Reports

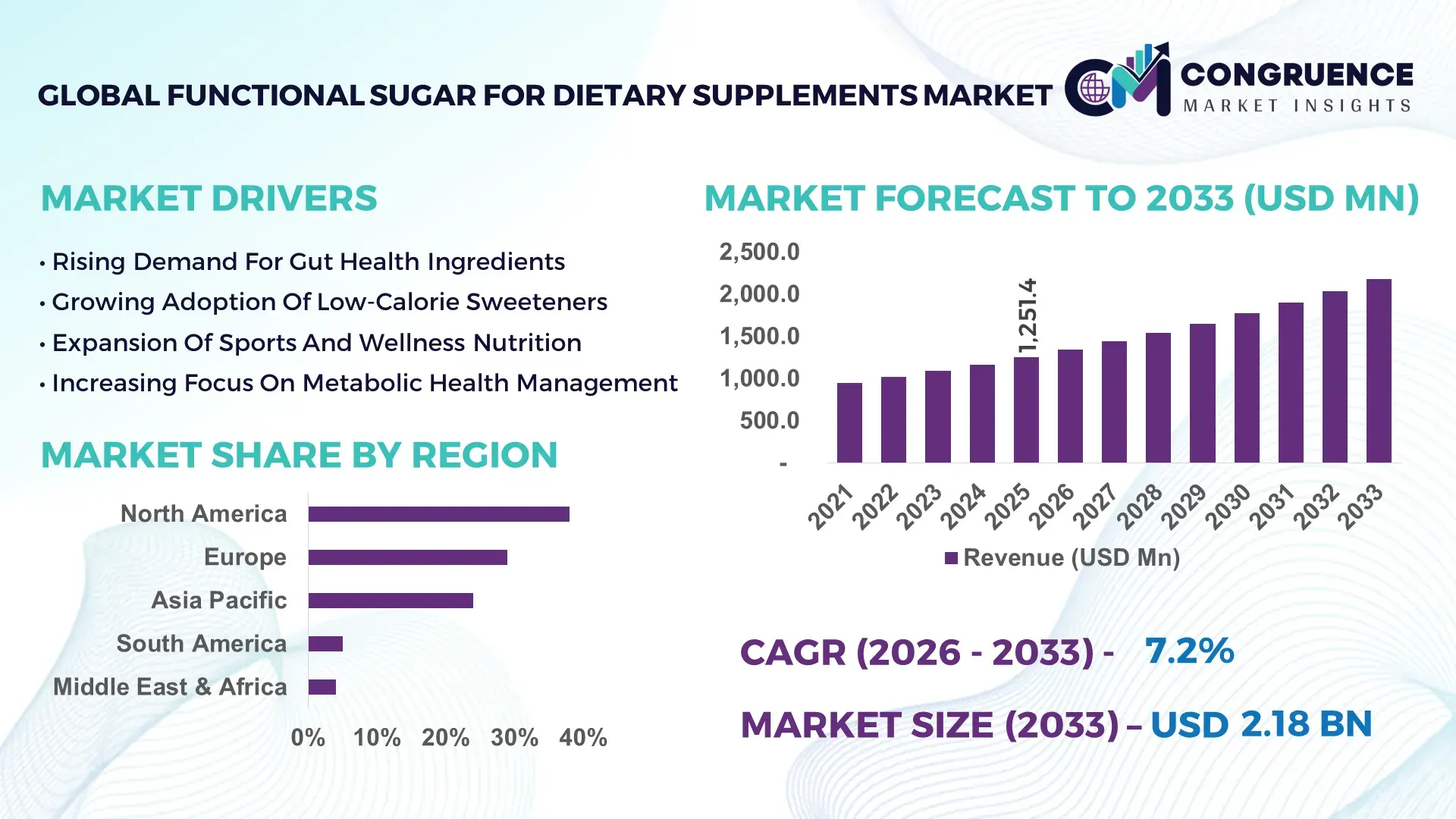

The Global Functional Sugar for Dietary Supplements Market was valued at USD 1,251.4 Million in 2025 and is anticipated to reach a value of USD 2,182.5 Million by 2033 expanding at a CAGR of 7.2% between 2026 and 2033. Growth is driven by rising demand for low-glycemic, prebiotic-enriched sugar alternatives integrated into nutraceutical formulations targeting metabolic health.

The United States leads the functional sugar for dietary supplements market with approximately 34% production share, supported by over 120 active nutraceutical manufacturing facilities and more than USD 280 million in annual R&D investments focused on sugar-reduction technologies. Adoption of prebiotic sugars such as isomaltooligosaccharides and allulose exceeds 41% in supplement formulations, compared to 28% in Germany, reflecting stronger product innovation cycles. Over 63% of functional supplement brands in the U.S. have reformulated at least one product line using low-calorie sugars, reinforcing commercialization depth and supply-chain integration. This dominance signals strong innovation-driven competitive positioning for manufacturers prioritizing functional ingredient portfolios.

Market Size & Growth: USD 1,251.4M in 2025 to USD 2,182.5M by 2033 at 7.2%, driven by metabolic health-focused formulations.

Top Growth Drivers: Low-glycemic adoption (46%), gut-health ingredients (39%), sugar-reduction mandates (31%).

Short-Term Forecast: By 2028, formulation efficiency improves by 28% through enzymatic sugar processing.

Emerging Technologies: Enzyme-based conversion, fermentation-derived rare sugars, precision nutrition integration.

Regional Leaders: North America USD 820M, Europe USD 610M, Asia-Pacific USD 520M by 2033 with localized ingredient sourcing trends.

Consumer Trends: 52% of supplement users prefer sugar-free or low-calorie formulations.

Pilot Example: 2025 pilot improved ingredient bioavailability by 22% using rare sugar blends.

Competitive Landscape: Tate & Lyle leads (~18%), followed by Cargill, Ingredion, ADM, BENEO.

Regulatory & ESG: Sugar reduction policies lowered added sugar content by 19% in formulations.

Investment Trends: USD 780M invested in functional sweetener innovation (2023–2025).

Innovation Outlook: AI-driven formulation and microbiome-linked sugars reshaping product design.

Functional sugar adoption is concentrated in sports nutrition, gut-health supplements, and diabetic-friendly formulations, contributing over 62% of ingredient demand. Innovations in rare sugar fermentation and plant-based oligosaccharides improved formulation stability by 18%. Supply-chain localization and clean-label regulations are accelerating demand across Asia and Europe, setting the stage for advanced ingredient optimization strategies.

The functional sugar for dietary supplements market is becoming strategically critical as manufacturers shift from traditional sweeteners to clinically validated, health-enhancing ingredients. This transition is driven by regulatory pressure on added sugars, rising metabolic disorder cases, and increasing demand for gut-health supplements. Supply-chain restructuring, particularly post-2024 ingredient sourcing disruptions, has pushed companies toward localized fermentation-based sugar production.

Advanced enzymatic conversion technologies deliver 26% higher yield efficiency compared to legacy chemical processing methods, reducing production waste and improving consistency. North America operates at scale with high product commercialization, while Japan leads in innovation with over 48% of supplement manufacturers integrating rare sugars into premium formulations. By 2027, precision nutrition-driven ingredient customization is expected to improve formulation targeting accuracy by 31%, particularly in diabetic and weight-management segments.

In 2025, a leading ingredient producer optimized allulose production using microbial fermentation, reducing energy consumption by 21%. Companies are actively investing in biotech partnerships and expanding production facilities to secure supply continuity. ESG-linked product development, including low-carbon sugar alternatives, is influencing procurement strategies. Functional sugars are evolving into a competitive differentiator, enabling manufacturers to achieve product differentiation, regulatory compliance, and long-term operational resilience.

The market is primarily driven by increasing adoption of low-glycemic functional sugars across dietary supplements. Over 47% of new nutraceutical formulations introduced in 2025 incorporated reduced-calorie or prebiotic sugars. Rising diabetes prevalence in countries such as the United States and India has pushed demand for alternative sweeteners with metabolic benefits. Regulatory sugar-reduction guidelines led to a 22% reformulation rate among supplement brands. Companies are expanding fermentation-based production and investing in enzyme optimization technologies, enabling scalable and cost-efficient manufacturing of functional sugars.

Raw material dependency on corn, chicory root, and starch derivatives exposes the market to price fluctuations, with input costs rising by 18% during recent supply disruptions. Limited processing infrastructure in emerging economies constrains production scalability. Import dependency in regions such as Southeast Asia increases procurement costs by 12–15%. Companies are mitigating risks through vertical integration and regional sourcing strategies, but cost instability continues to impact pricing competitiveness and profit margins.

Microbiome-focused dietary supplements present a major opportunity, with over 43% of consumers seeking gut-health-enhancing products. Functional sugars such as fructooligosaccharides and galactooligosaccharides support beneficial bacteria growth, improving digestive health outcomes by up to 25%. Japan and South Korea are leading in microbiome-based product innovation. Companies are investing in precision fermentation and personalized nutrition platforms to develop targeted ingredient solutions, unlocking high-value product segments.

Functional sugars face classification challenges across regions, with labeling regulations varying significantly. Over 28% of manufacturers report delays in product approvals due to inconsistent definitions of “added sugar” and “functional ingredient.” Compliance costs increased by 14% due to additional testing and documentation requirements. Companies must invest in regulatory expertise and standardized labeling practices to ensure smooth market entry and avoid product recalls.

Fermentation-driven rare sugar production: Adoption increased by 36%, reducing production costs by 18% and improving ingredient purity across supplement formulations.

Clean-label formulation shift: 58% of brands reformulated products to remove artificial sweeteners, increasing demand for natural functional sugars.

Microbiome-linked ingredient innovation: 44% of new supplements incorporate prebiotic sugars, improving gut health positioning and consumer trust.

Localized ingredient sourcing: 33% of manufacturers shifted sourcing to domestic suppliers, reducing logistics costs by 21%.

Strategic dominance of prebiotic sugars

Prebiotic sugars account for approximately 42% of total adoption due to their dual functionality in sweetness and gut-health enhancement. Rare sugars such as allulose and tagatose are the fastest-growing segment, driven by rising demand for low-calorie alternatives and expanding clinical validation. Sugar alcohols and specialty syrups collectively contribute 38%, offering cost-effective alternatives for mass-market supplements. Companies are prioritizing fermentation-derived sugars for scalability and regulatory acceptance, shifting investments toward high-purity production technologies.

In parallel, innovation is accelerating in hybrid sugar blends combining functional and sensory benefits, enabling manufacturers to enhance product differentiation. This trend is reshaping product development pipelines and driving strategic partnerships between ingredient suppliers and supplement manufacturers.

A 2025 industry survey indicated that over 61% of supplement manufacturers prioritized prebiotic sugars in new product development pipelines.

Rising demand in metabolic and gut health supplements

Metabolic health supplements dominate with a 39% share, driven by diabetes management and weight-control products. Gut health applications are the fastest growing, supported by increasing consumer awareness and clinical evidence linking microbiome health to overall wellness. Sports nutrition and immune support applications together contribute 44%, reflecting broader functional ingredient integration. Over 49% of new supplement launches in 2025 featured reduced-sugar or functional sugar positioning, highlighting a clear shift toward health-focused formulations.

Companies are scaling production capacity and investing in formulation R&D to meet demand from specialized applications. Strategic collaborations with healthcare providers and wellness brands are further accelerating adoption.

A 2026 institutional health study found that functional sugar-based supplements improved gut microbiome diversity in 32% of participants.

Dominance of nutraceutical manufacturers

Nutraceutical manufacturers account for approximately 51% of total demand, driven by large-scale supplement production and product diversification strategies. Pharmaceutical companies are the fastest-growing end-user segment, leveraging functional sugars in controlled-release and patient-friendly formulations. Functional food brands and wellness startups collectively represent 34%, expanding market reach through innovative product formats.

Companies are tailoring product portfolios based on end-user requirements, focusing on clean-label compliance and functional benefits. Increasing partnerships between ingredient suppliers and supplement brands are enhancing supply-chain integration and accelerating product innovation cycles.

A 2025 enterprise survey revealed that 46% of nutraceutical companies increased procurement of functional sugars for product reformulation initiatives.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.1% between 2026 and 2033.

High-value nutraceutical integration and formulation innovation

North America leads due to advanced supplement manufacturing and strong demand for low-glycemic ingredients. Over 64% of supplement brands actively incorporate functional sugars into new product lines. Strategic investments in fermentation technology improved ingredient yield efficiency by 23%. Supply-chain localization and regulatory support further strengthen market positioning.

United States Market Outlook: The U.S. drives regional growth with over 70% contribution, supported by high consumer adoption and strong R&D investments. More than 58% of dietary supplement manufacturers utilize functional sugars in reformulated products, reflecting strong innovation and commercialization capabilities.

Regulatory-driven clean-label transition and sustainability focus

Europe accounts for approximately 29% of the market, driven by strict sugar reduction policies and clean-label requirements. Germany, France, and the UK lead adoption, with over 53% of supplement products featuring functional sugars. Sustainable sourcing and regulatory compliance shape product innovation.

Germany Market Outlook: Germany leads with strong industrial processing infrastructure and advanced ingredient development. Over 47% of supplement manufacturers prioritize functional sugar integration, supported by robust regulatory frameworks and consumer preference for natural ingredients.

Scale-driven production and rapid consumer adoption

Asia-Pacific benefits from large-scale production and rising health awareness. China, Japan, and India collectively account for over 68% of regional demand. Local manufacturing expansion improved cost efficiency by 19%, enabling broader product accessibility.

China Market Outlook: China leads regional production with strong fermentation capabilities and growing domestic demand. Over 52% of supplement brands incorporate functional sugars, supported by expanding health-conscious consumer segments.

Emerging demand supported by urban health trends

South America shows growing adoption, particularly in Brazil and Argentina, with increasing urban consumption of dietary supplements. Infrastructure expansion improved supply availability by 16%, supporting market growth.

Brazil Market Outlook: Brazil dominates regional demand due to expanding nutraceutical industry and rising health awareness. Over 44% of supplement brands are integrating functional sugars, reflecting increasing market maturity.

Healthcare expansion and import-driven supply growth

The region is driven by healthcare modernization and rising demand for specialized nutrition. Import reliance remains high, with over 62% of functional sugars sourced externally. Strategic partnerships are improving supply-chain efficiency.

UAE Market Outlook: The UAE leads due to strong healthcare infrastructure and premium supplement demand. Over 48% of high-end supplement products incorporate functional sugars, supported by affluent consumer segments.

Global ingredient leaders such as Tate & Lyle, Cargill, Ingredion, ADM, and BENEO compete directly with regional fermentation specialists and niche biotech firms. The top five players control approximately 61% of the market, competing on formulation performance, purity levels, and supply-chain reliability. Technology-driven players achieve 20–25% higher efficiency in enzymatic processing, while cost-focused suppliers compete through localized production. Strategic moves include partnerships with nutraceutical brands, capacity expansion, and vertical integration into raw material sourcing. The competitive shift is driven by fermentation technology adoption and clean-label demand. Entry barriers include high capital investment and regulatory compliance complexity. Winning requires scalable production, innovation in functional benefits, and strong supply-chain integration.

ADM

BENEO

Roquette Frères

Matsutani Chemical Industry

Tereos Group

Sensus

Cosucra Groupe Warcoing

Nexira

Samyang Corporation

Advanced enzymatic conversion and microbial fermentation are redefining functional sugar production. Enzyme-based processing improves yield efficiency by 26% compared to traditional chemical hydrolysis while reducing by-product waste by 18%. Over 48% of manufacturers have adopted fermentation-based systems for producing rare sugars such as allulose and tagatose, enabling higher purity and consistent quality.

Emerging technologies include precision fermentation and AI-driven formulation platforms, improving ingredient customization accuracy by 31%. Integration with digital supply-chain systems enhances traceability and reduces logistics inefficiencies by 22%. Companies leveraging these technologies gain competitive advantage through faster product development cycles and improved scalability.

Looking ahead to 2026–2028, next-generation bioengineering techniques are expected to further optimize sugar conversion efficiency and reduce energy consumption by 20%. Companies investing in advanced bioprocessing and digital optimization tools are positioned to lead innovation, secure supply stability, and capture high-value market segments.

In March 2025, Tate & Lyle expanded its allulose production capacity by 35%, improving supply availability for low-calorie sweeteners and strengthening its global supply chain position. Source: Tate & Lyle

In July 2024, Cargill introduced a new fermentation-based sweetener solution with 18% improved production efficiency, enhancing cost competitiveness for dietary supplement manufacturers. Source: Cargill

In January 2026, Ingredion launched a next-generation prebiotic sugar ingredient improving digestive health performance by 24%, supporting premium supplement formulations. Source: Ingredion

In October 2024, BENEO expanded its chicory root processing facility, increasing output capacity by 28% to meet rising demand for functional sugars in Europe. Source: Beneo

The report provides comprehensive coverage of functional sugar types, including prebiotic sugars, rare sugars, and sugar alcohols, along with their applications across dietary supplements such as metabolic health, gut health, and sports nutrition. It evaluates adoption patterns across nutraceutical manufacturers, pharmaceutical companies, and functional food producers, covering over 70% of industry demand segments.

Geographic analysis spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, with country-level insights into production, consumption, and innovation trends. The report also examines emerging technologies such as fermentation-based production and precision nutrition integration, offering strategic insights for investment planning, competitive positioning, and long-term market expansion between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 1,251.4 Million |

|

Market Revenue in 2033 |

USD 2,182.5 Million |

|

CAGR (2026 - 2033) |

7.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Tate & Lyle, Cargill, Ingredion, ADM, BENEO, Roquette Frères, Matsutani Chemical Industry, Tereos Group, Sensus, Cosucra Groupe Warcoing, Nexira, Samyang Corporation |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |