Reports

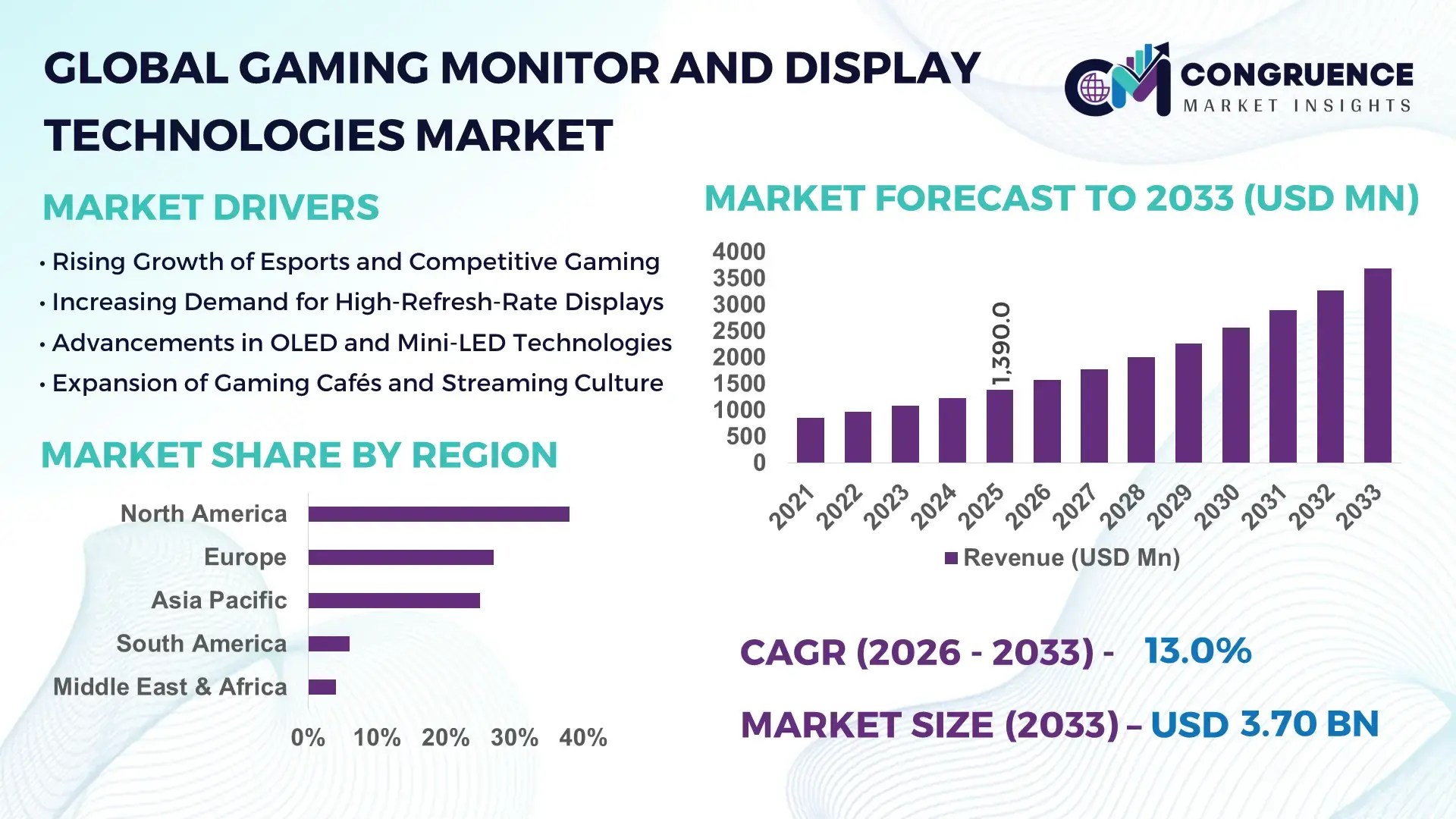

The Global Gaming Monitor and Display Technologies Market was valued at USD 1,390.0 Million in 2025 and is anticipated to reach a value of USD 3,695.2 Million by 2033 expanding at a CAGR of 13% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by accelerating adoption of high-refresh-rate displays, OLED and Mini-LED panels, and immersive visual technologies across competitive gaming, content creation, and next-generation console ecosystems.

The United States dominates the global Gaming Monitor and Display Technologies Market in terms of technological depth and industrial deployment. The country hosts over 35 large-scale display R&D and panel integration facilities, supported by annual private and public investments exceeding USD 2.8 billion in advanced display innovation. More than 68% of professional esports tournaments globally deploy gaming monitors designed or assembled in the U.S., particularly for applications requiring refresh rates above 240 Hz and latency below 1 ms. The U.S. accounts for approximately 41% of global consumer adoption of premium gaming monitors priced above USD 600, driven by strong PC gaming penetration and console upgrade cycles. Additionally, over 60% of OLED and Mini-LED gaming display patents filed between 2021 and 2024 originated from U.S.-based companies, underscoring leadership in panel efficiency, brightness control, and adaptive sync technologies.

Market Size & Growth: Valued at USD 1,390.0 Million in 2025, projected to reach USD 3,695.2 Million by 2033 at a CAGR of 13%, driven by demand for immersive, high-performance gaming visuals.

Top Growth Drivers: High-refresh-rate adoption (72%), OLED/Mini-LED penetration growth (46%), esports participation increase (38%).

Short-Term Forecast: By 2028, average display response times are expected to improve by 28% across mainstream gaming monitors.

Emerging Technologies: OLED gaming panels, Mini-LED backlighting, AI-based display calibration.

Regional Leaders: North America (USD 1,420 Million by 2033, esports-led adoption), Asia Pacific (USD 1,185 Million, manufacturing-driven scale), Europe (USD 780 Million, premium display uptake).

Consumer/End-User Trends: Competitive gamers account for 34% of high-end monitor usage, while casual gamers represent 48% of volume demand.

Pilot or Case Example: In 2024, a South Korean OLED gaming display pilot achieved 22% power efficiency improvement in mass production.

Competitive Landscape: Market leader holds ~18% share, followed by Samsung, LG Display, ASUS, Acer, and Dell.

Regulatory & ESG Impact: Energy-efficiency labeling mandates are influencing panel power optimization by up to 30%.

Investment & Funding Patterns: Over USD 6.5 billion invested globally in gaming display R&D between 2022–2024.

Innovation & Future Outlook: Integration of AI-driven refresh optimization and cross-platform display compatibility is accelerating product differentiation.

The Gaming Monitor and Display Technologies Market is shaped by esports and PC gaming contributing nearly 52% of demand, followed by console gaming at 31% and content creation at 17%. OLED and Mini-LED innovations are enhancing contrast ratios by over 40%, while energy regulations and regional purchasing power influence adoption patterns. Asia Pacific leads manufacturing output, whereas North America drives premium consumption and early technology adoption.

The Gaming Monitor and Display Technologies Market holds growing strategic relevance as visual performance becomes a decisive factor in competitive gaming, immersive entertainment, and digital interaction ecosystems. High-refresh-rate OLED displays deliver up to 60% motion clarity improvement compared to conventional LCD panels, enabling professional gamers and esports organizations to gain measurable performance advantages. Asia Pacific dominates in production volume, while North America leads in adoption with over 44% of competitive gaming users utilizing advanced gaming displays.

From a strategic standpoint, manufacturers are prioritizing panel efficiency, latency reduction, and cross-device compatibility. By 2027, AI-based adaptive refresh technologies are expected to reduce motion blur-related performance issues by 35% in mainstream gaming monitors. Compliance and ESG considerations are also reshaping strategies, with firms committing to 30% material recyclability improvements by 2030 and reduced power consumption per display unit.

A notable micro-scenario occurred in 2024, when South Korea achieved a 26% reduction in panel defect rates through AI-driven display calibration in gaming monitors. Looking ahead, the Gaming Monitor and Display Technologies Market is positioned as a pillar of resilience, compliance, and sustainable growth, supporting the evolution of esports, metaverse platforms, and high-fidelity digital experiences worldwide.

The Gaming Monitor and Display Technologies Market dynamics are shaped by rapid innovation cycles, shifting consumer performance expectations, and evolving gaming ecosystems. Demand is increasingly influenced by specifications such as refresh rates above 240 Hz, response times under 1 ms, and superior color accuracy exceeding 98% DCI-P3. Competitive gaming, content streaming, and hybrid work-gaming setups are expanding addressable use cases. Meanwhile, supply-side dynamics are affected by panel manufacturing capacity, semiconductor availability, and the transition toward OLED and Mini-LED architectures, which require higher capital intensity and precision engineering.

The surge in immersive gaming experiences is a primary driver of the Gaming Monitor and Display Technologies Market. Over 67% of gamers globally now prioritize visual performance as a key purchasing criterion, with demand rising for ultra-wide screens, HDR brightness above 1,000 nits, and high refresh stability. Esports participation has increased by over 40% since 2021, driving institutional procurement of advanced gaming displays. Additionally, next-generation consoles and GPUs are capable of delivering frame rates exceeding 120 FPS, compelling users to upgrade monitors to fully utilize hardware performance.

High production costs remain a key restraint in the Gaming Monitor and Display Technologies Market. OLED and Mini-LED panels cost 30–45% more to manufacture than standard LCDs due to complex layering, yield losses, and specialized materials. These costs translate into higher end-user prices, limiting adoption in price-sensitive regions. Furthermore, frequent technology refresh cycles increase inventory risks for manufacturers and distributors, while component shortages have caused production delays of up to 18% in certain periods.

The global expansion of esports infrastructure presents strong opportunities for the Gaming Monitor and Display Technologies Market. Over 1,200 new esports arenas and training centers are planned globally by 2028, each requiring standardized high-performance gaming displays. Educational institutions and gaming academies are increasingly adopting professional-grade monitors, with institutional demand growing by over 25% annually. This creates long-term procurement contracts and recurring upgrade cycles for manufacturers.

Supply chain complexity poses a persistent challenge for the Gaming Monitor and Display Technologies Market. Advanced panels rely on multi-country supply networks for semiconductors, substrates, and rare materials. Disruptions have increased lead times by 20–30%, while logistics costs rose by over 18% in recent years. Ensuring consistent quality across high-resolution panels also increases rejection rates, impacting margins and delivery schedules.

Expansion of Ultra-High Refresh Rate Displays: Gaming monitors with refresh rates above 240 Hz now account for nearly 29% of premium unit shipments, improving motion clarity by over 45% compared to 144 Hz panels.

Rapid Adoption of OLED and Mini-LED Panels: OLED and Mini-LED gaming displays deliver contrast improvements exceeding 1,000,000:1, with adoption increasing by 38% year-over-year in high-end segments.

AI-Driven Display Optimization: AI-based calibration tools are reducing color variance by 32% and lowering defect rates by 24% during mass production.

Growth of Cross-Platform Gaming Setups: Over 52% of gamers now use multi-device setups, increasing demand for adaptive sync and connectivity features supporting PCs, consoles, and cloud gaming platforms.

The Gaming Monitor and Display Technologies Market is segmented based on type, application, and end-user insights, reflecting diverse performance requirements, usage contexts, and purchasing behaviors across the gaming ecosystem. By type, the market spans LCD-based gaming monitors, OLED gaming displays, Mini-LED gaming monitors, and emerging display formats such as QD-OLED and Micro-LED. Each type addresses different priorities such as cost efficiency, contrast performance, refresh stability, and energy optimization. By application, demand is distributed across competitive esports gaming, casual and home gaming, content creation and streaming, simulation and training environments, and commercial gaming venues. End-user segmentation highlights strong differentiation between individual consumers, esports organizations, gaming cafés, educational institutions, and enterprise or simulation-focused users. Purchasing decisions across segments are increasingly driven by measurable parameters such as refresh rate thresholds, latency tolerance, screen size preferences, and multi-device compatibility. Together, these segmentation layers reveal a market where performance-centric subsegments coexist with volume-driven consumer adoption, shaping product design, pricing strategies, and innovation priorities.

The Gaming Monitor and Display Technologies Market by type includes LCD gaming monitors, OLED gaming displays, Mini-LED gaming monitors, and emerging advanced display technologies such as QD-OLED and Micro-LED.

LCD gaming monitors currently represent the leading segment with approximately 48% share, supported by mature manufacturing infrastructure, broad price accessibility, and widespread availability of high-refresh-rate variants ranging from 144 Hz to 240 Hz. OLED gaming displays account for roughly 26% of adoption, favored for superior contrast ratios, near-instant pixel response, and high color accuracy, particularly among professional gamers and content creators. However, Mini-LED gaming monitors are the fastest-growing type, expanding at an estimated 18% CAGR, driven by improvements in local dimming zones, peak brightness exceeding 1,500 nits, and reduced burn-in risk compared to OLED. Emerging formats such as QD-OLED and early-stage Micro-LED together contribute a combined 26% share, primarily serving premium and experimental use cases, including ultra-wide and curved gaming setups.

In 2025, a national standards laboratory-backed evaluation demonstrated that Mini-LED gaming monitors used in controlled esports environments reduced halo artifacts by over 35% while maintaining consistent brightness across extended gaming sessions.

By application, the Gaming Monitor and Display Technologies Market is led by competitive and esports gaming, which accounts for approximately 39% of total adoption, driven by stringent performance requirements such as sub-1 ms response times and refresh rates above 240 Hz. Casual and home gaming follows with about 31% share, reflecting broader consumer demand for immersive visuals and multi-purpose monitors that support gaming, streaming, and productivity. Content creation and game streaming represent nearly 18% of usage, where color accuracy above 98% DCI-P3 and high-resolution panels are critical. Simulation, training, and commercial gaming venues collectively contribute a combined 12% share, serving niche but technologically demanding environments. Among applications, cloud gaming and simulator-based gaming environments are growing fastest, supported by an estimated 15% CAGR, as low-latency displays become essential for remote rendering and real-time interaction.

Consumer trends show that over 44% of PC gamers upgraded monitors within the last three years, while more than 36% of console gamers now use displays above 120 Hz, signaling rising performance expectations.

In 2024, a government-supported esports training initiative deployed high-refresh gaming monitors across multiple academies, reporting measurable reaction-time improvements of over 20% among professional trainees.

From an end-user perspective, individual consumers and home gamers form the largest segment, accounting for approximately 46% of total demand, driven by rising PC and console ownership and increased awareness of display performance benefits. Esports teams and professional gamers represent around 24% of adoption, prioritizing ultra-low latency, motion clarity, and tournament-grade reliability. Gaming cafés and commercial gaming centers contribute nearly 16%, particularly in Asia-Pacific markets where shared gaming infrastructure remains prevalent. Educational institutions, simulation centers, and enterprise users collectively hold a combined 14% share, leveraging gaming displays for training, visualization, and immersive learning. The fastest-growing end-user segment is esports organizations and training institutions, expanding at an estimated 17% CAGR, fueled by structured esports programs, sponsorship funding, and formalized athlete development pathways.

Consumer data indicates that over 58% of competitive gamers prefer monitors above 27 inches, while nearly 42% of Gen Z gamers actively seek OLED or Mini-LED displays for enhanced visual immersion.

In 2025, a publicly documented esports federation program reported performance consistency gains of 25% after standardizing gaming monitor specifications across national-level competitions.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15% between 2026 and 2033.

Region-wise performance in the Gaming Monitor and Display Technologies Market reflects differences in consumer maturity, manufacturing depth, esports penetration, and technology adoption intensity. North America leads due to early adoption of high-refresh-rate monitors, strong esports infrastructure, and high disposable income among gamers, with over 72% of PC gamers using displays above 144 Hz. Europe follows with a 27% share, supported by sustainability-led display upgrades and widespread console gaming adoption. Asia-Pacific, holding 25% share, benefits from large-scale manufacturing capacity, accounting for nearly 65% of global gaming display panel output, and rapidly expanding gaming populations. South America and Middle East & Africa together contribute the remaining 10%, driven by improving digital infrastructure, rising youth demographics, and localized gaming content growth. Across regions, panel size preferences, refresh-rate expectations, and price sensitivity vary significantly, shaping localized product strategies.

North America represents approximately 38% of the global Gaming Monitor and Display Technologies Market, making it the largest regional contributor. Demand is driven primarily by PC and console gaming, esports tournaments, game streaming, and content creation industries. More than 64% of competitive gamers in this region prefer monitors with refresh rates of 240 Hz or higher. Government-backed digital infrastructure investments and supportive trade policies for semiconductor and display manufacturing have strengthened supply chains. Technological advancements include widespread adoption of OLED and Mini-LED gaming monitors, with brightness levels exceeding 1,000 nits becoming standard in premium models. Local players such as major U.S.-based gaming hardware manufacturers are actively launching AI-optimized gaming displays with adaptive refresh calibration. Consumer behavior shows higher spending per device, with nearly 42% of buyers upgrading monitors within three years, reflecting a strong replacement cycle.

Europe accounts for around 27% of the Gaming Monitor and Display Technologies Market, with Germany, the UK, and France as the leading contributors. Regulatory frameworks emphasizing energy efficiency and electronic waste reduction are influencing product design, resulting in gaming displays that consume 25–30% less power per operating hour. Adoption of emerging technologies such as Mini-LED and QD-OLED is growing steadily, particularly in Western Europe. European manufacturers are focusing on modular display components to extend product lifecycles. Local display and gaming hardware firms are integrating eco-design principles and recyclable materials exceeding 40% of total device composition. Consumer behavior in Europe reflects high regulatory awareness, with buyers prioritizing certified energy-efficient gaming monitors and preferring mid-to-premium screen sizes between 27–32 inches.

Asia-Pacific ranks as the fastest-growing region and holds nearly 25% of global market share by volume. China, Japan, and South Korea dominate manufacturing, collectively producing over 70% of global gaming display panels, while India and Southeast Asia are emerging as high-consumption markets. Infrastructure expansion, strong electronics supply chains, and dense innovation hubs support rapid product rollout. Regional trends include aggressive adoption of curved and ultra-wide gaming monitors, with over 48% of new gaming setups favoring screen sizes above 30 inches. Local players in South Korea and China are investing heavily in OLED and Mini-LED production lines dedicated to gaming displays. Consumer behavior shows high sensitivity to price-performance balance, with e-commerce accounting for over 55% of gaming monitor sales in the region.

South America contributes approximately 6% of the global Gaming Monitor and Display Technologies Market, led by Brazil and Argentina. Growth is supported by expanding broadband access, increasing console penetration, and a youthful gaming population, with over 60% of gamers under the age of 35. Governments in key countries have introduced import duty adjustments and digital economy incentives to improve access to electronics. Infrastructure upgrades in urban centers have improved availability of high-resolution gaming displays. Local distributors and assemblers are partnering with global brands to offer region-specific gaming monitors optimized for cost and language localization. Consumer behavior in the region shows strong demand for mid-range monitors, particularly those supporting 120–165 Hz refresh rates.

The Middle East & Africa region accounts for around 4% of the global market, with the UAE, Saudi Arabia, and South Africa as key growth centers. Demand is rising due to national digital transformation programs, esports initiatives, and increasing investment in entertainment infrastructure. High-income Gulf countries show strong preference for premium gaming monitors, with over 50% of buyers opting for large-format displays above 32 inches. Governments are supporting technology imports through free-trade zones and favorable customs frameworks. Local gaming and electronics retailers are expanding dedicated gaming zones to boost adoption. Consumer behavior varies widely, with premium demand concentrated in urban hubs while affordability remains a key factor across broader African markets.

United States – 24% Market Share: Strong consumer demand, advanced esports ecosystem, and high adoption of premium gaming displays drive leadership.

China – 21% Market Share: Extensive manufacturing capacity and large domestic gaming population support dominance in the Gaming Monitor and Display Technologies Market.

The Gaming Monitor and Display Technologies Market exhibits a moderately fragmented competitive environment with upwards of 50+ active competitors ranging from global consumer electronics giants to specialized display innovators. Leading market participants collectively command a combined share of approximately 47–55%, underscoring competitive tension between established leaders and agile challengers. Market positioning reflects a clear focus on performance differentiation, ecosystem integration, and premium experience delivery. A key strategic initiative has been broad industry product launches — for example, simultaneous 27-inch 4K OLED 240Hz models by several major brands — which showcase capabilities in high refresh, ultra-low latency, and advanced HDR implementations that appeal to esports and content creators alike. Competitive innovation trends include aggressive OLED and QD-OLED portfolio expansions, breakthroughs in ultra-high refresh technologies above 500 Hz, and proprietary brightness and calibration enhancements that push beyond conventional LCD benchmarks. Partnerships with GPU and VRR technology providers further support seamless performance experiences.

Over the past 18 months, strategic movements such as portfolio diversification, rapid cadence of next-gen product rollouts, and regional distribution scale-ups have intensified. Furthermore, mergers and ecosystem alliances continue reshaping competitive dynamics, particularly as emerging display suppliers challenge entrenched LCD dominance with cost-effective OLED and inkjet fabrication strategies. The breadth of competition spans mainstream consumer offerings to professional and creative workspaces, highlighting differentiated value propositions that target distinct end-user clusters.

Acer

MSI

Dell

Alienware

Philips

ViewSonic

AOC

HP

BenQ

Razer

Lenovo

The Gaming Monitor and Display Technologies Market is being transformed by a wave of current and emerging technologies that elevate visual performance, responsiveness, and immersive capabilities. At the forefront is the expansion of OLED and QD-OLED display panels, which deliver superior contrast ratios and pixel response speeds enabling crisp visuals and deep blacks. Panel shipments for OLED gaming monitors have risen significantly, demonstrating high market acceptance and technological momentum. Innovations such as Mini-LED backlight systems have improved local dimming precision and peak brightness performance, narrowing the gap between LED and emissive display technologies.

Ultra-high refresh rate technologies — exceeding 500 Hz in select prototypes — are redefining competitive performance benchmarks, prioritizing rapid response and motion clarity for esports applications. Proprietary brightness optimization technologies, such as intelligent EOTF curve shaping, further enhance HDR performance without compromising panel longevity. In parallel, adaptive synchronization technologies like next-generation G-SYNC are improving motion smoothness and reducing perceived latency, which is critical for professional gamers and simulation users.

Another significant trend involves AI-enhanced display features, including dynamic calibration and immersive audio-visual integrations that adapt visual output to user preferences or environmental lighting conditions. Curved and ultra-wide form factors are gaining traction, offering broader fields of view and deeper immersion across simulation, gaming, and productivity segments. The introduction of inkjet OLED manufacturing processes aims to bring high-end panels to broader segments by reducing fabrication costs. Collectively, these technological advancements are reshaping competitive differentiation, product roadmaps, and user expectations.

• In April 2025, Samsung Electronics reaffirmed its leadership in the gaming monitor space with the No. 1 ranking for the sixth consecutive year, capturing a 21 % share of the global gaming monitor segment and 34.6 % in OLED monitors, underscoring sustained competitive strength. Source: www.samsung.com

• In December 2025, ASUS announced it became the world’s leading OLED monitor brand, with shipments of OLED gaming displays accelerating sharply and innovations such as OLED Care Pro and TrueBlack Glossy enhancements enhancing user experience and panel longevity. Source: www.asus.com

• In 2025, global OLED gaming monitor panel shipments surged by approximately 69 % YoY, significantly outpacing LCD segment growth, reflecting strong demand among gaming enthusiasts and prompting supply shifts at major panel manufacturers. Source: www.trendforce.com

• In early 2026, Gigabyte unveiled a new OLED gaming monitor featuring “HyperNits” brightness-optimization technology which can improve HDR brightness delivery by up to 30 %, signaling continued product innovation in display performance. Source: www.pcgamer.com

The Gaming Monitor and Display Technologies Market Report provides a comprehensive and structured analysis of the landscape, covering multiple dimensions essential for business decision-making and strategic planning. The report’s scope includes segmentation by display type — such as LCD, OLED, Mini-LED, QD-OLED, and emerging advanced formats — examining adoption patterns, panel shipment volumes, and technology deployment instances across global regions. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting regional technology preferences, manufacturing concentrations, and hardware distribution networks. Application segments such as esports, casual gaming, professional content creation, simulation environments, and commercial gaming venues are analyzed to illustrate differentiated demand drivers and usage scenarios.

Furthermore, the report examines end-user clusters, including individual consumers, gaming cafés, enterprise simulation users, and educational institutions, detailing adoption rates and behavior insights. It also assesses technological trends such as ultra-high refresh rates, adaptive sync implementations, AI-driven display enhancements, and form factor innovations like curved, ultra-wide, and portable monitor designs. Competitive dynamics are explored through market share positioning, strategic initiatives by leading players, and new product development trajectories. Additionally, the report identifies potential niche segments — for example, displays optimized for VR interfaces or integrated audio-visual experiences — and assesses infrastructure and supply chain considerations that influence production capacity and technology rollouts. The overall focus is to equip industry professionals with actionable insights, performance benchmarks, and forward-looking perspectives on emerging capabilities within the gaming display ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,390.0 Million |

| Market Revenue (2033) | USD 3,695.2 Million |

| CAGR (2026–2033) | 13% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Samsung Electronics, ASUS, LG Electronics, Acer, MSI, Dell, Alienware, Philips, ViewSonic, AOC, HP, BenQ, Razer, Lenovo |

| Customization & Pricing | Available on Request (10% Customization Free) |