Reports

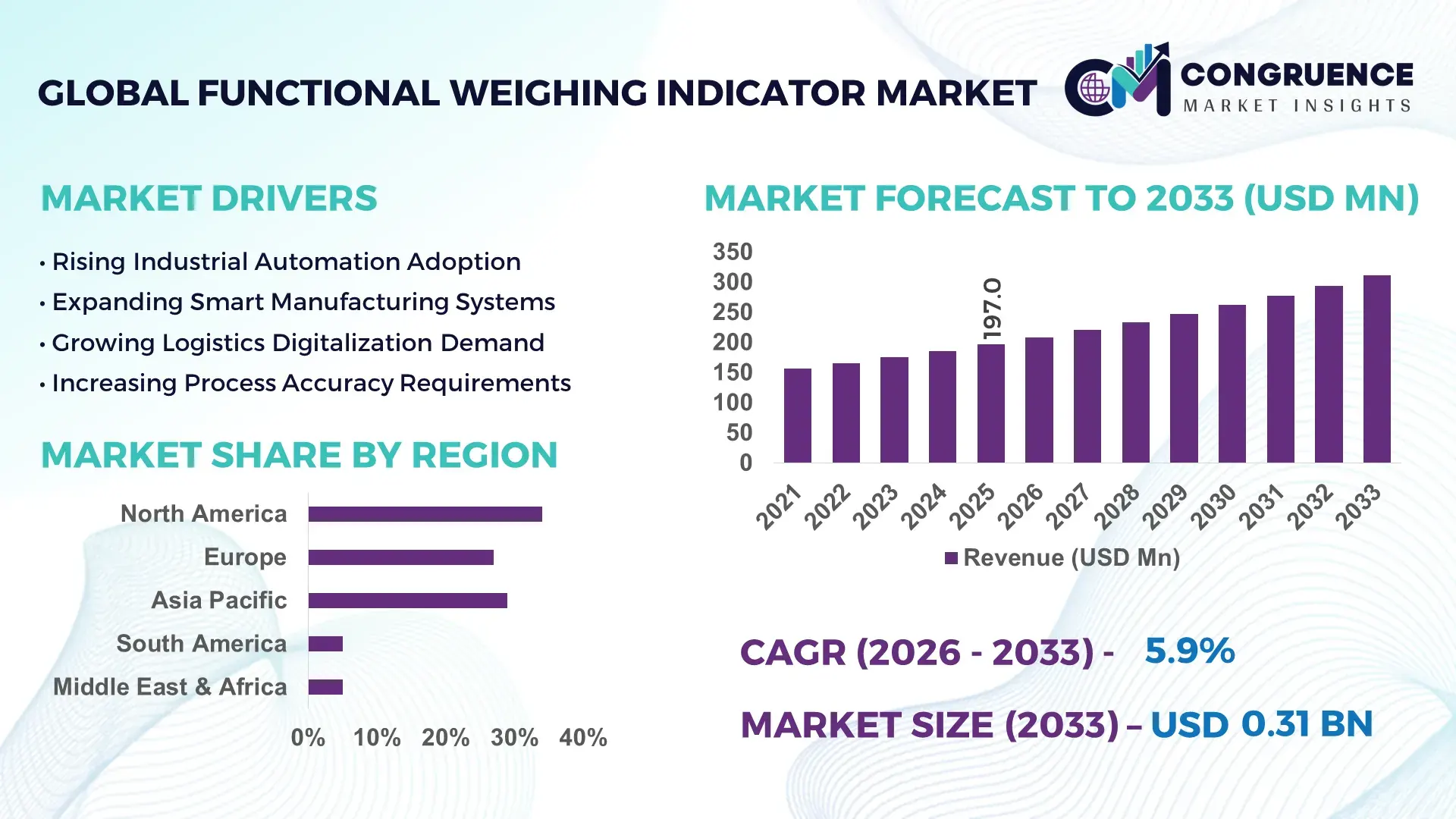

The Global Functional Weighing Indicator Market was valued at USD 197.0 Million in 2025 and is anticipated to reach a value of USD 311.4 Million by 2033 expanding at a CAGR of 5.89% between 2026 and 2033. The market is being driven by the rapid integration of digital load-cell interfaces, Industrial Internet of Things (IIoT) connectivity, and automated process control systems, enabling up to 28% faster weight-data processing and improved operational accuracy across manufacturing and logistics environments. Between 2024 and 2026, industrial digitalization initiatives, supply chain modernization programs, and stricter metrology compliance requirements across major economies have accelerated the replacement of conventional weighing systems with intelligent indicator platforms capable of real-time monitoring and remote diagnostics.

The United States remains the dominant country, accounting for approximately 31% of global market demand in 2025, supported by over 520,000 advanced manufacturing facilities, widespread warehouse automation investments, and strong adoption across food processing, chemicals, pharmaceuticals, and logistics sectors. More than 62% of newly deployed industrial weighing systems in large-scale facilities now incorporate network-enabled functional indicators, compared with less than 45% in several emerging markets. The country also leads in industrial automation spending, with manufacturers increasing digital equipment investments by nearly 18% over the last three years. This level of technology penetration significantly exceeds adoption rates observed across many developing industrial economies.

As industrial operators increasingly prioritize data-driven process optimization, companies capable of delivering highly connected, compliance-ready, and scalable weighing indicator solutions are positioned to secure long-term competitive advantage.

Market Size & Growth: USD 197.0 Million in 2025 reaching USD 311.4 Million by 2033 at 5.89% CAGR, supported by rising industrial automation and smart factory deployment.

Top Growth Drivers: Industrial automation adoption (+28%), warehouse digitization (+24%), and smart manufacturing investments (+21%) are accelerating demand.

Short-Term Forecast: By 2028, advanced weighing systems are expected to improve operational efficiency by 22% while reducing manual calibration requirements by 18%.

Emerging Technologies: AI-assisted diagnostics, IIoT-enabled monitoring, and cloud-based calibration platforms are improving system uptime by over 25%.

Regional Leaders: North America (~USD 72M), Asia-Pacific (~USD 63M), and Europe (~USD 48M) lead through automation upgrades, manufacturing expansion, and compliance-driven modernization.

Consumer/End-User Trends: Nearly 58% of industrial buyers prioritize real-time connectivity and predictive maintenance capabilities during procurement decisions.

Pilot/Case Example: In 2025, a large logistics automation deployment improved weighing throughput by 31% and reduced operational errors by 19%.

Competitive Landscape: Top manufacturers collectively control approximately 42% market share, led by established industrial weighing technology providers.

Regulatory & ESG Impact: Digital traceability requirements have increased smart indicator adoption by 17%, while energy-efficient designs reduce power consumption by 12%.

Investment & Funding: Industrial automation and weighing technology expansion projects surpassed USD 420 Million globally between 2024–2025.

Innovation & Future Outlook: Edge analytics, remote calibration, and autonomous process control are redefining next-generation high-growth weighing infrastructure.

Industrial manufacturing represents approximately 34% of overall demand, followed by logistics and warehousing at 27% and food processing at 19%, highlighting the market’s strong dependence on operational precision and process automation. Recent product innovation focuses on wireless connectivity, cloud-based diagnostics, and multi-platform integration, improving equipment utilization by nearly 25%. Asia-Pacific contributes roughly 32% of global demand growth, while increasing regulatory emphasis on measurement traceability is accelerating digital upgrades. Ongoing supply chain restructuring is encouraging investment in connected weighing ecosystems, positioning intelligent indicators as a core component of future industrial optimization strategies.

Functional weighing indicators are rapidly transforming from standalone measurement devices into mission-critical industrial intelligence platforms, making the market increasingly important for operational competitiveness, manufacturing efficiency, and digital transformation strategies. As industrial facilities accelerate automation initiatives, weighing systems are becoming integrated nodes within broader production, logistics, and quality-control ecosystems.

The market is experiencing pressure from supply chain restructuring, labor shortages, and stricter compliance requirements, forcing organizations to prioritize automated and traceable weighing operations. Advanced IIoT-enabled weighing indicators improve operational efficiency by approximately 27% while reducing maintenance-related costs by nearly 18% compared to legacy standalone systems. This performance advantage is accelerating replacement cycles across industrial sectors.

North America leads in overall deployment volume, while Asia-Pacific leads adoption acceleration with nearly 34% of new manufacturing facilities integrating connected weighing infrastructure. The competitive landscape is transforming as companies shift capital allocation toward smart factory technologies capable of generating actionable production data in real time. Over the next two to three years, predictive diagnostics and remote calibration capabilities are expected to reduce unplanned downtime by approximately 22% while improving asset utilization by nearly 20%. Sustainability has also emerged as a competitive differentiator, with energy-efficient digital indicators lowering power consumption by 12–15%, creating both compliance and operational cost advantages.

A notable example comes from automated distribution centers where integrated weighing platforms improved throughput by 31% and reduced manual verification requirements by 24%. This measurable productivity gain is influencing procurement priorities across logistics-intensive industries. Companies are increasingly expanding software-enabled product portfolios, investing in cloud integration, and developing ecosystem partnerships to strengthen long-term market positioning. Organizations that successfully combine precision measurement, connectivity, and analytics capabilities will secure a durable competitive advantage as industrial operations continue accelerating toward intelligent, data-driven environments.

The Functional Weighing Indicator Market is increasingly shaped by industrial automation, digital process optimization, and rising requirements for measurement accuracy across manufacturing, logistics, food processing, pharmaceuticals, and chemical production. Demand is shifting away from standalone weighing equipment toward intelligent indicator systems capable of data integration, remote monitoring, and predictive maintenance. Nearly 60% of large industrial facilities now prioritize connected measurement infrastructure as part of broader operational modernization programs. Simultaneously, regulatory emphasis on traceability, quality assurance, and process documentation is reshaping procurement priorities. Companies are investing in software-enabled weighing ecosystems that support real-time analytics and enterprise-wide visibility. As automation investments expand globally and supply chains become more data-centric, functional weighing indicators are evolving into strategic operational assets rather than simple measurement tools, redefining how organizations manage productivity, compliance, and process efficiency.

Industrial automation remains the strongest growth engine for the market, driven by the need for higher throughput, process consistency, and real-time operational visibility. More than 62% of newly automated production facilities now incorporate digitally connected weighing infrastructure, while smart manufacturing investments have increased by approximately 24% over recent years. Supply chain restructuring following global logistics disruptions has accelerated warehouse automation projects, creating additional demand for integrated weighing systems. The impact is significant: organizations deploying intelligent indicators report up to 28% faster process execution and nearly 20% lower manual intervention requirements. In response, manufacturers are expanding production capacity, accelerating software integration capabilities, and forming strategic partnerships with automation platform providers. This transition is forcing companies to shift from hardware-centric offerings toward complete data-enabled weighing solutions capable of supporting next-generation industrial operations.

Despite strong momentum, adoption remains constrained by integration complexity and capital expenditure requirements. Approximately 41% of industrial operators identify system interoperability as a major deployment challenge, while implementation costs can exceed conventional weighing systems by 25–35%. Many facilities continue operating legacy equipment that lacks compatibility with modern digital infrastructure, creating migration barriers. Additionally, electronic component sourcing concentration and periodic semiconductor supply disruptions have increased lead times by nearly 18% in certain industrial markets. These constraints directly impact project timelines, scalability, and return-on-investment calculations. To mitigate risks, companies are diversifying supplier networks, adopting modular architectures, and investing in standardized communication protocols. The market is therefore experiencing a strategic tension between the need for advanced functionality and the practical realities of industrial modernization budgets and infrastructure limitations.

The strongest opportunity lies in combining weighing indicators with advanced analytics, cloud connectivity, and predictive maintenance capabilities. Facilities deploying connected measurement ecosystems report efficiency improvements exceeding 23% and maintenance cost reductions approaching 17%. Adoption of remote diagnostics platforms has increased by nearly 30% among large industrial enterprises seeking greater operational resilience. A significant future signal is the convergence of edge computing and industrial AI, enabling real-time process optimization directly at production sites. Beyond obvious productivity gains, these technologies create new recurring-revenue opportunities through software subscriptions, performance monitoring, and service contracts. Companies are aggressively expanding R&D programs, developing ecosystem partnerships, and integrating cloud-native architectures into next-generation products. The organizations that establish scalable digital platforms today are positioning themselves to capture disproportionate value as intelligent industrial infrastructure becomes the new operational standard.

A major challenge involves maintaining measurement accuracy, cybersecurity resilience, and system performance as industrial environments become increasingly connected. Approximately 36% of industrial operators cite data integration and network security concerns as barriers to broader deployment. Furthermore, calibration inconsistencies can reduce operational efficiency by up to 15% when systems operate across multiple production sites. Regulatory requirements are also becoming more demanding, requiring continuous verification and traceability capabilities. These factors create execution risks that extend beyond technology deployment into long-term operational management. Companies must invest heavily in cybersecurity frameworks, advanced calibration technologies, and workforce training programs to sustain performance standards. Strategic partnerships between weighing technology providers, software developers, and industrial automation specialists are becoming essential. Firms that fail to address interoperability, reliability, and security challenges risk losing competitiveness as customers increasingly prioritize fully integrated and resilient industrial ecosystems.

28% Increase in IIoT-Connected Deployments Reshaping Industrial Weighing Operations Industrial facilities are rapidly replacing isolated weighing systems with connected indicators capable of transmitting operational data in real time. Connected deployments have increased by approximately 28%, while remote monitoring utilization has expanded by 21%. Companies are integrating weighing data directly into manufacturing execution systems, improving process visibility and reducing manual intervention. The shift is optimizing production consistency and enabling faster operational decisions. Suppliers are responding through software partnerships and cloud-enabled product launches.

24% Growth in Automated Warehousing Applications Redefining Equipment Requirements Warehouse automation projects have increased demand for high-speed functional weighing indicators integrated with conveyor and sorting systems. Automated facilities report throughput improvements of nearly 24% and weighing-related error reductions approaching 18%. Labor constraints and e-commerce fulfillment requirements are forcing companies to redesign operational workflows. Equipment providers are scaling production and expanding automation-focused product portfolios to support growing deployment requirements across logistics networks.

19% Rise in Compliance-Driven Digital Traceability Initiatives Across Regulated Industries Food processing, pharmaceuticals, and chemicals are increasingly deploying indicators capable of digital recordkeeping and audit-ready reporting. Traceability-focused implementations have increased by 19%, while electronic calibration documentation adoption has grown by 16%. Regulatory oversight and quality assurance requirements are reshaping procurement decisions. Companies are prioritizing platforms that combine precision measurement with automated documentation capabilities, reducing compliance workloads and improving operational transparency.

22% Expansion in Software-Enabled Service Models Transforming Competitive Positioning Manufacturers are increasingly bundling indicators with predictive maintenance, remote diagnostics, and subscription-based monitoring services. Software-enabled service adoption has expanded by approximately 22%, while customer retention rates improved by nearly 14% among providers offering digital support ecosystems. This shift is redefining competitive dynamics, moving value creation beyond hardware sales. Companies are restructuring business models, investing in analytics platforms, and strengthening long-term customer engagement through recurring service offerings.

The Functional Weighing Indicator Market is segmented by type, application, and end-user, with demand increasingly concentrated in digitally connected solutions capable of supporting automation, traceability, and real-time operational monitoring. Digital and programmable indicator platforms collectively account for more than 68% of market demand as industrial facilities modernize production environments. Application demand remains strongest in manufacturing and logistics operations, which together contribute approximately 57% of installations due to their reliance on precision measurement and throughput optimization. End-user demand is shifting toward highly automated industrial environments where data integration, compliance management, and operational visibility are becoming strategic priorities. As organizations pursue productivity improvements and digital transformation objectives, suppliers are increasingly focusing on intelligent indicator platforms, industry-specific software integration, and scalable deployment models that support both current operational requirements and future automation expansion.

Digital Functional Weighing Indicators dominate the market with approximately 42% share, driven by superior connectivity, real-time monitoring capabilities, and seamless integration with industrial automation platforms. Their ability to support remote diagnostics, process control, and centralized data management makes them the preferred choice across advanced manufacturing environments. Programmable Functional Weighing Indicators represent the fastest-growing segment, expanding at an estimated 7.8% adoption growth rate, as industries seek configurable solutions capable of supporting multiple operational workflows without extensive hardware modifications. A direct comparison highlights the market transition: while Digital Functional Weighing Indicators currently lead through widespread deployment and operational reliability, Programmable Functional Weighing Indicators are gaining traction because they offer greater flexibility and customization for evolving production requirements. Analog Functional Weighing Indicators and Panel-Mounted Indicators collectively account for approximately 32% of demand, maintaining relevance in cost-sensitive and legacy industrial environments where infrastructure upgrades remain limited. Demand is clearly shifting toward software-enabled and connected platforms. In response, manufacturers are increasing investments in smart interface development, wireless communication capabilities, and cloud-compatible architectures. The strongest investment opportunities remain concentrated in digital and programmable technologies where industrial automation adoption continues accelerating.

Manufacturing is the leading application segment, accounting for approximately 38% of market demand, reflecting the critical role of weighing indicators in production control, quality assurance, batching, and process optimization. Demand concentration exists because manufacturing environments require continuous measurement accuracy to maintain productivity and regulatory compliance standards. Logistics & Warehousing is the fastest-growing application segment, recording approximately 8.2% adoption growth, driven by warehouse automation, distribution center modernization, and increasing e-commerce fulfillment requirements. Compared with manufacturing, which remains a mature and high-volume application, logistics is experiencing stronger deployment momentum due to rapid digital transformation initiatives. Food Processing, Pharmaceuticals, and Chemical Processing collectively contribute approximately 44% of application demand. These sectors increasingly require traceability, digital documentation, and automated process monitoring capabilities to meet evolving operational and compliance requirements. Companies are responding by deploying integrated weighing ecosystems that connect directly with enterprise resource planning and production management systems. Demand is steadily moving toward applications where data visibility and operational intelligence create measurable business value. Organizations prioritizing automated logistics and digitally connected manufacturing environments are becoming the primary growth engines for advanced weighing indicator deployment.

Industrial Manufacturing remains the largest end-user segment, holding approximately 41% market share, due to high utilization intensity, continuous process monitoring requirements, and extensive automation investments. Large manufacturers depend heavily on weighing indicators for production consistency, quality control, and operational optimization, resulting in sustained demand concentration. Logistics & Distribution represents the fastest-growing end-user category, achieving approximately 8.5% growth in adoption, fueled by warehouse automation, fulfillment center expansion, and increasing parcel-handling volumes. Compared with Industrial Manufacturing, which focuses on production efficiency, logistics operators prioritize throughput speed, inventory visibility, and operational scalability. Food & Beverage, Pharmaceutical, and Chemical companies collectively account for approximately 46% of end-user demand. These industries increasingly favor advanced indicators that support traceability, audit readiness, and digital compliance reporting. Purchasing behavior is evolving toward solutions offering software integration, predictive maintenance capabilities, and long-term operational flexibility. Suppliers are responding through customized product offerings, industry-specific configurations, and strategic partnerships with automation providers. Future demand is expected to shift toward highly automated logistics and regulated industrial environments where operational intelligence delivers a direct competitive advantage.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

North America maintains leadership through advanced industrial automation adoption and strong investment in connected manufacturing infrastructure. Europe accounts for approximately 27% of global demand, supported by regulatory compliance requirements and precision-focused industrial operations. Asia-Pacific holds around 29% market share and is rapidly expanding due to manufacturing growth, infrastructure investment, and digital industrial transformation initiatives. South America contributes approximately 5%, while the Middle East & Africa represents 5% of market demand. Demand remains concentrated in North America, innovation leadership is increasingly visible in Europe, and expansion momentum is strongest in Asia-Pacific. Ongoing supply chain diversification strategies are encouraging manufacturers to strengthen regional deployment capabilities, with companies increasingly prioritizing Asia-Pacific expansion while maintaining North American and European technology leadership.

North America represents approximately 34% of global market demand, supported by advanced manufacturing, logistics automation, and food processing industries. More than 62% of newly automated industrial facilities incorporate digitally connected weighing infrastructure. Regulatory emphasis on operational traceability and production efficiency continues shaping procurement decisions across major industries. Organizations are increasingly deploying cloud-connected weighing indicators capable of supporting predictive maintenance and enterprise-wide monitoring. Recent industrial modernization programs have increased smart measurement investments by nearly 18%, while warehouse automation projects expanded deployment activity by over 21%. Enterprise buyers prioritize long-term integration capabilities over standalone hardware performance. The region remains a strategic investment destination because of its strong technology adoption rates, large industrial base, and continuous automation spending.

Europe accounts for approximately 27% of global market share, supported by strong industrial manufacturing activity across Germany, France, Italy, and the United Kingdom. Regulatory requirements related to measurement accuracy, traceability, and digital documentation continue driving demand. Nearly 56% of industrial equipment upgrades now prioritize digitally connected systems that improve compliance monitoring and reporting capabilities. Sustainability objectives are also influencing purchasing behavior, with energy-efficient measurement solutions reducing operational consumption by approximately 12%. Industrial enterprises increasingly favor quality-focused and compliance-ready technologies over low-cost alternatives. Deployment of integrated weighing systems has expanded by nearly 17% across regulated industries. The region continues forcing innovation through its combination of strict standards, advanced manufacturing practices, and operational efficiency objectives.

Asia-Pacific accounts for approximately 29% of global market demand and ranks as the fastest-expanding regional market. China, Japan, India, and South Korea drive growth through manufacturing expansion, logistics modernization, and industrial digitalization programs. More than 35% of new manufacturing capacity additions globally are concentrated within the region. Enterprises increasingly prefer scalable and cost-efficient weighing solutions that support large-volume production environments. Localized manufacturing and regional supply chain development have reduced deployment costs by nearly 15% compared with imported alternatives. Smart factory investments increased by approximately 24% across major industrial economies. For companies seeking scale, speed, and long-term expansion opportunities, Asia-Pacific remains the most critical region for future market penetration.

South America contributes approximately 5% of global market demand, led primarily by Brazil and Argentina. Growth is supported by food processing, agriculture, mining, and logistics modernization initiatives. However, infrastructure limitations and capital expenditure constraints continue influencing purchasing decisions. Approximately 43% of buyers prioritize cost-effective solutions over premium digital platforms. Despite these challenges, industrial automation deployments increased by nearly 14%, while connected weighing solution adoption rose approximately 11%. Companies are increasingly pursuing localized partnerships and service networks to improve market accessibility. Enterprise buyers remain highly price-sensitive but increasingly recognize the productivity benefits of digital measurement technologies. The region presents attractive expansion potential, although successful market participation requires balancing affordability with technology advancement.

The Middle East & Africa region accounts for approximately 5% of global market demand, supported by infrastructure development, industrial diversification, and modernization programs. Saudi Arabia, the UAE, and South Africa are leading adoption across logistics, manufacturing, and resource-processing industries. Industrial investment initiatives increased deployment activity by nearly 16%, while digital monitoring adoption expanded by approximately 13%. Organizations increasingly favor solutions capable of supporting large-scale industrial projects and operational efficiency targets. Strategic partnerships between technology providers and regional industrial operators are becoming more common. Buyers prioritize reliability, scalability, and long-term service support. The region is emerging as an increasingly strategic market as governments and enterprises continue investing in modernization and industrial transformation programs.

United States – 31% Market Share: Benefits from advanced industrial automation, extensive manufacturing infrastructure, and strong adoption of connected measurement technologies.

China – 22% Market Share: Driven by large-scale manufacturing capacity, expanding smart factory investments, and rapid deployment of industrial digitalization initiatives.

The Functional Weighing Indicator Market is characterized by intense competition between global precision measurement leaders such as Mettler Toledo, Avery Weigh-Tronix, Rice Lake Weighing Systems, Minebea Intec, and A&D Company against regional manufacturers competing on pricing, localization, and faster deployment models. The top five players collectively control approximately 42% of global market share, creating a moderately consolidated structure where technology leadership increasingly outweighs hardware scale alone.

Competition is centered on connectivity, software integration, accuracy, and lifecycle support rather than basic weighing functionality. Smart indicator deployments improve operational efficiency by nearly 27%, while cloud-enabled monitoring reduces maintenance interventions by approximately 18%. As a result, manufacturers are accelerating investments in digital platforms, remote diagnostics, and automation partnerships.

Competitive intensity is shifting toward software-enabled ecosystems, with companies expanding through strategic distribution alliances, industrial automation integrations, and cloud-based service offerings. Vertical integration across sensors, indicators, analytics, and process control platforms is becoming a critical differentiator. The primary barrier to entry remains industrial certification requirements, interoperability demands, and customer preference for proven reliability. Winning in this market increasingly requires connected platforms, industry-specific customization, and deep integration capabilities rather than competing on equipment pricing alone.

Avery Weigh-Tronix

Rice Lake Weighing Systems

Minebea Intec

A&D Company Ltd.

Dini Argeo

Precia Molen

Cardinal Scale Manufacturing Company

B-TEK Scales LLC

Flintec Group AB

Ohaus Corporation

RADWAG Balances and Scales

Giropes SL

Thames Side Sensors Ltd.

Digital connectivity is rapidly becoming the foundation of next-generation functional weighing indicators. More than 58% of newly installed industrial systems now incorporate Ethernet, Modbus, or cloud-enabled communication capabilities, enabling real-time monitoring and centralized process management. Businesses deploying connected weighing infrastructure report operational visibility improvements exceeding 25%, creating measurable productivity advantages across manufacturing and logistics operations.

The strongest technology transition involves the shift from analog indicator architectures to programmable digital platforms. Advanced digital systems improve weighing accuracy and process efficiency by approximately 28% while reducing calibration-related intervention requirements by nearly 19% compared with conventional standalone indicators. These platforms increasingly support predictive diagnostics, remote configuration, and integration with manufacturing execution systems, transforming weighing infrastructure into operational intelligence assets.

Emerging technologies such as Industrial Internet of Things (IIoT) integration, edge analytics, and AI-assisted diagnostics are reshaping competitive positioning. Nearly 34% of large-scale industrial facilities are actively deploying connected measurement ecosystems capable of automated performance monitoring and anomaly detection. Companies with advanced software-enabled platforms benefit from stronger customer retention and recurring service opportunities, while hardware-focused competitors face increasing differentiation pressure.

Between 2026 and 2028, remote calibration technologies, cloud-based asset management, and predictive maintenance solutions are expected to become core deployment requirements. Organizations that accelerate adoption of intelligent weighing ecosystems today will secure stronger operational efficiency, faster decision-making, and long-term competitive resilience as industrial automation continues expanding globally.

August 2025 – Avery Weigh-Tronix launched the ZM223 Weight Indicator featuring Bluetooth, Ethernet, MQTT connectivity, and 16GB onboard storage, enabling real-time cloud integration and remote monitoring across industrial environments. The platform supports multiple weighing applications through programmable workflows, improving operational flexibility and deployment speed. [Cloud Integration Push] Source: www.averyweigh-tronix.com

March 2024 – Rice Lake Weighing Systems expanded its distribution reach through a strategic partnership with Alpha Controls & Instrumentation, strengthening access across Eastern Canada. The collaboration broadened deployment opportunities for automated process control and weighing technologies while accelerating regional customer support capabilities. [Distribution Expansion Move]

September 2025 – Mettler Toledo introduced next-generation POWERCELL GDD digital load-cell technology for vehicle weighing applications, improving diagnostic visibility and installation efficiency. The system enhances weighing accuracy through advanced digital signal processing while reducing field setup complexity for heavy-capacity industrial operations. [Digital Accuracy Upgrade]

February 2025 – Rice Lake Weighing Systems showcased its 1280 Enterprise programmable indicator and iQUBE² diagnostic platform at GEAPS 2024, highlighting predictive monitoring capabilities that identify load-cell irregularities before operational failures occur. The deployment focus strengthens reliability and minimizes unplanned maintenance interruptions. [Predictive Monitoring Shift]

This report delivers comprehensive coverage of the Functional Weighing Indicator Market across product types, applications, end-user industries, regional markets, and technology ecosystems. The analysis evaluates digital indicators, programmable platforms, analog systems, and connected weighing technologies deployed across manufacturing, logistics, food processing, pharmaceuticals, chemicals, and industrial automation environments. Geographic coverage spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing detailed assessment of demand concentration, deployment patterns, and industrial adoption shifts.

The report examines more than 10 major industry participants, multiple application categories, and key operational trends influencing purchasing behavior and technology investment decisions. Approximately 58% of current market demand is linked to connected and digitally integrated weighing systems, while nearly 34% of future deployment momentum is concentrated in advanced automation environments. The study also evaluates emerging technologies including IIoT integration, predictive diagnostics, cloud-based monitoring, and remote calibration platforms.

From a strategic perspective, the report supports investment planning, regional expansion, product positioning, partnership development, and competitive benchmarking. Coverage extends through 2026–2033 directional market evolution, highlighting emerging deployment models, software-enabled service ecosystems, and next-generation industrial measurement technologies that are reshaping competitive dynamics and long-term growth opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 197.0 Million |

| Market Revenue (2033) | USD 311.4 Million |

| CAGR (2026–2033) | 5.89% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Mettler Toledo; Avery Weigh-Tronix; Rice Lake Weighing Systems; Minebea Intec; A&D Company Ltd.; Dini Argeo; Precia Molen; Cardinal Scale Manufacturing Company; B-TEK Scales LLC; Flintec Group AB; Ohaus Corporation; RADWAG Balances and Scales; Giropes SL; Thames Side Sensors Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |