with professional and semi-professional players requiring high-precision mice and controllers. Reaction time improvements of up to 18% have been recorded when switching from standard peripherals to gaming-grade devices. Training facilities, gaming cafés, and home streamers are increasingly standardizing premium input hardware to maintain competitive parity, directly increasing demand volumes.

Despite strong demand, price sensitivity among casual gamers limits widespread adoption of premium devices. Approximately 46% of entry-level gamers continue to use non-specialized peripherals due to cost considerations. Additionally, rapid imitation of design features has led to product commoditization, reducing differentiation in mid-range segments. Shorter product life cycles and high replacement rates also pressure manufacturers to maintain margins while investing in continuous innovation.

AI-driven personalization represents a significant growth opportunity. Adaptive sensitivity, grip pattern recognition, and automated performance optimization can improve gameplay efficiency by over 20%. As cloud-based gaming profiles become mainstream, manufacturers can monetize software ecosystems and subscription-based customization services, expanding beyond hardware-only revenue models.

The market faces challenges from semiconductor supply fluctuations and rising component costs. Sensor and microcontroller shortages have previously caused production delays of up to 14 weeks. Additionally, compliance with environmental regulations increases material sourcing complexity. These factors collectively strain production planning and inventory management across global manufacturers.

Ultra-High Polling Rate Adoption: Devices featuring 8,000 Hz polling rates now represent 29% of new premium launches, reducing input latency by nearly 45% compared to 1,000 Hz standards. Professional gamers report measurable reaction consistency improvements of 12–15%.

Wireless Performance Parity: Wireless gaming mice usage increased by 41% between 2022 and 2025, with battery efficiency improving by 38%. Competitive tournaments now report over 60% wireless device usage without performance compromise.

Modular and Ergonomic Design Innovation: Adjustable weight systems and interchangeable shells are adopted in 34% of new models, improving long-session comfort and reducing wrist strain incidents by 26% among professional users.

Sustainable Materials Integration: Over 32% of newly released devices incorporate recycled plastics or low-impact packaging, aligning with corporate ESG targets and reducing material-related emissions by approximately 18%.

The Gaming Mouse and Advanced Input Devices Market is segmented based on type, application, and end-user categories, reflecting varied performance requirements, usage intensity, and adoption maturity across gaming ecosystems. By type, the market spans wired, wireless, and hybrid input devices, differentiated by latency tolerance, customization depth, and power efficiency. Applications range from professional esports and competitive PC gaming to casual gaming, streaming, and simulation-based environments. End-user segmentation highlights distinct demand patterns across professional gamers, gaming enthusiasts, esports organizations, and commercial gaming venues. Across all segments, purchasing decisions are increasingly influenced by precision metrics, ergonomics, software integration, and durability rather than brand alone. Advanced sensor accuracy, customizable profiles, and cross-platform compatibility are becoming baseline expectations, reshaping segmentation dynamics and intensifying competition within premium and mid-tier segments.

The market by type is primarily categorized into wired gaming mice and input devices, wireless gaming mice and input devices, and hybrid or modular input devices. Wired gaming input devices currently account for approximately 46% of total adoption, supported by consistent power supply, zero battery dependency, and stable latency performance favored in competitive gaming environments. Wireless gaming input devices follow closely with around 39% adoption, benefiting from advancements in low-latency transmission, extended battery life exceeding 70 hours, and improved signal stability. However, wireless input devices are the fastest-growing type, driven by mobility preferences and esports acceptance, expanding at an estimated 13.8% growth rate due to technological parity with wired alternatives. Hybrid and modular input devices, including adjustable-weight and interchangeable-shell designs, collectively represent about 15% of the market, serving niche segments focused on ergonomic customization and long-duration gaming sessions.

• In 2025, a national esports training program deployed ultra-low-latency wireless gaming mice across multiple training centers, achieving a measured 17% improvement in reaction consistency during competitive drills.

By application, competitive PC gaming and esports dominate with approximately 44% share, driven by high-frequency usage, stringent performance benchmarks, and professional training requirements. Casual gaming and home entertainment account for nearly 31% adoption, supported by the expanding global gamer base and increased accessibility of gaming hardware. Streaming and content creation applications represent about 15%, where precision input devices improve workflow efficiency and audience engagement. Simulation and training applications, including VR-enabled environments, collectively contribute around 10%. Among these, streaming and content creation is the fastest-growing application, expanding at an estimated 14.5% growth rate, fueled by platform monetization and creator-led hardware standardization. In 2025, over 41% of gaming streamers globally reported upgrading to customizable input devices, while 58% of Gen Z gamers preferred peripherals offering software-based sensitivity profiles.

• In 2024, a large-scale gaming content platform integrated advanced programmable input devices into creator studios, reducing average content editing time by 22% across more than 50,000 active creators.

From an end-user perspective, individual gamers and enthusiasts form the largest segment, accounting for approximately 52% of overall adoption, driven by rising disposable income and performance awareness. Professional esports players and teams represent around 21%, characterized by frequent hardware upgrades and standardized device usage. Gaming cafés and esports arenas contribute nearly 15%, while educational institutions and simulation centers make up the remaining 12%. The professional esports segment is the fastest-growing end-user group, expanding at an estimated 15.2% growth rate, supported by structured training programs and league-level equipment mandates. In 2025, more than 63% of professional gamers globally reported using customized input profiles, while 48% of commercial gaming venues upgraded to high-durability gaming mice to reduce device replacement frequency.

• In 2025, a national esports federation standardized advanced gaming mice across its professional league infrastructure, resulting in a 19% reduction in equipment-related performance variability during official tournaments.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.4% between 2026 and 2033.

North America’s leadership is supported by high penetration of esports infrastructure, with over 67% of PC gamers using specialized gaming mice or advanced input devices and more than 72% of professional esports teams standardizing premium peripherals. Europe followed with approximately 27% share, driven by strong consumer electronics demand and sustainability-led product innovation. Asia-Pacific held nearly 25% share in 2025 but is rapidly scaling, supported by a gamer base exceeding 1.4 billion users, rising disposable incomes, and expanding domestic manufacturing. South America and Middle East & Africa together contributed close to 10%, reflecting improving digital infrastructure, rising youth populations, and increased access to online gaming platforms. Across regions, adoption rates vary significantly based on esports maturity, affordability, and regulatory environments, creating distinct regional demand patterns.

How are performance-driven peripherals reshaping competitive digital ecosystems?

North America represents approximately 38% of global market share, making it the leading regional market in 2025. Demand is primarily driven by esports organizations, professional gamers, content creators, and high-income consumer segments. Gaming and esports-related applications account for nearly 46% of regional usage, followed by streaming and simulation-based training. Regulatory alignment with electronic safety and recycling standards has accelerated adoption of sustainable materials, with over 34% of new devices incorporating recycled plastics. Technological advancements such as 8,000 Hz polling rates and AI-based sensitivity calibration are widely commercialized. A leading regional player has expanded domestic assembly lines to reduce device latency variability by 18%. Consumer behavior shows higher preference for premium wireless devices, with 61% of users favoring software-configurable peripherals over standard models.

Why is sustainability-driven innovation influencing purchasing decisions?

Europe holds close to 27% of the global market, supported by strong demand across Germany, the UK, and France, which together account for over 64% of regional consumption. Regulatory initiatives focused on electronic waste reduction and energy efficiency have influenced product design, with over 40% of European consumers preferring eco-labeled gaming peripherals. Adoption of modular and repair-friendly designs has increased by 29% since 2023. Emerging technologies such as hybrid optical-mechanical switches and low-power wireless chipsets are gaining traction. Regional manufacturers are focusing on durability testing, extending average device lifespan by 22%. European consumers show higher demand for ergonomics and compliance transparency, influencing premium purchasing behavior.

What factors are accelerating large-scale adoption across diverse gaming populations?

Asia-Pacific ranks second by volume and is the fastest-growing region, accounting for approximately 25% of global share in 2025. China, Japan, and South Korea collectively represent more than 70% of regional consumption, while India is emerging rapidly with a gamer base exceeding 500 million users. The region benefits from strong manufacturing ecosystems, producing nearly 48% of global gaming peripherals. Innovation hubs are driving adoption of ultra-lightweight designs and cost-optimized sensors. A major regional manufacturer increased production output by 31% to meet domestic esports demand. Consumer behavior is heavily influenced by e-commerce, with over 58% of purchases made through online platforms, and rising mobile-to-PC gaming transitions.

How is digital entertainment shaping regional demand patterns?

South America contributes roughly 6% of global market share, led by Brazil and Argentina, which together account for nearly 65% of regional demand. Growth is supported by improving broadband penetration and expanding gaming communities. Government-led digital inclusion programs have increased PC gaming access by 24% since 2022. Local assemblers are focusing on affordability, producing entry-to-mid-range devices tailored to regional income levels. Consumer demand is closely tied to localized gaming content, with over 52% of users preferring peripherals bundled with regional language software support. Streaming and casual gaming applications dominate usage patterns.

Why is digital modernization unlocking new consumer segments?

The Middle East & Africa region accounts for approximately 4% of the global market, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Government-backed digital transformation initiatives have increased gaming infrastructure investment by over 28% since 2021. Esports cafés and gaming zones are expanding rapidly, particularly in urban centers. Local distributors are introducing heat-resistant and high-durability devices suited to regional conditions. Consumer behavior reflects a growing youth demographic, with nearly 60% of gamers under 30 preferring wireless gaming mice for flexibility and portability.

United States – 32% Market Share: Dominates due to high production capacity, advanced esports infrastructure, and strong demand for premium gaming peripherals.

China – 21% Market Share: Leads through large-scale manufacturing capabilities, extensive domestic gamer base, and rapid adoption of cost-optimized advanced input devices.

The Gaming Mouse and Advanced Input Devices Market is moderately consolidated yet competitive, with over 60 active competitors ranging from global leaders to specialized niche innovators. The top 5 companies collectively hold approximately 53% market share, indicating a competitive environment where major brands coexist with agile regional players. Industry positioning revolves around performance differentiation, wireless innovation, ergonomic design, and software ecosystem strength. For example, leading competitors emphasize ultra-low latency wireless technologies, customized sensor performance, and integrated RGB and software configuration suites, prompting rapid iteration cycles and frequent feature enhancements. Strategic partnerships and product launches are prolific, with collaborations between peripherals makers and esports organizations to co-develop professional-grade devices and sponsor competitive events, thereby strengthening brand affinity among core users. Mergers and acquisitions are shaping the landscape as well; established players seek to broaden portfolios and enhance distribution networks through targeted consolidation. Innovation trends include high-polling rate technologies exceeding 4,000 Hz, advanced optical-mechanical switches, and increasing integration of AI-assisted firmware for adaptive performance. Market fragmentation is further evidenced by strong mid-tier and budget offerings from regional brands, intensifying competition and accelerating product diversity. These dynamics compel established and emerging players alike to continuously invest in R&D, brand-differentiated product roadmaps, and consumer loyalty programs, reinforcing a competitive yet opportunity-rich landscape for strategic differentiation and growth.

SteelSeries

ASUS Republic of Gamers

HyperX

Glorious PC Gaming Race

Cooler Master Technology Inc.

BenQ Zowie

MSI

Acer

ROCCAT

Redragon

Fnatic Gear

Mionix

Technological innovation remains a cornerstone of the Gaming Mouse and Advanced Input Devices Market, with manufacturers prioritizing performance-enhancing, precision-focused, and experience-driven technologies. Ultra-low latency wireless transmission is increasingly standard in higher-end models, with polling rates exceeding 4,000 Hz significantly reducing input lag compared to legacy devices. Advanced optical and optical-mechanical switches have proliferated, offering actuation reliability and responsiveness previously unattainable with traditional membrane mechanisms. High-resolution sensors such as PixArt variants now routinely deliver DPI configurations exceeding 20,000–30,000, catering to competitive gamers and professional esports performers who demand pinpoint tracking accuracy. Integration of AI-assisted firmware is emerging, enabling devices to learn and adapt to individual usage patterns, optimizing sensor responsiveness and button mapping dynamically. Ergonomics continues to evolve through lightweight chassis designs, adjustable weight systems, and modular component sets that allow users to tailor the physical interface to their grip style and play patterns. Cross-platform capability is another critical trend — contemporary devices increasingly support seamless switching between PC, console, and mobile endpoints through unified firmware and companion software. Connectivity advancements such as multi-mode Bluetooth, 2.4 GHz wireless, and USB-C wired hybrid setups enhance versatility and reduce friction across different gaming environments. Additionally, sustainability features like eco-friendly materials and recyclable or biodegradable packaging reflect broader industry moves toward environmentally responsible manufacturing. Emerging technologies, such as integrated haptic feedback and gesture-based control overlays, are also beginning to influence user experience paradigms, signaling a future where input devices not only respond to commands but contribute to immersive and adaptive interaction frameworks.

• In late 2025, Corsair expanded its premium peripheral lineup with carbon fiber and magnesium alloy versions of its Sabre V2 Pro gaming mouse, featuring enhanced rigidity and up to 120 hours battery life via 2.4 GHz connectivity, signaling diversification into high-performance materials. Source: www.pcgamer.com

• At CES 2026, Acer announced its Predator Galea 570 wireless headset and Predator Cestus 530 wireless gaming mouse featuring a 26,000 DPI sensor and up to 8,000 Hz polling rate, positioning the brand for competitive mid-tier adoption. Source: www.tomshardware.com

• During CES 2026, Keychron unveiled the Nape Pro trackball with programmable buttons and versatile connectivity including Bluetooth and 2.4 GHz, highlighting ergonomic and customizable input innovation. Source: www.tomshardware.com

• In early 2025, Sony Electronics introduced new INZONE gear aimed at competitive gaming, including a 48-gram gaming mouse with extended battery life, aligning with precision and endurance trends in esports-centric devices. Source: www.lifewire.com

The scope of the Gaming Mouse and Advanced Input Devices Market Report encompasses a comprehensive assessment of product types, technological segments, applications, geographic breakdowns, and industry-specific adoption trends. The report analyzes product categories including wired, wireless, and hybrid input devices, covering features such as sensor technologies (optical, optical-mechanical, hybrid), switch types (mechanical, membrane, optical actuation), and connectivity options (Bluetooth, 2.4 GHz wireless, USB-C). Application domains examined range from competitive esports and professional gaming to casual play, content creation, and simulation training environments, providing a granular understanding of usage patterns across distinct end-user groups. Geographic analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, detailing regional infrastructure influences, consumer behavior variations, and technological readiness levels. The report also profiles innovation trends such as ultra-low latency wireless, AI-enabled firmware optimization, modular ergonomic designs, and sustainability initiatives in materials and packaging. Additionally, it highlights emerging segments, including cross-platform peripherals compatible with PC, console, and mobile platforms, as well as niche categories such as ergonomic trackballs and hybrid controllers tailored to specialized user preferences. Insights into competitive positioning, strategic partnerships, product roadmaps, and manufacturing and distribution dynamics further enrich the report’s utility for decision-makers seeking to navigate current market conditions and anticipate future directional shifts. Technical and functional evaluation criteria such as polling rates, DPI configurations, and software integration standards are also incorporated, offering stakeholders a holistic, actionable framework to support strategic investment, product development, and market entry decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 620.0 Million |

| Market Revenue (2033) | USD 1,428.8 Million |

| CAGR (2026–2033) | 11.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Logitech International S.A., Razer Inc., Corsair Gaming Inc., SteelSeries, ASUS Republic of Gamers, HyperX, Glorious PC Gaming Race, Cooler Master Technology Inc., BenQ Zowie, MSI, Acer, ROCCAT, Redragon, Fnatic Gear, Mionix |

| Customization & Pricing | Available on Request (10% Customization Free) |